The purpose of this Standard is to specify the manner of accounting for general insurance contracts consistent with AASB 4, specify certain aspects of accounting for assets backing general insurance liabilities, specify certain aspects of accounting for non-insurance contracts and require disclosure of information relating to general insurance contracts.

Preamble

Pronouncement

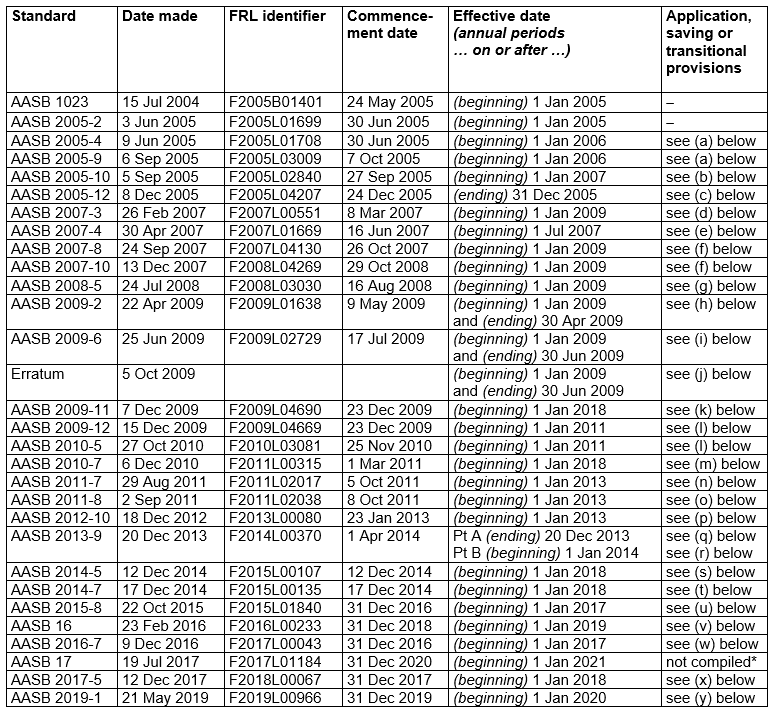

This compiled Standard applies to annual reporting periods beginning on or after 1 January 2020 but before 1 January 2021. Earlier application is permitted for annual reporting periods beginning after 24 July 2014 but before 1 January 2020. It incorporates relevant amendments made up to and including 21 May 2019.

Prepared on 2 March 2020 by the staff of the Australian Accounting Standards Board.

Compilation no. 16

Compilation date: 31 December 2019

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2020

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

Australian Accounting Standard AASB 1023 General Insurance Contracts (as amended) is set out in paragraphs 1.1 – 19.2 and Appendix A. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in this Standard are in italics the first time they appear in the Standard. AASB 1023 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IFRS 4

AASB 1023 General Insurance Contracts as amended incorporates the limited improvements to accounting for insurance contracts required by IFRS 4 Insurance Contracts.

General insurers applying this Standard and Australian Accounting Standards will be compliant with IFRS Standards.

IFRS 4 is implemented in Australia using three Accounting Standards:

(a) AASB 4 Insurance Contracts (the Australian equivalent to IFRS 4), which applies to fixed-fee service contracts that meet the definition of an insurance contract;

(b) AASB 1023, which applies to general insurance contracts; and

(c) AASB 1038 Life Insurance Contracts, which applies to life insurance contracts.

IFRS 4 applies to all insurance contracts and financial instruments with discretionary participation features, whereas AASB 1023 only applies to general insurance contracts as well as certain aspects of accounting for assets that back general insurance liabilities. Whereas IFRS 4 includes only limited improvements to accounting for insurance contracts and disclosure requirements, AASB 1023 addresses all aspects of the recognition, measurement and disclosure of general insurance contracts.

IFRS 4 allows insurers to use a practice described as “shadow accounting”. AASB 1023 does not allow shadow accounting.

Accounting Standard AASB 1023

The Australian Accounting Standards Board made Accounting Standard AASB 1023 General Insurance Contracts under section 334 of the Corporations Act 2001 on 15 July 2004.

This compiled version of AASB 1023 applies to annual reporting periods beginning on or after 1 January 2020 but before 1 January 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 21 May 2019 (see Compilation Details).

1 Application

1.1

This Standard applies to:

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other reporting entity; and

(c) financial statements that are, or are held out to be, general purpose financial statements.

AusCF1

AusCF paragraphs included in this Standard apply only to:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

Such entities are referred to as ‘AusCF entities’. For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting (as set out in paragraph Aus1.1 of the Conceptual Framework) shall not apply AusCF paragraphs.

1.2

This Standard applies to annual reporting periods beginning on or after 1 January 2005.

[Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

1.3

This Standard shall not be applied to annual reporting periods beginning before 1 January 2005.

1.4

[Deleted by the AASB]

1.4.1

[Deleted by the AASB]

1.4.2

For the purposes of AASB 134 Interim Financial Reporting, the determination of the outstanding claims liability does not necessarily require a full actuarial valuation. In accordance with AASB 134, the outstanding claims liability would need to be determined on a reliable basis, would be based on reasonable estimates, would include a full review of all assumptions, and would not be materially different from the outstanding claims liability determined by a full actuarial valuation.

1.5

When applicable, this Standard supersedes:

(a) Accounting Standard AASB 1023 Financial Reporting of General Insurance Activities as approved by notice published in the Commonwealth of Australia Gazette No S 415, 6 November 1996; and

(b) AAS 26 Financial Reporting of General Insurance Activities issued in November 1996.

1.6

Both AASB 1023 (issued in November 1996) and AAS 26 remain applicable until superseded by this Standard.

1.7

Notice of this Standard was published in the Commonwealth of Australia Gazette No S 294, 22 July 2004.

2 Scope

General Insurance Contracts

2.1

This Standard applies to:

(a) general insurance contracts (including general reinsurance contracts) that a general insurer issues and to general reinsurance contracts that it holds;

(b) certain assets backing general insurance liabilities;

(c) financial liabilities and financial assets that arise under non-insurance contracts; and

(d) certain assets backing financial liabilities that arise under non-insurance contracts.

2.1.1

There are various types of insurance contract. This Standard deals with general insurance contracts (including general reinsurance contracts). General insurance contracts are defined as insurance contracts that are not life insurance contracts.

2.1.2

This Standard applies to general insurance contracts issued by Registered Health Benefits Organisations (RHBOs) registered under the National Health Act 1953. RHBOs apply this Standard to contracts that meet the definition of a general insurance contract and to certain assets backing general insurance liabilities.

2.1.3

For ease of reference, this Standard describes any entity that issues an insurance contract as an insurer, whether or not the issuer is regarded as an insurer for legal, regulatory or supervisory purposes.

2.1.4

A reinsurance contract is a type of insurance contract. Accordingly, all references in this Standard to insurance contracts also apply to reinsurance contracts.

2.1.5

Weather derivatives that meet the definition of a general insurance contract under this Standard are treated under this Standard. A contract that requires payment based on climatic, geological or other physical variables only where there is an adverse effect on the contract holder is a weather derivative that is an insurance contract. To meet the definition of a general insurance contract, the physical variable specified in the contract will be specific to a party to the contract.

Transactions Outside the Scope of this Standard

2.2

This Standard does not apply to:

(a) life insurance contracts (see AASB 1038 Life Insurance Contracts);

(b) product warranties issued directly by a manufacturer, dealer or retailer (see AASB 15 Revenue from Contracts with Customers and AASB 137 Provisions, Contingent Liabilities and Contingent Assets);

(c) employers’ assets and liabilities under employee benefit plans (see AASB 119 Employee Benefits and AASB 2 Share-based Payment) and retirement benefit obligations reported by defined benefit retirement plans (see AASB 1056 Superannuation Entities);

(d) contingent consideration payable or receivable in a business combination (see AASB 3 Business Combinations);

(e) contractual rights or contractual obligations that are contingent on the future use of, or right to use, a non-financial item (for example, some license fees, royalties, variable lease payments and similar items), as well as a lessee’s residual value guarantee embedded in a lease (see AASB 15, AASB 16 Leases and AASB 138 Intangible Assets);

(f) financial guarantee contracts unless the issuer has previously asserted explicitly that it regards such contracts as insurance contracts and has used accounting applicable to insurance contracts, in which case the issuer may elect to apply either AASB 9 Financial Instruments, AASB 132 Financial Instruments: Presentation and AASB 7 Financial Instruments: Disclosures or this Standard to such financial guarantee contracts. The issuer may make that election contract by contract, but the election for each contract is irrevocable;

(g) direct insurance contracts that the entity holds (that is direct insurance contracts in which the entity is a policyholder). However, a cedant shall apply this Standard to reinsurance contracts that it holds; and

(h) fixed-fee service contracts, that meet the definition of an insurance contract, if the level of service depends on an uncertain event, for example maintenance contracts or roadside assistance contracts (see AASB 4 Insurance Contracts).

Embedded Derivatives

2.3.1

AASB 9 Financial Instruments requires hybrid contracts that contain financial asset hosts to be classified and measured in their entirety in accordance with the requirements in paragraphs 4.1.1-4.1.5 of that Standard. However, AASB 9 requires an entity to separate some embedded derivatives from their financial liability hosts, measure them at fair value and include changes in their fair value in the statement of comprehensive income. AASB 9 applies to derivatives embedded in a general insurance contract unless the embedded derivative is itself a general insurance contract.

2.3.2

As an exception to the requirement in AASB 9, an insurer need not separate, and measure at fair value, a policyholder’s option to surrender an insurance contract for a fixed amount (or for an amount based on a fixed amount and an interest rate) even if the exercise price differs from the carrying amount of the host insurance liability. However, the requirement in AASB 9 applies to a put option or cash surrender option embedded in an insurance contract if the surrender value varies in response to the change in a financial variable (such as an equity or commodity price or index), or a non-financial variable that is not specific to a party to the contract. Furthermore, that requirement also applies if the holder’s ability to exercise a put option or cash surrender option is triggered by a change in such a variable (for example, a put option that can be exercised if a stock market index reaches a specified level).

Deposit Components

2.4.1

Some general insurance contracts contain both an insurance component and a deposit component. In some cases, an insurer is required or permitted to unbundle those components.

(a) Unbundling is required if both the following conditions are met:

(i) the insurer can measure the deposit component (including any embedded surrender options) separately (that is, without considering the insurance component); and

(ii) the insurer’s accounting policies do not otherwise require it to recognise all obligations and rights arising from the deposit component.

(b) Unbundling is permitted, but not required, if the insurer can measure the deposit component separately as in paragraph 2.4.1(a)(i) but its accounting policies require it to recognise all obligations and rights arising from the deposit component, regardless of the basis used to measure those rights and obligations.

(c) Unbundling is prohibited if an insurer cannot measure the deposit component separately as in paragraph 2.4.1(a)(i).

2.4.2

The following is an example of a case when an insurer’s accounting policies do not require it to recognise all obligations arising from a deposit component. A cedant receives compensation for losses from a reinsurer, but the contract obliges the cedant to repay the compensation in future years. That obligation arises from a deposit component. If the cedant’s accounting policies would otherwise permit it to recognise the compensation as income without recognising the resulting obligation, unbundling is required.

2.4.3

A general insurer, in considering the need to unbundle the deposit component of the general insurance contract, would consider all expected cash flows over the period of the contract and would consider the substance of the contract. For example, while some financial reinsurance contracts may require annual renewal, in substance they may be expected to be renewed for a number of years.

2.4.4

To unbundle a general insurance contract, an insurer shall:

(a) apply this Standard to the insurance component; and

(b) apply AASB 9 to the deposit component. When applying AASB 9, an insurer shall designate the deposit component as “at fair value through profit or loss”, on first application of this Standard or on initial recognition of the deposit component.

3 Purpose of Standard

3.1

The purpose of this Standard is to:

(a) specify the manner of accounting for general insurance contracts consistent with AASB 4;

(b) specify certain aspects of accounting for assets backing general insurance liabilities;

(c) specify certain aspects of accounting for non-insurance contracts; and

(d) require disclosure of information relating to general insurance contracts.

5 Outstanding Claims Liability

Recognition and Measurement

5.1

An outstanding claims liability shall be recognised in respect of direct business and reinsurance business and shall be measured as the central estimate of the present value of the expected future payments for claims incurred with an additional risk margin to allow for the inherent uncertainty in the central estimate.

5.1.1

The recognition and measurement approach requires estimation of the probability-weighted expected cost (discounted to a present value) of settling claims incurred, and the addition of a risk margin to reflect inherent uncertainty in the central estimate.

5.1.2

The longer the expected period from the end of the reporting period to settlement, the more likely it is that the ultimate cost of settlement will be affected by inflationary factors likely to occur during the period to settlement. These factors include changes in specific price levels, for example, trends in average periods of incapacity and in the amounts of court awards for successful claims. For claims expected to be settled within one year of the end of the reporting period, the impact of inflationary factors might not be material.

5.1.3

For claims expected to be settled within one year of the end of the reporting period, where the amount of the expected future payments does not differ materially from the present value of those payments, insurers would not need to discount the expected future payments.

Central Estimate

5.1.4

In estimating the outstanding claims liability, a central estimate is adopted. If all the possible values of the outstanding claims liability are expressed as a statistical distribution, the central estimate is the mean of that distribution.

5.1.5

In estimating the outstanding claims liability, an insurer may make use of case estimates of individual reported claims that remain unsettled at the end of the reporting period. An insurer may base case estimates on the most likely claim costs. Where the range in potential outcomes is small, the likely cost may be close to the mean cost. However, where the potential range in outcomes is large and where the probability distribution may be highly skewed, the most likely cost, or the mode, could be below the mean and hence below the central estimate. In this situation, the insurer would need to increase the case estimates accordingly to ensure that they represent the central estimate.

Risk Margin

5.1.6

The outstanding claims liability includes, in addition to the central estimate of the present value of the expected future payments, a risk margin that relates to the inherent uncertainty in the central estimate of the present value of the expected future payments.

5.1.7

Risk margins are determined on a basis that reflects the insurer’s business. Regard is had to the robustness of the valuation models, the reliability and volume of available data, past experience of the insurer and the industry and the characteristics of the classes of business written.

5.1.8

The risk margin is applied to the net outstanding claims for the entity as a whole. The overall net uncertainty has regard to:

(a) the uncertainty in the gross outstanding claims liability;

(b) the effect of reinsurance on (a); and

(c) the uncertainty in reinsurance and other recoveries due.

5.1.9

In practice, however, outstanding claims liabilities are often estimated on a class-by-class basis, including an assessment of the uncertainty in each class and the determination of a risk margin by class of business. When these estimates are combined for all classes, the central estimates are combined, however the risk margin for all classes when aggregated may be determined by some insurers to be less than the sum of the individual risk margins. The extent of the difference that some insurers may decide to recognise is likely to depend upon the degree of diversification between the different classes and the degree of correlation between the experiences of these classes.

5.1.10

For the purposes of the liability adequacy test, required by section 9, the risk margin for the entity as a whole is apportioned across portfolios of contracts that are subject to broadly similar risks and are managed together as a single portfolio.

5.1.11

Risk margins adopted for regulatory purposes may be appropriate risk margins for the purposes of this Standard, or they may be an appropriate starting point in determining such risk margins.

Expected Future Payments

5.2

The expected future payments shall include:

(a) amounts in relation to unpaid reported claims;

(b) claims incurred but not reported (IBNR);

(c) claims incurred but not enough reported (IBNER); and

(d) costs, including claims handling costs, which the insurer expects to incur in settling these incurred claims.

5.2.1

It is important to identify the components of the ultimate cost to an insurer of settling incurred claims, for the purposes of determining the claims expense for the reporting period and determining the outstanding claims liability as at the end of the reporting period. These components comprise the policy benefit amounts required to be paid to or on behalf of those insured, and claims handling costs, that is, costs associated with achieving settlements with those insured. Claims handling costs include costs that can be associated directly with individual claims, such as legal and other professional fees, and costs that can only be indirectly associated with individual claims, such as claims administration costs.

5.2.2

Policy benefit amounts and direct claims handling costs are expenses of an insurer, representing the consumption or loss of economic benefits. The outstanding claims liability includes unpaid policy benefits and direct claims handling costs relating to claims arising during current and prior reporting periods, as they are outgoings that an insurer is presently obliged to meet as a result of past events.

5.2.3

Indirect claims handling costs incurred during the reporting period are also expenses of an insurer, and include a portion of the indirect claims handling costs to be paid in the future, being that portion which relates to handling claims incurred during the reporting period. The outstanding claims liability includes these unpaid indirect claims handling costs.

5.2.4

It is important to ensure that claims are recognised as expenses and liabilities for the correct reporting period. For contracts written on a claims incurred basis, claims arise from insured events that occur during the insurance contract period. Some events will occur and give rise to claims that are reported to the insurer and settled within the same reporting period. Other reported claims may be unsettled at the end of a particular reporting period. In addition, there may be events that give rise to claims that, at the end of a reporting period, have yet to be reported to the insurer. The latter are termed claims incurred but not reported (IBNR claims). The insurer also considers the need to recognise a liability for claims that may be re-opened after the reporting period.

5.2.5

For contracts written on a claims made basis, claims arise in respect of claims reported during the insurance contract period. The insured event that gave rise to the claim could have occurred in a previous period. While claims made insurance contracts should theoretically only give rise to outstanding claims liabilities and IBNER claims (see paragraph 5.2.10), as claims cannot be incurred but not reported under such a contract, this may not be the case for reinsurers. A reinsurer may have reinsured a claims made contract on a claims incurred basis. In this case whilst a loss or other event would be reported to the direct insurer during the period of insurance to generate a valid claim, the reinsurer may not have received information about the claim but would have an IBNR liability. Similarly, a reinsurer may have issued a claims made reinsurance contract but may need to consider that not all notices of claims may have been reported by the direct insurer. Insurers and reinsurers should also consider court rulings that may impact on the way claims made contracts are interpreted.

5.2.6

Claims arising from events that occur during a reporting period and which are settled during that same period are expenses of that period. In addition, a liability and corresponding expense is recognised for reported claims arising from events of the reporting period that have yet to be settled. This involves a process of estimation that includes assessment of individual claims and past claims experience.

5.2.7

When, based on knowledge of the business, IBNR claims are expected to exist, an estimate is made of the amount of the claims that will arise therefrom. This involves recognition of a liability and corresponding expense for the reporting period. As in the case of reported but unsettled claims, an estimate of the amount of the current claims incurred but not reported is based on past experience and takes into account any changes in circumstances, such as recent catastrophic events that may have occurred during the reporting period and changes in the volume or mix of insurance contracts underwritten, that may affect the pattern of unreported claims.

5.2.8

Some insurers use estimations or formulae, related to the amount of outstanding claims and based on the past experience of the insurer and the industry, to arrive at an estimate of direct and indirect claims handling costs.

5.2.9

Claims expense and the outstanding claims liability are adjusted on the basis of information, including re-opened claims, that becomes available after the initial recognition of claims, to enable the insurer to make a more accurate estimate of the ultimate cost of settlement. This is often referred to as claims development. As is the case with other liabilities, the effect of the adjustments to the liability for outstanding claims and to claims expense is recognised in the statement of comprehensive income when the information becomes available.

5.2.10

Where further information becomes available about reported claims and reveals that the ultimate cost of settling claims has been under-estimated, the upwards adjustment to claims expense and to the liability for outstanding claims is often referred to as claims incurred but not enough reported (IBNER claims). Where further information reveals that the ultimate cost of settling claims has been over-estimated, the adjustment is sometimes referred to as negative IBNER claims.

5.2.11

Appropriate allowance is made for future claim cost escalation when determining the central estimate of the present value of the expected future payments. Future claims payments may increase over current levels as a result of wage or price inflation, and as a result of superimposed inflation (cost increases) due to court awards, environmental factors or economic or other causes.

5.2.12

With inwards reinsurance claims the reinsurer will receive periodic advices from each cedant. These may include aggregate information relating to the claims liability. The reinsurer measures its outstanding claims liability on the basis of this information and its past experience of the claims payments made under reinsurance arrangements. The reinsurer also considers market knowledge of losses and other events such as hailstorms or earthquakes.

6 Discount Rates

6.1

The outstanding claims liability shall be discounted for the time value of money using risk-free discount rates that are based on current observable, objective rates that relate to the nature, structure and term of the future obligations.

6.1.1

The discount rates adopted are not intended to reflect risks inherent in the liability cash flows, which might be allowed for by a reduction in the discount rate in a fair value measurement, nor are they intended to reflect the insurance and other non-financial risks and uncertainties reflected in the outstanding claims liability. The discount rates are not intended to include allowance for the cost of any options or guarantees that are separately measured within the outstanding claims liability.

6.1.2

Typically, government bond rates may be appropriate discount rates for the purposes of this Standard, or they may be an appropriate starting point in determining such discount rates.

6.1.3

The portion of the increase in the liability for outstanding claims from the end of the previous reporting period to the end of the current reporting period which is due to discounted claims not yet settled being one period closer to settlement, ought, conceptually, to be recognised as interest expense of the current reporting period. However, it is considered that the costs of distinguishing this component of the increase in the outstanding claims liability exceed the benefits that may be gained from its disclosure. Thus, such increase is included in claims expense for the current reporting period.

8 Acquisition Costs

8.1

Acquisition costs incurred in obtaining and recording general insurance contracts shall be deferred and recognised as assets where they can be reliably measured and where it is probable that they will give rise to premium revenue that will be recognised in the statement of comprehensive income in subsequent reporting periods. Deferred acquisition costs shall be amortised systematically in accordance with the expected pattern of the incidence of risk under the related general insurance contracts.

8.1.1

Acquisition costs are incurred in obtaining and recording general insurance contracts. They include commission or brokerage paid to agents or brokers for obtaining business for the insurer, selling and underwriting costs such as advertising and risk assessment, the administrative costs of recording policy information and premium collection costs.

8.1.2

Because such costs are usually incurred at acquisition whilst the pattern of earnings occurs throughout the contract periods, which may extend beyond the end of the reporting period, those acquisition costs which lead to obtaining future benefits for the insurer are recognised as assets.

8.1.3

For an asset to be recognised, it will be probable that the future economic benefits will eventuate, and that it possesses a cost or other value that can be measured reliably. Direct acquisition costs such as commission or brokerage are readily measurable. However, it may be difficult to reliably measure indirect costs that give rise to premium revenue, such as administration costs, because it is difficult to associate them with particular insurance contracts.

9 Liability Adequacy Test

9.1

The adequacy of the unearned premium liability shall be assessed by considering current estimates of the present value of the expected future cash flows relating to future claims arising from the rights and obligations under current general insurance contracts. If the present value of the expected future cash flows relating to future claims arising from the rights and obligations under current general insurance contracts, plus an additional risk margin to reflect the inherent uncertainty in the central estimate, exceed the unearned premium liability less related intangible assets and related deferred acquisition costs, then the unearned premium liability is deficient. The entire deficiency shall be recognised in the statement of comprehensive income. In recognising the deficiency in the statement of comprehensive income the insurer shall first write-down any related intangible assets and then the related deferred acquisition costs. If an additional liability is required this shall be recognised in the statement of financial position as an unexpired risk liability. The liability adequacy test for the unearned premium liability shall be performed at the level of a portfolio of contracts that are subject to broadly similar risks and are managed together as a single portfolio.

9.1.1

In determining the present value of the expected future cash flows relating to future claims arising from the rights and obligations under current general insurance contracts, the insurer applies sections 5 and 6 and includes an appropriate risk margin to reflect inherent uncertainty in the central estimate, as set out in paragraphs 5.1.6 to 5.1.11.

9.1.2

Whilst the probability of adequacy adopted in performing the liability adequacy test may be the same or similar to the probability of adequacy adopted in determining the outstanding claims liability, this Standard does not require the same or similar probabilities of adequacy. However, the users of financial statements need to be presented with information explaining any differences in probabilities of adequacy adopted, and insurers are required to disclose the reasons for any differences in accordance with paragraph 17.8(e).

9.1.3

The unearned premium liability may include premiums in advance as described in paragraph 4.2.5. Insurers also consider whether there are any additional general insurance contracts, where the premium revenue is not recognised in the unearned premium liability, under which the insurer has a constructive obligation to settle future claims that may arise. That is, there may be general insurance contracts where there has not been a transfer of risk, as described in paragraph 4.2.5, but where a constructive obligation has arisen. The cash flows expected under these contracts are considered as part of the liability adequacy test.

9.1.4

In reviewing expected future cash flows, the insurer takes into account both future cash flows under insurance contracts it has issued and the related reinsurance.

9.1.5

The related intangible assets referred to in paragraph 9.1 are those that arise under paragraph 13.3.1(b). As the liability adequacy test for the unearned premium liability is performed at the level of portfolios of contracts that are subject to broadly similar risks and are managed together as a single portfolio, the intangible asset is allocated on a reasonable basis across these portfolios.

9.1.6

As the liability adequacy test applies to deferred acquisition costs and to intangible assets, these assets are excluded from the scope of AASB 136 Impairment of Assets.

10 Outwards Reinsurance Expense

10.1

Premium ceded to reinsurers shall be recognised by the cedant as outwards reinsurance expense in the statement of comprehensive income from the attachment date over the period of indemnity of the reinsurance contract in accordance with the expected pattern of the incidence of risk.

10.1.1

It is common for general insurers or reinsurers to reinsure a portion of the risks that they accept. To secure reinsurance cover, the cedant passes on a portion of the premiums received to a reinsurer. This is known as outwards reinsurance expense.

10.1.2

The cedant accounts for direct insurance and reinsurance transactions on a gross basis, so that the extent and effectiveness of the reinsurance arrangements are apparent to the users of the financial statements, and an indication of the insurer’s risk management performance is provided to users. The gross amount of premiums earned by the cedant during the reporting period is recognised as income because it undertakes to indemnify the full amount of the specified losses of those it has insured, regardless of the reinsurance arrangements. Correspondingly, the cedant recognises the gross amount of claims expense in the reporting period because it is obliged to meet the full cost of successful claims by those it has insured.

10.1.3

Accordingly, premium ceded to reinsurers is recognised in the statement of comprehensive income as an expense of the cedant on the basis that it is an outgoing incurred in undertaking the business of direct insurance underwriting, and is not to be netted off against premium revenue.

10.1.4

Outwards reinsurance expense is recognised in the statement of comprehensive income consistently with the recognition of reinsurance recoveries under the reinsurance contract. For proportional reinsurance the estimate of outwards reinsurance expense is based upon the gross premium of the underlying direct insurance contract. For non-proportional reinsurance the cedant estimates the total claims that are likely to be made under the contract and hence whether it needs to recognise additional outwards reinsurance expense under a minimum and deposit arrangement or whether it needs to recognise reinstatement premiums expense.

10.1.5

Some reinsurance contracts purchased by a cedant might involve an experience account. Whilst these contracts may require annual renewal, in substance, the contract period is likely to be greater than one year. In estimating the outwards reinsurance expense and reinsurance recoveries to be recognised in the reporting period the cedant considers the probability-weighted expected cash flows over the expected period of indemnity and discounts the cash flows to reflect the time value of money. In determining the discount rates to be adopted, an insurer applies the same principles that are used to determine the discount rates for outstanding claims liabilities outlined in section 6. In considering all expected cash flows the reinsurer considers any profit commissions and commission rebates.

11 Reinsurance Recoveries and Non-reinsurance Recoveries

11.1

Reinsurance recoveries received or receivable in relation to the outstanding claims liability and non-reinsurance recoveries received or receivable shall be recognised as income of the cedant and shall not be netted off against the claims expense or outwards reinsurance expense in the statement of comprehensive income, or the outstanding claims liability or unearned premium liability in the statement of financial position.

11.1.1

The reinsurance recoveries receivable in the statement of financial position may not be received for some time. The reinsurance recoveries receivable are discounted on a basis consistent with the discounting of the outstanding claims liabilities outlined in section 6.

11.1.2

An insurer may also be entitled to non-reinsurance recoveries under the insurance contract such as salvage, subrogation and sharing arrangements with other insurers. Non-reinsurance recoveries are not offset against gross claims, but are recognised as income or assets, in the same way as, but separately from, reinsurance recoveries. The non-reinsurance recoveries receivable in the statement of financial position may not be received for some time. The non-reinsurance recoveries receivable are discounted on a basis consistent with the discounting of the outstanding claims liabilities outlined in section 6.

11.1.3

Amounts that reduce the liability to the policyholder, such as excesses or allowances for contributory negligence, are not non-reinsurance recoveries and are offset against the gross claims.

12 Impairment of Reinsurance Assets

12.1.1

If a cedant’s reinsurance asset is impaired, the cedant shall reduce its carrying amount accordingly and recognise that impairment in the statement of comprehensive income. A reinsurance asset is impaired if, and only if:

(a) there is objective evidence, as a result of an event that occurred after initial recognition of the reinsurance asset, that the cedant may not receive amounts due to it under the terms of the contract; and

(b) that event has a reliably measurable impact on the amounts that the cedant will receive from the reinsurer.

13 Portfolio Transfers and Business Combinations

13.1

Where the responsibility in relation to claims on transferred insurance business remains with the transferring insurer, the transfer shall be treated by the transferring insurer and the accepting insurer as reinsurance business.

13.1.1

Portfolio transfer is a term used to describe the process by which premiums and claims are transferred from one insurer to another. Transfers may be completed in a number of ways in relation to claims arising from events that occurred before the transfer. The receiving insurer may take responsibility in relation to all claims under the agreement or treaty that have not yet been paid, or it may take responsibility only in relation to those claims arising from events that occur after the date of transfer.

13.1.2

In relation to the transfer of insurance business, while the acquiring insurer agrees to meet the claims of those insured from a particular time, the contractual responsibility of the original insurer to meet those claims normally remains.

13.1.3

In relation to the withdrawal of a reinsurer from a reinsurance treaty arrangement, the contractual responsibility of the reinsurer to the direct insurer in relation to outstanding claims may be passed back to the direct insurer with a return of any premium relating to unexpired risk, or may be retained by the withdrawing reinsurer. In the former case, the direct insurer may choose to reinsure the outstanding claims with another reinsurer. This assuming reinsurer would be ceded premium for bearing liability in relation to existing outstanding claims.

13.1.4

Where the responsibility in relation to claims on transferred insurance business remains with the transferring insurer:

(a) the transferring insurer recognises the transferred premium revenue and the relevant outstanding claims in the same way as other outwards reinsurance business; and

(b) the accepting insurer recognises the premium revenue ceded to it and the relevant outstanding claims in the same way as other inwards reinsurance business.

13.2

Where the responsibility in relation to claims on transferred insurance business passes from the transferring insurer to the accepting insurer, the transfer shall be accounted for as a portfolio withdrawal by the transferring insurer and as a portfolio assumption by the accepting insurer.

13.3

A portfolio withdrawal shall be accounted for by the transferring insurer by eliminating the liabilities and assets connected with the risks transferred. A portfolio assumption shall be accounted for by the accepting insurer by recognising the relevant amount of unexpired premium revenue and the outstanding claims for which the transferring insurer is no longer responsible.

13.3.1

To comply with AASB 3, an insurer shall, at the acquisition date, measure at fair value the insurance liabilities assumed and insurance assets acquired in a business combination. However, an insurer is permitted, but not required, to use an expanded presentation that splits the fair value of acquired insurance contracts into two components:

(a) a liability measured in accordance with the insurer’s accounting policies for general insurance contracts that it issues; and

(b) an intangible asset, representing the difference between:

(i) the fair value of the contractual insurance rights acquired and insurance obligations assumed; and

(ii) the amount described in paragraph 13.3.1(a).

The subsequent measurement of this asset shall be consistent with the measurement of the related insurance liability.

13.3.2

An insurer acquiring a portfolio of general insurance contracts may use an expanded presentation described in paragraph 13.3.1.

13.3.3

The intangible assets described in paragraphs 13.3.1 and 13.3.2 are excluded from the scope of AASB 136 and from the scope of AASB 138 in respect of recognition and measurement. AASB 136 and AASB 138 apply to customer lists and customer relationships reflecting the expectation of future contracts that are not part of the contractual insurance rights and contractual insurance obligations that existed at the date of a business combination or portfolio transfer.

13.3.4

AASB 138 includes specific disclosure requirements in relation to this intangible asset.

14 Underwriting Pools and Coinsurance

14.1

Insurance business allocated through underwriting pools and coinsurance arrangements, by an entity acting as agent, shall be accounted for by the accepting insurer as direct insurance business.

14.1.1

Direct insurers or reinsurers may form underwriting pools or enter coinsurance arrangements as vehicles for jointly insuring particular risks or types of risks. Premiums, claims and other expenses are usually shared in agreed ratios by insurers involved in these arrangements.

14.1.2

Many underwriting pools and coinsurance arrangements involve the acceptance of risks by an entity acting as an agent for pool members or coinsurers. The entity receives premiums and pays claims and expenses, and allocates shares of the business to each pool member or coinsurer in agreed ratios. As the entity acting as agent is not an insurer, the business allocated to pool members and coinsurers is not reinsurance business. Pool members and coinsurers treat such business allocated to them as direct insurance business.

14.2

Business directly underwritten by a member of an underwriting pool or coinsurance arrangement shall be treated as direct insurance business and the portion of the risk reinsured by other pool members or coinsurers, determined by reference to the extent of the shares in the pool or arrangement of other pool members or coinsurers, shall be treated as outwards reinsurance. The pool member’s or coinsurer’s share of insurance business that other insurers place in the pool or arrangement shall be treated as inwards reinsurance.

15 Assets Backing General Insurance Liabilities

Fair Value Approach

15.1.1

Paragraphs 15.2 to 15.5 address the measurement of certain assets backing general insurance liabilities or financial liabilities that arise under non-insurance contracts. The fair value approach to the measurement of assets backing general insurance liabilities or financial liabilities that arise under non-insurance contracts is consistent with the present value measurement approach for general insurance liabilities, and the fair value measurement for financial liabilities that arise under non-insurance contracts, required by this Standard. Where assets are not backing general insurance liabilities or financial liabilities that arise under non-insurance contracts, general insurers apply the applicable accounting standards making use of any measurement choices available.

Measurement

15.2

Financial assets that:

(a) are within the scope of AASB 9;

(b) back general insurance liabilities; and

(c) are permitted to be designated as “at fair value through profit or loss” under AASB 9;

shall be designated as “at fair value through profit or loss” under AASB 9 on first application of this Standard, or on initial recognition.

15.2.1

An insurer applies AASB 9 to its financial assets. Under AASB 9 a financial asset is classified and measured at fair value through profit or loss when:

(a) it does not meet the criteria specified in paragraph 4.1.2 of AASB 9 to be classified at amortised cost; or

(b) it does not meet the criteria specified in paragraph 4.1.2A of AASB 9 to be classified at fair value through other comprehensive income; or

(c) it is designated as “at fair value through profit or loss” upon initial recognition in accordance with paragraph 4.1.5 of AASB 9.

AASB 1 First-time Adoption of Australian Accounting Standards permits entities to designate financial assets as “at fair value through profit or loss” on first application of the Standard.

15.2.2

The view adopted in this Standard is that financial assets, within the scope of AASB 9 that back general insurance liabilities, are permitted to be measured at fair value through profit or loss under AASB 9. This is because the measurement of general insurance liabilities under this Standard incorporates current information and measuring the financial assets backing these general insurance liabilities at fair value, eliminates or significantly reduces a potential measurement or recognition inconsistency which would arise if the assets were classified and measured at amortised cost or fair value through other comprehensive income (refer to AASB 9 paragraph B4.1.30(a)).

15.4.1-15.4.2

[Deleted by the AASB]

15.5

When preparing separate financial statements, those investments in subsidiaries, joint ventures and associates that:

(a) are defined by AASB 10 Consolidated Financial Statements, AASB 11 Joint Arrangements and AASB 128 Investments in Associates and Joint Ventures;

(b) back general insurance liabilities; and

(c) are permitted to be designated as “at fair value through profit or loss” under AASB 9;

shall be designated as “at fair value through profit or loss” under AASB 9, on first application of this Standard or on initial recognition.

15.5.1

An insurer applies AASB 127 to its investments in subsidiaries, joint ventures and associates when preparing separate financial statements. Under AASB 127, in the parent’s own financial statements, the investments in subsidiaries, joint ventures and associates can either be accounted for at cost or in accordance with AASB 9.

15.5.2

In the parent’s separate financial statements, investments in subsidiaries, joint ventures and associates that are within the scope of AASB 127, that the insurer considers back general insurance liabilities, and that are permitted to be designated as “at fair value through profit or loss” under AASB 9, are designated as “at fair value through profit or loss” under AASB 9, on first application of this Standard or on initial recognition.

16 Non-insurance Contracts Regulated under the Insurance Act 1973

16.1

Non-insurance contracts regulated under the Insurance Act 1973 shall be treated under AASB 9 to the extent that they give rise to financial assets or financial liabilities respectively. However, the financial assets and the financial liabilities that arise under these contracts shall be designated as “at fair value through profit or loss”, on first application of this Standard, or on initial recognition of the financial assets or financial liabilities, where this is permitted under AASB 9.

16.1.1

In relation to non-insurance contracts regulated under the Insurance Act, an insurer applies AASB 9 to its financial assets and financial liabilities.

16.1.2

Under AASB 9 a financial asset is classified and measured at fair value through profit or loss when:

(a) it does not meet the criteria specified in paragraph 4.1.2 of AASB 9 to be classified at amortised cost; or

(b) it does not meet the criteria specified in paragraph 4.1.2A of AASB 9 to be classified at fair value through other comprehensive income; or

(c) it is designated as “at fair value through profit or loss” upon initial recognition in accordance with paragraph 4.1.5 of AASB 9.

AASB 1 First-time Adoption of Australian Accounting Standards permits entities to designate financial assets as “at fair value through profit or loss” on first application of the Standard.

16.1.3

Under AASB 9 a financial liability at fair value through profit or loss is a financial liability that meets either of the following conditions:

(a) it meets the definition of held for trading; or

(b) it is designated as “at fair value through profit or loss” upon initial recognition in accordance with paragraph 4.2.2, because either:

(i) it eliminates or significantly reduces a measurement or recognition inconsistency (sometimes referred to as ‘an accounting mismatch’) that would otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on different bases; or

(ii) a group of financial liabilities or financial assets and financial liabilities is managed and its performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information about the group is provided internally on that basis to the entity’s key management personnel (as defined in AASB 124 Related Party Disclosures), for example the entity’s board of directors and chief executive officer.

An entity may also use this designation when it is a contract with an embedded derivative and paragraph 4.3.3 of AASB 9 allows the entity to measure the hybrid contract as “at fair value through profit or loss”.

AASB 1 First-time Adoption of Australian Accounting Standards permits entities to designate financial liabilities as “at fair value through profit or loss” on first application of the Standard.

16.2

Paragraphs 15.2, 15.3, 15.4 and 15.5 shall also be applied to the measurement of assets that back financial liabilities that arise under non-insurance contracts.

17 Disclosures

Statement of Comprehensive Income

17.1

In relation to the statement of comprehensive income, the financial statements shall disclose:

(a) the underwriting result for the reporting period, determined as the amount obtained by deducting the sum of claims expense, outwards reinsurance premium expense and underwriting expenses from the sum of direct and inwards reinsurance premium revenues and recoveries revenue;

(b) net claims incurred shall be disclosed, showing separately:

(i) the amount relating to risks borne in the current reporting period; and

(ii) the amount relating to a reassessment of risks borne in all previous reporting periods.

An explanation shall be provided where net claims incurred relating to a reassessment of risks borne in previous reporting periods are material; and

(c) in respect of 17.1(b)(i) and 17.1(b)(ii), the following components shall be separately disclosed:

(i) gross claims incurred – undiscounted;

(ii) reinsurance and other recoveries – undiscounted; and

(iii) discount movements shown separately for (i) and (ii).

17.1.1

This Standard requires the underwriting result for the reporting period to be disclosed. This disclosure gives an indication of an insurer’s underwriting performance, including the extent to which underwriting activities rely on investment income for the payment of claims.

17.1.2

Based on the total movement in net claims incurred, it may appear that there has not been a material reassessment of risks borne in previous periods, however, there may be material movements at a business segment level, that mitigate each other. For example, the insurer may have seen a material deterioration in its motor portfolio, which has been mitigated by material savings in the professional indemnity portfolio, such that when both portfolios are aggregated there appears to have been little change in the reporting period. In such circumstances, the insurer provides an explanation of the reassessments that took place in the net claims incurred for previous periods during the reporting period at the business segment level.

Statement of Financial Position

17.2

The financial statements shall disclose in relation to the outstanding claims liability:

(a) the central estimate of the expected present value of future payments for claims incurred;

(b) the component related to the risk margin;

(c) the percentage risk margin adopted in determining the outstanding claims liability (determined from (a) and (b) above);

(d) the probability of adequacy intended to be achieved through adoption of the risk margin; and

(e) the process used to determine the risk margin, including the way in which diversification of risks has been allowed for.

17.3

An insurer shall disclose the process used to determine which assets back general insurance liabilities and which assets back financial liabilities arising under non-insurance contracts.

Non-insurance Contracts

17.4

Where a general insurer has issued a non-insurance contract or holds a non-insurance contract as a cedant, and that non-insurance contract has a material financial impact on the statement of comprehensive income, statement of financial position or cash flows, the general insurer shall disclose:

(a) the nature of the non-insurance contract;

(b) the recognised assets, liabilities, income, expense and cash flows arising from the non-insurance contract; and

(c) information that helps users to understand the amount, timing and uncertainty of future cash flows from the non-insurance contract.

17.4.1

In applying paragraph 17.4 a non-insurance contract shall be considered together with any related contracts or side letters, when determining the need for disclosure, and in making the disclosures required.

17.5

[Deleted by the AASB]

17.5.1

[Deleted by the AASB]

Insurance Contracts – Explanation of Recognised Amounts

17.6

An insurer shall disclose information that identifies and explains the amounts in its financial statements arising from insurance contracts.

17.6.1

To comply with paragraph 17.6, an insurer shall disclose:

(a) its accounting policies for insurance contracts and related assets, liabilities, income and expense;

(b) the recognised assets, liabilities, income, expense and cash flows arising from insurance contracts. Furthermore, if the insurer is a cedant, it shall disclose:

(i) gains and losses recognised in the statement of comprehensive income on buying reinsurance; and

(ii) if the cedant defers and amortises gains and losses arising on buying reinsurance, the amortisation for the period and the amounts remaining unamortised at the beginning and end of the period;

(c) the process used to determine the assumptions that have the greatest effect on the measurement of the recognised amounts described in (b). When practicable, an insurer shall also give quantified disclosure of those assumptions;

(d) the effect of changes in assumptions used to measure insurance assets and insurance liabilities, showing separately the effect of each change that has a material effect on the financial statements; and

(e) reconciliations of changes in insurance liabilities, reinsurance assets and, if any, related deferred acquisition costs.

17.6.2

In applying paragraph 17.6.1(b), the recognised assets and liabilities arising from insurance contracts would normally include:

(a) gross outstanding claims liability;

(b) reinsurance recoveries receivable arising from the outstanding claims liability;

(c) gross unearned premium liability;

(d) reinsurance recoveries receivable arising from the unearned premium liability;

(e) unexpired risk liability;

(f) other reinsurance recoveries receivable;

(g) other recoveries receivable;

(h) outwards reinsurance expense asset or liability;

(i) direct premium revenue receivable;

(j) inwards reinsurance premium revenue receivable;

(k) deferred acquisition cost asset; and

(l) intangible assets relating to acquired insurance contracts.

17.6.3

In applying paragraph 17.6.1(b), the recognised income and expenses arising from insurance contracts would normally include:

(a) direct premium revenue;

(b) inwards reinsurance premium revenue (including retrocessions);

(c) reinsurance and other recoveries revenue;

(d) direct claims expense;

(e) reinsurance claims expense;

(f) outwards reinsurance premium expense (including retrocessions);

(g) acquisition costs expense; and

(h) other underwriting expenses, including claims handling expenses.

17.6.4

When an insurer is presenting the disclosures required by paragraphs 17.6.1(c) and 17.6.1(d) the insurer determines the level and extent of disclosure that is appropriate having regard to its circumstances and the qualitative characteristics of financial statements under the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

AusCF17.6.4

Notwithstanding paragraph 17.6.4, in respect of AusCF entities, when an insurer is presenting the disclosures required by paragraphs 17.6.1(c) and 17.6.1(d) the insurer determines the level and extent of disclosure that is appropriate having regard to its circumstances and the qualitative characteristics of financial statements under the Framework for the Preparation and Presentation of Financial Statements (as identified in AASB 1048 Interpretation of Standards).

17.6.5

For an insurer that is involved in a large number of insurance classes, across different jurisdictions, disclosure by class of business is likely to be voluminous and may not be understandable to the user of the financial statements. Furthermore, for such an insurer, disclosure for the entity as a whole is also likely to be at too high a level of aggregation to be relevant or comparable. It is expected that for most insurers disclosure at the major business segment level would normally be most appropriate. The insurer may believe that disclosure of a range of values would be relevant to the users of the financial statements.

17.6.6

Some of the assumptions that would normally have the greatest effect on the measurement of the recognised amounts described in paragraph 17.6.1(b), are discount rates, inflation rates, average weighted term to settlement from the claims reporting date, average claim frequency, average claim size and expense rates. The insurer determines whether these assumptions shall be disclosed given the requirements of paragraphs 17.6 and 17.6.1.

Nature and Extent of Risks Arising from Insurance Contracts

17.7

An insurer shall disclose information that enables users of its financial statements to evaluate the nature and extent of risks arising from insurance contracts.

17.7.1

To comply with paragraph 17.7, an insurer shall disclose:

(a) its objectives, policies and processes for managing risks arising from insurance contracts and the methods used to manage those risks;

(b) information about insurance risk (both before and after risk mitigation by reinsurance), including information about:

(i) sensitivity to insurance risk (see paragraph 17.7.5);

(ii) concentrations of insurance risk, including a description of how management determines concentrations and a description of the shared characteristic that identifies each concentration (e.g. type of insured event, geographical area, or currency); and

(iii) actual claims compared with previous estimates (i.e. claims development). The disclosure about claims development shall go back to the period when the earliest material claim arose for which there is still uncertainty about the amount and timing of the claims payments, but need not go back more than ten years. An insurer need not disclose this information for claims for which uncertainty about the amount and timing of claims payments is typically resolved within one year;

(c) information about credit risk, liquidity risk and market risk that paragraphs 31-42 of AASB 7 Financial Instruments: Disclosures would require if the insurance contracts were within the scope of AASB 7. However:

(i) an insurer need not provide the maturity analyses required by paragraphs 39(a) and (b) of AASB 7 if it discloses information about the estimated timing of the net cash outflows resulting from recognised insurance liabilities instead. This may take the form of an analysis, by estimated timing, of the amounts recognised in the statement of financial position; and

(ii) if an insurer uses an alternative method to manage sensitivity to market conditions, such as an embedded value analysis, it may use that sensitivity analysis to meet the requirement in paragraph 40(a) of AASB 7. Such an insurer shall also provide the disclosures required by paragraph 41 of AASB 7; and

(d) information about exposures to market risk arising from embedded derivatives contained in a host insurance contract if the insurer is not required to, and does not, measure the embedded derivatives at fair value.

17.7.2

For an insurer that is involved in a large number of insurance classes, across different jurisdictions, disclosure by class of business is likely to be voluminous and may not be understandable to the user of the financial statements. Furthermore, for such an insurer disclosure for the entity as a whole would normally be at too high a level of aggregation to be relevant or comparable. It is expected that for most insurers disclosure at the major business segment level would normally be most appropriate.

17.7.3

The claims development disclosure required by paragraph 17.7.1(b)(iii) only applies to classes of business where claims are not typically resolved within one year. The insurer, in disclosing claims development, ensures it is clear to the reader of the financial statements, which classes of business, or which segments of the business, are covered by the disclosures and which classes of business, or which segments of the business, are not covered by the disclosures.

17.7.4

IG Example 5 in the Guidance on Implementing IFRS 4 Insurance Contracts, provides one possible format to meet the claims development disclosure requirements of this Standard. Such a format may be particularly appropriate for longer tail classes of business where the long tail nature of the claims is a significant aspect in the development of the claims, as this format illustrates the development of claims over a number of years. If this format is adopted, disclosure by accident year, gross and net of reinsurance, of undiscounted claims would normally be most relevant to the users of financial statements. The insurer explains the information presented. This includes whether the claims are discounted or undiscounted, gross or net of reinsurance and by accident year or underwriting year.

17.7.5

To comply with paragraph 17.7.1(b)(i), an insurer shall disclose either (a) or (b) as follows:

(a) a sensitivity analysis that shows how profit or loss and equity would have been affected had changes in the relevant risk variable that were reasonably possible at the end of the reporting period occurred; the methods and assumptions used in preparing the sensitivity analysis; and any changes from the previous period in the methods and assumptions used. However, if an insurer uses an alternative method to manage sensitivity to market conditions, such as an embedded value analysis, it may meet this requirement by disclosing that alternative sensitivity analysis and the disclosures required by paragraph 41 of AASB 7; and

(b) qualitative information about sensitivity, and information about those terms and conditions of insurance contracts that have a material effect on the amount, timing and uncertainty of the insurer’s future cash flows.

Liability Adequacy Test

17.8

In relation to the liability adequacy test in section 9, the financial statements shall disclose:

(a) where a deficiency has been identified, the amounts underlying the calculation performed, that is:

(i) unearned premium liability;

(ii) related reinsurance asset;

(iii) deferred acquisition costs;

(iv) intangible assets;

(v) present value of expected future cash flows for future claims, showing expected reinsurance recoveries separately; and

(vi) deficiency;

(b) any write-down of deferred acquisition costs under the liability adequacy test;

(c) any write-down of intangible assets under the liability adequacy test;

(d) in relation to the present value of expected future cash flows for future claims:

(i) the central estimate of the present value of expected future cash flows;

(ii) the component of present value of expected future cash flows related to the risk margin;

(iii) the percentage risk margin adopted in determining the present value of expected future cash flows (determined from (i) and (ii) above);

(iv) the probability of adequacy intended to be achieved through adoption of the risk margin; and

(v) the process used to determine the risk margin, including the way in which diversification of risks has been allowed for;

(e) where the probability of adequacy disclosed in paragraph 17.2(d) is not the same or similar to the probability of adequacy disclosed in paragraph 17.8(d)(iv), the reasons for the difference; and

(f) where a surplus has been identified, the fact that the liability adequacy test identified a surplus.

Other Disclosures

17.9.1

This Standard addresses disclosure requirements in relation to general insurance contracts. Other Australian Accounting Standards may be relevant to a general insurer’s financial statements. In particular, the disclosure requirements in AASB 7 would normally be relevant to general insurers.

18 Transitional Provisions

18.1

An entity need not apply the disclosure requirements in this Standard to comparative information that relates to annual periods beginning before 1 January 2005, except for the disclosures required by paragraphs 17.6.1(a) and 17.6.1(b) about accounting policies, and recognised assets, liabilities, income and expense and cash flows.

18.2

Where an entity applies the disclosure requirements in this Standard to comparative information that relates to annual periods beginning before 1 January 2005, if it is impracticable to apply a particular requirement of this Standard to comparative information that relates to annual periods beginning before 1 January 2005, an entity shall disclose that fact. AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors explains the term “impracticable”.

18.3

In applying paragraph 17.7.1(b)(iii), an entity need not disclose information about claims development that occurred earlier than five years before the end of the first annual reporting period in which it applies this Standard. Furthermore, if it is impracticable, when an entity first applies this Standard, to prepare information about claims development that occurred before the beginning of the earliest period for which an entity presents full comparative information that complies with this Standard, the entity shall disclose that fact.

18.4

[Deleted by the AASB]

18.5

[Deleted by the AASB]

19 Definitions

19.1

In this Standard:

19.1[1]

attachment date means, for a direct insurer, the date as from which the insurer accepts risk from the insured under an insurance contract or endorsement or, for a reinsurer, the date from which the reinsurer accepts risk from the direct insurer or another reinsurer under a reinsurance arrangement

19.1[2]

cedant means the policyholder under a reinsurance contract

19.1[3]

claim means a demand by any party external to the entity for payment by the insurer on account of an alleged loss resulting from an insured event or events, that have occurred, alleged to be covered by an insurance contract

19.1[4]

claims expense means the charge to the statement of comprehensive income for the reporting period and represents the sum of claims settled and claims management expenses relating to claims incurred in the period and the movement in the gross outstanding claims liability in the period

19.1[5]

claims incurred means claims that have occurred prior to the end of the reporting period, whether reported or unreported at the end of the reporting period

19.1[7]

deposit premium means the premium charged by the insurer at the inception of a contract under which the final premium depends on conditions prevailing over the contract period and so is not determined until the expiry of that period

19.1[8]

direct insurance contract means an insurance contract that is not a reinsurance contract

19.1[9]

fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. (See AASB 13.)

19.1[10]

financial risk means the risk of a possible future change in one or more of a specified interest rate, financial instrument price, commodity price, foreign exchange rate, index of prices or rates, a credit rating or credit index or other variable, provided in the case of a non-financial variable that the variable is not specific to a party to the contract

19.1[11]

future claims means claims in respect of insured events that are expected to occur in future reporting periods under policies where the attachment date is prior to the end of the reporting period

19.1[12]

general insurance contract means an insurance contract that is not a life insurance contract

19.1[13]

general insurer means an insurer that writes general insurance contracts

19.1[14]

general reinsurance contract means a reinsurance contract that is not a life reinsurance contract

19.1[15]

insurance asset means an insurer’s net contractual rights under an insurance contract

19.1[16]

insurance contract means a contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder

(Refer to Appendix for additional guidance in applying this definition.)

19.1[17]

insurance liability means an insurer’s net contractual obligations under an insurance contract

19.1[18]

insurance risk means risk, other than financial risk, transferred from the holder of a contract to the issuer

19.1[19]

insured event means an uncertain future event covered by an insurance contract and creates insurance risk

19.1[20]

insurer means the party that has an obligation under an insurance contract to compensate a policyholder if an insured event occurs

19.1[21]

inwards reinsurance means reinsurance contracts written by reinsurers

19.1[22]

liability adequacy test means an assessment of whether the carrying amount of an insurance liability needs to be increased (or the carrying amount of the related deferred acquisition costs or related intangible assets decreased) based on a review of future cash flows

19.1[23]

life insurance contract means an insurance contract, or a financial instrument with a discretionary participation feature, regulated under the Life Insurance Act 1995, and similar contracts issued by entities operating outside Australia

19.1[24]

life reinsurance contract means a life insurance contract issued by one insurer (the reinsurer) to compensate another insurer (the cedant) for losses on one or more contracts issued by the cedant

19.1[25]

net claims incurred means direct claims costs net of reinsurance and other recoveries, and indirect claims handling costs, determined on a discounted basis

19.1[26]

non-insurance contract means a contract regulated under the Insurance Act 1973, and similar contracts issued by entities operating outside Australia, which fails to meet the definition of an insurance contract under this Standard

(An example of a non-insurance contract might be a type of complex financial reinsurance contract.)

19.1[27]

outstanding claims liability means all unpaid claims and related claims handling expenses relating to claims incurred prior to the end of the reporting period

19.1[28]

policyholder means a party that has a right to compensation under an insurance contract if an insured event occurs

19.1[29]

premium means the amount charged in relation to accepting risk from the insured, but does not include amounts collected on behalf of third parties

19.1[30]

reinsurance assets means a cedant’s net contractual rights under a reinsurance contract

19.1[31]

reinsurance contract means an insurance contract issued by one insurer (the reinsurer) to compensate another insurer (the cedant) for losses on one or more contracts issued by the cedant

19.1[32]

reinsurer means the party that has an obligation under a reinsurance contract to compensate a cedant if an insured event occurs

19.1[33]

separate financial statements are those presented by a parent, an investor in an associate or a venturer in a jointly controlled entity, in which the investments are accounted for on the basis of the direct equity interest rather than on the basis of the reported results and net assets of the investees

19.1[34]

unbundle means to treat the components of a contract as if they were separate contracts

19.1[35]

weather derivative means a contract that requires payment based on climatic, geological or other physical variables

Appendix A -- Definition of an Insurance Contract

This Appendix is an integral part of AASB 1023.

1

This Appendix gives guidance on the definition of an insurance contract in section 19 of the Standard. It addresses the following issues:

(a) the term ‘uncertain future event’ (paragraphs 2-4);

(b) payments in kind (paragraphs 5-6);

(c) insurance risk and other risks (paragraphs 7-16);

(d) examples of insurance contracts (paragraphs 17-20);

(e) significant insurance risk (paragraphs 21-26); and

(f) changes in the level of insurance risk (paragraphs 27 and 28).

Uncertain Future Event

2

Uncertainty (or risk) is the essence of an insurance contract. Accordingly, at least one of the following is uncertain at the inception of an insurance contract:

(a) whether an insured event will occur;

(b) when it will occur; or

(c) how much the insurer will need to pay if it occurs.

3

In some insurance contracts, the insured event is the discovery of a loss during the term of the contract, even if the loss arises from an event that occurred before the inception of the contract. In other insurance contracts, the insured event is an event that occurs during the term of the contract, even if the resulting loss is discovered after the end of the contract term.

4

Some insurance contracts cover events that have already occurred, but whose financial effect is still uncertain. An example is a reinsurance contract that covers the direct insurer against adverse development of claims already reported by policyholders. In such contracts, the insured event is the discovery of the ultimate cost of those claims.

Payments in Kind

5