This Standard applies when a not-for-profit entity receives volunteer services or enters into other transactions where the consideration to acquire an asset is significantly less than the fair value of the asset principally to enable the entity to further its objectives.

Preamble

Pronouncement

This compiled Standard applies to annual periods beginning on or after 1 July 2021 but before 1 January 2023. Earlier application is permitted for annual periods beginning before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 21 July 2021 by the staff of the Australian Accounting Standards Board.

Compilation no. 3

Compilation date: 30 June 2021

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

Rubric

Australian Accounting Standard AASB 1058 Income of Not-for-Profit Entities (as amended) is set out in paragraphs 1 – 41 and Appendices A – E. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the Standard. AASB 1058 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Accounting Standard AASB 1058

The Australian Accounting Standards Board made Accounting Standard AASB 1058 Income of Not-for-Profit Entities under section 334 of the Corporations Act 2001 on 9 December 2016.

This compiled version of AASB 1058 applies to annual periods beginning on or after 1 July 2021 but before 1 January 2023. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

1

This Standard establishes principles for not-for-profit entities that apply to:

(a) transactions where the consideration to acquire an asset is significantly less than fair value principally to enable a not-for-profit entity to further its objectives; and

(b) the receipt of volunteer services.

2

If the consideration provided to acquire an asset, including cash, is significantly less than the fair value of that asset, or if no consideration was provided, and the difference is principally to enable the entity to further its objectives, such a transaction is within the scope of this Standard. For example, an entity that receives a cash grant to be used to further its objectives might not have provided any consideration in exchange for that cash. As another example, governments are entitled to non-contractual receivables arising from statutory requirements such as taxes and rates without providing consideration to the other party – those receivables provide income to the government to further its objectives. This Standard addresses the accounting for the income arising from such transactions.

Meeting the objective

3

To meet the objective in paragraph 1(a), an entity shall initially recognise:

(a) an asset in accordance with the applicable Australian Accounting Standard;

(b) any related contributions by owners, contract liabilities, financial liabilities, lease liabilities and other liabilities and revenue, measured in accordance with the applicable Australian Accounting Standard;

(c) any liabilities for obligations arising from transfers to enable the entity to acquire or construct non-financial assets to be controlled by the entity; and

(d) related income, representing the residual amount of resources received.

4

To meet the objective in paragraph 1(b), certain types of public sector entities shall recognise assets or expenses for volunteer services received if the fair value of those services can be measured reliably and the entity would have purchased those services if they had not been donated. Any not-for-profit entity may elect to recognise volunteer services received if their fair value can be measured reliably irrespective of whether that entity would have purchased those services if not donated.

5

AASB 15 Revenue from Contracts with Customers defines income as increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions by equity participants (that is, owners). This Standard addresses income arising from the acquisition of assets for consideration that is significantly less than the fair value of the asset when that difference is principally to enable the not-for-profit entity to further its objectives. This Standard applies to those differences that result in increases in equity, other than those relating to contributions by owners or those accounted for under another Standard (eg AASB 15). Other Australian Accounting Standards (eg AASB 1004 Contributions) address income arising from decreases of liabilities and the accounting for contributions by owners.

6

An entity shall apply the requirements of this Standard to each transaction based on the substance of the transaction, rather than its legal form or the description given to it (eg grants or donations), so as to provide a faithful representation of the economic substance of the transaction.

Scope (paragraphs B2-B11)

7

An entity shall apply this Standard to transactions where the consideration to acquire an asset is significantly less than fair value principally to enable the entity to further its objectives, and the receipt of volunteer services, except for:

(a) share-based payment transactions within the scope of AASB 2 Share-based Payment;

(b) business combinations within the scope of AASB 3 Business Combinations;

(c) insurance contracts within the scope of AASB 4 Insurance Contracts, AASB 1023 General Insurance Contracts or AASB 1038 Life Insurance Contracts;

(d) licences outside the scope of AASB 15;

(e) income taxes within the scope of AASB 112 Income Taxes; and

(f) restructures of administrative arrangements within the scope of AASB 1004.

Recognition and measurement

Recognition and measurement of an asset

8

Except as set out in paragraphs 18–22, an entity shall apply the requirements of other Australian Accounting Standards (as relevant) to an asset arising from a transaction within the scope of this Standard. Examples include:

(a) AASB 9 Financial Instruments (eg cash received);

(b) AASB 16 Leases;

(c) AASB 116 Property, Plant and Equipment; and

(d) AASB 138 Intangible Assets.

Recognition and measurement of income and related amounts (paragraphs B12–B31)

9

On initial recognition of an asset, an entity shall recognise any related contributions by owners, increases in liabilities, decreases in assets, and revenue (‘related amounts’) in accordance with other Australian Accounting Standards. For example, related amounts may take the form of:

(a) contributions by owners, in accordance with AASB 1004;

(b) revenue or a contract liability arising from a contract with a customer, in accordance with AASB 15;

(c) a lease liability in accordance with AASB 16;

(d) a financial instrument, in accordance with AASB 9; or

(e) a provision, in accordance with AASB 137 Provisions, Contingent Liabilities and Contingent Assets.

10

Except as set out in paragraphs 15–17, an entity shall recognise income immediately in profit or loss for the excess of the initial carrying amount of an asset over the related amounts recognised in accordance with paragraph 9.

11

Appendix F Australian Implementation Guidance for Not-for-Profit Entities of AASB 15 provides guidance on the identification of a contract with a customer in a not-for-profit entity context. The Appendix also clarifies the measurement of revenue and contract liabilities where the transaction price includes an amount that would otherwise be separately recognised and accounted for as income immediately in accordance with this Standard.

14

An entity shall subsequently apply the requirements of other Australian Accounting Standards applicable to the related amounts referred to in paragraph 9.

Transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity

15

A transfer of a financial asset to enable an entity to acquire or construct a recognisable non-financial asset that is to be controlled by the entity is one that:

(a) requires the entity to use that financial asset to acquire or construct a recognisable non-financial asset to identified specifications;

(b) does not require the entity to transfer the non-financial asset to the transferor or other parties; and

(c) occurs under an enforceable agreement.

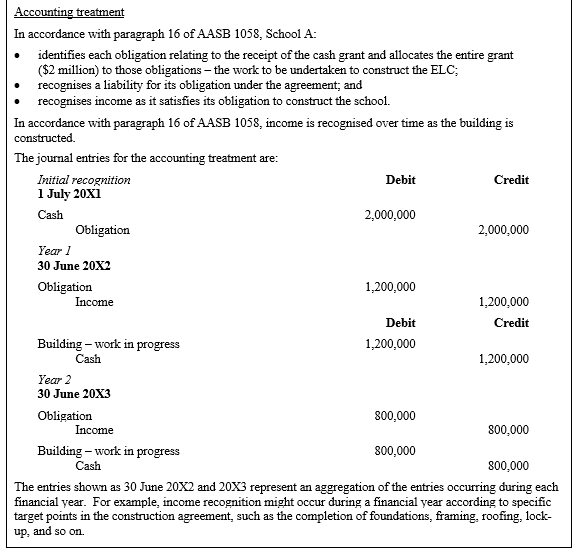

16

An entity shall recognise a liability for the excess of the initial carrying amount of a financial asset received in a transfer to enable the entity to acquire or construct a recognisable non-financial asset that is to be controlled by the entity over any related amounts recognised in accordance with paragraph 9. The entity shall recognise income in profit or loss when (or as) the entity satisfies its obligations under the transfer.

17

In such circumstances, the transferor has in substance transferred a recognisable non-financial asset to the entity. The entity recognises the financial asset received in accordance with AASB 9 and subsequently recognises the acquired or constructed non-financial asset in accordance with the applicable Australian Accounting Standard (eg AASB 116 for property, plant and equipment). This Standard requires the entity to initially recognise a liability representing the entity’s obligation to acquire or construct the non-financial asset and, if applicable, other performance obligations under AASB 15, which involve the transfer of goods or services to other parties. The liability in relation to acquiring or constructing the non-financial asset is initially measured at the carrying amount of the financial asset received from the transferor that is not attributable to related amounts for performance obligations under AASB 15, contributions by owners, etc. The liability is recognised until such time when (or as) the entity satisfies its obligations under the transfer.

Volunteer services

18

(a) the fair value of those services can be measured reliably; and

(b) the services would have been purchased if they had not been donated.

21

Recognised volunteer services shall be measured at fair value.

22

On the initial recognition of volunteer services as an asset or an expense, an entity shall recognise any related amounts in accordance with paragraph 9 (such as contributions by owners or revenue) and the applicable Australian Accounting Standards. The entity shall recognise the excess of the fair value of the volunteer services over the recognised related amounts as income immediately in profit or loss.

Disclosure

23

The objective of the disclosure requirements is for an entity to disclose sufficient information to enable users of financial statements to understand the effects of volunteer services and other transactions where an entity acquires an asset for consideration that is significantly less than fair value principally to enable the entity to further its objectives on the financial position, financial performance and cash flows of the entity. Paragraphs 24–41 specify requirements relating to this objective.

26

An entity shall disclose income recognised during the period, disaggregated into categories that reflect how the nature and amount of income (and the resultant cash flows) are affected by economic factors. An entity considers disclosing separately the following categories of income:

(a) grants, bequests and donations of cash, other financial assets and goods;

(b) recognised volunteer services; and

(c) for government departments and other public sector entities, appropriation amounts recognised as income, by class of appropriation.

27

To assist users to make informed judgements about the contribution of volunteer services and inventories to the achievement of the entity’s objectives during the reporting period, and the entity’s dependence on such contributions for the achievement of its objectives in the future, an entity is encouraged to disclose qualitative information, by major class of transaction, about the nature of the entity’s dependence arising from:

(a) volunteer services it receives, including those not recognised; and

(b) inventories held but not recognised as assets during the period.

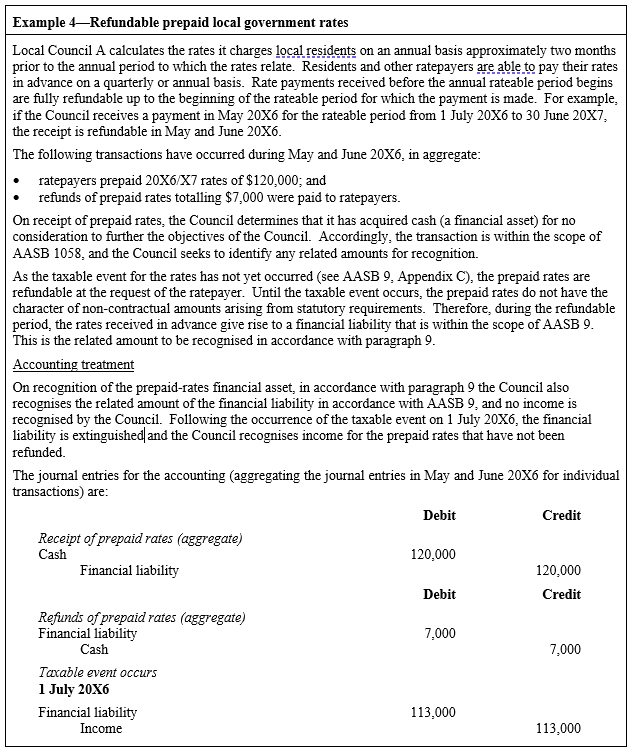

Non-contractual income arising from statutory requirements

28

An entity shall disclose income arising from statutory requirements (such as taxes, rates and fines) recognised during the period, disaggregated into categories that reflect how the nature and amount of income (and the resultant cash flows) are affected by economic factors.

29

To meet the objective in paragraph 23, an entity shall consider disclosing information about assets and liabilities recognised at the reporting date in accordance with this Standard, including the amounts of:

(a) receivables that are not a financial asset as defined in AASB 132 Financial Instruments: Presentation (eg income tax receivable from a taxpayer), and:

(i) interest income recognised in relation to such receivables during the period; and

(ii) impairment losses recognised in relation to such receivables during the period; and

(b) financial liabilities relating to prepaid taxes or rates for which the taxable event has yet to occur, and the future period(s) to which those taxes or rates relate.

30

Other information that may be appropriate for an entity to disclose includes, for each class of taxation income that the entity cannot measure reliably during the period in which the taxable event occurs (see paragraphs B28–B31):

(a) information about the nature of the tax;

(b) the reason(s) why that income cannot be measured reliably; and

(c) when that uncertainty might be resolved.

Transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity

31

An entity shall disclose the opening and closing balances of financial assets arising from transfers to enable an entity to acquire or construct recognisable non-financial assets to be controlled by the entity and the associated liabilities arising from such transfers, if not otherwise separately presented or disclosed. An entity shall also disclose income recognised in the reporting period arising from the reduction of an associated liability.

32

An entity shall disclose information about its obligations under such transfers, including a description of when the entity typically satisfies its obligations (for example, as the asset is constructed, upon completion of construction or when the asset is acquired).

33

An entity shall disclose an explanation of when it expects to recognise as income any liability for unsatisfied obligations as at the end of the reporting period. An entity may disclose this information in either of the following ways:

(a) on a quantitative basis using the time bands that would be most appropriate for the duration of the remaining obligations; or

(b) through qualitative information.

34

An entity shall disclose the judgements, and changes in the judgements, made in applying this Standard that significantly affect the determination of the amount and timing of income arising from transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity. In particular, an entity shall explain the judgements, and changes in the judgements, made in determining the timing of satisfaction of obligations (see paragraphs 35 and 36).

35

For obligations that an entity satisfies over time, an entity shall disclose both of the following:

(a) the methods used to recognise income (for example, a description of the output methods or input methods used and how those methods are applied); and

(b) an explanation of why the methods used provide a faithful depiction of the entity’s progress toward satisfying its obligations.

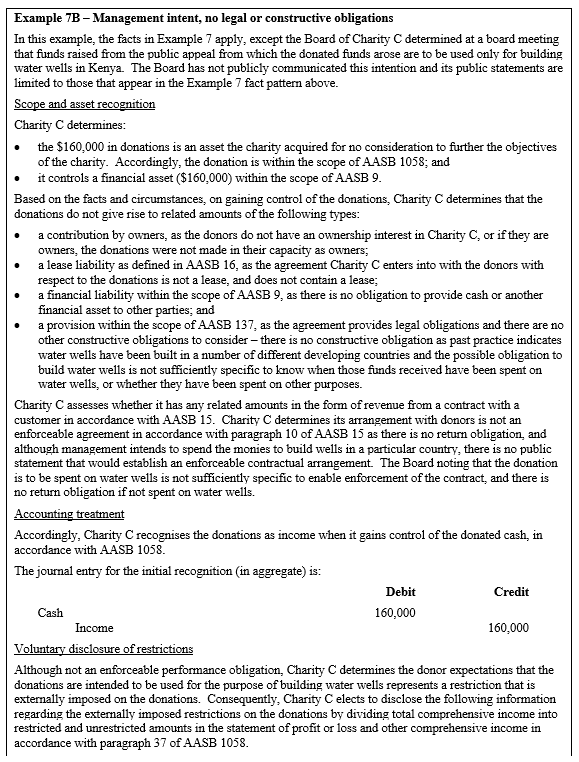

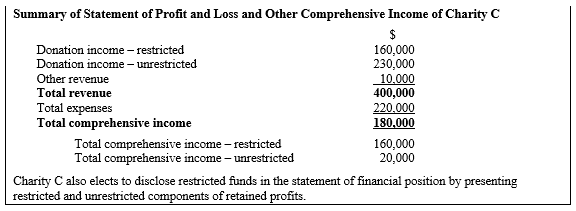

Restrictions

37

An entity is encouraged to disclose information about externally imposed restrictions that limit or direct the purpose for which resources controlled by the entity may be used. For example, an entity may elect to disclose an explanation of the judgements used in determining whether funds are restricted and any of, or any combination of, the following:

(a) assets to be used for specified purposes;

(b) components of equity divided into restricted and unrestricted amounts; and

(c) total comprehensive income divided into restricted and unrestricted amounts – either on the face of the statement of profit or loss and other comprehensive income or in the notes.

Compliance with parliamentary appropriations and other related authorities for expenditure

38

Paragraphs 39–41 apply only to government departments and other public sector entities that obtain part or all of their spending authority for the period from a parliamentary appropriation. The amounts disclosed in accordance with paragraphs 39–41 include any amounts appropriated in respect of which the entity recognises revenue or other income in accordance with another Australian Accounting Standard.

39

An entity shall disclose:

(a) a summary of the recurrent, capital or other major categories of amounts authorised for expenditure (including parliamentary appropriations), disclosing separately:

(i) the original amounts appropriated; and

(ii) the total of any supplementary amounts appropriated and amounts authorised other than by way of appropriation (eg by the Treasurer, other Minister or other legislative authority);

(b) the expenditures in respect of each of the items disclosed in (a) above; and

(c) the reasons for any material variances between the amounts appropriated or otherwise authorised and the resulting associated expenditures, and any financial consequences for the entity of unauthorised expenditure.

40

For the purposes of resource allocation decisions, including assessments of accountability, this Standard requires that users of financial statements of government departments and other public sector entities that obtain part or all of their spending authority for the period from a parliamentary appropriation be provided with information about the amounts appropriated or otherwise authorised for the entity’s use, and whether the entity’s expenditures were as authorised. This information may be based on acquittal processes applied by an entity. When spending limits imposed by parliamentary appropriation or other authorisation have not been complied with, information regarding the amount of, and reasons for, the non-compliance is relevant for assessing the performance of management, the likely consequences of non-compliance, and the ability of the entity to continue to provide services at a similar or different level in the future.

41

Broad summaries of the major categories of appropriations and associated expenditures, rather than detailed reporting of appropriations for each activity or output, is sufficient for most users of such an entity’s financial statements. Determining the level of detail and the structure of the summarised information is a matter of judgement. To develop effective disclosures, entities also subject to AASB 1055 Budgetary Reporting might consider the variance disclosure requirements in that Standard at the same time.

Appendix A -- Defined terms

This appendix is an integral part of the Standard.

contributions by owners

A[1]

Future economic benefits that have been contributed to the entity by parties external to the entity, other than those which result in liabilities of the entity, that give rise to a financial interest in the net assets of the entity which:

(a) conveys entitlement both to distributions of future economic benefits by the entity during its life, such distributions being at the discretion of the ownership group or its representatives, and to distributions of any excess of assets over liabilities in the event of the entity being wound up; and/or

(b) can be sold, transferred or redeemed.

fines

A[2]

Economic benefits received or receivable by an entity, as determined by a court or other law enforcement body, as a consequence of a breach of a law or regulation.

payable tax credits

A[3]

Tax credits that are not limited to the amount of a taxpayer’s tax liability for the period, because they are available to beneficiaries regardless of whether they pay taxes.

tax relief

A[4]

Preferential provisions of the tax law that provide particular taxpayers with concessions that are not available to others. Tax relief excludes payable tax credits.

taxable event

A[5]

The event that the government, legislature or other authority has determined will be subject to taxation.

taxes

A[6]

Economic benefits compulsorily paid or payable to public sector entities in accordance with laws and/or regulations established to provide income to the government. Taxes exclude fines.

Appendix B-- Application guidance

This appendix is an integral part of the Standard. It describes the application of paragraphs 1–41.

Application of this Standard

B1

The following flowcharts summarise the main requirements of this Standard to assist in its application.

Chart 1 – Transactions other than Volunteer Services

Chart 2 – Volunteer Services

Scope (paragraph 7)

B2

(a) cash and other assets received from grants, bequests or donations;

(b) receipts of appropriations by government departments and other public sector entities;

(c) receipts of taxes, rates or fines; and

(d) assets acquired for nominal or low amounts.

B3

Where an asset is acquired for consideration that is significantly less than fair value but that difference is not principally related to furthering the entity’s objectives, the transaction is not within the scope of this Standard. Examples of such transactions include:

(a) distress sales; and

(b) trade discounts.

B4

When assessing whether the consideration for an asset is less than fair value principally to enable the entity to further its objectives, the entity may consider whether another entity could have obtained the asset under the same terms and conditions. If those terms and conditions are generally not available to other entities of the same class/nature, it is more likely that the difference between the consideration for the asset and the fair value of the asset acquired is principally for enabling the entity to further its objectives. For example, trade discounts available to all not-for-profit entities, but not to for-profit entities, are not considered principally to further the specific not-for-profit entity’s objectives.

B5

Where the consideration provided under a transaction solely involves performance obligations recognised in accordance with AASB 15, the asset is not acquired for consideration that is significantly less than fair value. Therefore, the transaction is not within the scope of this Standard.

B6

Transfers with consideration significantly less than fair value primarily to enable a not-for-profit entity to further its objectives may be called grants, bequests, donations or appropriations and are usually made voluntarily. Such transfers could be in the form of cash or another financial asset, goods, or volunteer services, and may or may not be made with restrictions or conditions on their use. Transactions may include elements with consideration that is significantly less than fair value primarily to enable the not-for-profit entity to further its objectives and other elements with consideration at fair value. For example, a donation by a customer may be present in a contract in which a customer promises consideration in exchange for goods or services (eg a fundraising dinner).

B7

Volunteer services are services transferred by individuals or other entities without charge or for consideration significantly less than the fair value of those services. Whether such services (when recognised in accordance with paragraphs 18 and 19) are recognised as an asset or an expense depends on the entity’s determination whether it is probable that economic benefits will flow to the entity beyond the current accounting period. In many instances, the economic benefits of volunteer services will be consumed as the services are acquired. In some cases, the volunteer services will contribute to the development of an asset and be included in the carrying amount of that asset.

B8

Entities may be recipients of volunteer services under voluntary or compulsory schemes operated in the public interest, for example:

(a) technical assistance from other governments or international organisations;

(b) persons convicted of offences who are required to perform community service for the entity;

(c) hospitals receiving the services of volunteers;

(d) schools receiving voluntary services from parents as teachers’ aides or as board members; and

(e) local governments receiving the services of volunteer firefighters.

B9

Entities may also be recipients of volunteer professional services that support their broader activities. For example, charities and religious organisations may receive free professional accounting or legal services.

B10

Government appropriations, which establish the authority to spend money for particular purposes, are a form of a transfer made voluntarily as the government is not compelled to make particular payments of amounts appropriated.

Recognition and measurement of income and related amounts (paragraphs 9–17)

B13

Any income recognised in accordance with paragraph 10 is strictly the residual of the difference between the fair value of the asset recognised and the consideration for that asset, after deducting any other related amounts described in paragraph 9. However, income is not recognised under paragraph 10 where another Standard addresses the accounting for the difference, such as the “day one gain/loss” requirements in AASB 9.

Refund obligations

B14

An entity typically has the ability, through its own actions, to avoid the circumstances that would give rise to a breach of conditions or requirements in an agreement necessitating a return of funds received. In such cases, liabilities recognised in accordance with other Standards do not include refund obligations that apply in the event of a breach, unless the breach has occurred or is expected to occur. For example, a grant agreement may require the funds provided to an entity to be spent only in a particular period, failing which repayment to the grantor will be required. As the entity has the discretion whether to spend funds received in advance of the specified period, a refund liability is not recognised unless the entity breaches the condition or a breach is expected.

Transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity

B15

An entity that receives a financial asset, such as cash, in a transfer to enable the entity to acquire or construct a recognisable non-financial asset to be controlled by the entity shall apply the requirements of AASB 9 to that financial asset. The acquisition or construction of the non-financial asset is accounted for separately to the transfer of the financial asset, in accordance with other Standards. If the non-financial asset is not permitted to be recognised by another Standard (eg knowledge or intellectual property developed through research, which cannot be recognised as an asset in accordance with AASB 138), paragraphs 15–17 do not apply. The key criterion is that the recognisable non-financial asset will be under the control of the entity (ie for its own use) – it will not be transferred to the transferor or other parties. Therefore, the transfer of the financial asset (or the relevant part) to the entity does not occur under a contract with a customer and is not subject to AASB 15. However, the recognisable non-financial asset could increase the entity’s ability or capacity to provide goods or services to other parties pursuant to other transactions, which are separate to the transfer that enabled the entity to acquire or construct the non-financial asset for its own use.

B16

On initial recognition of the financial asset, the entity recognises the requirement to acquire or construct the recognisable non-financial asset as an obligation and considers whether there are other conditions that give rise to performance obligations that require the entity to transfer goods or services to other entities (which are accounted for under AASB 15). The obligation to acquire or construct the non-financial asset is accounted for similarly to a performance obligation under AASB 15. For each obligation, the entity shall determine whether the obligation would be satisfied over time or at a point in time. If an entity does not satisfy an obligation over time, the obligation would be satisfied at a point in time.

B17

An entity shall apply a single method of measuring progress for each obligation satisfied over time and the entity shall apply that method consistently to similar obligations and in similar circumstances. At the end of each reporting period, an entity shall remeasure its progress towards complete satisfaction of each obligation that is satisfied over time, and shall recognise income over time on that basis.

Endowments

B18

An endowment is a transfer of an asset to an entity for the ongoing support of the entity’s objectives, and may (but not necessarily) be made as part of a bequest. An endowment may be made for the perpetual benefit of the entity in that the transfer is made with a requirement for the principal to be preserved, and only income earned on investment activity to be available for use in furthering the entity’s objectives.

B19

An endowment may include conditions pertaining to investment of the principal and the purpose to which investment income must be applied. For example, an endowment made to a university may be made on condition that the principal is invested and the investment income used for annual scholarships. An entity shall consider whether the conditions of the transfer give rise to any related contribution by owners, liabilities or revenue that is recognised at the same time as the entity recognises an asset. For example, an entity may determine the conditions give rise to a financial liability within the scope of AASB 9 for the obligation to provide a financial asset into the future, or a contract liability within the scope of AASB 15 for unperformed performance obligations relating to the transfer of goods or services under the terms of the endowment.

Bequests

B20

A bequest is a transfer made according to the provisions of a deceased person’s will. Whether the initial recognition of bequeathed items as assets in accordance with another Standard simultaneously gives rise to the recognition of income will depend on whether the entity recognises a liability, or other related amounts, as a result of the bequest. For example, the terms of a bequest may establish a contract between an entity and the estate that is within the scope of AASB 15 and give rise to a contract liability.

Provisions

Constructive obligations

B21

When an entity recognises an asset in accordance with another Australian Accounting Standard for consideration that is significantly less than fair value principally to enable the entity to further its objectives, the entity applies paragraph 9 to recognise any related amounts. When applying that paragraph, an entity considers whether a provision should be recognised in accordance with AASB 137 for a constructive obligation.

B21

When an entity recognises an asset in accordance with another Australian Accounting Standard for consideration that is significantly less than fair value principally to enable the entity to further its objectives, the entity applies paragraph 9 to recognise any related amounts. When applying that paragraph, an entity considers whether a provision should be recognised in accordance with AASB 137 for a constructive obligation.

B22

Critical to recognising a provision for a constructive obligation, an entity must demonstrate that its published policies, past practices or current statements are sufficiently specific to raise a valid expectation on the part of other parties that the entity will discharge its responsibilities under those policies, practices or statements. Determining whether an entity’s policies, practices or statements are sufficiently specific to create such an expectation among other parties is a matter of judgement. However, it is unlikely that an entity’s charter or stated objectives would satisfy the definition of a constructive obligation.

B23

An established pattern of past practices might also create a valid expectation among other parties that the entity will continue to adhere to those practices in the future. While entities might establish a general pattern for utilising assets received, they often do not adhere to those patterns to such a degree as to create a valid expectation among other parties.

Legal obligations

B24

Contractual terms (implicit or explicit), legislation or another operation of the law might create a legal non-financial obligation for an entity. In these circumstances an entity applies AASB 137 to recognise a provision, if any, arising from those legal obligations.

B24

Contractual terms (implicit or explicit), legislation or another operation of the law might create a legal non-financial obligation for an entity. In these circumstances an entity applies AASB 137 to recognise a provision, if any, arising from those legal obligations.

B25

Provisions might arise from terms included in a lease, such as an obligation to return or restore the leased asset in its original condition. Paragraphs 24 and 25 of AASB 16 provide guidance on accounting for an obligation to maintain, or restore, assets to conditions specified in a lease. Where such an obligation exists, the obligation is also accounted for in accordance with AASB 137.

Parliamentary appropriations as income

B26

The nature of parliamentary appropriations, and the circumstances that give rise to a government department’s recognition of such appropriations, can vary across different jurisdictions in Australia, and may vary for different types of appropriations within a particular jurisdiction. Similarly, the nature and content of appropriation legislation, the manner in which government departments’ activities are funded, and the mechanisms by which parliament and the government ensure that the government departments’ use of public funds is appropriate and consistent with government priorities as sanctioned by parliament, can change over time. Accordingly, the extent to which amounts appropriated for a government department’s use are recognised as income of a particular reporting period is determined by reference to the characteristics of the appropriation process and the circumstances in which the government department recognises appropriated amounts.

B27

For example, the parliamentary appropriation process currently adopted in some jurisdictions in Australia is such that the government departments do not gain control of funds appropriated for their use until obligations are incurred or expenditures are made by the government department. In these jurisdictions, appropriations recognised as income are in the nature of a recovery of costs incurred for the acquisition of goods and services or for amounts otherwise expended.

Non-contractual income arising from statutory requirements

B28

Taxes, rates and fines do not give rise to a contract liability or revenue recognised in accordance with AASB 15, even when they are raised in respect of specific goods or services. This is because the entity does not promise to provide goods or services in an agreement that creates obligations enforceable against the entity by legal or equivalent means.

Volunteer services (paragraphs 18–22)

B32

A not-for-profit entity that makes an accounting policy choice to recognise volunteer services under paragraph 19 shall only change its accounting policy if the change meets the criteria in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors (paragraph 14). That is, an entity can change an accounting policy only if the change:

(a) is required by an Australian Accounting Standard; or

(b) results in the financial statements providing reliable and more relevant information about the effects of transactions, other events or conditions on the entity’s financial position, financial performance or cash flows.

Appendix C-- Effective date and transition

This appendix is an integral part of the Standard.

Effective date

C1

An entity shall apply this Standard for annual reporting periods beginning on or after 1 January 2019. Earlier application is permitted provided that entities apply AASB 15 Revenue from Contracts with Customers to the same period. If an entity applies this Standard earlier, it shall disclose that fact.

C1A

Notwithstanding paragraph C1, an entity may elect not to apply this Standard to research grants until annual reporting periods beginning on or after 1 July 2019. If a not-for-profit entity applies this Standard to research grants prior to that, it shall also apply AASB 15 to research grants at the same time.

Transition

C2

For the purposes of the transition requirements in paragraphs C3–C12:

(a) the date of initial application is the beginning of the annual reporting period in which an entity first applies this Standard; and

(b) a completed contract is a contract or transaction for which the entity has recognised all of the income in accordance with AASB 1004 Contributions.

C3

An entity shall apply this Standard either:

(a) retrospectively to each prior reporting period presented in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors; or

(b) retrospectively with the cumulative effect of initially applying this Standard recognised at the date of initial application in accordance with paragraphs C6–C11.

C4

Notwithstanding the requirements of paragraph 28 of AASB 108, when this Standard is first applied, an entity need only present the quantitative information required by paragraph 28(f) of AASB 108 for the annual reporting period immediately preceding the first annual reporting period for which this Standard is applied (the ‘immediately preceding period’) and only if the entity applies this Standard retrospectively in accordance with paragraph C3(a). An entity may also present this information for the current period or for earlier comparative periods, but is not required to do so.

C5

When applying this Standard retrospectively in accordance with paragraph C3(a), as a practical expedient an entity need not restate completed contracts or transactions that:

(a) begin and end within the same annual reporting period; or

(b) are completed contracts or transactions at the beginning of the earliest period presented.

If an entity applies this expedient, it shall do so consistently to all completed contracts or transactions within all reporting periods presented and shall disclose the use of this expedient.

C6

If an entity elects to apply this Standard retrospectively in accordance with paragraph C3(b), the entity shall not restate comparative information. Instead, the entity shall recognise the cumulative effect of initially applying this Standard as an adjustment to the opening balance of retained earnings (or other component of equity, as appropriate) at the date of initial application. Under this transition method, an entity may elect to apply this Standard retrospectively only to contracts and transactions that are not completed contracts at the date of initial application.

C7

For the reporting period that includes the date of initial application, an entity shall provide both of the following additional disclosures if this Standard is applied retrospectively in accordance with paragraph C3(b):

(a) the amount by which each financial statement line item is affected in the current reporting period by the application of this Standard as compared to AASB 1004 Contributions before the change; and

(b) an explanation of the reasons for significant changes identified in paragraph C7(a).

Assets acquired for significantly less than fair value

C8

Assets acquired for consideration that was significantly less than fair value principally to enable the entity to further its objectives may have been measured on initial recognition under other Australian Accounting Standards at a cost that was significantly less than fair value. As a practical expedient, such assets are not required to be remeasured at fair value, whether the entity elects to apply this Standard retrospectively in accordance with paragraph C3(a) or C3(b).

Leases with significantly below-market terms and conditions

Leases classified as operating leases

C9

If an entity applies this Standard before applying AASB 16 Leases, and notwithstanding the requirements in paragraph C3, for leases that (1) at inception had significantly below-market terms and conditions principally to enable the entity to further its objectives and (2) were classified as operating leases in accordance with AASB 117 Leases, the entity shall not apply the requirements of this Standard to recognise any asset or income. Instead, the entity shall continue to apply its accounting policy under AASB 117 to those operating leases. On transition to AASB 16 Leases, the entity shall apply the transition requirements of that Standard to leases classified as operating leases in accordance with AASB 117.

Leases classified as finance leases

C10

If an entity elects to measure a class of right-of-use assets at initial recognition at fair value and applies this Standard before applying AASB 16, for leases that (1) at inception had significantly below-market terms and conditions principally to enable the entity to further its objectives and (2) were classified as finance leases in accordance with AASB 117, and if an entity elects to apply this Standard in accordance with:

(a) paragraph C3(a) – the entity shall:

(i) measure each leased asset in the class at fair value at the beginning of the earliest period presented;

(ii) measure the lease liability in accordance with AASB 117;

(iii) recognise any related items in accordance with paragraph 9; and

(iv) recognise any income arising as an adjustment to the opening balance of retained earnings (or other component of equity, as appropriate) at the beginning of the earliest period presented; or

(b) paragraph C3(b) – the entity shall:

(i) measure each leased asset in the class at fair value at the date of initial application of this Standard;

(ii) measure the lease liability in accordance with AASB 117;

(iii) recognise any related items in accordance with paragraph 9; and

(iv) recognise any income arising as an adjustment to the opening balance of retained earnings (or other component of equity, as appropriate) at the date of initial application of this Standard.

C10A

If an entity elects not to measure a class of right-of-use assets at initial recognition at fair value and applies this Standard before applying AASB 16, for leases that (1) at inception had significantly below-market terms and conditions principally to enable the entity to further its objectives and (2) were classified as finance leases in accordance with AASB 117, the entity shall continue to apply its accounting policy under AASB 117 to those finance leases. On transition to AASB 16, the entity shall apply the transition requirements of that Standard to leases classified as finance leases in accordance with AASB 117.

C11

An entity applying paragraph C10 may, as a practical expedient, apply the paragraph to a portfolio of leases with similar characteristics if the entity reasonably expects that the effects on the financial statements of this approach would not differ materially from applying paragraph C10 to the individual leases within that portfolio. If accounting for a portfolio, an entity shall use estimates and assumptions that reflect the size and composition of the portfolio.

Appendix E -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusE1

Paragraphs 23–41 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Illustrative examples

These illustrative examples accompany, but are not part of, AASB 1058. They illustrate aspects of AASB 1058, but are not intended to provide interpretative guidance.

IE1

The following examples portray hypothetical situations. They are intended to illustrate how a not-for-profit entity might apply some of the requirements of AASB 1058 Income of Not-for-Profit Entities to particular types of transactions, on the basis of the limited facts presented. Although some aspects of the examples might be present in actual fact patterns, all relevant facts and circumstances of a particular fact pattern need to be evaluated when applying AASB 1058.

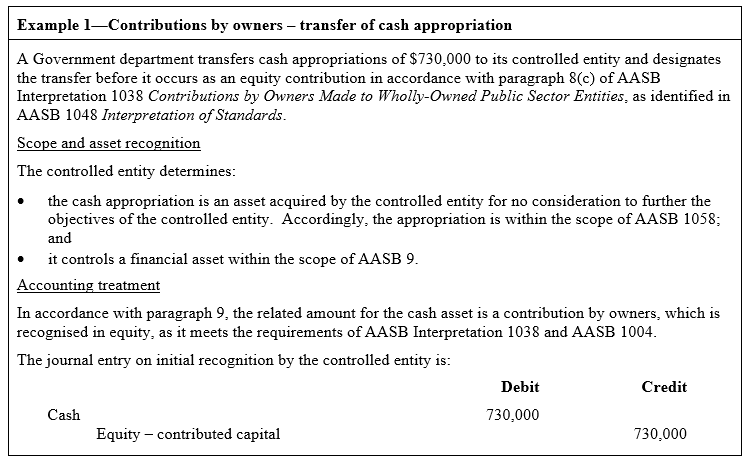

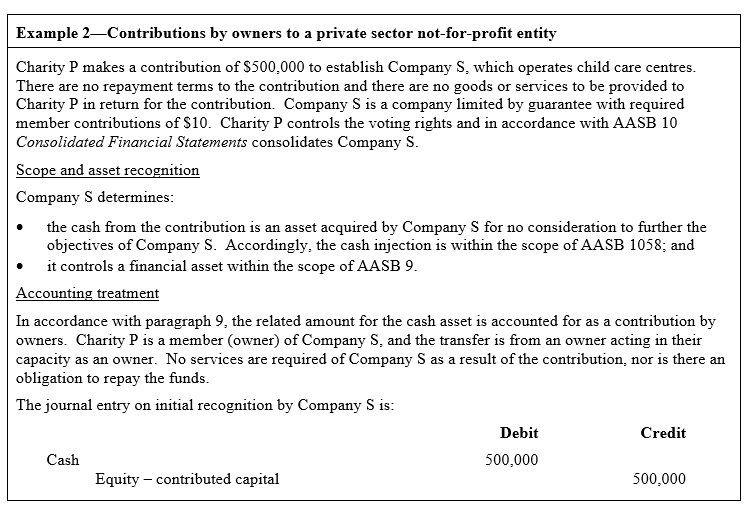

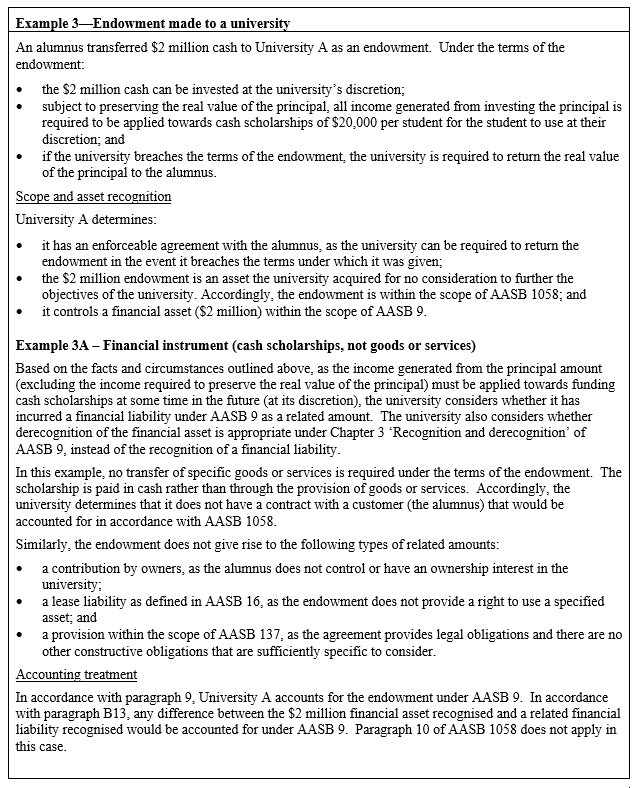

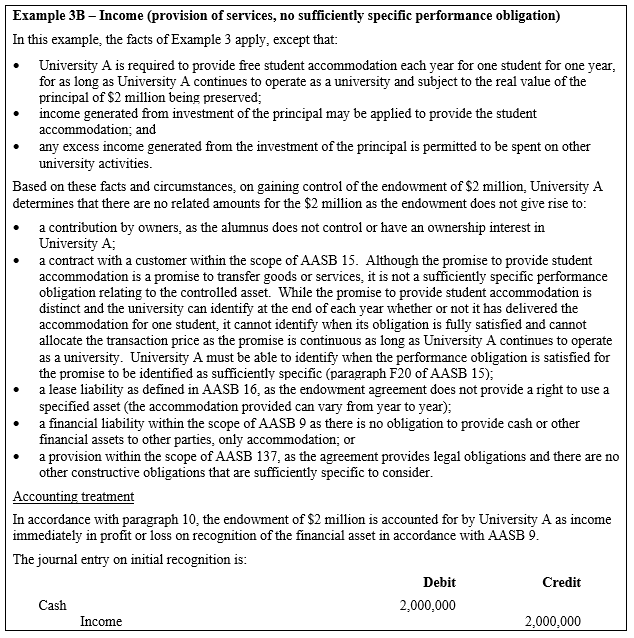

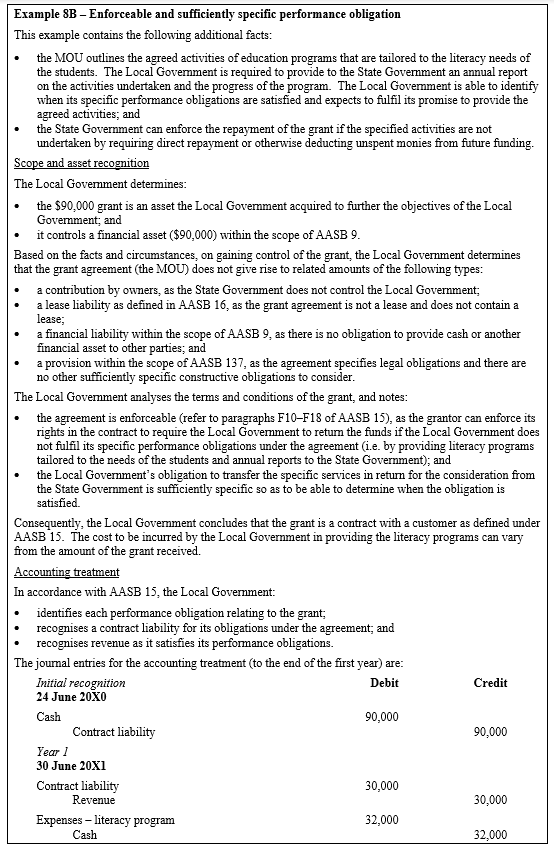

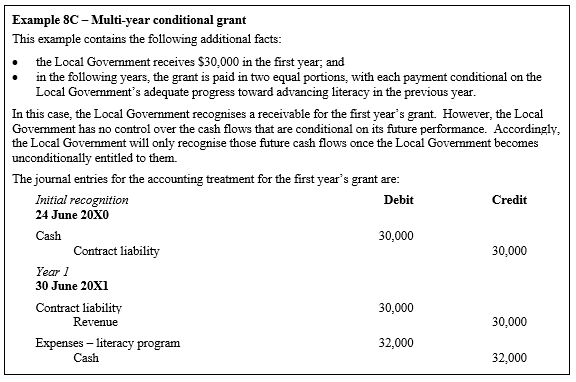

Recognition and measurement of income and related amounts (paragraphs 9–22)

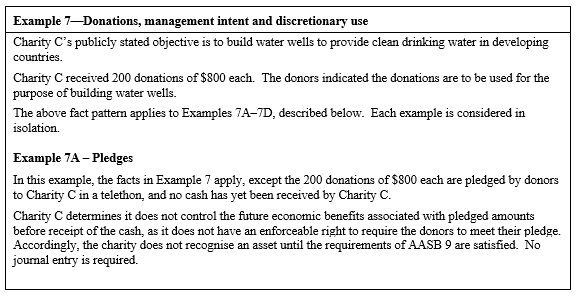

IE2

Examples 1–8 illustrate the requirements in AASB 1058 for identifying related amounts and income to be recognised in accordance with paragraphs 9 and 10 on the initial recognition of an asset. The following requirements are illustrated in the examples in identifying related amounts in the form of:

(a) contributions by owners, in accordance with AASB 1004;

(b) a financial instrument, in accordance with AASB 9;

(c) a lease liability arising in a lease contract, in accordance with AASB 16; and

(d) revenue or a contract liability arising from a contract with a customer, in accordance with AASB 15.

Contributions by owners

Financial instruments, bequests and endowments

IE3

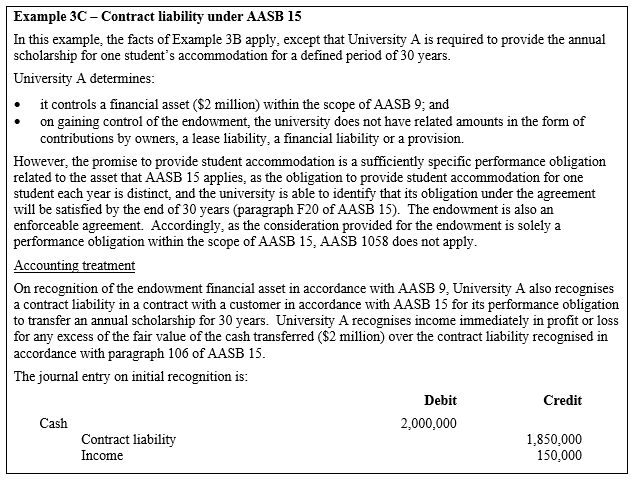

Examples 3 and 4 illustrate the requirements of paragraphs 9 and 10 in AASB 1058 for the accounting treatment for financial instruments, bequests and endowments. Examples 3A and 4 illustrate the identification of related amounts in the form of a financial instrument, in accordance with AASB 9. Receiving a bequest or endowment in the form of cash, or paying out the principal and/or interest in the form of cash, requires the application of the financial instrument accounting requirements in AASB 9.

Leases

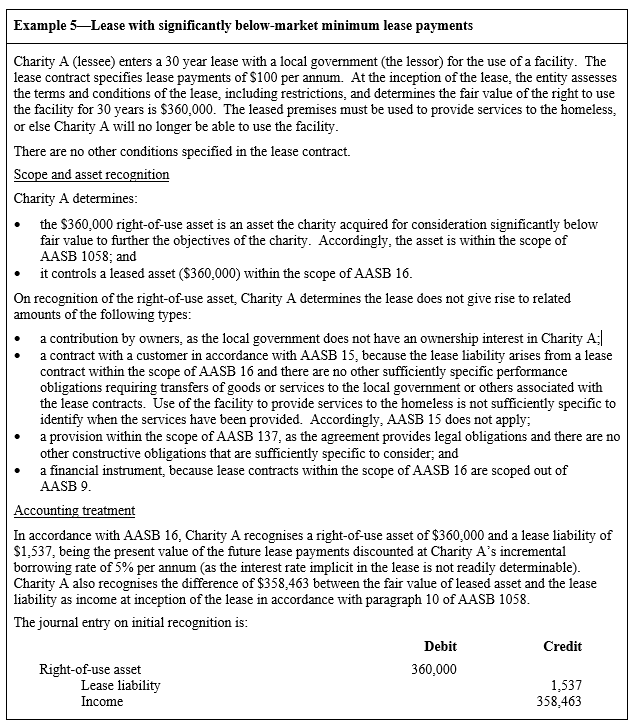

IE4

Example 5 illustrates the requirements in AASB 1058 regarding the recognition of a lease liability in accordance with AASB 16.

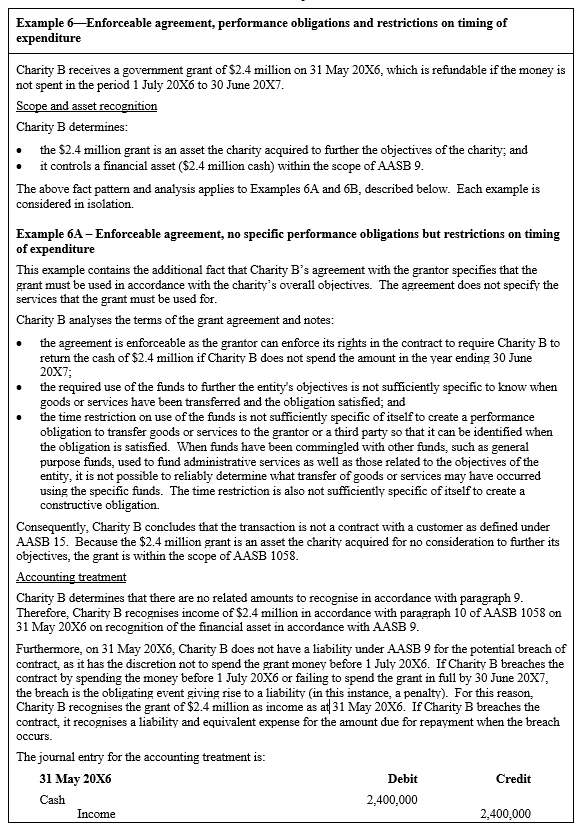

Contract with a customer – revenue and income

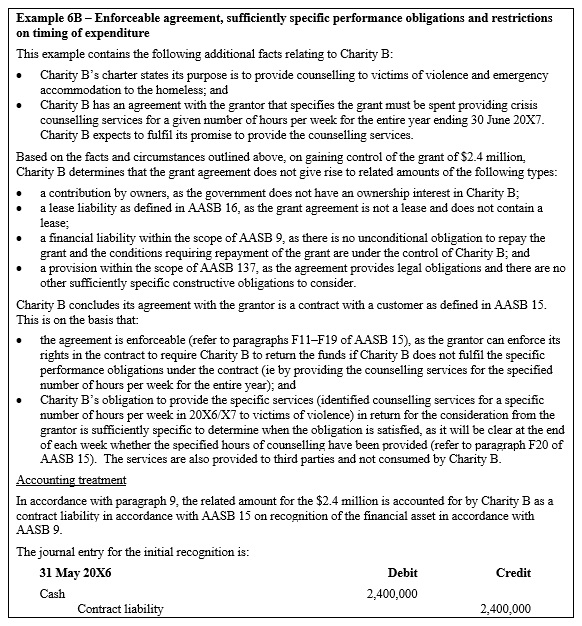

IE5

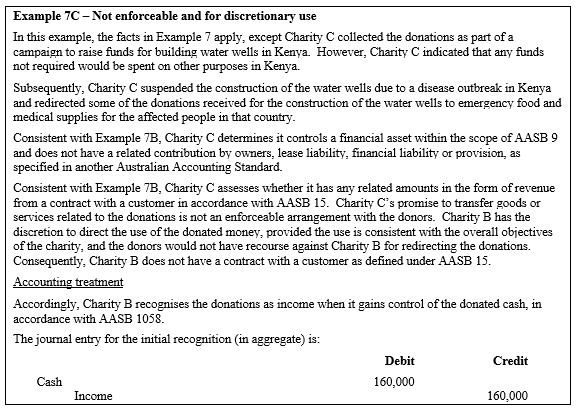

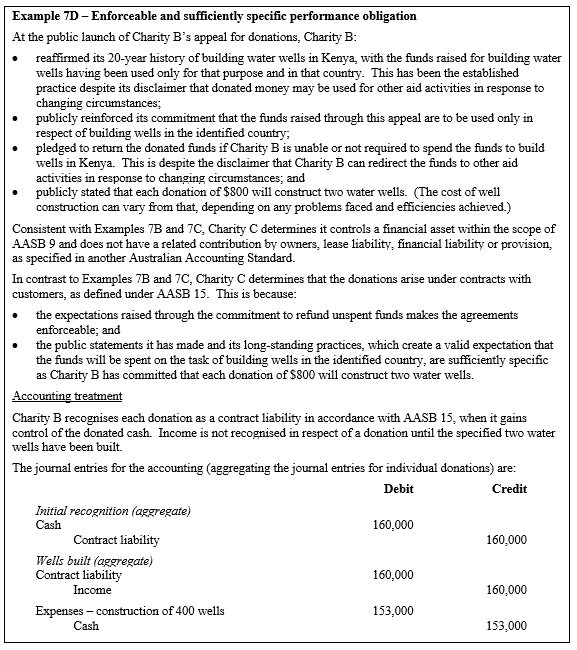

Examples 6–8 illustrate the requirements in AASB 1058 regarding recognition of revenue and a contract liability in accordance with AASB 15. To be in the scope of AASB 15, the contract must:

(a) be enforceable;

(b) contain performance obligations to transfers goods or services to another party that are sufficiently specific to enable determination of when the obligation has been satisfied; and

(c) not result in the goods or services specified being retained by the entity, ie the goods or services will be transferred to the customer or to other parties on behalf of the customer.

Transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity (paragraphs 15–17)

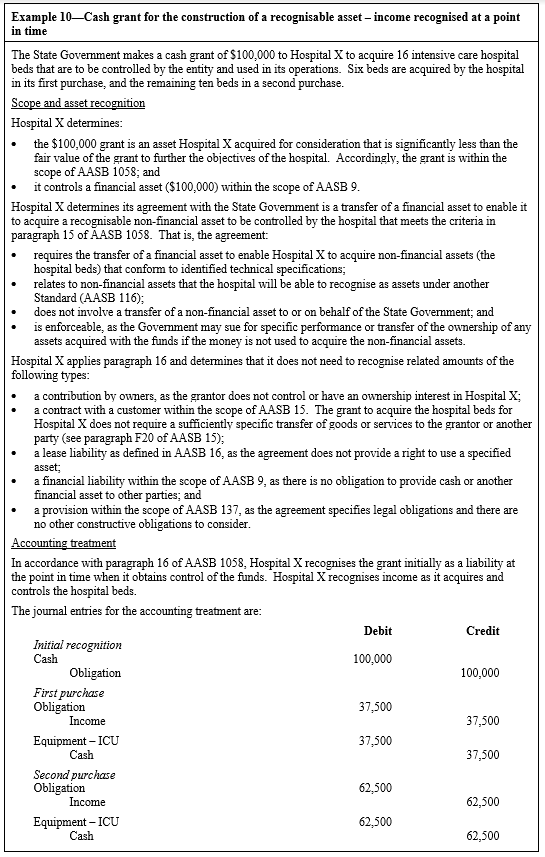

IE6

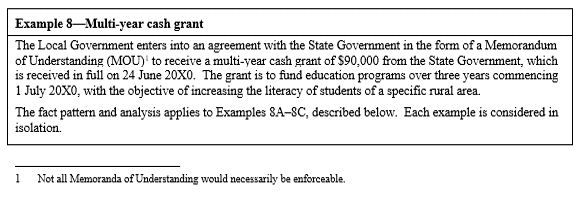

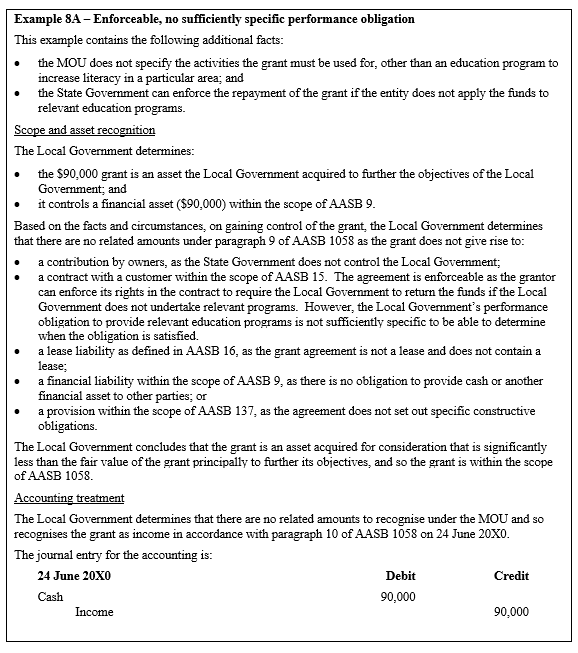

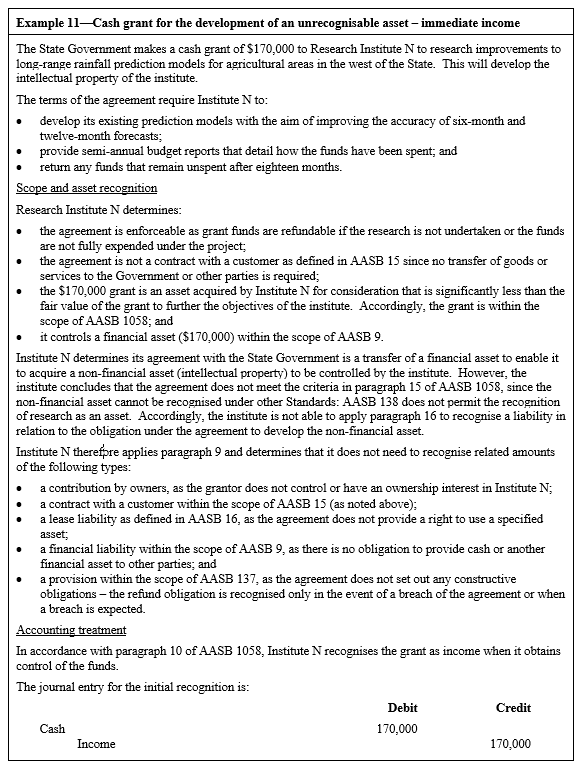

Examples 9 and 10 illustrate the requirements in AASB 1058 regarding a transfer of a financial asset to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity, and when revenue is recognised. Example 11 illustrates a transfer to enable an entity to develop a non-financial asset that cannot be recognised under Australian Accounting Standards, and hence does not meet the criteria for the accounting for transfers of financial assets set out in paragraphs 15–17.

Volunteer services (paragraphs 18–22)

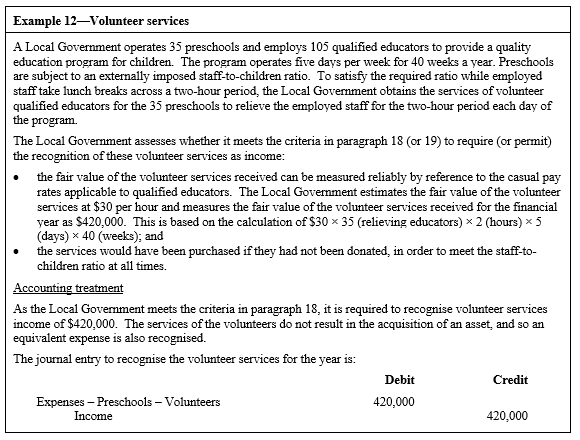

IE7

Example 12 illustrates the requirements in AASB 1058 for recognising the receipt of volunteer services as income and as an asset or an expense.

Disclosure

Restrictions (paragraph 37)

IE8

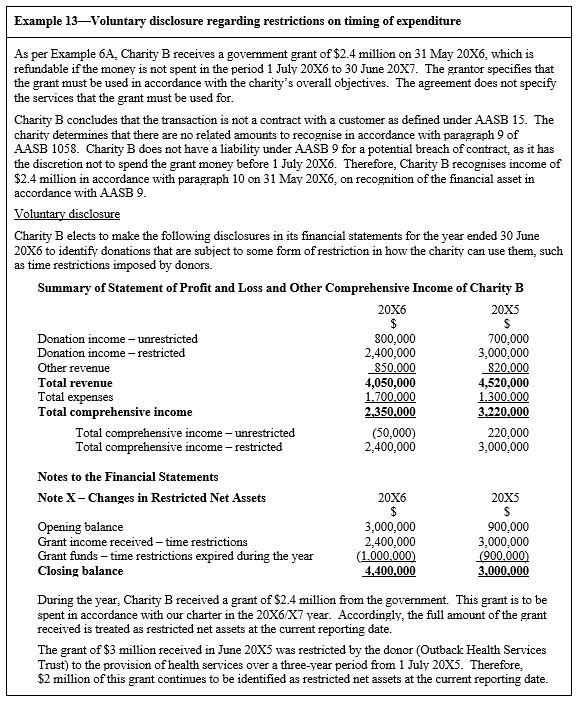

Example 13 illustrates disclosures about externally imposed restrictions that limit or direct the purpose for which resources controlled by an entity may be used. Such disclosures are encouraged by this Standard but not required. This example extends Example 6A to illustrate possible disclosures about time restrictions on the expenditure of grant monies received. This example illustrates voluntary disclosures about restricted and unrestricted donation income in the Statement of Profit and Loss and Other Comprehensive Income, as well as disclosures relating to restricted net assets. Example 7B also illustrates voluntary disclosures of restrictions.

Transition (paragraphs C2–C7)

IE9

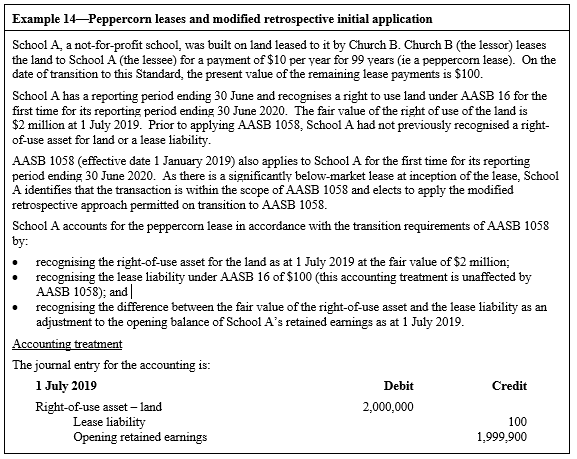

Example 14 illustrates the modified retrospective initial application of this Standard to peppercorn leases.

Compilation details

Accounting Standard AASB 1058 Income of Not-for-Profit Entities (as amended)

Compilation details are not part of AASB 1058.

This compiled Standard applies to annual periods beginning on or after 1 July 2021 but before 1 January 2023. It takes into account amendments up to and including 6 March 2020 and was prepared on 21 July 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1058 (December 2016) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments