The objective of this Standard is to ensure that an entity’s financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties and by transactions and outstanding balances, including commitments, with such parties.

Preamble

Pronouncement

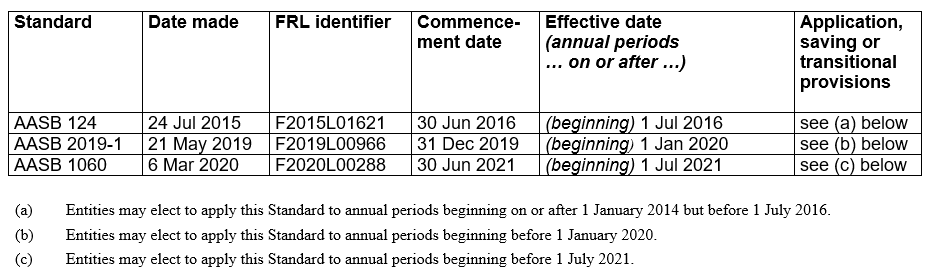

This compiled Standard applies to annual periods beginning on or after 1 July 2021. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 8 June 2021 by the staff of the Australian Accounting Standards Board.

Compilation no. 2

Compilation date: 30 June 2021

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

Australian Accounting Standard AASB 124 Related Party Disclosures (as amended) is set out in paragraphs 1 – Aus29.2, Appendices A and B and the Australian Implementation Guidance. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 124 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IAS 24

AASB 124 Related Party Disclosures as amended incorporates IAS 24 Related Party Disclosures as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IAS 24) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB 124 also comply with IAS 24.

Not-for-profit entities’ compliance with IAS 24 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IAS 24.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Accounting Standard AASB 124

The Australian Accounting Standards Board made Accounting Standard AASB 124 Related Party Disclosures under section 334 of the Corporations Act 2001 on 24 July 2015.

This compiled version of AASB 124 applies to annual periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

1

The objective of this Standard is to ensure that an entity’s financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties and by transactions and outstanding balances, including commitments, with such parties.

AusCF1

AusCF entities are:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting are set out in paragraph Aus1.1 of the Conceptual Framework.

Scope

2

This Standard shall be applied in:

(a) identifying related party relationships and transactions;

(b) identifying outstanding balances, including commitments, between an entity and its related parties;

(c) identifying the circumstances in which disclosure of the items in (a) and (b) is required; and

(d) determining the disclosures to be made about those items.

3

This Standard requires disclosure of related party relationships, transactions and outstanding balances, including commitments, in the consolidated and separate financial statements of a parent or investors with joint control of, or significant influence over, an investee presented in accordance with AASB 10 Consolidated Financial Statements or AASB 127 Separate Financial Statements. This Standard also applies to individual financial statements.

4

Related party transactions and outstanding balances with other entities in a group are disclosed in an entity’s financial statements. Intragroup related party transactions and outstanding balances are eliminated, except for those between an investment entity and its subsidiaries measured at fair value through profit or loss, in the preparation of consolidated financial statements of the group.

Definitions

9

The following terms are used in this Standard with the meanings specified:

9[1]

A related party is a person or entity that is related to the entity that is preparing its financial statements (in this Standard referred to as the ‘reporting entity’).

(a) A person or a close member of that person’s family is related to a reporting entity if that person:

(i) has control or joint control of the reporting entity;

(ii) has significant influence over the reporting entity; or

(iii) is a member of the key management personnel of the reporting entity or of a parent of the reporting entity.

(b) An entity is related to a reporting entity if any of the following conditions applies:

(i) The entity and the reporting entity are members of the same group (which means that each parent, subsidiary and fellow subsidiary is related to the others).

(ii) One entity is an associate or joint venture of the other entity (or an associate or joint venture of a member of a group of which the other entity is a member).

(iii) Both entities are joint ventures of the same third party.

(iv) One entity is a joint venture of a third entity and the other entity is an associate of the third entity.

(v) The entity is a post-employment benefit plan for the benefit of employees of either the reporting entity or an entity related to the reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

(vi) The entity is controlled or jointly controlled by a person identified in (a).

(vii) A person identified in (a)(i) has significant influence over the entity or is a member of the key management personnel of the entity (or of a parent of the entity).

(viii) The entity, or any member of a group of which it is a part, provides key management personnel services to the reporting entity or to the parent of the reporting entity.

9[2]

A related party transaction is a transfer of resources, services or obligations between a reporting entity and a related party, regardless of whether a price is charged.

9[3]

Close members of the family of a person are those family members who may be expected to influence, or be influenced by, that person in their dealings with the entity and include:

(a) that person’s children and spouse or domestic partner;

(b) children of that person’s spouse or domestic partner; and

(c) dependants of that person or that person’s spouse or domestic partner.

9[4]

Compensation includes all employee benefits (as defined in AASB 119 Employee Benefits) including employee benefits to which AASB 2 Share-based Payment applies. Employee benefits are all forms of consideration paid, payable or provided by the entity, or on behalf of the entity, in exchange for services rendered to the entity. It also includes such consideration paid on behalf of a parent of the entity in respect of the entity. Compensation includes:

(a) short-term employee benefits, such as wages, salaries and social security contributions, paid annual leave and paid sick leave, profit-sharing and bonuses (if payable within twelve months of the end of the period) and non-monetary benefits (such as medical care, housing, cars and free or subsidised goods or services) for current employees;

(b) post-employment benefits such as pensions, other retirement benefits, post-employment life insurance and post-employment medical care;

(c) other long-term employee benefits, including long-service leave or sabbatical leave, jubilee or other long-service benefits, long-term disability benefits and, if they are not payable wholly within twelve months after the end of the period, profit-sharing, bonuses and deferred compensation;

(d) termination benefits; and

(e) share-based payment.

9[5]

Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including any director (whether executive or otherwise) of that entity.

9[6]

Government refers to government, government agencies and similar bodies whether local, national or international.

9[7]

A government-related entity is an entity that is controlled, jointly controlled or significantly influenced by a government.

Definitions [further paragraphs]

9[8]

The terms ‘control’ and ‘investment entity’, ‘joint control’ and ‘significant influence’ are defined in AASB 10, AASB 11 Joint Arrangements and AASB 128 Investments in Associates and Joint Ventures respectively and are used in this Standard with the meanings specified in those Australian Accounting Standards.

10

In considering each possible related party relationship, attention is directed to the substance of the relationship and not merely the legal form.

11

In the context of this Standard, the following are not related parties:

(a) two entities simply because they have a director or other member of key management personnel in common or because a member of key management personnel of one entity has significant influence over the other entity.

(b) two joint venturers simply because they share joint control of a joint venture.

(c) (i) providers of finance,

(ii) trade unions,

(iii) public utilities, and

(iv) departments and agencies of a government that does not control, jointly control or significant influence the reporting entity,

simply by virtue of their normal dealings with an entity (even though they may affect the freedom of action of an entity or participate in its decision-making process).

(d) a customer, supplier, franchisor, distributor or general agent with whom an entity transacts a significant volume of business, simply by virtue of the resulting economic dependence.

12

In the definition of a related party, an associate includes subsidiaries of the associate and a joint venture includes subsidiaries of the joint venture. Therefore, for example, an associate’s subsidiary and the investor that has significant influence over the associate are related to each other.

Disclosures

All entities

13

Relationships between a parent and its subsidiaries shall be disclosed irrespective of whether there have been transactions between them. An entity shall disclose the name of its parent and, if different, the ultimate controlling party. If neither the entity’s parent nor the ultimate controlling party produces consolidated financial statements available for public use, the name of the next most senior parent that does so shall also be disclosed.

Aus13.1

When any of the parent entities and/or ultimate controlling parties named in accordance with paragraph 13 is incorporated or otherwise constituted outside Australia, an entity shall:

(a) identify which of those entities is incorporated overseas and where; and

(b) disclose the name of the ultimate controlling entity incorporated within Australia.

14

To enable users of financial statements to form a view about the effects of related party relationships on an entity, it is appropriate to disclose the related party relationship when control exists, irrespective of whether there have been transactions between the related parties.

16

Paragraph 13 refers to the next most senior parent. This is the first parent in the group above the immediate parent that produces consolidated financial statements available for public use.

17

An entity shall disclose key management personnel compensation in total and for each of the following categories:

(a) short-term employee benefits;

(b) post-employment benefits;

(c) other long-term benefits;

(d) termination benefits; and

(e) share-based payment.

17A

If an entity obtains key management personnel services from another entity (the ‘management entity’), the entity is not required to apply the requirements in paragraph 17 to the compensation paid or payable by the management entity to the management entity’s employees or directors.

18

If an entity has had related party transactions during the periods covered by the financial statements, it shall disclose the nature of the related party relationship as well as information about those transactions and outstanding balances, including commitments, necessary for users to understand the potential effect of the relationship on the financial statements. These disclosure requirements are in addition to those in paragraph 17. At a minimum, disclosures shall include:

(a) the amount of the transactions;

(b) the amount of outstanding balances, including commitments, and:

(i) their terms and conditions, including whether they are secured, and the nature of the consideration to be provided in settlement; and

(ii) details of any guarantees given or received;

(c) provisions for doubtful debts related to the amount of outstanding balances; and

(d) the expense recognised during the period in respect of bad or doubtful debts due from related parties.

18A

Amounts incurred by the entity for the provision of key management personnel services that are provided by a separate management entity shall be disclosed.

19

The disclosures required by paragraph 18 shall be made separately for each of the following categories:

(a) the parent;

(b) entities with joint control of, or significant influence over, the entity;

(c) subsidiaries;

(d) associates;

(e) joint ventures in which the entity is a joint venturer;

(f) key management personnel of the entity or its parent; and

(g) other related parties.

20

The classification of amounts payable to, and receivable from, related parties in the different categories as required in paragraph 19 is an extension of the disclosure requirement in AASB 101 Presentation of Financial Statements for information to be presented either in the statement of financial position or in the notes. The categories are extended to provide a more comprehensive analysis of related party balances and apply to related party transactions.

21

The following are examples of transactions that are disclosed if they are with a related party:

(a) purchases or sales of goods (finished or unfinished);

(b) purchases or sales of property and other assets;

(c) rendering or receiving of services;

(d) leases;

(e) transfers of research and development;

(f) transfers under licence agreements;

(g) transfers under finance arrangements (including loans and equity contributions in cash or in kind);

(h) provision of guarantees or collateral;

(i) commitments to do something if a particular event occurs or does not occur in the future, including executory contracts[1] (recognised and unrecognised); and

(j) settlement of liabilities on behalf of the entity or by the entity on behalf of that related party.

22

Participation by a parent or subsidiary in a defined benefit plan that shares risks between group entities is a transaction between related parties (see paragraph 42 of AASB 119).

23

Disclosures that related party transactions were made on terms equivalent to those that prevail in arm’s length transactions are made only if such terms can be substantiated.

24

Items of a similar nature may be disclosed in aggregate except when separate disclosure is necessary for an understanding of the effects of related party transactions on the financial statements of the entity.

Government-related entities

25

A reporting entity is exempt from the disclosure requirements of paragraph 18 in relation to related party transactions and outstanding balances, including commitments, with:

(a) a government that has control or joint control of, or significant influence over, the reporting entity; and

(b) another entity that is a related party because the same government has control or joint control of, or significant influence over, both the reporting entity and the other entity.

26

If a reporting entity applies the exemption in paragraph 25, it shall disclose the following about the transactions and related outstanding balances referred to in paragraph 25:

(a) the name of the government and the nature of its relationship with the reporting entity (ie control, joint control or significant influence);

(b) the following information in sufficient detail to enable users of the entity’s financial statements to understand the effect of related party transactions on its financial statements:

(i) the nature and amount of each individually significant transaction; and

(ii) for other transactions that are collectively, but not individually, significant, a qualitative or quantitative indication of their extent. Types of transactions include those listed in paragraph 21.

AASB 137 Provisions, Contingent Liabilities and Contingent Assets defines executory contracts as contracts under which neither party has performed any of its obligations or both parties have partially performed their obligations to an equal extent.

27

In using its judgement to determine the level of detail to be disclosed in accordance with the requirements in paragraph 26(b), the reporting entity shall consider the closeness of the related party relationship and other factors relevant in establishing the level of significance of the transaction such as whether it is:

(a) significant in terms of size;

(b) carried out on non-market terms;

(c) outside normal day-to-day business operations, such as the purchase and sale of businesses;

(d) disclosed to regulatory or supervisory authorities;

(e) reported to senior management;

(f) subject to shareholder approval.

Effective date and transition

28

[Deleted by the AASB]

Aus28.1

An entity shall apply this Standard for annual periods beginning on or after 1 July 2016. Earlier application is permitted for periods beginning on or after 1 January 2014 but before 1 July 2016. If an entity applies this Standard for a period beginning before 1 July 2016, it shall disclose that fact.

Aus28.2

AASB 2015-6 Amendments to Australian Accounting Standards – Extending Related Party Disclosures to Not-for-Profit Public Sector Entities amended the previous version of this Standard as follows: deleted paragraph Aus1.3, amended paragraph Aus9.1 and added the Australian Implementation Guidance for Not-for-Profit Public Sector Entities. An entity shall apply those amendments for annual periods beginning on or after 1 July 2016. Earlier application is permitted. Those amendments shall be applied prospectively as at the beginning of the annual period in which this Standard is initially applied. For example, a not-for-profit public sector entity shall apply this Standard prospectively as at the beginning of the annual period in which this Standard is initially applied.

28A–28B

[Deleted by the AASB]

28C

AASB 2014-1 Amendments to Australian Accounting Standards, issued in June 2014, amended the previous version of this Standard as follows: amended paragraph 9 and added paragraphs 17A and 18A. An entity shall apply that amendment for annual periods beginning on or after 1 July 2014. Earlier application is permitted. If an entity applies that amendment for an earlier period it shall disclose that fact.

Withdrawal of AASB pronouncements

Aus29.2

This Standard repeals AASB 124 Related Party Disclosures issued in December 2009. Despite the repeal, after the time this Standard starts to apply under section 334 of the Corporations Act (either generally or in relation to an individual entity), the repealed Standard continues to apply in relation to any period ending before that time as if the repeal had not occurred.

[Note: When this Standard applies under section 334 of the Corporations Act (either generally or in relation to an individual entity), it supersedes the application of the repealed Standard.]

Appendix A -- Australian defined terms

This appendix is an integral part of AASB 124.

Aus9.1

The following terms are also used in this Standard with the meaning specified.

Aus9.1[1]

Director means:

(a) a person who is a director under the Corporations Act; and

(b) in the case of entities governed by bodies not called a board of directors, a person who, regardless of the name that is given to the position, is appointed to the position of member of the governing body, council, commission or authority.

Aus9.1[2]

Remuneration is compensation as defined in this Standard.

Aus9.1.1

Although the defined term ‘compensation’ is used in this Standard rather than the term ‘remuneration’, both words refer to the same concept and all references in the Corporations Act to the remuneration of directors and executives is taken as referring to compensation as defined and explained in this Standard.

Appendix B -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusB1

This Standard does not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Australian implementation guidance for not-for-profit public sector entities

This guidance is an integral part of AASB 124 and has the same authority as the other parts of the Standard. The guidance applies only to public sector entities. The guidance does not apply to private sector entities or affect their application of AASB 124.

IG1

AASB 124 Related Party Disclosures incorporates International Financial Reporting Standard IAS 24 Related Party Disclosures, issued by the International Accounting Standards Board. Consequently, much of the text of the body of this Standard and the Illustrative Examples is expressed from the perspective of for-profit entities. The AASB has prepared this guidance to explain and illustrate the principles in the Standard to assist application of the Standard by not-for-profit public sector entities, particularly to address circumstances where a for-profit perspective does not readily translate to a not-for-profit public sector perspective. This guidance also assists not-for-profit public sector entities in determining the extent of the information necessary to meet the objective of the Standard. This guidance does not remove the need for judgement to be applied by an entity in complying with the requirements of the Standard.

IG2

This guidance addresses a range of matters affecting not-for-profit public sector entities broadly in the order in which the related paragraphs appear in the body of the Standard. Illustrative examples are provided in the implementation guidance. The examples apply by analogy to types of not-for-profit public sector entities other than those identified in the examples and similar circumstances. It is the facts and circumstances in any case, not simply the type of not-for-profit public sector entity, that need to be assessed in determining the appropriate disclosures that apply.

Identification of key management personnel

IG3

Paragraph 9 of the Standard defines key management personnel as being those persons having the authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including any director (whether executive or otherwise) of the entity. In a public sector context, entities should consider the facts and circumstances, including the terms of the relevant legislative instruments that give rise to the entity, in assessing whether a person is a member of the key management personnel, as defined, of the entity. For example, the facts and circumstances may reflect that not all persons described as ‘senior executive staff’ or ‘Secretary’ or ‘Minister’ may be a member of the key management personnel of the entity. Similarly, in relation to a not-for-profit public sector entity, the facts and circumstances may reflect that a person’s powers do not give rise to a capacity to direct or control the activities of an entity, where the powers are only ceremonial or procedural in substance.

IG4

Normally, the determination of key management personnel is similar for entities in the public sector and the private sector. However, ministerial-type roles do not normally arise in a private sector context. A Minister would be a member of the key management personnel of an entity that is within the Minister’s portfolio if the Minister has the “authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly”. In some entities or jurisdictions, the responsible Minister may not, in substance, have such authority and responsibility over the activities of the entity, and consequently would not meet the definition of key management personnel.

IG5

A Minister may be a member of the key management personnel of an entity where the Minister’s role and responsibilities result in the Minister forming part of the group of persons tasked with determining the direction of the entity. It would be uncommon for a Minister to be a member of the key management personnel of an entity that is within their portfolio where the entity is not otherwise controlled by the government, as the government’s powers and functions (executed by the Minister) in relation to that entity would have formed part of the government’s assessment of whether it controls the entity. Whether a Minister is a member of the key management personnel of an entity controlled by the government will depend on the facts and circumstances that apply in each instance, as the determination of the key management personnel of an entity is made on an entity by entity basis. Accordingly, a member of the key management personnel of the government is not necessarily also a member of the key management personnel of each entity controlled by that government (see also paragraph IG10).

IG6

Examples 1–6 illustrate application of the definition of key management personnel by not-for-profit public sector entities. These examples do not limit the persons who may be key management personnel of a not-for-profit public sector entity to only those roles described.

Example 1

Minister A is the Australian Minister for Education and Training. Minister A administers their portfolio through the Department of Education and Training (the Department), a controlled entity of the Australian Government. Minister A is accountable to Parliament for the actions of the Department. As part of the portfolio, the Minister is responsible for:

• education policy and programs including schools, vocational, higher education and Indigenous education, but excluding migrant adult education;

• education and training transitions policy and programs;

• science awareness programs in schools;

• training, including apprenticeships and training services;

• policy, co-ordination and support for education exports and services; and

• income support policies and programs for students and apprentices.

Minister B is the Assistant Minister for Education and Training. Assistant Ministers are appointed to assist Ministers in prioritising work, to provide a training experience for future Ministers, to facilitate public access to the Ministers and to enable the bureaucracy to have an ongoing point of contact so that parliamentary correspondence and other parliamentary administrative issues are neither overlooked nor downgraded. As an Assistant Minister, Minister B cannot:

• sit as a Minister in Cabinet;

• attend a meeting of the Executive Council or sign Executive Council Minutes on behalf of the Minister;

• perform any duties in Parliament on behalf of the Minister including answering questions without notice, presenting Ministerial Statements, tabling documents and introducing legislation; or

• appear before a Committee of Parliament on behalf of the Minister.

The Department is responsible for delivering national policies and programs that help Australians access quality early childhood education, school education, higher education, vocational education and training, international education and research. The Department is headed by the Secretary of the Department, who reports to the Australian Minister for Education and Training. At the same time, the Secretary also makes reports to the Assistant Minister for Education and Training. The Secretary of the Department, and two Associate Secretaries and a Deputy Secretary within the Department, operate as the executive management team responsible for the day-to-day delivery of the Department’s services.

Based on the facts and circumstances above, Minister A, the Secretary of the Department, and the two Associate Secretaries and Deputy Secretary are members of the key management personnel of the Department as they have the authority and responsibility for planning, directing and controlling the activities of the entity. Minister A’s role is akin to that of a director in a company, as the Minister discharges their role and responsibilities regarding the Department and is ultimately responsible for the performance of the Department. Minister B is not a member of the key management personnel of the Department as Minister B’s role supports that of the Minister, rather than having any authority and responsibility for planning, directing and controlling the activities of the Department in Minister B’s own right.

Example 2

The Cabinet is a group within the Australian Government (the Commonwealth of Australia) comprising the Prime Minister and a number of senior Ministers. All current Ministers are part of the Executive Council, but not all Ministers are also part of Cabinet. The Governor-General is the chair of the Executive Council.

Minister A, the Australian Minister for Education and Training, is part of Cabinet. Minister B, the Assistant Minister for Education and Training is not part of Cabinet but is part of the Executive Council. Minister D, the Minister for Justice, is also not part of Cabinet but is part of the Executive Council.

Cabinet’s role is to direct the overall government policy and make decisions about national issues. In Cabinet meetings, Ministers also present bills from their government departments. Cabinet examines these bills, and recommends whether bills should proceed to Parliament or changes should be made. A Minister who is not part of Cabinet may be invited to a Cabinet meeting to speak about developments within their portfolio. The Cabinet is accountable to Parliament for the running of the government.

The Executive Council is a constitutional body charged with advising the Governor-General. Legally, members of the Executive Council are chosen by the Governor-General; however, in practice, all current Ministers are part of the Executive Council. The Executive Council acts as a formal ratification body for the decisions of Cabinet, and is required to undertake a range of functions including making proclamations, regulations and ordinances as delegated by various Acts of Parliament, issuing writs for elections, appointing public servants and recommending the appointment of judges.

Section 61 of the Australian Constitution provides that “The executive power of the Commonwealth is vested in the Queen and is exercisable by the Governor-General as the Queen’s representative, and extends to the execution and maintenance of this Constitution, and of the laws of the Commonwealth”. However, the Governor-General is bound by convention to follow the advice of the Executive Council.

Based on the facts and circumstances above, Minister A is a member of the key management personnel of the Australian Government. As part of Cabinet and having regard to Cabinet’s powers, Minister A has the authority and responsibility for planning, directing and controlling the activities of the Australian Government. In addition, as a member of the key management personnel of the Australian Government, Minister A is also a related party of any entities controlled by the Australian Government, consistent with paragraph 9 of the Standard.

Minister B and Minister D are unlikely to be members of the key management personnel of the Australian Government as, although they are part of the Executive Council, they are outside the group of persons responsible for making decisions about the overall running of the government. Further, in substance, neither the members of the Executive Council nor Governor-General have the authority and responsibility for directing and controlling the activities of the Australian Government, and accordingly, are not members of the key management personnel of the Australian Government reporting entity.

Example 3

University XYZ is a not-for-profit public sector entity established under an Act of the State Government. The State Government has determined that it does not control the University.

The governing body of the University is the University Council. The University Council consists of 17 members, five of whom are appointed directly or indirectly by the State Minister for Education. The Chair of the University Council is the Chancellor, who is the formal head of the University. The Chancellor is responsible for ensuring the efficient operation of the University Council in the performance of its governance role, presiding at ceremonial occasions of the University and acting as a signatory to official statutory reports of the University.

The Act specifies that the University Council’s responsibilities, powers and functions include:

• approving the mission, strategic direction and annual budget and business plan of the University;

• establishing policies (‘university statutes and regulations’) relating to the governance and operation of the University, including trusts and endowments, and research, development, consultancy, commercial activities and other services undertaken for commercial organisations or public bodies;

• developing guidelines (if any) concerning the carrying out of commercial activities, finance and property matters, or any other related matter;

• overseeing the management of the property, finances and business affairs of the University, such as risk management across the University, including its commercial activities;

• any other powers and functions conferred on it by or under legislation or any university statute or regulation; and

• the power to do anything else necessary or convenient to be done for or in connection with its powers and functions.

The University Council has a range of powers and functions that it can exercise directly, including the following:

• appointing the Vice-Chancellor, who is the chief executive officer of the University and responsible for the conduct of the University’s affairs in all matters;

• determining the composition of borrowings within the parameters set by the State Government;

• approving the University’s budget for a financial year, incorporating total revenue and the planned revenue sources, including planning the mix between teaching, research and commercial activities, the fees and charges to apply to those activities, and the type and value of government grants desired;

• determining the course mix and target student mix, such as vocational, undergraduate, graduate and executive courses, on-campus or distance learning, and local and international students;

• appointing staff and determining their terms and conditions;

• deciding whether to operate through multiple campuses and how to utilise the University’s infrastructure; and

• making university regulations with respect to any matter relating to the University.

The University Council has delegated the day-to-day management responsibilities and other functions to the University’s executive and other senior staff in order to be able to focus on the broader policy and strategic issues.

The State Minister for Education has the following powers and functions as part of the Minister’s role in the State Government:

• fixing the remuneration and fees to be paid to University Council members who are not full-time staff of the University or holders of statutory office;

• approving (or vetoing) University statutes and guidelines made by the University Council;

• declaring an activity to be a university commercial activity;

• making interim guidelines concerning university commercial activities and finance and property matters – these apply unless replaced by University-submitted guidelines approved by the Minister;

• in conjunction with the State Treasurer, approving the limits and conditions (eg security) for University borrowings;

• approving (or vetoing) the disposal of land that was previously Crown land granted to the University;

• requesting commercial and financial reports from the University;

• referring a university commercial activity or any aspect thereof to the auditor-general for investigation; and

• ensuring that the University complies with certain rights specified in State Government grants provided to the University – some of the grants are required to be repaid if not applied as specified.

Based on the facts and circumstances above, as the State Government has determined that it does not control the University, it is unlikely that the State Minister for Education, as the executor of the State Government’s powers, is a member of the key management personnel of the University, as the evaluation of control includes an assessment of the State Government’s ability to direct the activities that most significantly affect the University’s outcomes. The State Minister’s powers and functions (provided to the position) may restrict the way in which the University operates, but do not of themselves give the State Minister authority and responsibility for the activities of the University.

Rather, based on the facts and circumstances above, it is the University Council (who are akin to a board of directors, with the Chancellor akin to a non-executive chairman) and the University’s executive and other senior staff who have the authority and responsibility for planning, directing and controlling the activities of the University.

The purpose of this Example is to assist entities with the identification of key management personnel of a not-for-profit public sector entity. However, an entity should also consider whether the State Minister for Education, or the State Government, will otherwise meet the definition of a related party of the University (see paragraph 9 of the Standard).

Example 4

The LMN local government (the Council) is a local government entity created under a State’s Local Government Act (the Act) and is subject to a wide range of State Government regulatory powers. The interest of the State Government in the activities of the Council is primarily to ensure that the general objectives set out in the Act are being achieved or furthered. The State Government’s rights in respect of the Council are held primarily by the State Minister for Local Government. These rights allow the State Government (via the State Minister for Local Government) to advise or guide the Council in its activities, or under particular circumstances, to intervene in the activities of the Council.

Minister X is the State Minister for Local Government. The Minister administers their portfolio through the Local Government branch of the State Department of Transport, Planning and Local Infrastructure (the Department). As part of the Minister’s role and responsibilities, Minister X is responsible for:

• the scrutiny of councils, including municipal boundaries;

• making recommendations for allocation of project grants to local governments for projects;

• overseeing tendering processes for council services;

• ensuring the concerns of local governments are communicated to the State Cabinet; and

• the coordination of council community and infrastructure work at a State level.

The Council’s primary objective is to achieve the best outcomes for the local community over the long term. The Council is empowered by the Act to do all things necessary and convenient for the achievement of its objectives and the performance of its functions, subject to any limitations under the Act or any other legislation.

The Council is administered by 10 councillors, who are elected directly by the local community in periodic elections. The Council’s functions include raising revenue to fund its functions and activities, and planning for and providing services and facilities (including infrastructure) for the local community. In carrying out its functions, the Council undertakes a wide range of activities including the imposition of rates and charges upon constituents, and the provision without charge of services such as parks and roads. The day-to-day operations of the Council are carried out by council staff under the direction of its elected councillors.

The State Government has determined that it does not control the Council.

Based on the facts and circumstances above, Minister X is not a member of the key management personnel of the Council, as the Minister’s role does not extend to having the authority and responsibility for planning, directing and controlling the activities of the Council itself. Having concluded that the State Government does not control the council, Minister X’s role as executor of the State Government’s powers and rights over the Council cannot of itself enable Minister X to meet the definition of key management personnel of the Council. Rather, in this example, it is the councillors and senior council staff who have the authority and responsibility for the activities of the Council (similar to a board of directors and senior management of a company).

The purpose of this Example is to assist entities with the identification of key management personnel of a not-for-profit public sector entity. However, an entity should also consider whether Minister X, or the State Government, will otherwise meet the definition of a related party of the Council (see paragraph 9 of the Standard).

Example 5

Minister E, the State Minister for Education, Minister F, the State Minister for Children and Early Childhood, and Minister G, the State Minister for Higher Education and Skills, administer their portfolios wholly through the State Department of Education (the Department), a controlled entity of the State Government.

The day-to-day operations of the Department are managed by an Executive Board comprising the Secretary of the Department and the head of each of the Department’s divisions. The Executive Board is the governance and decision-making body for the Department accountable for the:

• strategic direction and leadership of the Department;

• management of the Department;

• decision-making and risk management;

• monitoring and evaluation of the Department’s activities; and

• compliance and stakeholder management.

The Department reports to the three Ministers, separately or jointly as appropriate to the nature of the Ministers’ portfolio. The Ministers are jointly accountable to Parliament for the actions of the Department.

Based on the facts and circumstances above, Minister E, Minister F and Minister G, and the members of the Executive Board are members of the key management personnel of the Department as they have the authority and responsibility for planning, directing and controlling the activities of the Department. The Ministers’ roles are akin to that of directors in a company, even though each has responsibility only to the extent of their respective portfolios, as they discharge their roles and responsibilities regarding the Department and are ultimately responsible for the performance of the Department.

Example 6

Statutory authority SLA is a statutory authority of the State Government tasked with providing legal information, advice and representation to financially disadvantaged residents of the State. As a statutory authority, SLA was established under its own enabling legislation, which sets out its functions, powers and responsibilities. Its remit is such that it generally operates independently of any governmental direction or influence.

SLA is funded by the State Government to undertake state law matters. The State Government may specify areas to which certain of the funds granted should be allocated. SLA is a controlled entity of the State Government.

The execution and authority for the day-to-day operations of SLA are the responsibility of its executive management team, who report to the Board of SLA. The Board is the statutory authority’s governing body and is responsible for managing SLA and ensuring that its objectives are achieved. The Board is responsible for deciding SLA’s priorities and strategies, leading its policy direction and ensuring its sound and prudent financial management. Board members are appointed by the State Governor in Council, on advice of the State Minister for Justice.

SLA is accountable to the State Government for the delivery of legal assistance services. As a statutory authority, the Board of SLA reports to the State Minister for Justice, who is responsible to Parliament for the oversight of statutory authorities within the Minister’s portfolio.

SLA’s enabling legislation provides that the Board must:

• if asked by the State Minister for Justice, give the Minister a report on any issue relevant to its functions, other than about legal assistance for a particular person; and

• act upon a written direction given by the State Minister for Justice about the performance of SLA’s functions or exercise of its powers, and its policies, priorities or guidelines, including priorities in legal assistance funding. The direction cannot be about giving legal assistance to a particular person.

While SLA generally operates independently of any governmental direction or influence, from time to time, the State Minister for Justice has requested various reports and required SLA to act as directed.

Based on the facts and circumstances above, the Board and executive management team of SLA are members of the key management personnel of the entity, as they ultimately have the authority and responsibility for planning, directing and controlling the activities of the entity. In this fact pattern, the State Minister for Justice is also a member of the key management personnel of SLA, as the powers vested in the Minister’s role also give the Minister authority and responsibility for planning, directing and controlling the activities of the entity, as SLA is required to act in accordance with the Minister’s written directions (which may relate to SLA’s execution of its remit).

The purpose of this Example is to assist entities with the identification of key management personnel of a not-for-profit public sector entity. However, consideration should also be given to whether the State Government is a related party of SLA (see paragraph 9 of the Standard).

Key management personnel compensation

IG7

In the public sector, Ministers are normally compensated through one or more central government agencies or authorities. In relation to not-for-profit public sector entities, the central government agency typically operates as a management entity for the purposes of applying paragraph 17A of the Standard.

IG8

Paragraph 18A of the Standard requires disclosure of amounts incurred by the entity preparing general purpose financial statements for the key management personnel services that are provided by a separate management entity. No disclosure is required to comply with the requirement in paragraph 18A where an entity is not obligated to reimburse the management entity for key management personnel services it has obtained.

Related party transactions

IG9

Paragraph 18 of the Standard requires an entity to disclose information about transactions that have occurred between the entity and its related parties, including transactions between the entity and its key management personnel or key management personnel of the entity’s parent, that is necessary for users to understand the potential effect of the relationship on the financial statements.

IG10

Ministers, councillors and other senior public servants may qualify as a related party of a public sector entity under one or more of the criteria set down in paragraph (a) in the definition of ‘related party’ in AASB 124. For example, a Minister who is a member of the key management personnel of the Commonwealth or State government is, under the definition of ‘related party’, a related party not only of the Commonwealth or State government consolidated entity but also of each controlled entity of that government (see Example 2 in paragraph IG6). In such instances, the Standard requires the controlled government entity to disclose related party transactions with that Minister which are necessary to meet the objective noted in paragraph 1 of the Standard, whether or not the Minister has responsibility for the entity.

IG11

A related party transaction is a transfer of resources, services or obligations between an entity and its related party, regardless of whether a price is charged. In the not-for-profit public sector, many entities are likely to engage frequently with persons who are a related party of that entity in the course of delivering the entity’s public service objectives, including the raising of funds (for example, rates and taxes) to meet those objectives. These related party transactions often occur on terms and conditions no different to those applying to the general public (for example, the Medicare rebate or public school fees). A not-for-profit public sector entity may determine that information about related party transactions occurring during the course of delivering its public service objectives and which occur on no different terms to that of the general public is not material for disclosure in its general purpose financial statements and accordingly need not be disclosed. Guidance relevant to an entity’s assessment of the materiality of a disclosure to its general purpose financial statements is included in AASB 101 Presentation of Financial Statements and AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. The factors described in paragraph 27 of the Standard may also assist an entity in making this determination.

IG12

Examples 7–8 describe different types of related party transactions that may occur between not-for-profit public sector entities and their related parties:

Example 7

Councillor P is a member of the key management personnel of the LMN local government (the Council). The Council’s functions include raising revenue to fund its functions and activities, and planning for and providing services and facilities (including infrastructure) for the local community. In carrying out its functions, the Council undertakes a wide range of activities including the imposition of rates and charges upon constituents, and the provision without charge of services such as parks and roads.

Councillor P is a ratepayer residing within the Council’s constituency. As such, Councillor P takes advantage of the availability of free public access to local parks and libraries. Councillor P also used the swimming pool at the Council’s Recreation Centre twice during the financial year, paying the casual entry fee applicable to the general public each time. The recreation centre has approximately 20,000 visitors each financial year.

All of the transactions described above between the Council and Councillor P are related party transactions of the Council considered for disclosure in the Council’s general purpose financial statements. Based on the facts and circumstances described, the Council may determine that these transactions are unlikely to influence the decisions that users of the Council’s financial statements make having regard to both the extent of the transactions, and that the transactions have occurred between the Council and Councillor P within a public service provider/ taxpayer relationship.

Example 8

Minister Z, the State Minister for Planning, has responsibility for a range of functions and, in certain circumstances, has the power to intervene on matters associated with planning and heritage processes. Minister Z is a member of the key management personnel of State Government H.

Entity MED is a controlled entity of State Government H, and operates within the State Health sector. Entity MED is currently seeking State development approval for a potentially contentious new building.

Around this time, Entity MED enters into a contract with Entity STU, an entity wholly-owned and controlled by a close member of Minister Z’s family for Entity STU to provide cleaning services at various current and future Entity MED locations, including the new building when completed. The cleaning contract was won by Entity STU in an open tender. Minister Z has declared information about the contract to provide cleaning services to Cabinet and it is included as part of the Minister’s Register of Members’ Interests. During the reporting period, Entity STU rendered services of $50,000 to Entity MED. No amounts remain outstanding at Entity STU’s reporting date. Entity MED assesses the cleaning services rendered to be a material component of its total operating expenses.

Entity STU is a related party of Entity MED in accordance with the definition of a related party in paragraph 9 of the Standard. The provision of $50,000 cleaning services by Entity STU to Entity MED described above is a related party transaction of Entity MED as there has been a transfer of services and resources between Entity MED and Entity STU. Based on the facts and circumstances described, management of Entity MED may determine that information about the transaction is material for disclosure in its general purpose financial statements as there has been a transfer of resources occurring other than as a result of a public service provider/ taxpayer relationship between related parties and the amount of the transaction is material to Entity MED.

The provision of $50,000 cleaning services by Entity STU to Entity MED described above is also a related party transaction of State Government H as Minister Z is a member of the key management personnel of State Government H and Entity MED is a controlled entity of State Government H. State Government H should separately assess whether the related party transaction is material for disclosure in the whole-of-government financial statements.

Government-related entities

IG13

Paragraph 25 of the Standard provides a limited exemption from the disclosure requirements of paragraph 18 for government-related entities, subject to the alternative disclosures in paragraph 26 of the Standard. An entity considers, on balance, the range of factors included in paragraph 27, as well as any additional relevant factors, in determining the extent of the disclosure required by paragraph 26(b). In some instances, the presence of a single factor identified in paragraph 27 will not be sufficient to inform the entity of the level of individual or collective significance of the transaction. For example, a requirement of legislation to report on various transactions to Parliament may not of itself inform a not-for-profit public sector entity of the significance of a transaction to itself where the entity’s objective is to carry out such transactions, and consequently, the entity should also have regard to other factors in forming its assessment of the significance of the transaction. In other instances, a single factor may be adequate to establish the extent of the significance of the transaction to the entity.

IG14

Individually significant transactions would normally form a small subset, by number, of the total related party transactions of the entity. Paragraph IE3 in the Illustrative Examples accompanying the Standard provides examples of disclosure to comply with paragraph 26(b).

Illustrative examples

The following examples accompany, but are not part of, AASB 124 Related Party Disclosures. They illustrate:

• the partial exemption for government-related entities; and

• how the definition of a related party would apply in specified circumstances.

In the examples, references to ‘financial statements’ relate to the individual, separate or consolidated financial statements.

Partial exemption for government-related entities

Example 1 – Exemption from disclosure (paragraph 25)

IE1

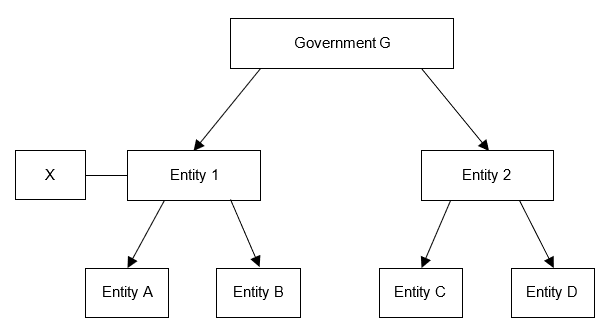

Government G directly or indirectly controls Entities 1 and 2 and Entities A, B, C and D. Person X is a member of the key management personnel of Entity 1.

IE2

For Entity A’s financial statements, the exemption in paragraph 25 applies to:

(a) transactions with Government G; and

(b) transactions with Entities 1 and 2 and Entities B, C and D.

However, that exemption does not apply to transactions with Person X.

Disclosure requirements when exemption applies (paragraph 26)

IE3

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(i) for individually significant transactions could be:

Example of disclosure for individually significant transaction carried out on non-market terms

On 15 January 20X1 Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, sold a 10 hectare piece of land to another government-related utility company for CU5 million. On 31 December 20X0 a plot of land in a similar location, of a similar size and with similar characteristics, was sold for CU3 million.[2] There had not been any appreciation or depreciation of the land in the intervening period. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure for individually significant transaction because of size of transaction

In the year ended December 20X1 Government G provided Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, with a loan equivalent to 50 per cent of its funding requirement, repayable in quarterly instalments over the next five years. Interest is charged on the loan at a rate of 3 per cent, which is comparable to that charged on Entity A’s bank loans.[3] See notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure of collectively significant transactions

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(ii) for collectively significant transactions could be:

Government G, indirectly, owns 75 per cent of Entity A’s outstanding shares. Entity A’s significant transactions with Government G and other entities controlled, jointly controlled or significantly influenced by Government G are [a large portion of its sales of goods and purchases of raw materials] or [about 50 per cent of its sales of goods and about 35 per cent of its purchases of raw materials].

The company also benefits from guarantees by Government G of the company’s bank borrowing. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

IE3

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(i) for individually significant transactions could be:

Example of disclosure for individually significant transaction carried out on non-market terms

On 15 January 20X1 Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, sold a 10 hectare piece of land to another government-related utility company for CU5 million. On 31 December 20X0 a plot of land in a similar location, of a similar size and with similar characteristics, was sold for CU3 million.[2] There had not been any appreciation or depreciation of the land in the intervening period. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure for individually significant transaction because of size of transaction

In the year ended December 20X1 Government G provided Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, with a loan equivalent to 50 per cent of its funding requirement, repayable in quarterly instalments over the next five years. Interest is charged on the loan at a rate of 3 per cent, which is comparable to that charged on Entity A’s bank loans.[3] See notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure of collectively significant transactions

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(ii) for collectively significant transactions could be:

Government G, indirectly, owns 75 per cent of Entity A’s outstanding shares. Entity A’s significant transactions with Government G and other entities controlled, jointly controlled or significantly influenced by Government G are [a large portion of its sales of goods and purchases of raw materials] or [about 50 per cent of its sales of goods and about 35 per cent of its purchases of raw materials].

The company also benefits from guarantees by Government G of the company’s bank borrowing. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

In these examples monetary amounts are denominated in ‘currency units (CU)’.

If the reporting entity had concluded that this transaction constituted government assistance it would have needed to consider the disclosure requirements in AASB 120.

Definition of a related party

The references are to subparagraphs of the definition of a related party in paragraph 9 of AASB 124.

Example 2 – Associates and subsidiaries

IE4

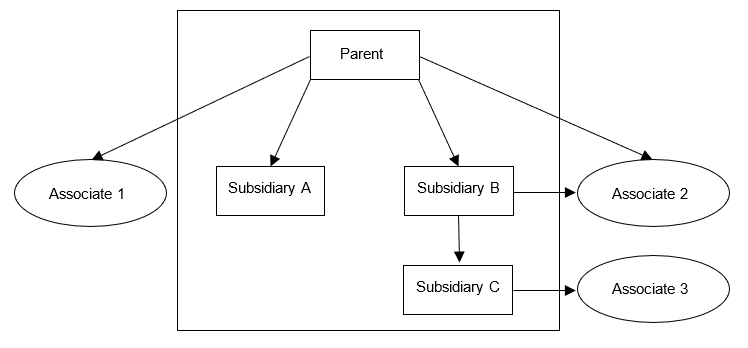

Parent entity has a controlling interest in Subsidiaries A, B and C and has significant influence over Associates 1 and 2. Subsidiary C has significant influence over Associate 3.

IE5

For Parent’s separate financial statements, Subsidiaries A, B and C and Associates 1, 2 and 3 are related parties. [Paragraph 9(b)(i) and (ii)]

IE6

For Subsidiary A’s financial statements, Parent, Subsidiaries B and C and Associates 1, 2 and 3 are related parties. For Subsidiary B’s separate financial statements, Parent, Subsidiaries A and C and Associates 1, 2 and 3 are related parties. For Subsidiary C’s financial statements, Parent, Subsidiaries A and B and Associates 1, 2 and 3 are related parties. [Paragraph 9(b)(i) and (ii)]

IE7

For the financial statements of Associates 1, 2 and 3, Parent and Subsidiaries A, B and C are related parties. Associates 1, 2 and 3 are not related to each other. [Paragraph 9(b)(ii)]

IE8

For Parent’s consolidated financial statements, Associates 1, 2 and 3 are related to the Group. [Paragraph 9(b)(ii)]

Example 3 – Key management personnel

IE9

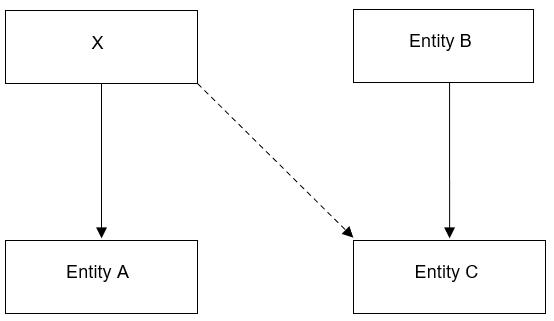

A person, X, has a 100 per cent investment in Entity A and is a member of the key management personnel of Entity C. Entity B has a 100 per cent investment in Entity C.

IE10

For Entity C’s financial statements, Entity A is related to Entity C because X controls Entity A and is a member of the key management personnel of Entity C. [Paragraph 9(b)(vi)–(a)(iii)]

IE11

For Entity C’s financial statements, Entity A is also related to Entity C if X is a member of the key management personnel of Entity B and not of Entity C. [Paragraph 9(b)(vi)–(a)(iii)]

IE12

Furthermore, the outcome described in paragraphs IE10 and IE11 will be the same if X has joint control over Entity A. [Paragraph 9(b)(vi)–(a)(iii)] (If X had only significant influence over Entity A and not control or joint control, then Entities A and C would not be related to each other.)

IE13

For Entity A’s financial statements, Entity C is related to Entity A because X controls A and is a member of Entity C’s key management personnel. [Paragraph 9(b)(vii)–(a)(i)]

IE14

Furthermore, the outcome described in paragraph IE13 will be the same if X has joint control over Entity A. The outcome will also be the same if X is a member of key management personnel of Entity B and not of Entity C. [Paragraph 9(b)(vii)–(a)(i)]

IE15

For Entity B’s consolidated financial statements, Entity A is a related party of the Group if X is a member of key management personnel of the Group. [Paragraph 9(b)(vi)–(a)(iii)]

Example 4 – Person as investor

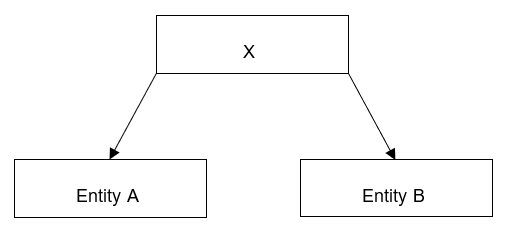

IE16

A person, X, has an investment in Entity A and Entity B.

IE17

For Entity A’s financial statements, if X controls or jointly controls Entity A, Entity B is related to Entity A when X has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vii)–(a)(i)]

IE18

For Entity B’s financial statements, if X controls or jointly controls Entity A, Entity A is related to Entity B when X has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vi)–(a)(ii)]

IE19

If X has significant influence over both Entity A and Entity B, Entities A and B are not related to each other.

Example 5 – Close members of the family holding investments

IE20

A person, X, is the domestic partner of Y. X has an investment in Entity A and Y has an investment in Entity B.

IE21

For Entity A’s financial statements, if X controls or jointly controls Entity A, Entity B is related to Entity A when Y has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vii)–(a)(i)]

IE22

For Entity B’s financial statements, if X controls or jointly controls Entity A, Entity A is related to Entity B when Y has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vi)–(a)(ii)]

IE23

If X has significant influence over Entity A and Y has significant influence over Entity B, Entities A and B are not related to each other.

Example 6 – Entity with joint control

IE24

Entity A has both (i) joint control over Entity B and (ii) joint control or significant influence over Entity C.

IE25

For Entity B’s financial statements, Entity C is related to Entity B. [Paragraph 9(b)(iii) and (iv)]

IE26

Similarly, for Entity C’s financial statements, Entity B is related to Entity C. [Paragraph 9(b)(iii) and (iv)]

Compilation details

Accounting Standard AASB 124 Related Party Disclosures (as amended)

Compilation details are not part of AASB 124.

This compiled Standard applies to annual periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 8 June 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 124 (July2015) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments

Deleted IAS 24 text

Deleted IAS 24 text is not part of AASB 124.

28

An entity shall apply this Standard retrospectively for annual periods beginning on or after 1 January 2011. Earlier application is permitted, either of the whole Standard or of the partial exemption in paragraphs 25–27 for government-related entities. If an entity applies either the whole Standard or that partial exemption for a period beginning before 1 January 2011, it shall disclose that fact.

28A

IFRS 10, IFRS 11 Joint Arrangements and IFRS 12, issued in May 2011, amended paragraphs 3, 9, 11(b), 15, 19(b) and (e) and 25. An entity shall apply those amendments when it applies IFRS 10, IFRS 11 and IFRS 12.

28B

Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27), issued in October 2012, amended paragraphs 4 and 9. An entity shall apply those amendments for annual periods beginning on or after 1 January 2014. Earlier application of Investment Entities is permitted. If an entity applies those amendments earlier it shall also apply all amendments included in Investment Entities at the same time.

29

This Standard supersedes IAS 24 Related Party Disclosures (as revised in 2003).

Basis for Conclusions on AASB 2015-6

This Basis for Conclusions accompanies, but is not part of, AASB 124. The Basis for Conclusions was originally published with AASB 2015-6 Amendments to Australian Accounting Standards – Extending Related Party Disclosures to Not-for-Profit Public Sector Entities.

The Basis for Conclusions is provided with this Standard as a linked PDF document. See AASB Extras at right.