Illustrative examples

The following examples accompany, but are not part of, AASB 124 Related Party Disclosures. They illustrate:

• the partial exemption for government-related entities; and

• how the definition of a related party would apply in specified circumstances.

In the examples, references to ‘financial statements’ relate to the individual, separate or consolidated financial statements.

Partial exemption for government-related entities

Example 1 – Exemption from disclosure (paragraph 25)

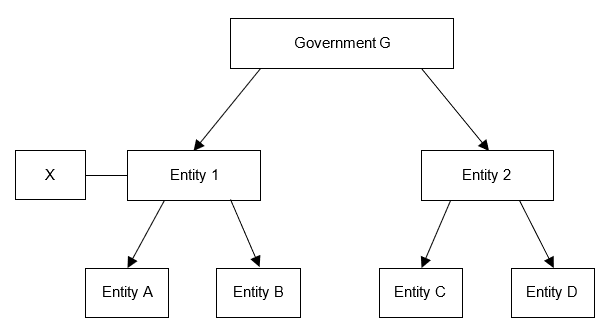

IE1

Government G directly or indirectly controls Entities 1 and 2 and Entities A, B, C and D. Person X is a member of the key management personnel of Entity 1.

IE2

For Entity A’s financial statements, the exemption in paragraph 25 applies to:

(a) transactions with Government G; and

(b) transactions with Entities 1 and 2 and Entities B, C and D.

However, that exemption does not apply to transactions with Person X.

Disclosure requirements when exemption applies (paragraph 26)

IE3

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(i) for individually significant transactions could be:

Example of disclosure for individually significant transaction carried out on non-market terms

On 15 January 20X1 Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, sold a 10 hectare piece of land to another government-related utility company for CU5 million. On 31 December 20X0 a plot of land in a similar location, of a similar size and with similar characteristics, was sold for CU3 million.[2] There had not been any appreciation or depreciation of the land in the intervening period. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure for individually significant transaction because of size of transaction

In the year ended December 20X1 Government G provided Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, with a loan equivalent to 50 per cent of its funding requirement, repayable in quarterly instalments over the next five years. Interest is charged on the loan at a rate of 3 per cent, which is comparable to that charged on Entity A’s bank loans.[3] See notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure of collectively significant transactions

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(ii) for collectively significant transactions could be:

Government G, indirectly, owns 75 per cent of Entity A’s outstanding shares. Entity A’s significant transactions with Government G and other entities controlled, jointly controlled or significantly influenced by Government G are [a large portion of its sales of goods and purchases of raw materials] or [about 50 per cent of its sales of goods and about 35 per cent of its purchases of raw materials].

The company also benefits from guarantees by Government G of the company’s bank borrowing. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

IE3

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(i) for individually significant transactions could be:

Example of disclosure for individually significant transaction carried out on non-market terms

On 15 January 20X1 Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, sold a 10 hectare piece of land to another government-related utility company for CU5 million. On 31 December 20X0 a plot of land in a similar location, of a similar size and with similar characteristics, was sold for CU3 million.[2] There had not been any appreciation or depreciation of the land in the intervening period. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure for individually significant transaction because of size of transaction

In the year ended December 20X1 Government G provided Entity A, a utility company in which Government G indirectly owns 75 per cent of outstanding shares, with a loan equivalent to 50 per cent of its funding requirement, repayable in quarterly instalments over the next five years. Interest is charged on the loan at a rate of 3 per cent, which is comparable to that charged on Entity A’s bank loans.[3] See notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

Example of disclosure of collectively significant transactions

In Entity A’s financial statements, an example of disclosure to comply with paragraph 26(b)(ii) for collectively significant transactions could be:

Government G, indirectly, owns 75 per cent of Entity A’s outstanding shares. Entity A’s significant transactions with Government G and other entities controlled, jointly controlled or significantly influenced by Government G are [a large portion of its sales of goods and purchases of raw materials] or [about 50 per cent of its sales of goods and about 35 per cent of its purchases of raw materials].

The company also benefits from guarantees by Government G of the company’s bank borrowing. See note X [of the financial statements] for disclosure of government assistance as required by AASB 120 Accounting for Government Grants and Disclosure of Government Assistance and notes Y and Z [of the financial statements] for compliance with other relevant Australian Accounting Standards.

In these examples monetary amounts are denominated in ‘currency units (CU)’.

If the reporting entity had concluded that this transaction constituted government assistance it would have needed to consider the disclosure requirements in AASB 120.

Definition of a related party

The references are to subparagraphs of the definition of a related party in paragraph 9 of AASB 124.

Example 2 – Associates and subsidiaries

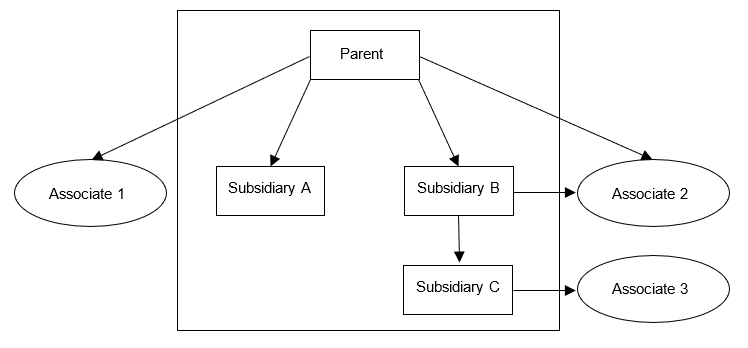

IE4

Parent entity has a controlling interest in Subsidiaries A, B and C and has significant influence over Associates 1 and 2. Subsidiary C has significant influence over Associate 3.

IE5

For Parent’s separate financial statements, Subsidiaries A, B and C and Associates 1, 2 and 3 are related parties. [Paragraph 9(b)(i) and (ii)]

IE6

For Subsidiary A’s financial statements, Parent, Subsidiaries B and C and Associates 1, 2 and 3 are related parties. For Subsidiary B’s separate financial statements, Parent, Subsidiaries A and C and Associates 1, 2 and 3 are related parties. For Subsidiary C’s financial statements, Parent, Subsidiaries A and B and Associates 1, 2 and 3 are related parties. [Paragraph 9(b)(i) and (ii)]

IE7

For the financial statements of Associates 1, 2 and 3, Parent and Subsidiaries A, B and C are related parties. Associates 1, 2 and 3 are not related to each other. [Paragraph 9(b)(ii)]

IE8

For Parent’s consolidated financial statements, Associates 1, 2 and 3 are related to the Group. [Paragraph 9(b)(ii)]

Example 3 – Key management personnel

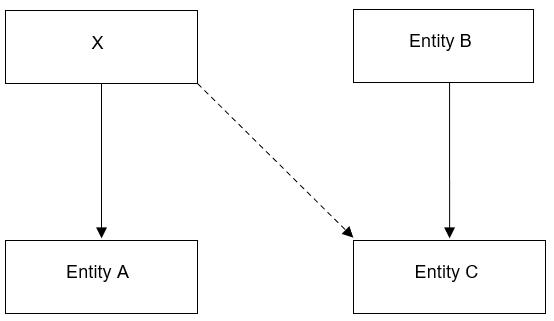

IE9

A person, X, has a 100 per cent investment in Entity A and is a member of the key management personnel of Entity C. Entity B has a 100 per cent investment in Entity C.

IE10

For Entity C’s financial statements, Entity A is related to Entity C because X controls Entity A and is a member of the key management personnel of Entity C. [Paragraph 9(b)(vi)–(a)(iii)]

IE11

For Entity C’s financial statements, Entity A is also related to Entity C if X is a member of the key management personnel of Entity B and not of Entity C. [Paragraph 9(b)(vi)–(a)(iii)]

IE12

Furthermore, the outcome described in paragraphs IE10 and IE11 will be the same if X has joint control over Entity A. [Paragraph 9(b)(vi)–(a)(iii)] (If X had only significant influence over Entity A and not control or joint control, then Entities A and C would not be related to each other.)

IE13

For Entity A’s financial statements, Entity C is related to Entity A because X controls A and is a member of Entity C’s key management personnel. [Paragraph 9(b)(vii)–(a)(i)]

IE14

Furthermore, the outcome described in paragraph IE13 will be the same if X has joint control over Entity A. The outcome will also be the same if X is a member of key management personnel of Entity B and not of Entity C. [Paragraph 9(b)(vii)–(a)(i)]

IE15

For Entity B’s consolidated financial statements, Entity A is a related party of the Group if X is a member of key management personnel of the Group. [Paragraph 9(b)(vi)–(a)(iii)]

Example 4 – Person as investor

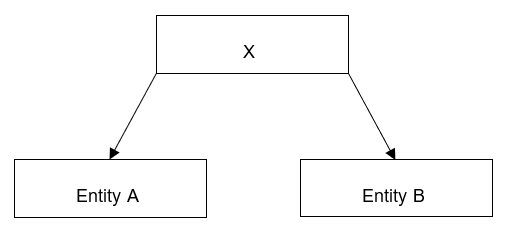

IE16

A person, X, has an investment in Entity A and Entity B.

IE17

For Entity A’s financial statements, if X controls or jointly controls Entity A, Entity B is related to Entity A when X has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vii)–(a)(i)]

IE18

For Entity B’s financial statements, if X controls or jointly controls Entity A, Entity A is related to Entity B when X has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vi)–(a)(ii)]

IE19

If X has significant influence over both Entity A and Entity B, Entities A and B are not related to each other.

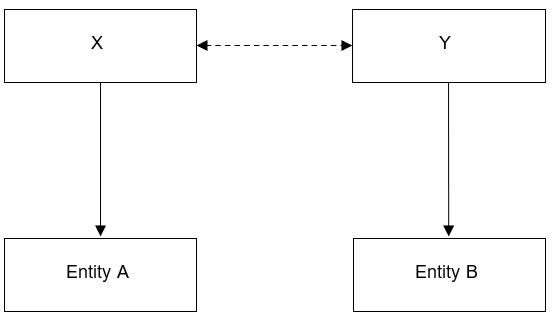

Example 5 – Close members of the family holding investments

IE20

A person, X, is the domestic partner of Y. X has an investment in Entity A and Y has an investment in Entity B.

IE21

For Entity A’s financial statements, if X controls or jointly controls Entity A, Entity B is related to Entity A when Y has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vii)–(a)(i)]

IE22

For Entity B’s financial statements, if X controls or jointly controls Entity A, Entity A is related to Entity B when Y has control, joint control or significant influence over Entity B. [Paragraph 9(b)(vi)–(a)(i) and 9(b)(vi)–(a)(ii)]

IE23

If X has significant influence over Entity A and Y has significant influence over Entity B, Entities A and B are not related to each other.

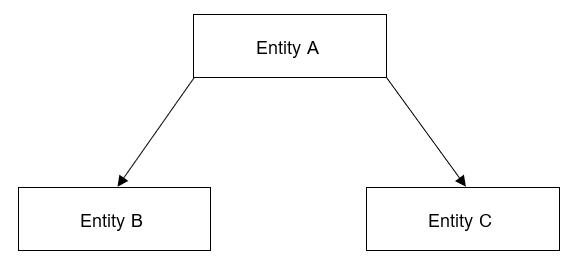

Example 6 – Entity with joint control

IE24

Entity A has both (i) joint control over Entity B and (ii) joint control or significant influence over Entity C.

IE25

For Entity B’s financial statements, Entity C is related to Entity B. [Paragraph 9(b)(iii) and (iv)]

IE26

Similarly, for Entity C’s financial statements, Entity B is related to Entity C. [Paragraph 9(b)(iii) and (iv)]