The Conceptual Framework describes the objective of, and the concepts for, general purpose financial reporting. The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions relating to providing resources to the entity.

Preamble

Pronouncement

This compiled Conceptual Framework applies to annual periods beginning on or after 1 July 2021. Earlier application is permitted for annual periods beginning before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board.

Obtaining copies of this Conceptual Framework

Compiled versions of Conceptual Frameworks, original Frameworks and amending pronouncements (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This compiled AASB Conceptual Framework contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwelath. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non‑commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non‑commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Comparison with the IASB Conceptual Framework

This AASB Conceptual Framework for Financial Reporting (as amended) incorporates the Conceptual Framework for Financial Reporting as issued and amended by the International Accounting Standards Board (IASB). Australian-specific paragraphs (which are not included in the IASB Conceptual Framework) are identified with the prefix “Aus.”

AASB Conceptual Framework

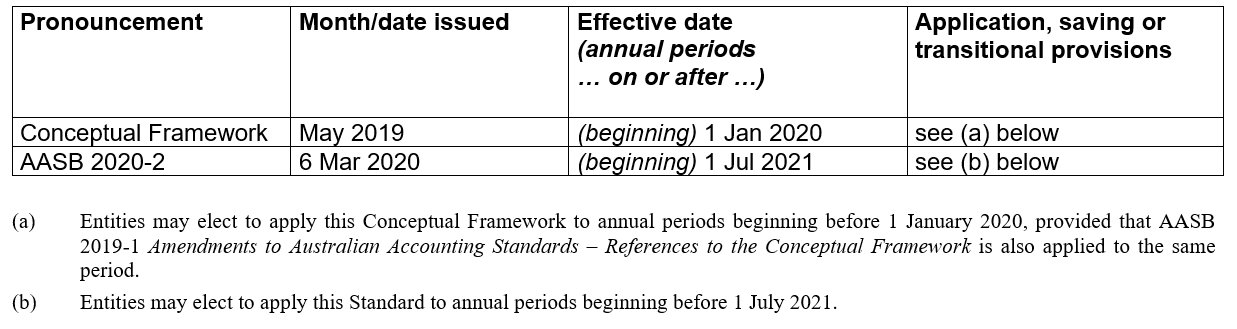

The Australian Accounting Standards Board issued the Conceptual Framework for Financial Reporting in May 2019.

This compiled version of the Conceptual Framework applies to annual periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB pronouncements up to and including 6 March 2020 (see Compilation Details).

Application

Aus1.1

This Conceptual Framework applies to:

(a) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards;

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021; and

(c) other for-profit entities (private sector or public sector) that elect to prepare general purpose financial statements.

Aus1.2

This Conceptual Framework applies to periods beginning on or after 1 July 2021. Earlier application is permitted if at the same time an entity also applies the amendments made by AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework and AASB 2020-2 Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities.

Aus1.3

When applicable, this Conceptual Framework supersedes:

(a) the Framework for the Preparation and Presentation of Financial Statements (July 2004); and

(b) Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity (August 1990);

except as otherwise required by Australian Accounting Standards.

Status and purpose of the Conceptual Framework

SP1.2

The Conceptual Framework is not a Standard. Nothing in the Conceptual Framework overrides any Standard or any requirement in a Standard. This is consistent with the Australian Securities and Investments Commission Act 2001, section 227(1).

SP1.5

Chapter 1—The objective of general purpose financial reporting

Objective, usefulness and limitations of general purpose financial reporting

1.2

The objective of general purpose financial reporting[1] is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions relating to providing resources to the entity.[2] Those decisions involve decisions about:

(a) buying, selling or holding equity and debt instruments;

(b) providing or settling loans and other forms of credit; or

Throughout the Conceptual Framework, the terms ‘financial reports’ and ‘financial reporting’ refer to general purpose financial reports and general purpose financial reporting unless specifically indicated otherwise.

Throughout the Conceptual Framework, the term ‘entity’ refers to the reporting entity unless specifically indicated otherwise.

1.3

The decisions described in paragraph 1.2 depend on the returns that existing and potential investors, lenders and other creditors expect, for example, dividends, principal and interest payments or market price increases. Investors’, lenders’ and other creditors’ expectations about returns depend on their assessment of the amount, timing and uncertainty of (the prospects for) future net cash inflows to the entity and on their assessment of management’s stewardship of the entity’s economic resources. Existing and potential investors, lenders and other creditors need information to help them make those assessments.

1.4

To make the assessments described in paragraph 1.3, existing and potential investors, lenders and other creditors need information about:

(a) the economic resources of the entity, claims against the entity and changes in those resources and claims (see paragraphs 1.12–1.21); and

(b) how efficiently and effectively the entity’s management and governing board[3] have discharged their responsibilities to use the entity’s economic resources (see paragraphs 1.22–1.23).

Throughout the Conceptual Framework, the term ‘management’ refers to management and the governing board of an entity unless specifically indicated otherwise.

1.5

Many existing and potential investors, lenders and other creditors cannot require reporting entities to provide information directly to them and must rely on general purpose financial reports for much of the financial information they need. Consequently, they are the primary users to whom general purpose financial reports are directed.[4]

Throughout the Conceptual Framework, the terms ‘primary users’ and ‘users’ refer to those existing and potential investors, lenders and other creditors who must rely on general purpose financial reports for much of the financial information they need.

Information about a reporting entity’s economic resources, claims against the entity and changes in resources and claims

Changes in economic resources and claims

1.15

Changes in a reporting entity’s economic resources and claims result from that entity’s financial performance (see paragraphs 1.17–1.20) and from other events or transactions such as issuing debt or equity instruments (see paragraph 1.21). To properly assess both the prospects for future net cash inflows to the reporting entity and management’s stewardship of the entity’s economic resources, users need to be able to identify those two types of changes.

1.18

Information about a reporting entity’s financial performance during a period, reflected by changes in its economic resources and claims other than by obtaining additional resources directly from investors and creditors (see paragraph 1.21), is useful in assessing the entity’s past and future ability to generate net cash inflows. That information indicates the extent to which the reporting entity has increased its available economic resources, and thus its capacity for generating net cash inflows through its operations rather than by obtaining additional resources directly from investors and creditors. Information about a reporting entity’s financial performance during a period can also help users to assess management’s stewardship of the entity’s economic resources.

Changes in economic resources and claims not resulting from financial performance

Information about use of the entity’s economic resources

Chapter 2—Qualitative characteristics of useful financial information

2.3

The qualitative characteristics of useful financial information[5] apply to financial information provided in financial statements, as well as to financial information provided in other ways. Cost, which is a pervasive constraint on the reporting entity’s ability to provide useful financial information, applies similarly. However, the considerations in applying the qualitative characteristics and the cost constraint may be different for different types of information. For example, applying them to forward-looking information may be different from applying them to information about existing economic resources and claims and to changes in those resources and claims.

Throughout the Conceptual Framework, the terms ‘qualitative characteristics’ and ‘cost constraint’ refer to the qualitative characteristics of, and the cost constraint on, useful financial information.

Qualitative characteristics of useful financial information

Fundamental qualitative characteristics

2.5

The fundamental qualitative characteristics are relevance and faithful representation.

Materiality

2.11

Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial reports (see paragraph 1.5) make on the basis of those reports, which provide financial information about a specific reporting entity. In other words, materiality is an entity-specific aspect of relevance based on the nature or magnitude, or both, of the items to which the information relates in the context of an individual entity’s financial report. Consequently, the Board cannot specify a uniform quantitative threshold for materiality or predetermine what could be material in a particular situation.

Faithful representation

2.12

Financial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the substance of the phenomena that it purports to represent. In many circumstances, the substance of an economic phenomenon and its legal form are the same. If they are not the same, providing information only about the legal form would not faithfully represent the economic phenomenon (see paragraphs 4.59–4.62).

2.12

Financial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the substance of the phenomena that it purports to represent. In many circumstances, the substance of an economic phenomenon and its legal form are the same. If they are not the same, providing information only about the legal form would not faithfully represent the economic phenomenon (see paragraphs 4.59–4.62).

2.16

Neutrality is supported by the exercise of prudence. Prudence is the exercise of caution when making judgements under conditions of uncertainty. The exercise of prudence means that assets and income are not overstated and liabilities and expenses are not understated.[6] Equally, the exercise of prudence does not allow for the understatement of assets or income or the overstatement of liabilities or expenses. Such misstatements can lead to the overstatement or understatement of income or expenses in future periods.

Assets, liabilities, income and expenses are defined in Table 4.1. They are the elements of financial statements.

2.19

When monetary amounts in financial reports cannot be observed directly and must instead be estimated, measurement uncertainty arises. The use of reasonable estimates is an essential part of the preparation of financial information and does not undermine the usefulness of the information if the estimates are clearly and accurately described and explained. Even a high level of measurement uncertainty does not necessarily prevent such an estimate from providing useful information (see paragraph 2.22).

Applying the fundamental qualitative characteristics

Applying the enhancing qualitative characteristics

The cost constraint on useful financial reporting

Chapter 3—Financial statements and the reporting entity

Financial statements

3.1

Chapters 1 and 2 discuss information provided in general purpose financial reports and Chapters 3–8 discuss information provided in general purpose financial statements, which are a particular form of general purpose financial reports. Financial statements[7] provide information about economic resources of the reporting entity, claims against the entity, and changes in those resources and claims, that meet the definitions of the elements of financial statements (see Table 4.1).

Throughout the Conceptual Framework, the term ‘financial statements’ refers to general purpose financial statements.

Objective and scope of financial statements

3.2

The objective of financial statements is to provide financial information about the reporting entity’s assets, liabilities, equity, income and expenses[8] that is useful to users of financial statements in assessing the prospects for future net cash inflows to the reporting entity and in assessing management’s stewardship of the entity’s economic resources (see paragraph 1.3).

Assets, liabilities, equity, income and expenses are defined in Table 4.1. They are the elements of financial statements.

3.3

(a) in the statement of financial position, by recognising assets, liabilities and equity;

(b) in the statement(s) of financial performance,[9] by recognising income and expenses; and

(c) in other statements and notes, by presenting and disclosing information about:

(i) recognised assets, liabilities, equity, income and expenses (see paragraph 5.1), including information about their nature and about the risks arising from those recognised assets and liabilities;

(ii) assets and liabilities that have not been recognised (see paragraph 5.6), including information about their nature and about the risks arising from them;

(iii) cash flows;

(iv) contributions from holders of equity claims and distributions to them; and

The Conceptual Framework does not specify whether the statement(s) of financial performance comprise(s) a single statement or two statements.

Reporting period

3.4

3.7

Financial statements include information about transactions and other events that have occurred after the end of the reporting period if providing that information is necessary to meet the objective of financial statements (see paragraph 3.2).

Perspective adopted in financial statements

3.11

Sometimes one entity (parent) has control over another entity (subsidiary). If a reporting entity comprises both the parent and its subsidiaries, the reporting entity’s financial statements are referred to as ‘consolidated financial statements’ (see paragraphs 3.15–3.16). If a reporting entity is the parent alone, the reporting entity’s financial statements are referred to as ‘unconsolidated financial statements’ (see paragraphs 3.17–3.18).

3.14

3.17

Chapter 4—The elements of financial statements

Introduction

4.1

The elements of financial statements defined in the Conceptual Framework are:

(a) assets, liabilities and equity, which relate to a reporting entity’s financial position; and

(b) income and expenses, which relate to a reporting entity’s financial performance.

4.2

Table 4.1—The elements of financial statements

|

Item discussed in Chapter 1 |

Element |

Definition or description |

|

Economic resource |

Asset |

A present economic resource controlled by the entity as a result of past events. |

|

An economic resource is a right that has the potential to produce economic benefits. |

||

|

Claim |

Liability |

A present obligation of the entity to transfer an economic resource as a result of past events. |

|

Equity |

The residual interest in the assets of the entity after deducting all its liabilities. |

|

|

Changes in economic resources and claims, reflecting financial performance |

Income |

Increases in assets, or decreases in liabilities, that result in increases in equity, other than those relating to contributions from holders of equity claims. |

|

Expenses |

Decreases in assets, or increases in liabilities, that result in decreases in equity, other than those relating to distributions to holders of equity claims. |

|

|

Other changes in economic resources and claims |

– |

Contributions from holders of equity claims, and distributions to them. |

|

– |

Exchanges of assets or liabilities that do not result in increases or decreases in equity. |

Definition of an asset

4.5

This section discusses three aspects of those definitions:

(a) right (see paragraphs 4.6–4.13);

(b) potential to produce economic benefits (see paragraphs 4.14–4.18); and

(c) control (see paragraphs 4.19–4.25).

Right

4.6

Rights that have the potential to produce economic benefits take many forms, including:

(a) rights that correspond to an obligation of another party (see paragraph 4.39), for example:

(ii) rights to receive goods or services.

(iv) rights to benefit from an obligation of another party to transfer an economic resource if a specified uncertain future event occurs (see paragraph 4.37).

(b) rights that do not correspond to an obligation of another party, for example:

(i) rights over physical objects, such as property, plant and equipment or inventories. Examples of such rights are a right to use a physical object or a right to benefit from the residual value of a leased object.

4.7

(a) by acquiring or creating know-how that is not in the public domain (see paragraph 4.22); or

(b) through an obligation of another party that arises because that other party has no practical ability to act in a manner inconsistent with its customary practices, published policies or specific statements (see paragraph 4.31).

4.9

Not all of an entity’s rights are assets of that entity—to be assets of the entity, the rights must both have the potential to produce for the entity economic benefits beyond the economic benefits available to all other parties (see paragraphs 4.14–4.18) and be controlled by the entity (see paragraphs 4.19–4.25). For example, rights available to all parties without significant cost—for instance, rights of access to public goods, such as public rights of way over land, or know-how that is in the public domain—are typically not assets for the entities that hold them.

4.10

An entity cannot have a right to obtain economic benefits from itself. Hence:

(a) debt instruments or equity instruments issued by the entity and repurchased and held by it—for example, treasury shares—are not economic resources of that entity; and

(b) if a reporting entity comprises more than one legal entity, debt instruments or equity instruments issued by one of those legal entities and held by another of those legal entities are not economic resources of the reporting entity.

4.11

In principle, each of an entity’s rights is a separate asset. However, for accounting purposes, related rights are often treated as a single unit of account that is a single asset (see paragraphs 4.48–4.55). For example, legal ownership of a physical object may give rise to several rights, including:

(a) the right to use the object;

(b) the right to sell rights over the object;

(c) the right to pledge rights over the object; and

4.13

In some cases, it is uncertain whether a right exists. For example, an entity and another party might dispute whether the entity has a right to receive an economic resource from that other party. Until that existence uncertainty is resolved—for example, by a court ruling—it is uncertain whether the entity has a right and, consequently, whether an asset exists. (Paragraph 5.14 discusses recognition of assets whose existence is uncertain.)

Potential to produce economic benefits

4.15

A right can meet the definition of an economic resource, and hence can be an asset, even if the probability that it will produce economic benefits is low. Nevertheless, that low probability might affect decisions about what information to provide about the asset and how to provide that information, including decisions about whether the asset is recognised (see paragraphs 5.15–5.17) and how it is measured.

4.16

(a) receive contractual cash flows or another economic resource;

(b) exchange economic resources with another party on favourable terms;

(c) produce cash inflows or avoid cash outflows by, for example:

(ii) using the economic resource to enhance the value of other economic resources; or

(iii) leasing the economic resource to another party;

(d) receive cash or other economic resources by selling the economic resource; or

(e) extinguish liabilities by transferring the economic resource.

Definition of a liability

4.27

For a liability to exist, three criteria must all be satisfied:

(a) the entity has an obligation (see paragraphs 4.28–4.35);

(b) the obligation is to transfer an economic resource (see paragraphs 4.36–4.41); and

(c) the obligation is a present obligation that exists as a result of past events (see paragraphs 4.42–4.47).

4.31

Many obligations are established by contract, legislation or similar means and are legally enforceable by the party (or parties) to whom they are owed. Obligations can also arise, however, from an entity’s customary practices, published policies or specific statements if the entity has no practical ability to act in a manner inconsistent with those practices, policies or statements. The obligation that arises in such situations is sometimes referred to as a ‘constructive obligation’

4.35

In some cases, it is uncertain whether an obligation exists. For example, if another party is seeking compensation for an entity’s alleged act of wrongdoing, it might be uncertain whether the act occurred, whether the entity committed it or how the law applies. Until that existence uncertainty is resolved—for example, by a court ruling—it is uncertain whether the entity has an obligation to the party seeking compensation and, consequently, whether a liability exists. (Paragraph 5.14 discusses recognition of liabilities whose existence is uncertain.)

Transfer of an economic resource

4.38

An obligation can meet the definition of a liability even if the probability of a transfer of an economic resource is low. Nevertheless, that low probability might affect decisions about what information to provide about the liability and how to provide that information, including decisions about whether the liability is recognised (see paragraphs 5.15–5.17) and how it is measured.

4.39

Obligations to transfer an economic resource include, for example:

(b) obligations to deliver goods or provide services.

(c) obligations to exchange economic resources with another party on unfavourable terms. Such obligations include, for example, a forward contract to sell an economic resource on terms that are currently unfavourable or an option that entitles another party to buy an economic resource from the entity.

(d) obligations to transfer an economic resource if a specified uncertain future event occurs.

(e) obligations to issue a financial instrument if that financial instrument will oblige the entity to transfer an economic resource.

4.41

In the situations described in paragraph 4.40, an entity has the obligation to transfer an economic resource until it has settled, transferred or replaced that obligation.

Present obligation as a result of past events

4.45

If new legislation is enacted, a present obligation arises only when, as a consequence of obtaining economic benefits or taking an action to which that legislation applies, an entity will or may have to transfer an economic resource that it would not otherwise have had to transfer. The enactment of legislation is not in itself sufficient to give an entity a present obligation. Similarly, an entity’s customary practice, published policy or specific statement of the type mentioned in paragraph 4.31 gives rise to a present obligation only when, as a consequence of obtaining economic benefits, or taking an action, to which that practice, policy or statement applies, the entity will or may have to transfer an economic resource that it would not otherwise have had to transfer.

4.47

An entity does not yet have a present obligation to transfer an economic resource if it has not yet satisfied the criteria in paragraph 4.43, that is, if it has not yet obtained economic benefits, or taken an action, that would or could require the entity to transfer an economic resource that it would not otherwise have had to transfer. For example, if an entity has entered into a contract to pay an employee a salary in exchange for receiving the employee’s services, the entity does not have a present obligation to pay the salary until it has received the employee’s services. Before then the contract is executory—the entity has a combined right and obligation to exchange future salary for future employee services (see paragraphs 4.56–4.58).

Assets and liabilities

4.50

If an entity transfers part of an asset or part of a liability, the unit of account may change at that time, so that the transferred component and the retained component become separate units of account (see paragraphs 5.26–5.33).

4.51

A unit of account is selected to provide useful information, which implies that:

(a) the information provided about the asset or liability and about any related income and expenses must be relevant. Treating a group of rights and obligations as a single unit of account may provide more relevant information than treating each right or obligation as a separate unit of account if, for example, those rights and obligations:

(i) cannot be or are unlikely to be the subject of separate transactions;

(ii) cannot or are unlikely to expire in different patterns;

(b) the information provided about the asset or liability and about any related income and expenses must faithfully represent the substance of the transaction or other event from which they have arisen. Therefore, it may be necessary to treat rights or obligations arising from different sources as a single unit of account, or to separate the rights or obligations arising from a single source (see paragraph 4.62). Equally, to provide a faithful representation of unrelated rights and obligations, it may be necessary to recognise and measure them separately.

4.53

Sometimes, both rights and obligations arise from the same source. For example, some contracts establish both rights and obligations for each of the parties. If those rights and obligations are interdependent and cannot be separated, they constitute a single inseparable asset or liability and hence form a single unit of account. For example, this is the case with executory contracts (see paragraph 4.57). Conversely, if rights are separable from obligations, it may sometimes be appropriate to group the rights separately from the obligations, resulting in the identification of one or more separate assets and liabilities. In other cases, it may be more appropriate to group separable rights and obligations in a single unit of account treating them as a single asset or a single liability.

4.54

Treating a set of rights and obligations as a single unit of account differs from offsetting assets and liabilities (see paragraph 7.10).

4.55

Possible units of account include:

(a) an individual right or individual obligation;

(c) a subgroup of those rights and/or obligations—for example, a subgroup of rights over an item of property, plant and equipment for which the useful life and pattern of consumption differ from those of the other rights over that item;

(d) a group of rights and/or obligations arising from a portfolio of similar items;

(e) a group of rights and/or obligations arising from a portfolio of dissimilar items—for example, a portfolio of assets and liabilities to be disposed of in a single transaction; and

(f) a risk exposure within a portfolio of items—if a portfolio of items is subject to a common risk, some aspects of the accounting for that portfolio could focus on the aggregate exposure to that risk within the portfolio.

Substance of contractual rights and contractual obligations

4.59

The terms of a contract create rights and obligations for an entity that is a party to that contract. To represent those rights and obligations faithfully, financial statements report their substance (see paragraph 2.12). In some cases, the substance of the rights and obligations is clear from the legal form of the contract. In other cases, the terms of the contract or a group or series of contracts require analysis to identify the substance of the rights and obligations.

4.62

A group or series of contracts may achieve or be designed to achieve an overall commercial effect. To report the substance of such contracts, it may be necessary to treat rights and obligations arising from that group or series of contracts as a single unit of account. For example, if the rights or obligations in one contract merely nullify all the rights or obligations in another contract entered into at the same time with the same counterparty, the combined effect is that the two contracts create no rights or obligations. Conversely, if a single contract creates two or more sets of rights or obligations that could have been created through two or more separate contracts, an entity may need to account for each set as if it arose from separate contracts in order to faithfully represent the rights and obligations (see paragraphs 4.48–4.55).

Definition of equity

4.67

Business activities are often undertaken by entities such as sole proprietorships, partnerships, trusts or various types of government business undertakings. The legal and regulatory frameworks for such entities are often different from frameworks that apply to corporate entities. For example, there may be few, if any, restrictions on the distribution to holders of equity claims against such entities. Nevertheless, the definition of equity in paragraph 4.63 of the Conceptual Framework applies to all reporting entities.

4.72

Different transactions and other events generate income and expenses with different characteristics. Providing information separately about income and expenses with different characteristics can help users of financial statements to understand the entity’s financial performance (see paragraphs 7.14–7.19).

Chapter 5—Recognition and derecognition

The recognition process

5.1

Recognition is the process of capturing for inclusion in the statement of financial position or the statement(s) of financial performance an item that meets the definition of one of the elements of financial statements—an asset, a liability, equity, income or expenses. Recognition involves depicting the item in one of those statements—either alone or in aggregation with other items—in words and by a monetary amount, and including that amount in one or more totals in that statement. The amount at which an asset, a liability or equity is recognised in the statement of financial position is referred to as its ‘carrying amount’.

5.4

(a) the recognition of income occurs at the same time as:

(i) the initial recognition of an asset, or an increase in the carrying amount of an asset; or

(ii) the derecognition of a liability, or a decrease in the carrying amount of a liability.

(b) the recognition of expenses occurs at the same time as:

(i) the initial recognition of a liability, or an increase in the carrying amount of a liability; or

(ii) the derecognition of an asset, or a decrease in the carrying amount of an asset.

5.7

(a) relevant information about the asset or liability and about any resulting income, expenses or changes in equity (see paragraphs 5.12–5.17); and

(b) a faithful representation of the asset or liability and of any resulting income, expenses or changes in equity (see paragraphs 5.18–5.25).

Relevance

5.12

(a) it is uncertain whether an asset or liability exists (see paragraph 5.14); or

(b) an asset or liability exists, but the probability of an inflow or outflow of economic benefits is low (see paragraphs 5.15–5.17).

5.13

The presence of one or both of the factors described in paragraph 5.12 does not lead automatically to a conclusion that the information provided by recognition lacks relevance. Moreover, factors other than those described in paragraph 5.12 may also affect the conclusion. It may be a combination of factors and not any single factor that determines whether recognition provides relevant information.

Existence uncertainty

5.14

Paragraphs 4.13 and 4.35 discuss cases in which it is uncertain whether an asset or liability exists. In some cases, that uncertainty, possibly combined with a low probability of inflows or outflows of economic benefits and an exceptionally wide range of possible outcomes, may mean that the recognition of an asset or liability, necessarily measured at a single amount, would not provide relevant information. Whether or not the asset or liability is recognised, explanatory information about the uncertainties associated with it may need to be provided in the financial statements.

5.14

Paragraphs 4.13 and 4.35 discuss cases in which it is uncertain whether an asset or liability exists. In some cases, that uncertainty, possibly combined with a low probability of inflows or outflows of economic benefits and an exceptionally wide range of possible outcomes, may mean that the recognition of an asset or liability, necessarily measured at a single amount, would not provide relevant information. Whether or not the asset or liability is recognised, explanatory information about the uncertainties associated with it may need to be provided in the financial statements.

Low probability of an inflow or outflow of economic benefits

5.15

An asset or liability can exist even if the probability of an inflow or outflow of economic benefits is low (see paragraphs 4.15 and 4.38).

5.15

An asset or liability can exist even if the probability of an inflow or outflow of economic benefits is low (see paragraphs 4.15 and 4.38).

5.17

Even if the probability of an inflow or outflow of economic benefits is low, recognition of the asset or liability may provide relevant information beyond the information described in paragraph 5.16. Whether that is the case may depend on a variety of factors. For example:

(a) if an asset is acquired or a liability is incurred in an exchange transaction on market terms, its cost generally reflects the probability of an inflow or outflow of economic benefits. Thus, that cost may be relevant information, and is generally readily available. Furthermore, not recognising the asset or liability would result in the recognition of expenses or income at the time of the exchange, which might not be a faithful representation of the transaction (see paragraph 5.25(a)).

Measurement uncertainty

5.19

For an asset or liability to be recognised, it must be measured. In many cases, such measures must be estimated and are therefore subject to measurement uncertainty. As noted in paragraph 2.19, the use of reasonable estimates is an essential part of the preparation of financial information and does not undermine the usefulness of the information if the estimates are clearly and accurately described and explained. Even a high level of measurement uncertainty does not necessarily prevent such an estimate from providing useful information.

5.19

For an asset or liability to be recognised, it must be measured. In many cases, such measures must be estimated and are therefore subject to measurement uncertainty. As noted in paragraph 2.19, the use of reasonable estimates is an essential part of the preparation of financial information and does not undermine the usefulness of the information if the estimates are clearly and accurately described and explained. Even a high level of measurement uncertainty does not necessarily prevent such an estimate from providing useful information.

5.20

5.21

In some of the cases described in paragraph 5.20, the most useful information may be the measure that relies on the highly uncertain estimate, accompanied by a description of the estimate and an explanation of the uncertainties that affect it. This is especially likely to be the case if that measure is the most relevant measure of the asset or liability. In other cases, if that information would not provide a sufficiently faithful representation of the asset or liability and of any resulting income, expenses or changes in equity, the most useful information may be a different measure (accompanied by any necessary descriptions and explanations) that is slightly less relevant but is subject to lower measurement uncertainty.

5.23

Whether or not an asset or liability is recognised, a faithful representation of the asset or liability may need to include explanatory information about the uncertainties associated with the asset or liability’s existence or measurement, or with its outcome—the amount or timing of any inflow or outflow of economic benefits that will ultimately result from it (see paragraphs 6.60–6.62).

5.25

Derecognition

5.26

5.28

The aims described in paragraph 5.27 are normally achieved by:

(c) applying one or more of the following procedures, if that is necessary to achieve one or both of the aims described in paragraph 5.27:

(i) presenting any retained component separately in the statement of financial position;

5.29

(a) if an entity has apparently transferred an asset but retains exposure to significant positive or negative variations in the amount of economic benefits that may be produced by the asset, this sometimes indicates that the entity might continue to control that asset (see paragraph 4.24); or

(b) if an entity has transferred an asset to another party that holds the asset as an agent for the entity, the transferor still controls the asset (see paragraph 4.25).

5.30

In the cases described in paragraph 5.29, derecognition of that asset or liability is not appropriate because it would not achieve either of the two aims described in paragraph 5.27.

5.31

When an entity no longer has a transferred component, derecognition of the transferred component faithfully represents that fact. However, in some of those cases, derecognition may not faithfully represent how much a transaction or other event changed the entity’s assets or liabilities, even when supported by one or more of the procedures described in paragraph 5.28(c). In those cases, derecognition of the transferred component might imply that the entity’s financial position has changed more significantly than it has. This might occur, for example:

5.32

If derecognition is not sufficient to achieve both aims described in paragraph 5.27, even when supported by one or more of the procedures described in paragraph 5.28(c), those two aims might sometimes be achieved by continuing to recognise the transferred component. This has the following consequences:

5.33

(a) if a contract modification only eliminates existing rights or obligations, the discussion in paragraphs 5.26–5.32 is considered in deciding whether to derecognise those rights or obligations;

(b) if a contract modification only adds new rights or obligations, it is necessary to decide whether to treat the added rights or obligations as a separate asset or liability, or as part of the same unit of account as the existing rights and obligations (see paragraphs 4.48–4.55); and

Chapter 6—Measurement

6.3

Measurement bases

Historical cost

6.4

Historical cost measures provide monetary information about assets, liabilities and related income and expenses, using information derived, at least in part, from the price of the transaction or other event that gave rise to them. Unlike current value, historical cost does not reflect changes in values, except to the extent that those changes relate to impairment of an asset or a liability becoming onerous (see paragraphs 6.7(c) and 6.8(b)).

6.6

When an asset is acquired or created, or a liability is incurred or taken on, as a result of an event that is not a transaction on market terms (see paragraph 6.80), it may not be possible to identify a cost, or the cost may not provide relevant information about the asset or liability. In some such cases, a current value of the asset or liability is used as a deemed cost on initial recognition and that deemed cost is then used as a starting point for subsequent measurement at historical cost.

Current value

6.10

Current value measures provide monetary information about assets, liabilities and related income and expenses, using information updated to reflect conditions at the measurement date. Because of the updating, current values of assets and liabilities reflect changes, since the previous measurement date, in estimates of cash flows and other factors reflected in those current values (see paragraphs 6.14–6.15 and 6.20). Unlike historical cost, the current value of an asset or liability is not derived, even in part, from the price of the transaction or other event that gave rise to the asset or liability.

6.11

Current value measurement bases include:

(a) fair value (see paragraphs 6.12–6.16);

(b) value in use for assets and fulfilment value for liabilities (see paragraphs 6.17–6.20); and

(c) current cost (see paragraphs 6.21–6.22).

6.14

In some cases, fair value can be determined directly by observing prices in an active market. In other cases, it is determined indirectly using measurement techniques, for example, cash-flow-based measurement techniques (see paragraphs 6.91–6.95), reflecting all the following factors:

(a) estimates of future cash flows.

6.15

The factors mentioned in paragraphs 6.14(b) and 6.14(d) include the possibility that a counterparty may fail to fulfil its liability to the entity (credit risk), or that the entity may fail to fulfil its liability (own credit risk).

6.20

Value in use and fulfilment value cannot be observed directly and are determined using cash-flow-based measurement techniques (see paragraphs 6.91–6.95). Value in use and fulfilment value reflect the same factors described for fair value in paragraph 6.14, but from an entity-specific perspective rather than from a market-participant perspective.

Information provided by particular measurement bases

6.23

When selecting a measurement basis, it is important to consider the nature of the information that the measurement basis will produce in both the statement of financial position and the statement(s) of financial performance. Table 6.1 summarises that information and paragraphs 6.24–6.42 provide additional discussion.

6.30

Information about the cost of assets sold or consumed, including goods and services consumed immediately (see paragraph 4.8), and about the consideration received, may have predictive value. That information can be used as an input in predicting future margins from the future sale of goods (including goods not currently held by the entity) and services and hence to assess the entity’s prospects for future net cash inflows. To assess an entity’s prospects for future cash flows, users of financial statements often focus on the entity’s prospects for generating future margins over many periods, not just on its prospects for generating margins from goods already held. Income and expenses measured at historical cost may also have confirmatory value because they may provide feedback to users of financial statements about their previous predictions of cash flows or of margins. Information about the cost of assets sold or consumed may also help in an assessment of how efficiently and effectively the entity’s management has discharged its responsibilities to use the entity’s economic resources.

Current value

6.34

A change in the fair value of an asset or liability can result from various factors identified in paragraph 6.14. When those factors have different characteristics, identifying separately income and expenses that result from those factors can provide useful information to users of financial statements (see paragraph 7.14(b)).

Value in use and fulfilment value

Table 6.1—Summary of information provided by particular measurement bases

|

Statement of financial position |

||||

|

|

Historical cost |

Fair value (market-participant assumptions) |

Value in use (entity-specific assumptions)(a) |

Current cost |

|

Carrying amount |

Historical cost (including transaction costs), to the extent unconsumed or uncollected, and recoverable. |

Price that would be received to sell the asset (without deducting transaction costs on disposal). |

Present value of future cash flows from the use of the asset and from its ultimate disposal (after deducting present value of transaction costs on disposal). |

Current cost (including transaction costs), to the extent unconsumed or uncollected, and recoverable. |

|

|

(Includes interest accrued on any financing component.) |

|

|

|

|

Statement(s) of financial performance |

||||

|

Event |

Historical cost |

Fair value (market-participant assumptions) |

Value in use (entity-specific assumptions) |

Current cost |

|

Initial recognition(b) |

— |

Difference between consideration paid and fair value of the asset acquired.(c) |

Difference between consideration paid and value in use of the asset acquired. |

— |

|

|

|

Transaction costs on acquiring the asset. |

Transaction costs on acquiring the asset. |

|

|

Sale or consumption of the asset(d), (e) |

Expenses equal to historical cost of the asset sold or consumed. |

Expenses equal to fair value of the asset sold or consumed. |

Expenses equal to value in use of the asset sold or consumed. |

Expenses equal to current cost of the asset sold or consumed. |

|

|

Income received. |

Income received. |

Income received. |

Income received. |

|

|

(Could be presented gross or net.) |

(Could be presented gross or net.) |

(Could be presented gross or net.) |

(Could be presented gross or net.) |

|

|

Expenses for transaction costs on selling the asset. |

Expenses for transaction costs on selling the asset. |

|

Expenses for transaction costs on selling the asset. |

|

Interest income |

Interest income, at historical rates, updated if the asset bears variable interest. |

Reflected in income and expenses from changes in fair value. |

Reflected in income and expenses from changes in value in use. |

Interest income, at current rates. |

|

|

|

(Could be identified separately.) |

(Could be identified separately.) |

|

|

Impairment |

Expenses arising because historical cost is no longer recoverable. |

Reflected in income and expenses from changes in fair value. |

Reflected in income and expenses from changes in value in use. |

Expenses arising because current cost is no longer recoverable. |

|

|

|

(Could be identified separately.) |

(Could be identified separately.) |

|

|

Value changes |

Not recognised, except to reflect an impairment. |

Reflected in income and expenses from changes in fair value. |

Reflected in income and expenses from changes in value in use. |

Income and expenses reflecting the effect of changes in prices (holding gains and holding losses). |

|

|

For financial assets—income and expenses from changes in estimated cash flows. |

|

|

|

|

(a) This column summarises the information provided if value in use is used as a measurement basis. However, as noted in paragraph 6.75, value in use may not be a practical measurement basis for regular remeasurements. (b) Income or expenses may arise on the initial recognition of an asset not acquired on market terms. (c) Income or expenses may arise if the market in which an asset is acquired is different from the market that is the source of the prices used when measuring the fair value of the asset. (d) Consumption of the asset is typically reported through cost of sales, depreciation or amortisation. (e) Income received is often equal to the consideration received but will depend on the measurement basis used for any related liability. |

||||

|

Statement of financial position |

||||

|

|

Historical cost |

Fair value |

Fulfilment value |

Current cost |

|

Carrying amount |

Consideration received (net of transaction costs) for taking on the unfulfilled part of the liability, increased by excess of estimated cash outflows over consideration received. |

Price that would be paid to transfer the unfulfilled part of the liability (not including transaction costs that would be incurred on transfer). |

Present value of future cash flows that will arise in fulfilling the unfulfilled part of the liability (including present value of transaction costs to be incurred in fulfilment or transfer). |

Consideration (net of transaction costs) that would be currently received for taking on the unfulfilled part of the liability, increased by excess of estimated cash outflows over that consideration. |

|

|

(Includes interest accrued on any financing component.) |

|

|

|

|

Statement(s) of financial performance |

||||

|

Event |

Historical cost |

Fair value |

Fulfilment value |

Current cost |

|

Initial recognition(a) |

— |

Difference between consideration received and the fair value of the liability.(b) |

Difference between consideration received and the fulfilment value of the liability. |

— |

|

|

|

Transaction costs on incurring or taking on the liability. |

Transaction costs on incurring or taking on the liability. |

|

|

Fulfilment of the liability |

Income equal to historical cost of the liability fulfilled (reflects historical consideration). |

Income equal to fair value of the liability fulfilled. |

Income equal to fulfilment value of the liability fulfilled. |

Income equal to current cost of the liability fulfilled (reflects current consideration). |

|

|

Expenses for costs incurred in fulfilling the liability. |

Expenses for costs incurred in fulfilling the liability. |

Expenses for costs incurred in fulfilling the liability. |

Expenses for costs incurred in fulfilling the liability. |

|

|

(Could be presented net or gross.) |

(Could be presented net or gross. If gross, historical consideration could be presented separately.) |

(Could be presented net or gross. If gross, historical consideration could be presented separately.) |

(Could be presented net or gross. If gross, historical consideration could be presented separately.) |

|

Transfer of the liability |

Income equal to historical cost of the liability transferred (reflects historical consideration). |

Income equal to fair value of the liability transferred. |

Income equal to fulfilment value of the liability transferred. |

Income equal to current cost of the liability transferred (reflects current consideration). |

|

|

Expenses for costs paid (including transaction costs) to transfer the liability. |

Expenses for costs paid (including transaction costs) to transfer the liability. |

Expenses for costs paid (including transaction costs) to transfer the liability. |

Expenses for costs paid (including transaction costs) to transfer the liability. |

|

|

(Could be presented net or gross.) |

(Could be presented net or gross.) |

(Could be presented net or gross.) |

(Could be presented net or gross.) |

|

Interest expenses |

Interest expenses, at historical rates, updated if the liability bears variable interest. |

Reflected in income and expenses from changes in fair value. |

Reflected in income and expenses from changes in fulfilment value. |

Interest expenses, at current rates. |

|

|

|

(Could be identified separately.) |

(Could be identified separately.) |

|

|

Effect of events that cause a liability to become onerous |

Expenses equal to the excess of the estimated cash outflows over the historical cost of the liability, or a subsequent change in that excess. |

Reflected in income and expenses from changes in fair value. |

Reflected in income and expenses from changes in fulfilment value. |

Expenses equal to the excess of the estimated cash outflows over the current cost of the liability, or a subsequent change in that excess. |

|

|

|

(Could be identified separately.) |

(Could be identified separately.) |

|

|

Value changes |

Not recognised except to the extent that the liability is onerous. |

Reflected in income and expenses from changes in fair value. |

Reflected in income and expenses from changes in fulfilment value. |

Income and expenses reflecting the effect of changes in prices (holding gains and holding losses). |

|

|

For financial liabilities—income and expenses from changes in estimated cash flows. |

|

|

|

|

(a) Income or expenses may arise on the initial recognition of a liability incurred or taken on not on market terms. (b) Income or expenses may arise if the market in which a liability is incurred or taken on is different from the market that is the source of the prices used when measuring the fair value of the liability. |

||||

Factors to consider when selecting a measurement basis

6.43

In selecting a measurement basis for an asset or liability and for the related income and expenses, it is necessary to consider the nature of the information that the measurement basis will produce in both the statement of financial position and the statement(s) of financial performance (see paragraphs 6.23–6.42 and Table 6.1), as well as other factors (see paragraphs 6.44–6.86).

6.46

As explained in paragraph 2.21, the most efficient and effective process for applying the fundamental qualitative characteristics would usually be to identify the most relevant information about an economic phenomenon. If that information is not available or cannot be provided in a way that faithfully represents the economic phenomenon, the next most relevant type of information is considered. Paragraphs 6.49–6.76 provide further discussion of the role played by the qualitative characteristics in the selection of a measurement basis.

6.47

The discussion in paragraphs 6.49–6.76 focuses on the factors to be considered in selecting a measurement basis for recognised assets and recognised liabilities. Some of that discussion may also apply in selecting a measurement basis for information provided in the notes, for recognised or unrecognised items.

6.48

Paragraphs 6.77–6.82 discuss additional factors to consider in selecting a measurement basis on initial recognition. If the initial measurement basis is inconsistent with the subsequent measurement basis, income and expenses might be recognised at the time of the first subsequent measurement solely because of the change in measurement basis. Recognising such income and expenses might appear to depict a transaction or other event when, in fact, no such transaction or event has occurred. Hence, the choice of measurement basis for an asset or liability, and for the related income and expenses, is determined by considering both initial measurement and subsequent measurement.

Relevance

6.49

(a) the characteristics of the asset or liability (see paragraphs 6.50–6.53); and

(b) how that asset or liability contributes to future cash flows (see paragraphs 6.54–6.57).

Characteristics of the asset or liability

Contribution to future cash flows

6.54

As noted in paragraph 1.14, some economic resources produce cash flows directly; in other cases, economic resources are used in combination to produce cash flows indirectly. How economic resources are used, and hence how assets and liabilities produce cash flows, depends in part on the nature of the business activities conducted by the entity.

6.54

As noted in paragraph 1.14, some economic resources produce cash flows directly; in other cases, economic resources are used in combination to produce cash flows indirectly. How economic resources are used, and hence how assets and liabilities produce cash flows, depends in part on the nature of the business activities conducted by the entity.

6.55

When a business activity of an entity involves the use of several economic resources that produce cash flows indirectly, by being used in combination to produce and market goods or services to customers, historical cost or current cost is likely to provide relevant information about that activity. For example, property, plant and equipment is typically used in combination with an entity’s other economic resources. Similarly, inventory typically cannot be sold to a customer, except by making extensive use of the entity’s other economic resources (for example, in production and marketing activities). Paragraphs 6.24–6.31 and 6.40–6.42 explain how measuring such assets at historical cost or current cost can provide relevant information that can be used to derive margins achieved during the period.

6.59

As noted in paragraphs 2.13 and 2.18, although a perfectly faithful representation is free from error, this does not mean that measures must be perfectly accurate in all respects.

6.60

When a measure cannot be determined directly by observing prices in an active market and must instead be estimated, measurement uncertainty arises. The level of measurement uncertainty associated with a particular measurement basis may affect whether information provided by that measurement basis provides a faithful representation of an entity’s financial position and financial performance. A high level of measurement uncertainty does not necessarily prevent the use of a measurement basis that provides relevant information. However, in some cases the level of measurement uncertainty is so high that information provided by a measurement basis might not provide a sufficiently faithful representation (see paragraph 2.22). In such cases, it is appropriate to consider selecting a different measurement basis that would also result in relevant information.

6.61

Measurement uncertainty is different from both outcome uncertainty and existence uncertainty:

(b) existence uncertainty arises when it is uncertain whether an asset or a liability exists. Paragraphs 5.12–5.14 discuss how existence uncertainty may affect decisions about whether an entity recognises an asset or liability when it is uncertain whether that asset or liability exists.

Enhancing qualitative characteristics and the cost constraint

6.63

The enhancing qualitative characteristics of comparability, understandability and verifiability, and the cost constraint, have implications for the selection of a measurement basis. The following paragraphs discuss those implications. Paragraphs 6.69–6.76 discuss further implications specific to particular measurement bases. The enhancing qualitative characteristic of timeliness has no specific implications for measurement.

6.68

Verifiability is enhanced by using measurement bases that result in measures that can be independently corroborated either directly, for example, by observing prices, or indirectly, for example, by checking inputs to a model. If a measure cannot be verified, users of financial statements may need explanatory information to enable them to understand how the measure was determined. In some such cases, it may be necessary to specify the use of a different measurement basis.

6.76

Using a current cost measurement basis, identical assets acquired or liabilities incurred at different times are reported in the financial statements at the same amount. This can enhance comparability, both from period to period for a reporting entity and in a single period across entities. However, determining current cost can be complex, subjective and costly. For example, as noted in paragraph 6.22, it may be necessary to estimate the current cost of an asset by adjusting the current price of a new asset to reflect the current age and condition of the asset held by the entity. In addition, because of changes in technology and changes in business practices, many assets would not be replaced with identical assets. Thus, a further subjective adjustment to the current price of a new asset would be required in order to estimate the current cost of an asset equivalent to the existing asset. Also, splitting changes in current cost carrying amounts between the current cost of consumption and the effect of changes in prices (see paragraph 6.42) may be complex and require arbitrary assumptions. Because of these difficulties, current cost measures may lack verifiability and understandability.

Factors specific to initial measurement

6.77

Paragraphs 6.43–6.76 discuss factors to consider when selecting a measurement basis, whether for initial recognition or subsequent measurement. Paragraphs 6.78–6.82 discuss some additional factors to consider at initial recognition.

6.78

At initial recognition, the cost of an asset acquired, or of a liability incurred, as a result of an event that is a transaction on market terms is normally similar to its fair value at that date, unless transaction costs are significant. Nevertheless, even if those two amounts are similar, it is necessary to describe what measurement basis is used at initial recognition. If historical cost will be used subsequently, that measurement basis is also normally appropriate at initial recognition. Similarly, if a current value will be used subsequently, it is also normally appropriate at initial recognition. Using the same measurement basis for initial recognition and subsequent measurement avoids recognising income or expenses at the time of the first subsequent measurement solely because of a change in measurement basis (see paragraph 6.48).

6.81

In such cases, measuring the asset acquired, or the liability incurred, at its historical cost may not provide a faithful representation of the entity’s assets and liabilities and of any income or expenses arising from the transaction or other event. Hence, it may be appropriate to measure the asset acquired, or the liability incurred, at deemed cost, as described in paragraph 6.6. Any difference between that deemed cost and any consideration given or received would be recognised as income or expenses at initial recognition.

6.82

When assets are acquired, or liabilities incurred, as a result of an event that is not a transaction on market terms, all relevant aspects of the transaction or other event need to be identified and considered. For example, it may be necessary to recognise other assets, other liabilities, contributions from holders of equity claims or distributions to holders of equity claims to faithfully represent the substance of the effect of the transaction or other event on the entity’s financial position (see paragraphs 4.59–4.62) and any related effect on the entity’s financial performance.

More than one measurement basis

6.83

Sometimes, consideration of the factors described in paragraphs 6.43–6.76 may lead to the conclusion that more than one measurement basis is needed for an asset or liability and for related income and expenses in order to provide relevant information that faithfully represents both the entity’s financial position and its financial performance.

6.85

(b) a different measurement basis for the related income and expenses in the statement of profit or loss[10] (see paragraphs 7.17–7.18).

In selecting those measurement bases, it is necessary to consider the factors discussed in paragraphs 6.43–6.76.

The Conceptual Framework does not specify whether the statement(s) of financial performance comprise(s) a single statement or two statements. The Conceptual Framework uses the term ‘statement of profit or loss’ to refer both to a separate statement and to a separate section within a single statement of financial performance.

6.86

In such cases, the total income or total expenses arising in the period from the change in the current value of the asset or liability is separated and classified (see paragraphs 7.14–7.19) so that:

(i) the carrying amount of the asset or liability in the statement of financial position; and

6.89

Although total equity is not measured directly, it may be appropriate to measure directly the carrying amount of some individual classes of equity (see paragraph 4.65) and some components of equity (see paragraph 4.66). Nevertheless, because total equity is measured as a residual, at least one class of equity cannot be measured directly. Similarly, at least one component of equity cannot be measured directly.

Cash-flow-based measurement techniques

6.91

Sometimes, a measure cannot be observed directly. In some such cases, one way to estimate the measure is by using cash-flow-based measurement techniques. Such techniques are not measurement bases. They are techniques used in applying a measurement basis. Hence, when using such a technique, it is necessary to identify which measurement basis is used and the extent to which the technique reflects the factors applicable to that measurement basis. For example, if the measurement basis is fair value, the applicable factors are those described in paragraph 6.14.

6.93

Outcome uncertainty (see paragraph 6.61(a)) arises from uncertainties about the amount or timing of future cash flows. Those uncertainties are important characteristics of assets and liabilities. When measuring an asset or liability by reference to estimates of uncertain future cash flows, one factor to consider is possible variations in the estimated amount or timing of those cash flows (see paragraph 6.14(b)). Those variations are considered in selecting a single amount from within the range of possible cash flows. The amount selected is itself sometimes the amount of a possible outcome, but this is not always the case. The amount that provides the most relevant information is usually one from within the central part of the range (a central estimate). Different central estimates provide different information. For example:

6.94

A central estimate depends on estimates of future cash flows and possible variations in their amounts or timing. It does not capture the price for bearing the uncertainty that the ultimate outcome may differ from that central estimate (that is, the factor described in paragraph 6.14(d)).

Chapter 7—Presentation and disclosure

Presentation and disclosure as communication tools

Presentation and disclosure objectives and principles

7.4

7.6

Classification of assets and liabilities

7.9

Classification is applied to the unit of account selected for an asset or liability (see paragraphs 4.48–4.55). However, it may sometimes be appropriate to separate an asset or liability into components that have different characteristics and to classify those components separately. That would be appropriate when classifying those components separately would enhance the usefulness of the resulting financial information. For example, it could be appropriate to separate an asset or liability into current and non-current components and to classify those components separately.

7.11

Offsetting assets and liabilities differs from treating a set of rights and obligations as a single unit of account (see paragraphs 4.48–4.55).

Classification of equity

7.12

To provide useful information, it may be necessary to classify equity claims separately if those equity claims have different characteristics (see paragraph 4.65).

7.12

To provide useful information, it may be necessary to classify equity claims separately if those equity claims have different characteristics (see paragraph 4.65).

7.13

Similarly, to provide useful information, it may be necessary to classify components of equity separately if some of those components are subject to particular legal, regulatory or other requirements. For example, in some jurisdictions, an entity is permitted to make distributions to holders of equity claims only if the entity has sufficient reserves specified as distributable (see paragraph 4.66). Separate presentation or disclosure of those reserves may provide useful information.

Classification of income and expenses

7.14

(a) income and expenses resulting from the unit of account selected for an asset or liability; or

(b) components of such income and expenses if those components have different characteristics and are identified separately. For example, a change in the current value of an asset can include the effects of value changes and the accrual of interest (see Table 6.1). It would be appropriate to classify those components separately if doing so would enhance the usefulness of the resulting financial information.

7.14

(a) income and expenses resulting from the unit of account selected for an asset or liability; or

(b) components of such income and expenses if those components have different characteristics and are identified separately. For example, a change in the current value of an asset can include the effects of value changes and the accrual of interest (see Table 6.1). It would be appropriate to classify those components separately if doing so would enhance the usefulness of the resulting financial information.

Profit or loss and other comprehensive income

7.15

Income and expenses are classified and included either:

(a) in the statement of profit or loss;[11] or

(b) outside the statement of profit or loss, in other comprehensive income.

7.15

Income and expenses are classified and included either:

(a) in the statement of profit or loss;[11] or

(b) outside the statement of profit or loss, in other comprehensive income.

The Conceptual Framework does not specify whether the statement(s) of financial performance comprise(s) a single statement or two statements. The Conceptual Framework uses the term ‘statement of profit or loss’ to refer to a separate statement and to a separate section within a single statement of financial performance. Likewise, it uses the term ‘total for profit or loss’ to refer both to a total for a separate statement and to a subtotal for a section within a single statement of financial performance.

7.18

Income and expenses that arise on a historical cost measurement basis (see Table 6.1) are included in the statement of profit or loss. That is also the case when income and expenses of that type are separately identified as a component of a change in the current value of an asset or liability. For example, if a financial asset is measured at current value and if interest income is identified separately from other changes in value, that interest income is included in the statement of profit or loss.

Chapter 8—Concepts of capital and capital maintenance

Concepts of capital maintenance and the determination of profit

8.3

The concepts of capital in paragraph 8.1 give rise to the following concepts of capital maintenance:

Appendix -- Defined terms

The following defined terms are extracted or derived from the relevant paragraphs of the Conceptual Framework for Financial Reporting.

aggregation

[1]

The adding together of assets, liabilities, equity, income or expenses that have shared characteristics and are included in the same classification. CF.7.20

asset

[2]

A present economic resource controlled by the entity as a result of past events. CF.4.3

carrying amount

[3]

The amount at which an asset, a liability or equity is recognised in the statement of financial position. CF.5.1

classification

[4]

The sorting of assets, liabilities, equity, income or expenses on the basis of shared characteristics for presentation and disclosure purposes. CF.7.7

combined financial statements

[5]

Financial statements of a reporting entity that comprises two or more entities that are not all linked by a parent-subsidiary relationship. CF.3.12

consolidated financial statements

[6]

Financial statements of a reporting entity that comprises both the parent and its subsidiaries. CF.3.11

control of an economic resource

[7]

The present ability to direct the use of the economic resource and obtain the economic benefits that may flow from it. CF.4.20

derecognition

[8]

The removal of all or part of a recognised asset or liability from an entity’s statement of financial position. CF.5.26

economic resource

[9]

A right that has the potential to produce economic benefits. CF.4.4

equity

[11]

The residual interest in the assets of the entity after deducting all its liabilities. CF.4.63

equity claim

[12]

A claim on the residual interest in the assets of the entity after deducting all its liabilities. CF.4.64

executory contract

[13]

A contract, or a portion of a contract, that is equally unperformed—neither party has fulfilled any of its obligations, or both parties have partially fulfilled their obligations to an equal extent. CF.4.56

expenses

[15]

Decreases in assets, or increases in liabilities, that result in decreases in equity, other than those relating to distributions to holders of equity claims. CF.4.69

general purpose financial report

general purpose financial statements

[18]

A particular form of general purpose financial reports that provide information about the reporting entity’s assets, liabilities, equity, income and expenses. CF.3.2

income

[19]

Increases in assets, or decreases in liabilities, that result in increases in equity, other than those relating to contributions from holders of equity claims. CF.4.68

liability

[20]

A present obligation of the entity to transfer an economic resource as a result of past events. CF.4.26

material information

[21]

Information whose omission or misstatement could influence decisions that the primary users of general purpose financial reports make on the basis of those reports, which provide financial information about a specific reporting entity. CF.2.11

measure

[22]

The result of applying a measurement basis to an asset or liability and related income and expenses. CF.6.1

measurement basis

[23]

An identified feature—for example, historical cost, fair value or fulfilment value—of an item being measured. CF.6.1

measurement uncertainty

[24]

Uncertainty that arises when monetary amounts in financial reports cannot be observed directly and must instead be estimated. CF.2.19

offsetting

[25]

Grouping an asset and liability that are recognised and measured as separate units of account into a single net amount in the statement of financial position. CF.7.10

outcome uncertainty

[26]

Uncertainty about the amount or timing of any inflow or outflow of economic benefits that will result from an asset or liability. CF.6.61

potential to produce economic benefits

[27]

Within an economic resource, a feature that already exists and that, in at least one circumstance, would produce for the entity economic benefits beyond those available to all other parties. CF.4.14

primary users (of general purpose financial reports)

[28]

Existing and potential investors, lenders and other creditors. CF.1.2

prudence

[29]