The objective of this Standard is to specify the requirements for financial reporting of land under roads by local governments, government departments, General Government Sectors (GGSs) and whole of governments. This Standard applies only to land under roads acquired before the end of the first reporting period that ends on or after 31 December 2007. Other Standards, such as AASB 116, apply to land under roads acquired after that.

Preamble

Pronouncement

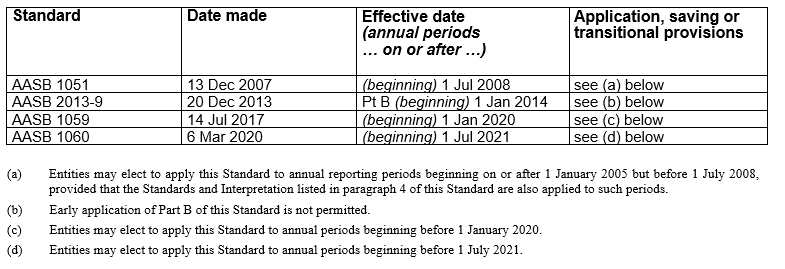

This compiled Standard applies to annual periods beginning on or after 1 July 2021. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

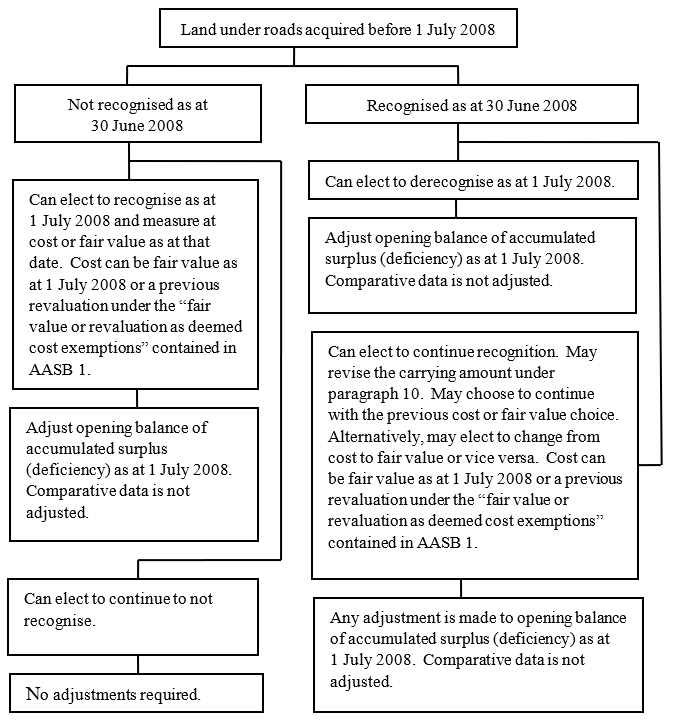

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1051 Land Under Roads (as amended) is set out in paragraphs 1 – 15 and Appendices A and D. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the Standard. AASB 1051 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with international pronouncements

AASB 1051 and International Public Sector Accounting Standards

International Public Sector Accounting Standards (IPSAS) are issued by the International Public Sector Accounting Standards Board (IPSASB).

Land under roads falls within the scope of IPSAS 17 Property, Plant, and Equipment (issued December 2006, as amended), but is not mentioned specifically.

IPSAS 33 First-Time Adoption of Accrual Basis IPSASs does not require the recognition of property, plant and equipment (which would include land under roads) for reporting periods beginning on a date within three years following the date of first adoption of accrual accounting in accordance with IPSAS. This means that, at the expiry of the transitional period, all holdings of land under roads would be required to be recognised under IPSAS 17 where they satisfy the recognition criteria.

AASB 1051 does not require the recognition of land under roads acquired before the end of the first reporting period ending on or after 31 December 2007. However, an entity may elect to recognise such land in accordance with this Standard.

Land under roads acquired after the end of the first reporting period ending on or after 31 December 2007 is accounted for under AASB 116 Property, Plant and Equipment.

AASB 1051 and International Financial Reporting Standards

Land under roads falls within the scope of IAS 16 Property, Plant and Equipment, which does not contain requirements or choices equivalent to this Standard for land under roads acquired before the end of the first reporting period ending on or after 31 December 2007.

Land under roads acquired after the end of the first reporting period ending on or after 31 December 2007 is accounted for under AASB 116. A comparison with the corresponding IAS 16 is presented with AASB 116.

This Standard allows an entity to elect, in certain circumstances, to apply the fair value or a previous revaluation under the “fair value or revaluation as deemed cost exemptions” in AASB 1 First-time Adoption of Australian Accounting Standards when recognising land under roads acquired before the end of the first reporting period ending on or after 31 December 2007. A comparison with the corresponding IFRS 1 First-time Adoption of International Financial Reporting Standards is presented with AASB 1.

Accounting Standard AASB 1051

The Australian Accounting Standards Board made Accounting Standard AASB 1051 Land Under Roads on 13 December 2007.

This compiled version of AASB 1051 applies to annual periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

1

The objective of this Standard is to specify the requirements for financial reporting of land under roads by local governments, government departments, General Government Sectors (GGSs) and whole of governments.

Application

2

This Standard applies to general purpose financial statements of local governments, government departments and whole of governments, and financial statements of GGSs.

3

This Standard applies to annual reporting periods beginning on or after 1 July 2008. [Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

4

This Standard may be applied to annual reporting periods beginning on or after 1 January 2005 but before 1 July 2008, provided there is early adoption for the same annual reporting period of the following pronouncements being issued at about the same time, as applicable:

(a) AASB 1004 Contributions;

(b) AASB 1049 Whole of Government and General Government Sector Financial Reporting;

(c) AASB 1050 Administered Items;

(d) AASB 1052 Disaggregated Disclosures;

(e) AASB 2007-9 Amendments to Australian Accounting Standards arising from the Review of AASs 27, 29 and 31; and

(f) AASB Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities.

5

[Deleted by the AASB]

6

When applicable, this Standard, together with the Standards referred to in paragraph 4, supersede:

(a) AAS 27 Financial Reporting by Local Governments as issued in June 1996, as amended;

(b) AAS 29 Financial Reporting by Government Departments as issued in June 1998, as amended; and

(c) AAS 31 Financial Reporting by Governments as issued in June 1998, as amended.

Land under roads

7

Other Australian Accounting Standards (including AASB 116 Property, Plant and Equipment) apply to land under roads, except to the extent that this Standard requires or permits otherwise. This Standard does not apply to land under roads that are service concession assets in accordance with AASB 1059 Service Concession Arrangements: Grantors.

8

An entity may elect to recognise (including continue to recognise or to recognise for the first time), subject to satisfaction of the asset recognition criteria, or not to recognise (including continue not to recognise or to derecognise) as an asset, land under roads acquired before the end of the first reporting period ending on or after 31 December 2007.

9

An entity shall make a final election under paragraph 8 effective as at the first day of the next reporting period following the end of the first reporting period ending on or after 31 December 2007. Any adjustments that arise from a final election that is made effective as at that first day shall be made against the opening balance of accumulated surplus (deficiency) of that next reporting period.

10

Adjustments arising under paragraph 9 include those relating to a revision of recognised amounts of previously recognised land under roads acquired before the end of the first reporting period ending on or after 31 December 2007, made to reflect a reassessment of the factors used to determine those recognised amounts. Any adjustments that arise from an election that is made effective:

(a) before the first day of the next reporting period following the end of the first reporting period ending on or after 31 December 2007, is made against accumulated surplus (deficiency) of the earliest prior period presented, and therefore comparative data is adjusted; and

(b) on the first day of the next reporting period following the end of the first reporting period ending on or after 31 December 2007, is made against the opening balance of accumulated surplus (deficiency) of that next reporting period, and therefore comparative data is not adjusted.

11

An entity shall disclose its accounting policy for land under roads acquired before the end of the first reporting period ending on or after 31 December 2007, in each reporting period to which this Standard is applied.

12

The nature and net amount of each adjustment made in accordance with paragraph 9 shall be disclosed.

13

Where an entity recognises land under roads in accordance with paragraphs 8 and 9, but after the entity’s first-time adoption of Australian equivalents to International Financial Reporting Standards (IFRSs), the entity may, in relation to land under roads, elect to adopt the fair value (as at the date of that election) or a previous revaluation under the “fair value or revaluation as deemed cost” exemptions contained in AASB 1 First-time Adoption of Australian Equivalents to International Financial Reporting Standards, as if it were adopting Australian equivalents to IFRSs for the first time.

14

Paragraph 13 enables an entity that recognises land under roads acquired before the end of the first reporting period ending on or after 31 December 2007, after its first-time adoption of Australian equivalents to IFRSs and under paragraphs 8 and 9, to elect to:

(a) measure the fair value of land under roads as at the date of the election made under paragraph 13 and use that fair value as the deemed cost;

(b) use an earlier revaluation of land under roads as its deemed cost; or

(c) use an earlier deemed cost of land under roads established from an event-driven fair value measurement as its deemed cost.

15

Land under roads acquired after the end of the first reporting period ending on or after 31 December 2007 is accounted for in accordance with AASB 116.

Appendix B -- Comparison of AASB 1051 with AASs 27, 29 and 31

This Appendix accompanies, but is not part of, AASB 1051.

The requirements of this Standard differ from the requirements contained in AASs 27 Financial Reporting by Local Governments, AAS 29 Financial Reporting by Government Departments and AAS 31 Financial Reporting by Governments (as amended), and expresses the requirements generically. The main differences between AASB 1051 and AASs 27, 29 and 31 (as amended) are:

(a) this Standard extends indefinitely the relief from the requirement to recognise land under roads acquired before the end of the first reporting period ending on or after 31 December 2007. AASs 27, 29 and 31 provided recognition relief only for a transitional period;

(b) AASs 27, 29 and 31 encouraged entities to recognise land under roads as an asset wherever it can be measured reliably. Consistent with the AASB’s policy of not including encouragements within Standards, this encouragement has not been included in this Standard;

(c) this Standard notes that AASB 116 Property, Plant and Equipment applies to land under roads acquired after the end of the first reporting period ending on or after 31 December 2007. AASs 27, 29 and 31 would have required that AASB 116 be retrospectively applied to land under roads after the end of the transitional period;

(d) in certain circumstances this Standard allows an entity, in relation to land under roads acquired before the end of the first reporting period ending on or after 31 December 2007, to elect to adopt the fair value (as at the date of that election) or a previous revaluation under the “fair value or revaluation as deemed cost” exemptions contained in AASB 1 First-time Adoption of Australian Equivalents to International Financial Reporting Standards, as if it were adopting Australian equivalents to IFRSs for the first time. AASs 27, 29 and 31 did not contain this relief;

(e) AASs 29 and 31 did not explicitly require that, if the recognised amounts of land under roads acquired before the end of the first reporting period ending on or after 31 December 2007 are revised, up until the first day of the next reporting period, to reflect a reassessment of the factors used to determine those recognised amounts, the net amount of the resultant adjustments be made against accumulated surplus (deficiency) in the reporting periods in which the recognised amounts are revised; and

(f) this Standard extends the requirements to General Government Sectors.

Appendix C -- Implementation guidance

This Appendix accompanies, but is not part of, AASB 1051.

The following diagram illustrates the effect of the requirements in this Standard for land under roads acquired before 1 July 2008, assuming an entity with a 1 July 2008 to 30 June 2009 reporting period makes a final election under paragraphs 8 and 9 as at 1 July 2008. (Note that land under roads acquired after 30 June 2008 is accounted for in accordance with AASB 116.)

Appendix D -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusD1

Paragraphs 11 and 12 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Compilation details

Accounting Standard AASB 1051 Land Under Roads (as amended)

Compilation details are not part of AASB 1051.

This compiled Standard applies to annual periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1051 (December 2007) as amended by other Accounting Standards, which are listed in the table below.

Table of pronouncements

Table of amendments