Illustrative examples

These illustrative examples accompany, but are not part of, AASB 1058. They illustrate aspects of AASB 1058, but are not intended to provide interpretative guidance.

IE1

The following examples portray hypothetical situations. They are intended to illustrate how a not-for-profit entity might apply some of the requirements of AASB 1058 Income of Not-for-Profit Entities to particular types of transactions, on the basis of the limited facts presented. Although some aspects of the examples might be present in actual fact patterns, all relevant facts and circumstances of a particular fact pattern need to be evaluated when applying AASB 1058.

Recognition and measurement of income and related amounts (paragraphs 9–22)

IE2

Examples 1–8 illustrate the requirements in AASB 1058 for identifying related amounts and income to be recognised in accordance with paragraphs 9 and 10 on the initial recognition of an asset. The following requirements are illustrated in the examples in identifying related amounts in the form of:

(a) contributions by owners, in accordance with AASB 1004;

(b) a financial instrument, in accordance with AASB 9;

(c) a lease liability arising in a lease contract, in accordance with AASB 16; and

(d) revenue or a contract liability arising from a contract with a customer, in accordance with AASB 15.

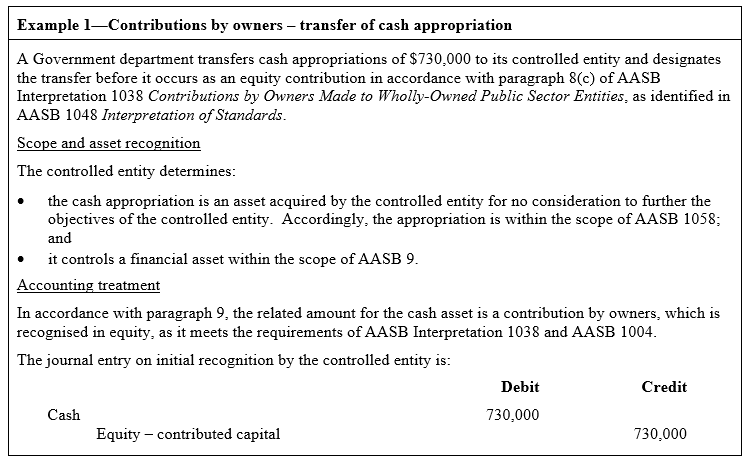

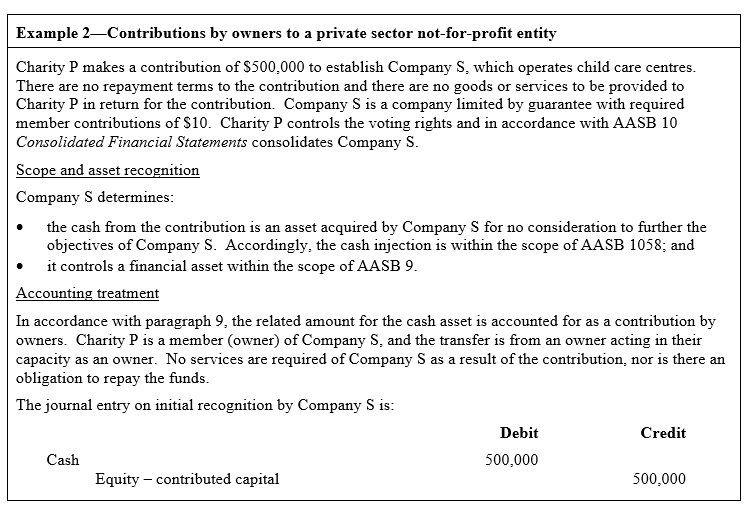

Contributions by owners

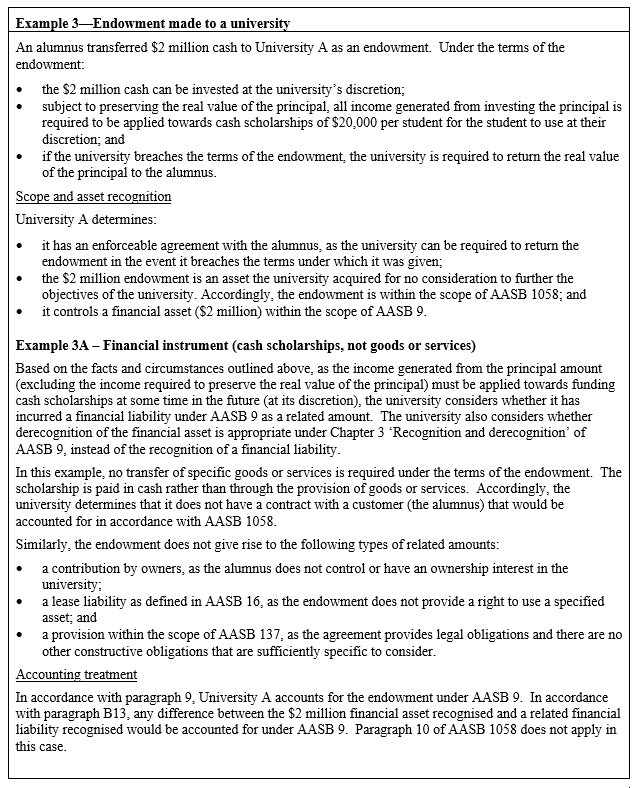

Financial instruments, bequests and endowments

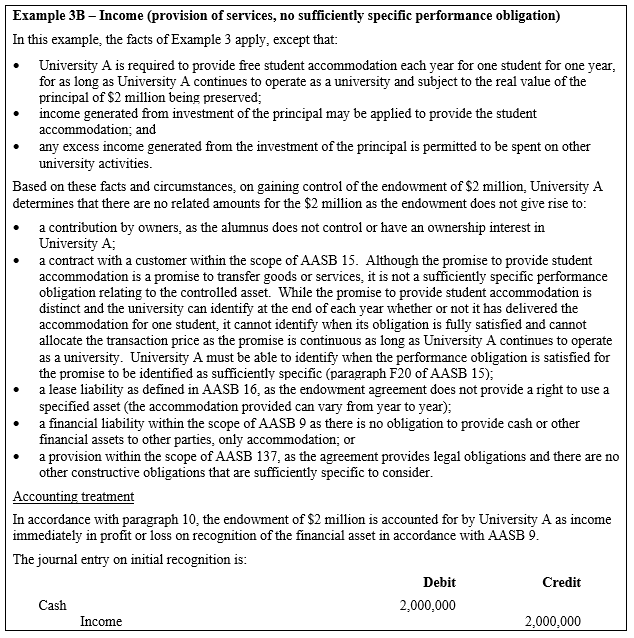

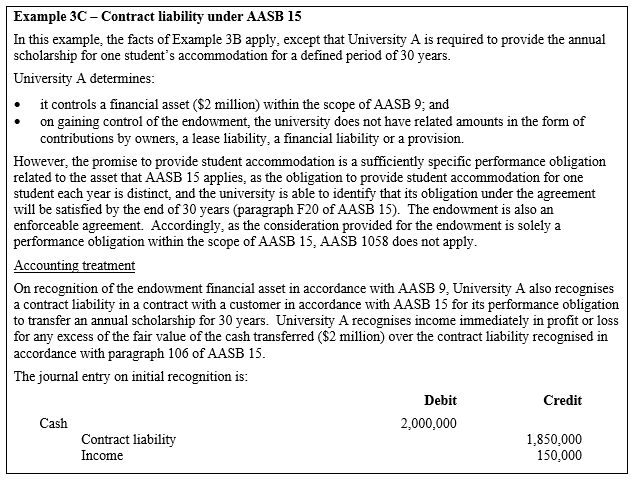

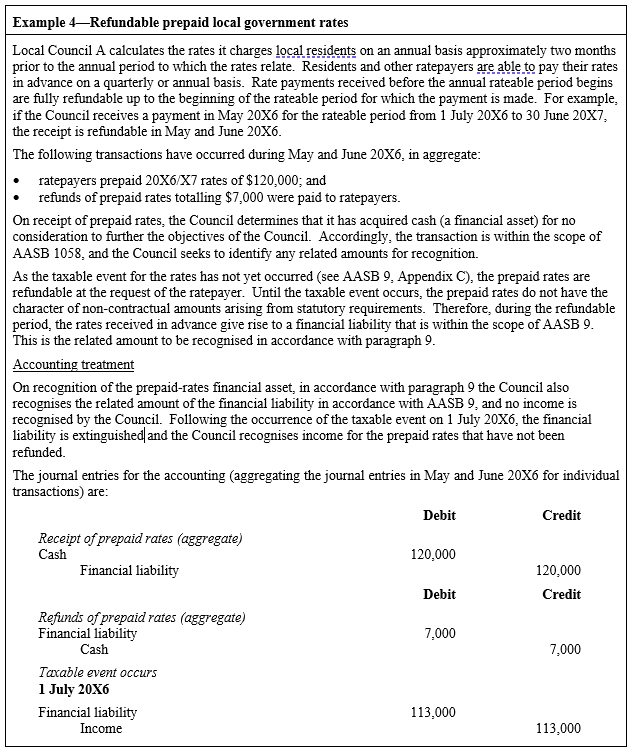

IE3

Examples 3 and 4 illustrate the requirements of paragraphs 9 and 10 in AASB 1058 for the accounting treatment for financial instruments, bequests and endowments. Examples 3A and 4 illustrate the identification of related amounts in the form of a financial instrument, in accordance with AASB 9. Receiving a bequest or endowment in the form of cash, or paying out the principal and/or interest in the form of cash, requires the application of the financial instrument accounting requirements in AASB 9.

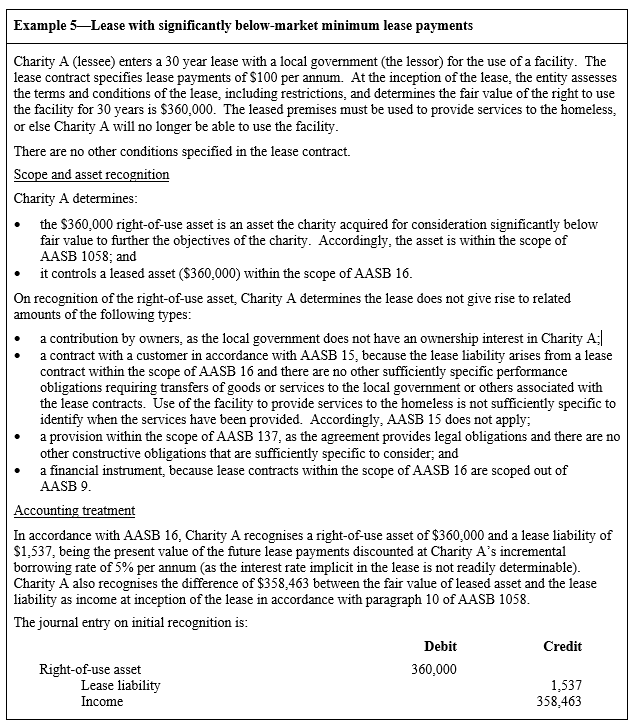

Leases

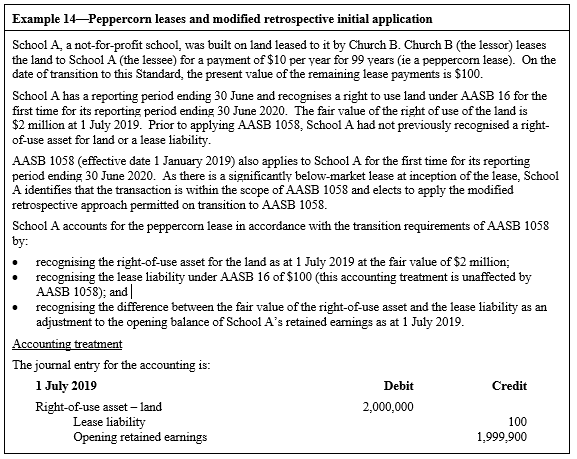

IE4

Example 5 illustrates the requirements in AASB 1058 regarding the recognition of a lease liability in accordance with AASB 16.

Contract with a customer – revenue and income

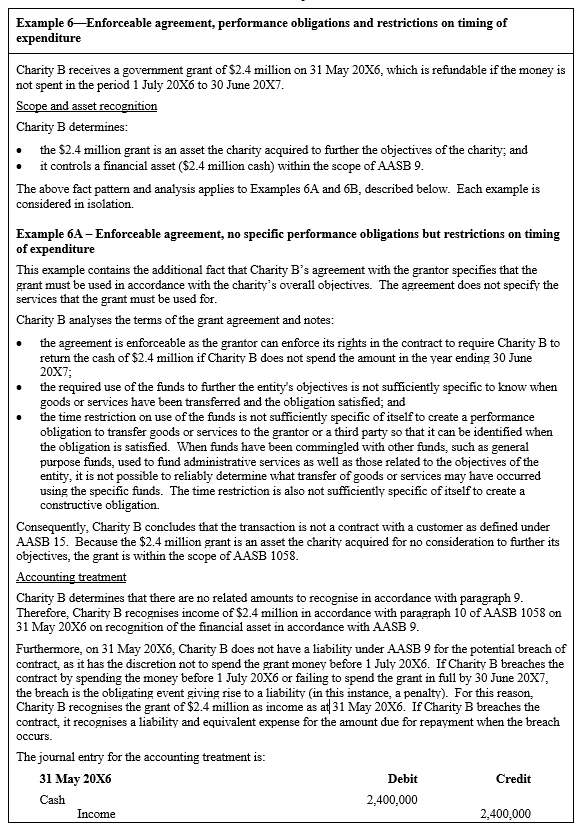

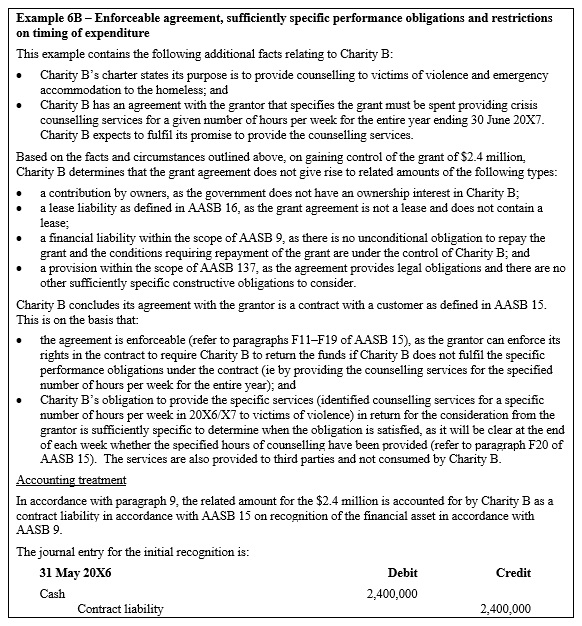

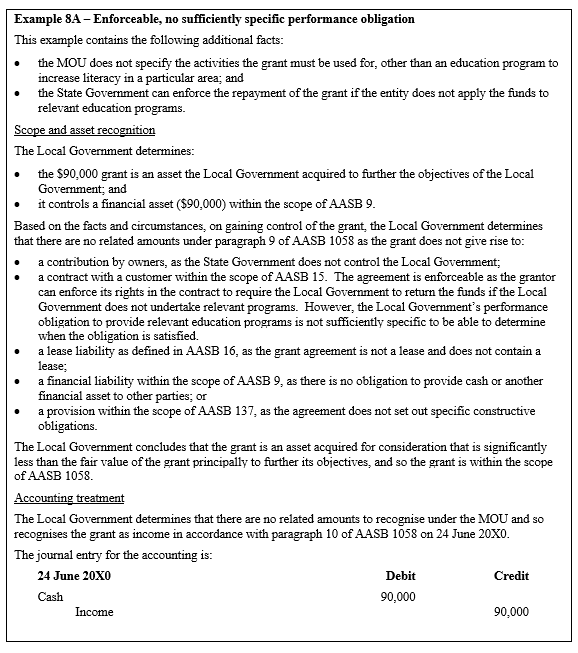

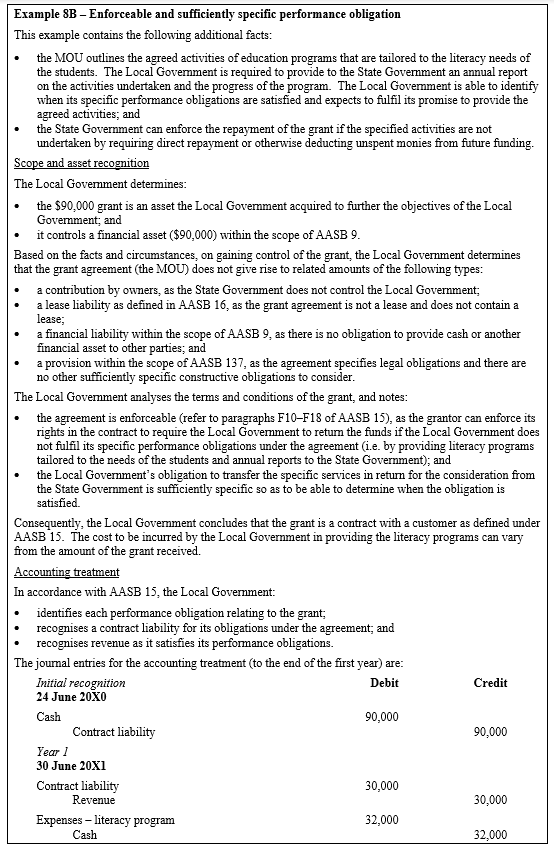

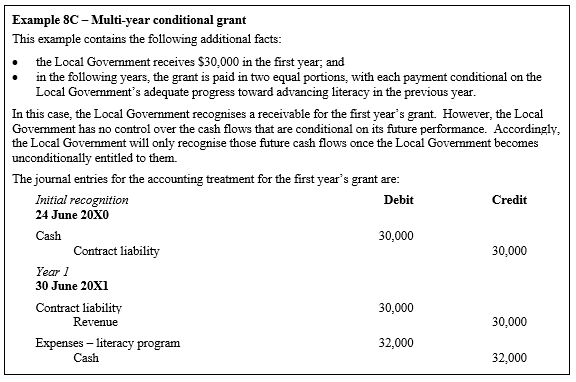

IE5

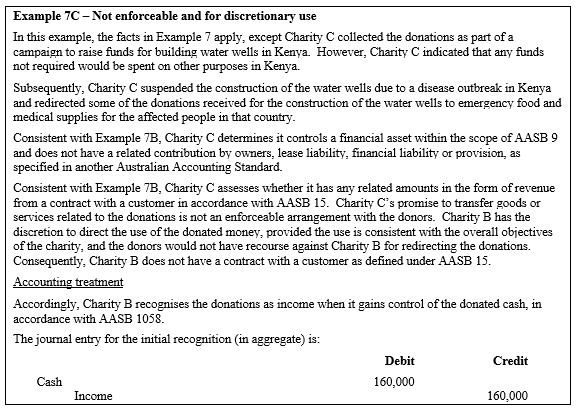

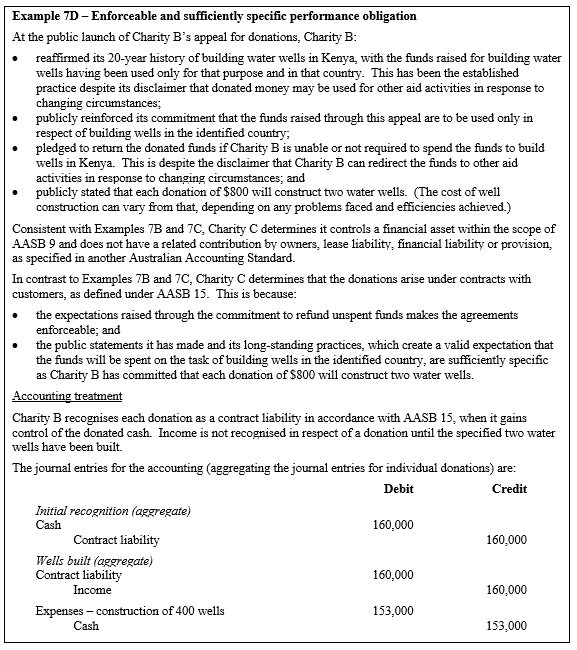

Examples 6–8 illustrate the requirements in AASB 1058 regarding recognition of revenue and a contract liability in accordance with AASB 15. To be in the scope of AASB 15, the contract must:

(a) be enforceable;

(b) contain performance obligations to transfers goods or services to another party that are sufficiently specific to enable determination of when the obligation has been satisfied; and

(c) not result in the goods or services specified being retained by the entity, ie the goods or services will be transferred to the customer or to other parties on behalf of the customer.

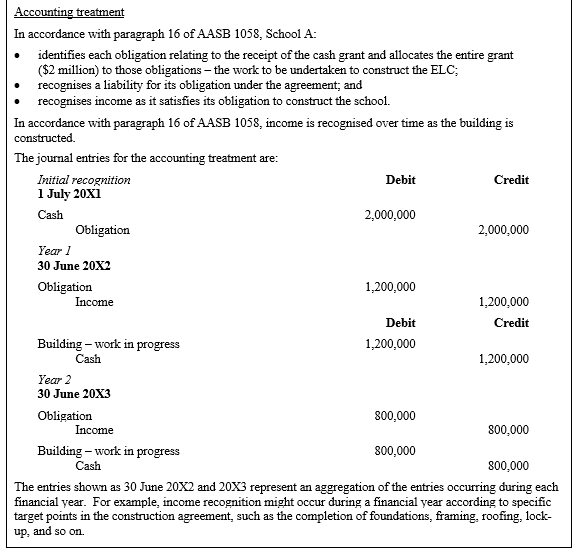

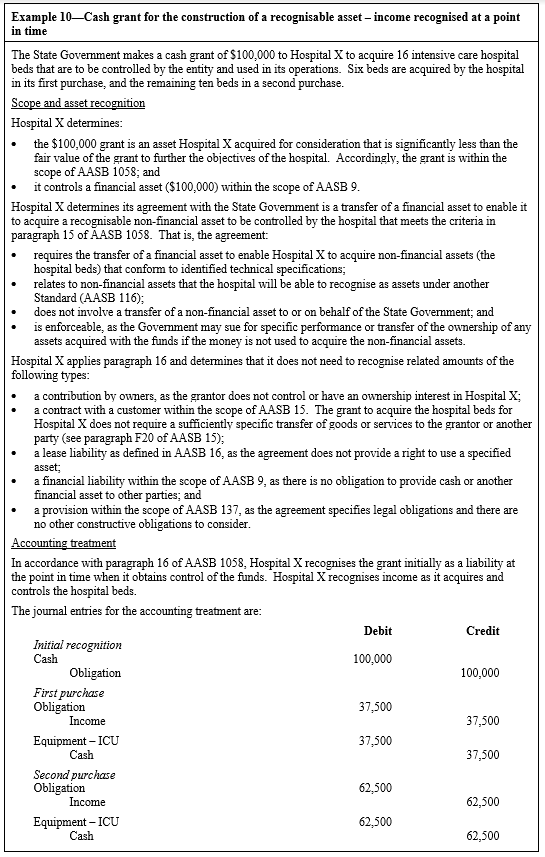

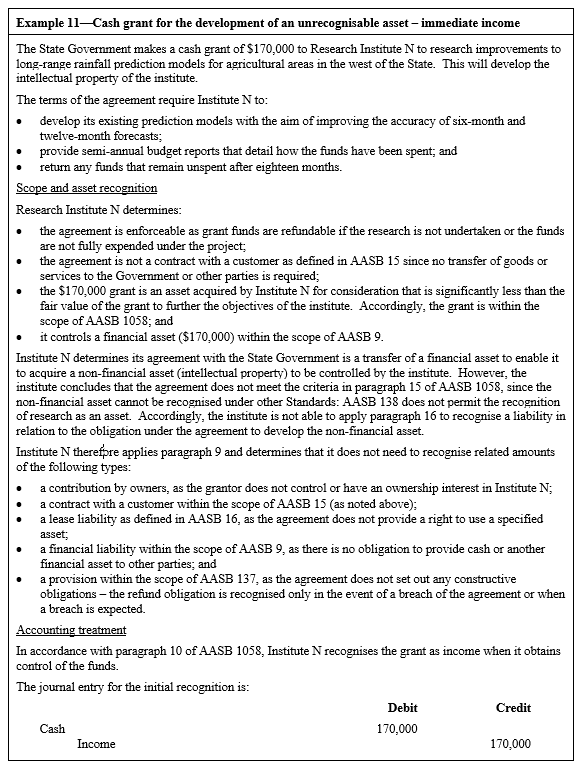

Transfers to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity (paragraphs 15–17)

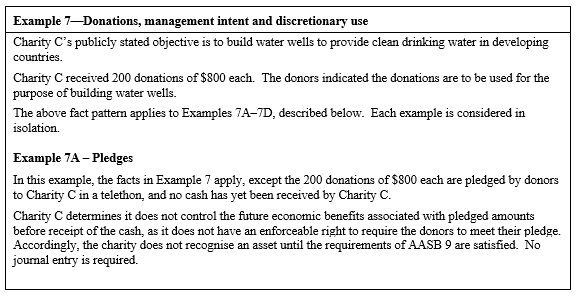

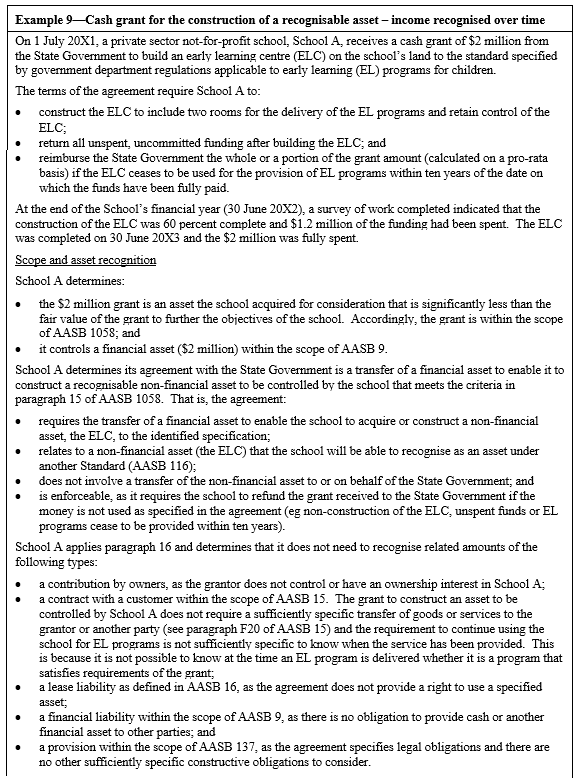

IE6

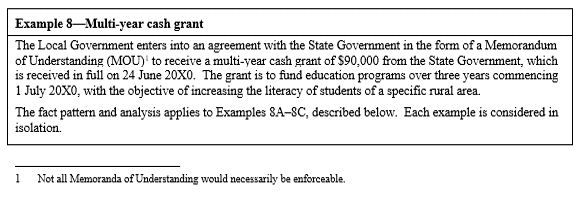

Examples 9 and 10 illustrate the requirements in AASB 1058 regarding a transfer of a financial asset to enable an entity to acquire or construct a recognisable non-financial asset to be controlled by the entity, and when revenue is recognised. Example 11 illustrates a transfer to enable an entity to develop a non-financial asset that cannot be recognised under Australian Accounting Standards, and hence does not meet the criteria for the accounting for transfers of financial assets set out in paragraphs 15–17.

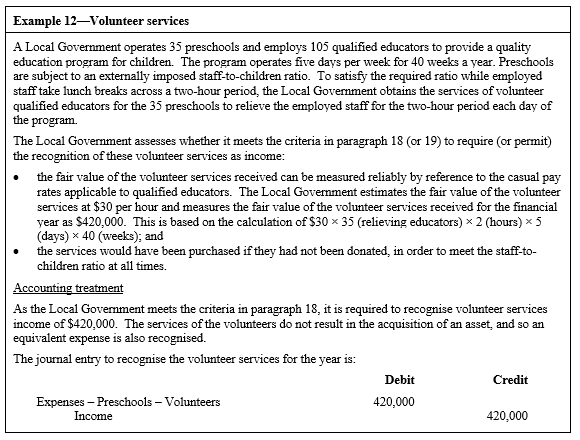

Volunteer services (paragraphs 18–22)

IE7

Example 12 illustrates the requirements in AASB 1058 for recognising the receipt of volunteer services as income and as an asset or an expense.

Disclosure

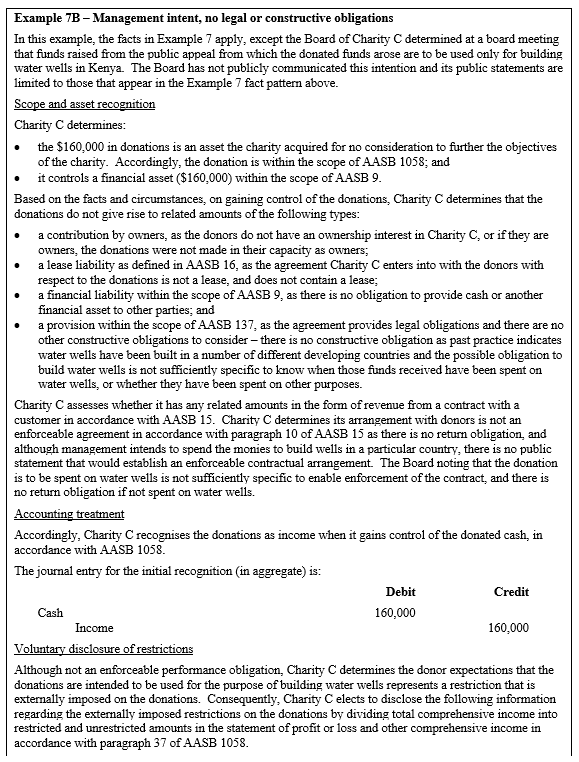

Restrictions (paragraph 37)

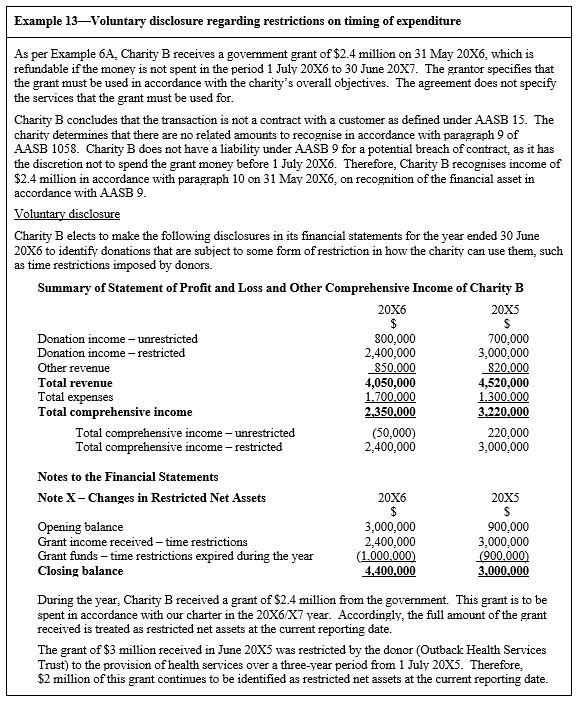

IE8

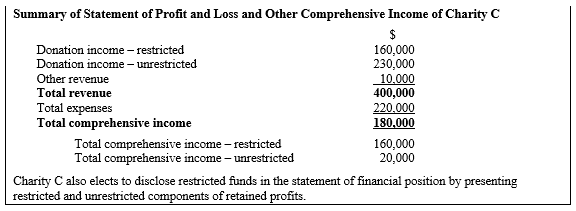

Example 13 illustrates disclosures about externally imposed restrictions that limit or direct the purpose for which resources controlled by an entity may be used. Such disclosures are encouraged by this Standard but not required. This example extends Example 6A to illustrate possible disclosures about time restrictions on the expenditure of grant monies received. This example illustrates voluntary disclosures about restricted and unrestricted donation income in the Statement of Profit and Loss and Other Comprehensive Income, as well as disclosures relating to restricted net assets. Example 7B also illustrates voluntary disclosures of restrictions.

Transition (paragraphs C2–C7)

IE9

Example 14 illustrates the modified retrospective initial application of this Standard to peppercorn leases.