The objective of this Standard is to specify the types of entities and financial statements to which Australian Accounting Standards (including Interpretations) apply.

Preamble

Pronouncement

This compiled Standard applies to annual periods beginning on or after 1 January 2022 but before 1 January 2023 that end on or after 30 June 2022. Earlier application is permitted for annual periods beginning before 1 January 2023 that end before 30 June 2022. It incorporates relevant amendments made up to and including 23 June 2022.

Prepared on 15 September 2022 by the staff of the Australian Accounting Standards Board.

Compilation no. 6

Compilation date: 29 June 2022

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2022

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights should be addressed to The Managing Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1057 Application of Australian Accounting Standards (as amended) is set out in paragraphs 1 – 26 and the Appendix. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in the Appendix are in italics the first time they appear in the Standard. AASB 1057 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Accounting Standard AASB 1057

The Australian Accounting Standards Board made Accounting Standard AASB 1057 Application of Australian Accounting Standards under section 334 of the Corporations Act 2001 on 24 July 2015.

This compiled version of AASB 1057 applies to annual periods beginning on or after 1 January 2022 but before 1 January 2023 that end on or after 30 June 2022. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 23 June 2022 (see Compilation Details).

Objective

1

The objective of this Standard is to specify the types of entities and financial statements to which Australian Accounting Standards (including Interpretations) apply. The term ‘Australian Accounting Standards’ refers to accounting standards (including Interpretations) made by the AASB. Each reference to an Interpretation refers to that Interpretation as identified in AASB 1048 Interpretation of Standards.

AusCF1

AusCF entities are:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

For AusCF entities, the term ‘reporting entity’ is defined in this Standard and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting are set out in paragraph Aus1.1 of the Conceptual Framework.

Application of this Standard

2

This Standard applies to:

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) financial statements of General Government Sectors (GGSs) prepared in accordance with AASB 1049 Whole of Government and General Government Sector Financial Reporting;

(e) for-profit private sector entities that are required by legislation[*] to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(f) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards.

3

This Standard applies to annual periods beginning on or after 1 January 2016.

4

This Standard may be applied to annual periods beginning before 1 January 2016.

References in this Standard to ‘legislation’ mean legislation of a government in Australia.

Application of Australian Accounting Standards

5

Unless specified otherwise in paragraphs 6–21, Australian Accounting Standards apply to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

6

AASB 8 Operating Segments and AASB 120 Accounting for Government Grants and Disclosure of Government Assistance apply as set out in paragraph 5, provided the entity is a for-profit entity.

7

Except as specified in paragraph 20C, AASB 101 Presentation of Financial Statements, AASB 107 Statement of Cash Flows, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors and AASB 1048 Interpretation of Standards apply to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

8

[Deleted by the AASB]

9

AASB 133 Earnings per Share applies to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity or discloses earnings per share; and

(b) for-profit private sector entities that are required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act or disclose earnings per share.

10

AASB 134 Interim Financial Reporting applies to:

(a) each disclosing entity required to prepare half-year financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) interim financial reports that are general purpose financial statements of each not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare interim financial reports that are, or are held out to be, general purpose financial statements;

(d) interim financial reports of for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) interim financial reports of other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

11

AASB 1004 Contributions applies to general purpose financial statements of local governments, government departments, other government controlled not-for-profit entities and whole of governments.

12

AASB 1038 Life Insurance Contracts applies to:

(a) a life insurer; or

(b) the parent in a group that includes a life insurer;

when the entity:

(c) is a reporting entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(d) is an other reporting entity and prepares general purpose financial statements; or

(e) prepares financial statements that are, or are held out to be, general purpose financial statements.

13

AASB 1039 Concise Financial Reports applies to a concise financial report prepared by an entity in accordance with paragraph 314(2)(a) in Part 2M.3 of the Corporations Act.

14

AASB 1049 applies to each government’s whole of government general purpose financial statements and GGS financial statements.

15

AASB 1050 Administered Items applies to general purpose financial statements of government departments.

16

AASB 1051 Land Under Roads applies to general purpose financial statements of local governments, government departments and whole of governments, and financial statements of GGSs.

17

AASB 1052 Disaggregated Disclosures applies to general purpose financial statements of local governments and government departments.

18

AASB 1053 Application of Tiers of Australian Accounting Standards applies to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) financial statements of GGSs prepared in accordance with AASB 1049;

(e) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(f) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

18A

AASB 1054 Australian Additional Disclosures applies to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act;

(b) general purpose financial statements of each not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards.

19

AASB 1055 Budgetary Reporting applies to:

(a) whole of government general purpose financial statements of each government;

(b) financial statements of each government’s GGS;

(c) general purpose financial statements of each not-for-profit reporting entity within the GGS; and

(d) financial statements of each not-for-profit entity within the GGS that are, or are held out to be, general purpose financial statements.

20

AASB 1056 Superannuation Entities applies to:

(a) general purpose financial statements of each not-for-profit superannuation entity that is a reporting entity;

(b) each superannuation entity that elects to prepare financial statements that are held out to be general purpose financial statements;

(c) for-profit private sector superannuation entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(d) other for-profit private sector superannuation entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

20A

AASB 1058 Income of Not-for-Profit Entities applies to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit entity that is a reporting entity; and

(c) financial statements of a not-for-profit entity that are, or are held out to be, general purpose financial statements.

20B

AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities applies as set out in paragraph 5, provided the entity is eligible to apply Tier 2 reporting requirements, as set out in AASB 1053, paragraph 13.

20C

Entities applying AASB 1060 are not required to apply the following Australian Accounting Standards:

(a) AASB 7 Financial Instruments: Disclosures;

(b) AASB 12 Disclosure of Interests in Other Entities;

(c) AASB 101 Presentation of Financial Statements;

(d) AASB 107 Statement of Cash Flows; and

(e) AASB 124 Related Party Disclosures.

21

[Deleted]

Application of Australian Interpretations

22

Unless specified otherwise in paragraphs 23–26, Interpretations apply to:

(a) each not-for-profit entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit entity that is a reporting entity;

(c) each entity that elects to prepare financial statements that are, or are held out to be, general purpose financial statements;

(d) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards, and

(e) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

23

Interpretation 110 Government Assistance – No Specific Relation to Operating Activities applies as set out in paragraph 22, provided the entity is a for-profit entity.

24

Interpretation 1019 The Superannuation Contributions Surcharge applies to:

(a) each not-for-profit superannuation plan that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other not-for-profit superannuation plan that is a reporting entity;

(c) each superannuation plan that elects to prepare financial statements of a superannuation plan that are, or are held out to be, general purpose financial statements;

(d) for-profit superannuation plans that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards; and

(e) other for-profit superannuation plans that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021.

25

Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities applies to public sector entities as follows:

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other reporting entity; and

(c) financial statements that are, or are held out to be, general purpose financial statements.

26

Interpretation 1047 Professional Indemnity Claims Liabilities in Medical Defence Organisations applies to entities that are or include medical defence organisations as follows:

(a) each entity that is required to prepare financial reports in accordance with Part 2M.3 of the Corporations Act and that is a reporting entity;

(b) general purpose financial statements of each other reporting entity; and

(c) financial statements that are, or are held out to be, general purpose financial statements.

Appendix -- Defined terms

This appendix is an integral part of AASB 1057.

general purpose financial statements

A[1]

Financial statements that are intended to meet the needs of users who are not in a position to require an entity to prepare reports tailored to their particular information needs.

reporting entity

A[2]

An entity in respect of which it is reasonable to expect the existence of users who rely on the entity’s general purpose financial statements for information that will be useful to them for making and evaluating decisions about the allocation of resources. A reporting entity can be a single entity or a group comprising a parent and all of its subsidiaries.

This reporting entity definition is not relevant to:

(a) for-profit private sector entities that are required by legislation to prepare financial statements that comply with either Australian Accounting Standards or accounting standards;

(b) other for-profit private sector entities that are required only by their constituting document or another document to prepare financial statements that comply with Australian Accounting Standards, provided that the relevant document was created or amended on or after 1 July 2021; and

(c) other for-profit entities (private sector or public sector) that elect to prepare general purpose financial statements.

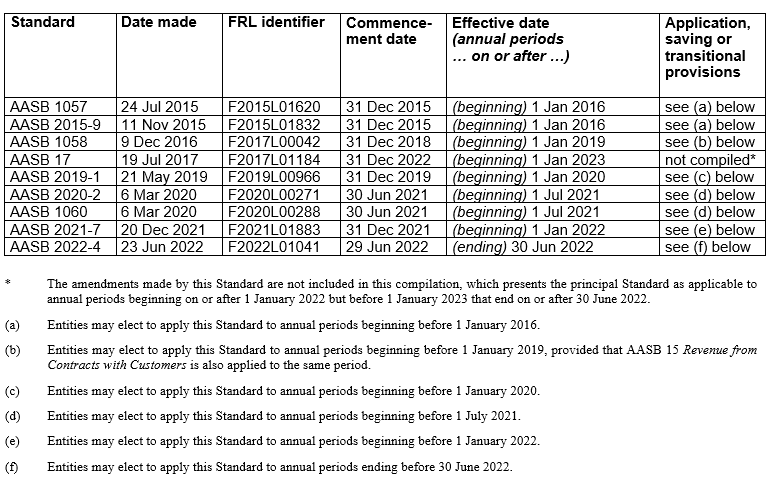

Compilation details

Accounting Standard AASB 1057 Application of Australian Accounting Standards (as amended)

Compilation details are not part of AASB 1057.

This compiled Standard applies to annual periods beginning on or after 1 January 2022 but before 1 January 2023 that end on or after 30 June 2022. It takes into account amendments up to and including 23 June 2022 and was prepared on 15 September 2022 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1057 (July 2015) as amended by other Accounting Standards, which are listed in the table below.

Basis for Conclusions on AASB 2019-1

This Basis for Conclusions accompanies, but is not part of, AASB 1057. The Basis for Conclusions was originally published with AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework.

The Basis for Conclusions is provided with this Standard as a linked PDF document. See AASB Extras at right.

Basis for Conclusions on AASB 2020-2

This Basis for Conclusions accompanies, but is not part of, AASB 1057. The Basis for Conclusions was originally published with AASB 2020-2 Amendments to Australian Accounting Standards – Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities.

The Basis for Conclusions is provided with this Standard as a linked PDF document. See AASB Extras at right.