The objective of this Standard is to ensure that an entity’s first Australian-Accounting-Standards financial statements, and its interim financial reports for part of the period covered by those financial statements, contain high-quality information that is transparent for users and comparable over all periods presented, provide a suitable starting point for accounting in accordance with Australian Accounting Standards and can be generated at a cost that does not exceed the benefits.

Preamble

Pronouncement

This compiled Standard applies to annual periods beginning on or after 1 July 2021 but before 1 January 2022. Earlier application is permitted for annual periods beginning after 24 July 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 7 December 2020.

Prepared on 17 August 2021 by the staff of the Australian Accounting Standards Board.

Compilation no. 3

Compilation date: 30 June 2021

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

Australian Accounting Standard AASB 1 First-time Adoption of Australian Accounting Standards (as amended) is set out in paragraphs 1 – Aus40.2 and Appendices A – F. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the Standard. AASB 1 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IFRS 1

AASB 1 First-time Adoption of Australian Accounting Standards as amended incorporates IFRS 1 First-time Adoption of International Financial Reporting Standards as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IFRS 1) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB 1 also comply with IFRS 1.

Not-for-profit entities’ compliance with IFRS 1 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IFRS 1.

Tier 2

Entities preparing general purpose financial statements under Australian Accounting Standards – Simplified Disclosures (Tier 2) will not be in compliance with IFRS Standards.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Accounting Standard AASB 1

The Australian Accounting Standards Board made Accounting Standard AASB 1 First-time Adoption of Australian Accounting Standards under section 334 of the Corporations Act 2001 on 24 July 2015.

This compiled version of AASB 1 applies to annual periods beginning on or after 1 July 2021 but before 1 January 2022. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 7 December 2020 (see Compilation Details).

Objective

1

The objective of this Standard is to ensure that an entity’s first Australian-Accounting-Standards financial statements, and its interim financial reports for part of the period covered by those financial statements, contain high quality information that:

(a) is transparent for users and comparable over all periods presented;

(b) provides a suitable starting point for accounting in accordance with Australian Accounting Standards[1]; and

(c) can be generated at a cost that does not exceed the benefits.

Scope

2

An entity shall apply this Standard in:

(a) its first Australian-Accounting-Standards financial statements; and

(b) each interim financial report, if any, that it presents in accordance with AASB 134 Interim Financial Reporting for part of the period covered by its first Australian-Accounting-Standards financial statements.

[Aus] The term ‘Australian Accounting Standards’ refers to Standards (including Interpretations) made by the AASB that apply to any reporting period beginning on or after 1 January 2005. In this context, the term encompasses Australian Accounting Standards – Simplified Disclosures, which some entities are permitted to apply in accordance with AASB 1053 Application of Tiers of Australian Accounting Standards in preparing general purpose financial statements.

3

An entity’s first Australian-Accounting-Standards financial statements are the first annual financial statements in which the entity adopts Australian Accounting Standards, by an explicit and unreserved statement in those financial statements of compliance with Australian Accounting Standards. Financial statements in accordance with Australian Accounting Standards are an entity’s first Australian-Accounting-Standards financial statements if, for example, the entity:

(a) presented its most recent previous financial statements:

(i) in accordance with national requirements that are not consistent with Australian Accounting Standards or International Financial Reporting Standards (IFRSs) in all respects;

(ii) in conformity with Australian Accounting Standards or IFRSs in all respects, except that the financial statements did not contain an explicit and unreserved statement that they complied with Australian Accounting Standards or IFRSs;

(iii) containing an explicit statement of compliance with some, but not all, Australian Accounting Standards or IFRSs;

(iv) in accordance with national requirements inconsistent with Australian Accounting Standards or IFRSs, using some individual Australian Accounting Standards or IFRSs to account for items for which national requirements did not exist; or

(v) in accordance with national requirements, with a reconciliation of some amounts to the amounts determined in accordance with Australian Accounting Standards or IFRSs;

(b) prepared financial statements in accordance with Australian Accounting Standards or IFRSs for internal use only, without making them available to the entity’s owners or any other external users;

(c) prepared a reporting package in accordance with Australian Accounting Standards or IFRSs for consolidation purposes without preparing a complete set of financial statements as defined in AASB 101 Presentation of Financial Statements (as revised in 2007); or

(d) did not present financial statements for previous periods.

Aus3.1

[Deleted by the AASB]

Aus3.2

In rare circumstances, a not-for-profit public sector entity may experience extreme difficulties in complying with the requirements of certain Australian Accounting Standards due to information deficiencies that have caused the entity to state non-compliance with previous GAAP. In these cases, the conditions specified in paragraph 3 for the application of this Standard are taken to be satisfied provided the entity:

(a) discloses in its first Australian-Accounting-Standards financial statements:

(i) an explanation of information deficiencies and its strategy for rectifying those deficiencies; and

(ii) the Australian Accounting Standards that have not been complied with; and

(b) makes an explicit and unreserved statement of compliance with other Australian Accounting Standards for which there are no information deficiencies.

4

This Standard applies when an entity first adopts Australian Accounting Standards. It does not apply when, for example, an entity:

(a) stops presenting financial statements in accordance with national requirements, having previously presented them as well as another set of financial statements that contained an explicit and unreserved statement of compliance with Australian Accounting Standards or IFRSs;

(b) presented financial statements in the previous year in accordance with national requirements and those financial statements contained an explicit and unreserved statement of compliance with Australian Accounting Standards or IFRSs; or

(c) presented financial statements in the previous year that contained an explicit and unreserved statement of compliance with Australian Accounting Standards or IFRSs, even if the auditors qualified their audit report on those financial statements.

4A

Notwithstanding the requirements in paragraphs 2 and 3, an entity that has applied Australian Accounting Standards or IFRSs in a previous reporting period, but whose most recent previous annual financial statements did not contain an explicit and unreserved statement of compliance with Australian Accounting Standards or IFRSs, must either apply this Standard or else apply Australian Accounting Standards retrospectively in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors as if the entity had never stopped applying Australian Accounting Standards or IFRSs.

4B

When an entity does not elect to apply this Standard in accordance with paragraph 4A, the entity shall nevertheless apply the disclosure requirements in paragraphs 23A–23B of AASB 1, in addition to the disclosure requirements in AASB 108.

5

This Standard does not apply to changes in accounting policies made by an entity that already applies Australian Accounting Standards. Such changes are the subject of:

(a) requirements on changes in accounting policies in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors; and

(b) specific transitional requirements in other Australian Accounting Standards.

Recognition and measurement

Opening Australian-Accounting-Standards statement of financial position

6

An entity shall prepare and present an opening Australian-Accounting-Standards statement of financial position at the date of transition to Australian Accounting Standards. This is the starting point for its accounting in accordance with Australian Accounting Standards.

Accounting policies

7

An entity shall use the same accounting policies in its opening Australian-Accounting-Standards statement of financial position and throughout all periods presented in its first Australian-Accounting-Standards financial statements. Those accounting policies shall comply with each Australian Accounting Standard effective at the end of its first Australian-Accounting-Standards reporting period, except as specified in paragraphs 13–19 and Appendices B–E.

8

An entity shall not apply different versions of Australian Accounting Standards that were effective at earlier dates. An entity may apply a new Standard that is not yet mandatory if that Standard permits early application.

|

Example: Consistent application of latest version of Australian Accounting Standards |

|

Background The end of entity A’s first Australian-Accounting-Standards reporting period is 31 December 20X5. Entity A decides to present comparative information in those financial statements for one year only (see paragraph 21). Therefore, its date of transition to Australian Accounting Standards is the beginning of business on 1 January 20X4 (or, equivalently, close of business on 31 December 20X3). Entity A presented financial statements in accordance with its previous GAAP annually to 31 December each year up to, and including, 31 December 20X4. |

|

Application of requirements Entity A is required to apply the Australian Accounting Standards effective for periods ending on 31 December 20X5 in: (a) preparing and presenting its opening Australian-Accounting-Standards statement of financial position at 1 January 20X4; and (b) preparing and presenting its statement of financial position for 31 December 20X5 (including comparative amounts for 20X4), statement of comprehensive income, statement of changes in equity and statement of cash flows for the year to 31 December 20X5 (including comparative amounts for 20X4) and disclosures (including comparative information for 20X4). If a new Standard is not yet mandatory but permits early application, entity A is permitted, but not required, to apply that Standard in its first Australian-Accounting-Standards financial statements. |

9

The transitional provisions in other Australian Accounting Standards apply to changes in accounting policies made by an entity that already uses Australian Accounting Standards; they do not apply to a first-time adopter’s transition to Australian Accounting Standards, except as specified in Appendices B–E.

10

Except as described in paragraphs 13–19 and Appendices B–E, an entity shall, in its opening Australian-Accounting-Standards statement of financial position:

(a) recognise all assets and liabilities whose recognition is required by Australian Accounting Standards;

(b) not recognise items as assets or liabilities if Australian Accounting Standards do not permit such recognition;

(c) reclassify items that it recognised in accordance with previous GAAP as one type of asset, liability or component of equity, but are a different type of asset, liability or component of equity in accordance with Australian Accounting Standards; and

(d) apply Australian Accounting Standards in measuring all recognised assets and liabilities.

11

The accounting policies that an entity uses in its opening Australian-Accounting-Standards statement of financial position may differ from those that it used for the same date using its previous GAAP. The resulting adjustments arise from events and transactions before the date of transition to Australian Accounting Standards. Therefore, an entity shall recognise those adjustments directly in retained earnings (or, if appropriate, another category of equity) at the date of transition to Australian Accounting Standards.

12

This Standard establishes two categories of exceptions to the principle that an entity’s opening Australian-Accounting-Standards statement of financial position shall comply with each Australian Accounting Standard:

(a) paragraphs 14–17 and Appendix B prohibit retrospective application of some aspects of other Australian Accounting Standards.

(b) Appendices C–E grant exemptions from some requirements of other Australian Accounting Standards.

Aus12.1

Entities that elect to apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities to periods beginning before 1 July 2021 (ie early application) may also elect to apply the short-term exemptions from restating comparative information set out in AASB 1053 Application of Tiers of Australian Accounting Standards Appendix E, where applicable. For entities that apply that relief, references to the ‘date of transition to Australian Accounting Standards’ in this Standard shall mean the beginning of the first Australian-Accounting-Standards reporting period.

Exceptions to the retrospective application of other Australian Accounting Standards

13

This Standard prohibits retrospective application of some aspects of other Australian Accounting Standards. These exceptions are set out in paragraphs 14–17 and Appendix B.

Estimates

14

An entity’s estimates in accordance with Australian Accounting Standards at the date of transition to Australian Accounting Standards shall be consistent with estimates made for the same date in accordance with previous GAAP (after adjustments to reflect any difference in accounting policies), unless there is objective evidence that those estimates were in error.

15

An entity may receive information after the date of transition to Australian Accounting Standards about estimates that it had made under previous GAAP. In accordance with paragraph 14, an entity shall treat the receipt of that information in the same way as non-adjusting events after the reporting period in accordance with AASB 110 Events after the Reporting Period. For example, assume that an entity’s date of transition to Australian Accounting Standards is 1 January 20X4 and new information on 15 July 20X4 requires the revision of an estimate made in accordance with previous GAAP at 31 December 20X3. The entity shall not reflect that new information in its opening Australian-Accounting-Standards statement of financial position (unless the estimates need adjustment for any differences in accounting policies or there is objective evidence that the estimates were in error). Instead, the entity shall reflect that new information in profit or loss (or, if appropriate, other comprehensive income) for the year ended 31 December 20X4.

16

An entity may need to make estimates in accordance with Australian Accounting Standards at the date of transition to Australian Accounting Standards that were not required at that date under previous GAAP. To achieve consistency with AASB 110, those estimates in accordance with Australian Accounting Standards shall reflect conditions that existed at the date of transition to Australian Accounting Standards. In particular, estimates at the date of transition to Australian Accounting Standards of market prices, interest rates or foreign exchange rates shall reflect market conditions at that date.

17

Paragraphs 14–16 apply to the opening Australian-Accounting-Standards statement of financial position. They also apply to a comparative period presented in an entity’s first Australian-Accounting-Standards financial statements, in which case the references to the date of transition to Australian Accounting Standards are replaced by references to the end of that comparative period.

Exemptions from other Australian Accounting Standards

18

An entity may elect to use one or more of the exemptions contained in Appendices C–E. An entity shall not apply these exemptions by analogy to other items.

19

[Deleted]

Presentation and disclosure

20

This Standard does not provide exemptions from the presentation and disclosure requirements in other Australian Accounting Standards.

Comparative information

21

An entity’s first Australian-Accounting-Standards financial statements shall include at least three statements of financial position, two statements of profit or loss and other comprehensive income, two separate statements of profit or loss (if presented), two statements of cash flows and two statements of changes in equity and related notes, including comparative information for all statements presented.

Non-Australian-Accounting-Standards comparative information and historical summaries

22

Some entities present historical summaries of selected data for periods before the first period for which they present full comparative information in accordance with Australian Accounting Standards. This Standard does not require such summaries to comply with the recognition and measurement requirements of Australian Accounting Standards. Furthermore, some entities present comparative information in accordance with previous GAAP as well as the comparative information required by AASB 101. In any financial statements containing historical summaries or comparative information in accordance with previous GAAP, an entity shall:

(a) label the previous GAAP information prominently as not being prepared in accordance with Australian Accounting Standards; and

(b) disclose the nature of the main adjustments that would make it comply with Australian Accounting Standards. An entity need not quantify those adjustments.

Explanation of transition to Australian Accounting Standards

23

An entity shall explain how the transition from previous GAAP to Australian Accounting Standards affected its reported financial position, financial performance and cash flows.

23A

An entity that has applied Australian Accounting Standards or IFRSs in a previous period, as described in paragraph 4A, shall disclose:

(a) the reason it stopped applying Australian Accounting Standards or IFRSs; and

(b) the reason it is resuming or commencing the application of Australian Accounting Standards.

23B

When an entity, in accordance with paragraph 4A, does not elect to apply AASB 1, the entity shall explain the reasons for electing to apply Australian Accounting Standards as if it had never stopped applying Australian Accounting Standards or IFRSs.

Reconciliations

24

To comply with paragraph 23, an entity’s first Australian-Accounting-Standards financial statements shall include:

(a) reconciliations of its equity reported in accordance with previous GAAP to its equity in accordance with Australian Accounting Standards for both of the following dates:

(i) the date of transition to Australian Accounting Standards; and

(ii) the end of the latest period presented in the entity’s most recent annual financial statements in accordance with previous GAAP.

(b) a reconciliation to its total comprehensive income in accordance with Australian Accounting Standards for the latest period in the entity’s most recent annual financial statements. The starting point for that reconciliation shall be total comprehensive income in accordance with previous GAAP for the same period or, if an entity did not report such a total, profit or loss under previous GAAP.

(c) if the entity recognised or reversed any impairment losses for the first time in preparing its opening Australian-Accounting-Standards statement of financial position, the disclosures that AASB 136 Impairment of Assets would have required if the entity had recognised those impairment losses or reversals in the period beginning with the date of transition to Australian Accounting Standards.

25

The reconciliations required by paragraph 24(a) and (b) shall give sufficient detail to enable users to understand the material adjustments to the statement of financial position and statement of comprehensive income. If an entity presented a statement of cash flows under its previous GAAP, it shall also explain the material adjustments to the statement of cash flows.

26

If an entity becomes aware of errors made under previous GAAP, the reconciliations required by paragraph 24(a) and (b) shall distinguish the correction of those errors from changes in accounting policies.

27

AASB 108 does not apply to the changes in accounting policies an entity makes when it adopts Australian Accounting Standards or to changes in those policies until after it presents its first Australian-Accounting-Standards financial statements. Therefore, AASB 108’s requirements about changes in accounting policies do not apply in an entity’s first Australian-Accounting-Standards financial statements.

27A

If during the period covered by its first Australian-Accounting-Standards financial statements an entity changes its accounting policies or its use of the exemptions contained in this Standard, it shall explain the changes between its first Australian-Accounting-Standards interim financial report and its first Australian-Accounting-Standards financial statements, in accordance with paragraph 23, and it shall update the reconciliations required by paragraph 24(a) and (b).

28

If an entity did not present financial statements for previous periods, its first Australian-Accounting-Standards financial statements shall disclose that fact.

Designation of financial assets or financial liabilities

29

An entity is permitted to designate a previously recognised financial asset as a financial asset measured at fair value through profit or loss in accordance with paragraph D19A. The entity shall disclose the fair value of financial assets so designated at the date of designation and their classification and carrying amount in the previous financial statements.

29A

An entity is permitted to designate a previously recognised financial liability as a financial liability at fair value through profit or loss in accordance with paragraph D19. The entity shall disclose the fair value of financial liabilities so designated at the date of designation and their classification and carrying amount in the previous financial statements.

Use of fair value as deemed cost

30

If an entity uses fair value in its opening Australian-Accounting-Standards statement of financial position as deemed cost for an item of property, plant and equipment, an investment property, an intangible asset or a right-of-use asset (see paragraphs D5 and D7), the entity’s first Australian-Accounting-Standards financial statements shall disclose, for each line item in the opening Australian-Accounting-Standards statement of financial position:

(a) the aggregate of those fair values; and

(b) the aggregate adjustment to the carrying amounts reported under previous GAAP.

Use of deemed cost for investments in subsidiaries, joint ventures and associates

31

Similarly, if an entity uses a deemed cost in its opening Australian-Accounting-Standards statement of financial position for an investment in a subsidiary, joint venture or associate in its separate financial statements (see paragraph D15), the entity’s first Australian-Accounting-Standards separate financial statements shall disclose:

(a) the aggregate deemed cost of those investments for which deemed cost is their previous GAAP carrying amount;

(b) the aggregate deemed cost of those investments for which deemed cost is fair value; and

(c) the aggregate adjustment to the carrying amounts reported under previous GAAP.

Use of deemed cost for oil and gas assets

31A

If an entity uses the exemption in paragraph D8A(b) for oil and gas assets, it shall disclose that fact and the basis on which carrying amounts determined under previous GAAP were allocated.

Use of deemed cost for operations subject to rate regulation

31B

If an entity uses the exemption in paragraph D8B for operations subject to rate regulation, it shall disclose that fact and the basis on which carrying amounts were determined under previous GAAP.

Use of deemed cost after severe hyperinflation

31C

If an entity elects to measure assets and liabilities at fair value and to use that fair value as the deemed cost in its opening Australian-Accounting-Standards statement of financial position because of severe hyperinflation (see paragraphs D26–D30), the entity’s first Australian-Accounting-Standards financial statements shall disclose an explanation of how, and why, the entity had, and then ceased to have, a functional currency that has both of the following characteristics:

(a) a reliable general price index is not available to all entities with transactions and balances in the currency.

(b) exchangeability between the currency and a relatively stable foreign currency does not exist.

Interim financial reports

32

To comply with paragraph 23, if an entity presents an interim financial report in accordance with AASB 134 for part of the period covered by its first Australian-Accounting-Standards financial statements, the entity shall satisfy the following requirements in addition to the requirements of AASB 134:

(a) Each such interim financial report shall, if the entity presented an interim financial report for the comparable interim period of the immediately preceding financial year, include:

(i) a reconciliation of its equity in accordance with previous GAAP at the end of that comparable interim period to its equity under Australian Accounting Standards at that date; and

(ii) a reconciliation to its total comprehensive income in accordance with Australian Accounting Standards for that comparable interim period (current and year to date). The starting point for that reconciliation shall be total comprehensive income in accordance with previous GAAP for that period or, if an entity did not report such a total, profit or loss in accordance with previous GAAP.

(b) In addition to the reconciliations required by (a), an entity’s first interim financial report in accordance with AASB 134 for part of the period covered by its first Australian-Accounting-Standards financial statements shall include the reconciliations described in paragraph 24(a) and (b) (supplemented by the details required by paragraphs 25 and 26) or a cross-reference to another published document that includes these reconciliations.

(c) If an entity changes its accounting policies or its use of the exemptions contained in this Standard, it shall explain the changes in each such interim financial report in accordance with paragraph 23 and update the reconciliations required by (a) and (b).

33

AASB 134 requires minimum disclosures, which are based on the assumption that users of the interim financial report also have access to the most recent annual financial statements. However, AASB 134 also requires an entity to disclose ‘any events or transactions that are material to an understanding of the current interim period’. Therefore, if a first-time adopter did not, in its most recent annual financial statements in accordance with previous GAAP, disclose information material to an understanding of the current interim period, its interim financial report shall disclose that information or include a cross-reference to another published document that includes it.

Effective date

34

An entity shall apply this Standard if its first Australian-Accounting-Standards financial statements are for a period beginning on or after 1 January 2018. Earlier application is permitted for periods beginning after 24 July 2014 but before 1 January 2018.

35–39A

[Deleted by the AASB]

39B

[Deleted]

39C

[Deleted by the AASB]

39D

[Deleted]

39E

[Deleted by the AASB]

39F

[Deleted]

39G

[Deleted]

39H–39N

[Deleted by the AASB]

39O

Paragraphs B10 and B11 refer to AASB 9. If an entity applies this Standard but does not yet apply AASB 9, the references in paragraphs B10 and B11 to AASB 9 shall be read as references to AASB 139 Financial Instruments: Recognition and Measurement.

39P–39T

[Deleted by the AASB]

39U

[Deleted]

39V

AASB 2014-1 Amendments to Australian Accounting Standards, issued in June 2014, amended paragraph D8B in the previous version of this Standard. An entity shall apply that amendment for annual periods beginning on or after 1 January 2016. Earlier application is permitted. If an entity applies AASB 14 for an earlier period, the amendment shall be applied for that earlier period.

39W

AASB 2014-3 Amendments to Australian Accounting Standards – Accounting for Acquisitions of Interests in Joint Operations, issued in August 2014, amended paragraph C5 in the previous version of this Standard. An entity shall apply that amendment in annual periods beginning on or after 1 January 2016. If an entity applies related amendments to AASB 11 from AASB 2014-3 in an earlier period, the amendment to paragraph C5 shall be applied in that earlier period.

39X

AASB 2014-5 Amendments to Australian Accounting Standards arising from AASB 15, issued in December 2014, amended the previous version of this Standard as follows: deleted paragraph D24 and its related heading and added paragraphs D34–D35 and their related heading. An entity shall apply those amendments when it applies AASB 15.

39Y

AASB 2010-7 Amendments to Australian Accounting Standards arising from AASB 9 (December 2010) (as amended), AASB 2014-1 Amendments to Australian Accounting Standards and AASB 2014-7 Amendments to Australian Accounting Standards arising from AASB 9 (December 2014) amended the previous version of this Standard as follows: amended paragraphs 29, B1–B6, D1, D14, D19 and D20, deleted paragraph 39B and added paragraphs 29A, B8–B8G, B9, D19A–D19C, D33, E1 and E2. Paragraph 39G, added by AASB 2010-7, was deleted by AASB 2014-1. Paragraph 39U, added by AASB 2014-1, was deleted by AASB 2014-7. An entity shall apply those amendments when it applies AASB 9.

39Z

AASB 2014-9 Amendments to Australian Accounting Standards – Equity Method in Separate Financial Statements, issued in December 2014, amended the previous version of this Standard as follows: amended paragraph D14 and added paragraph D15A. An entity shall apply those amendments for annual periods beginning on or after 1 January 2016. Earlier application is permitted. If an entity applies those amendments for an earlier period, it shall disclose that fact.

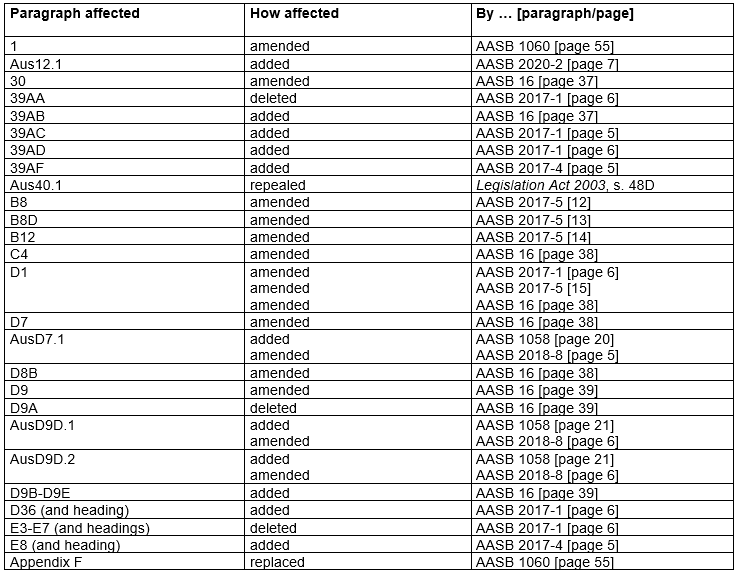

39AA

[Deleted]

39AB

AASB 16 Leases, issued in February 2016, amended paragraphs 30, C4, D1, D7, D8B and D9, deleted paragraph D9A and added paragraphs D9B–D9E. An entity shall apply those amendments when it applies AASB 16.

39AC

AASB 2017-1 Amendments to Australian Accounting Standards – Transfers of Investment Property, Annual Improvements 2014–2016 Cycle and Other Amendments added paragraph D36 and amended paragraph D1. An entity shall apply that amendment when it applies AASB Interpretation 22 Foreign Currency Transactions and Advance Consideration, as identified in AASB 1048 Interpretation of Standards.

39AD

AASB 2017-1 Amendments to Australian Accounting Standards – Transfers of Investment Property, Annual Improvements 2014–2016 Cycle and Other Amendments, issued in February 2017, deleted paragraph 39AA. A for-profit entity shall apply those amendments for annual periods beginning on or after 1 January 2018. A not-for-profit entity shall apply those amendments for annual periods beginning on or after 1 January 2019.

39AF

AASB 2017-4 Amendments to Australian Accounting Standards – Uncertainty over Income Tax Treatments added paragraph E8. An entity shall apply that amendment when it applies AASB Interpretation 23 Uncertainty over Income Tax Treatments, as identified in AASB 1048 Interpretation of Standards.

Withdrawal of AASB pronouncements

Aus40.2

This Standard repeals AASB 1 First-time Adoption of Australian Accounting Standards issued in May 2009. Despite the repeal, after the time this Standard starts to apply under section 334 of the Corporations Act (either generally or in relation to an individual entity), the repealed Standard continues to apply in relation to any period ending before that time as if the repeal had not occurred.

[Note: When this Standard applies under section 334 of the Corporations Act (either generally or in relation to an individual entity), it supersedes the application of the repealed Standard.]

Appendix A -- Defined terms

This appendix is an integral part of the Standard.

date of transition to Australian Accounting Standards

A[1]

The beginning of the earliest period for which an entity presents full comparative information under Australian Accounting Standards in its first Australian-Accounting-Standards financial statements.

deemed cost

A[2]

An amount used as a surrogate for cost or depreciated cost at a given date. Subsequent depreciation or amortisation assumes that the entity had initially recognised the asset or liability at the given date and that its cost was equal to the deemed cost.

fair value

A[3]

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. (See AASB 13.)

first Australian-Accounting-Standards financial statements

A[4]

The first annual financial statements in which an entity adopts Australian Accounting Standards, by an explicit and unreserved statement of compliance with Australian Accounting Standards.

first Australian-Accounting-Standards reporting period

A[5]

The latest reporting period covered by an entity’s first Australian-Accounting-Standards financial statements.

first-time adopter

A[6]

An entity that presents its first Australian-Accounting-Standards financial statements.

International Financial Reporting Standards (IFRSs)

A[7]

Standards and Interpretations issued by the International Accounting Standards Board (IASB). They comprise:

(a) International Financial Reporting Standards;

(b) International Accounting Standards;

(c) IFRIC Interpretations; and

(d) SIC Interpretations.(a)

Definition of IFRSs amended after the name changes introduced by the revised Constitution of the IFRS Foundation in 2010.

opening Australian-Accounting-Standards statement of financial position

A[8]

An entity’s statement of financial position at the date of transition to Australian Accounting Standards.

previous GAAP

A[9]

The basis of accounting that a first-time adopter used immediately before adopting Australian Accounting Standards.

Appendix B -- Exceptions to the retrospective application of other Australian Accounting Standards

This appendix is an integral part of the Standard.

B1

An entity shall apply the following exceptions:

(a) derecognition of financial assets and financial liabilities (paragraphs B2 and B3);

(b) hedge accounting (paragraphs B4–B6);

(c) non-controlling interests (paragraph B7);

(d) classification and measurement of financial assets (paragraph B8–B8C);

(e) impairment of financial assets (paragraphs B8D–B8G);

(f) embedded derivatives (paragraph B9); and

(g) government loans (paragraphs B10–B12).

Derecognition of financial assets and financial liabilities

B2

Except as permitted by paragraph B3, a first-time adopter shall apply the derecognition requirements in AASB 9 prospectively for transactions occurring on or after the date of transition to Australian Accounting Standards. For example, if a first-time adopter derecognised non-derivative financial assets or non-derivative financial liabilities in accordance with its previous GAAP as a result of a transaction that occurred before the date of transition to Australian Accounting Standards, it shall not recognise those assets and liabilities in accordance with Australian Accounting Standards (unless they qualify for recognition as a result of a later transaction or event).

B3

Despite paragraph B2, an entity may apply the derecognition requirements in AASB 9 retrospectively from a date of the entity’s choosing, provided that the information needed to apply AASB 9 to financial assets and financial liabilities derecognised as a result of past transactions was obtained at the time of initially accounting for those transactions.

Hedge accounting

B4

As required by AASB 9, at the date of transition to Australian Accounting Standards an entity shall:

(a) measure all derivatives at fair value; and

(b) eliminate all deferred losses and gains arising on derivatives that were reported in accordance with previous GAAP as if they were assets or liabilities.

B5

An entity shall not reflect in its opening Australian-Accounting-Standards statement of financial position a hedging relationship of a type that does not qualify for hedge accounting in accordance with AASB 9 (for example, many hedging relationships where the hedging instrument is a stand-alone written option or a net written option; or where the hedged item is a net position in a cash flow hedge for another risk than foreign currency risk). However, if an entity designated a net position as a hedged item in accordance with previous GAAP, it may designate as a hedged item in accordance with Australian Accounting Standards an individual item within that net position, or a net position if that meets the requirements in paragraph 6.6.1 of AASB 9, provided that it does so no later than the date of transition to Australian Accounting Standards.

B6

If, before the date of transition to Australian Accounting Standards, an entity had designated a transaction as a hedge but the hedge does not meet the conditions for hedge accounting in AASB 9, the entity shall apply paragraphs 6.5.6 and 6.5.7 of AASB 9 to discontinue hedge accounting. Transactions entered into before the date of transition to Australian Accounting Standards shall not be retrospectively designated as hedges.

Non-controlling interests

B7

A first-time adopter shall apply the following requirements of AASB 10 prospectively from the date of transition to Australian Accounting Standards:

(a) the requirement in paragraph B94 that total comprehensive income is attributed to the owners of the parent and to the non-controlling interests even if this results in the non-controlling interests having a deficit balance;

(b) the requirements in paragraphs 23 and B96 for accounting for changes in the parent’s ownership interest in a subsidiary that do not result in a loss of control; and

(c) the requirements in paragraphs B97–B99 for accounting for a loss of control over a subsidiary, and the related requirements of paragraph 8A of AASB 5 Non-current Assets Held for Sale and Discontinued Operations.

However, if a first-time adopter elects to apply AASB 3 retrospectively to past business combinations, it shall also apply AASB 10 in accordance with paragraph C1 of this Standard.

Classification and measurement of financial instruments

B8

An entity shall assess whether a financial asset meets the conditions in paragraph 4.1.2 of AASB 9 or the conditions in paragraph 4.1.2A of AASB 9 on the basis of the facts and circumstances that exist at the date of transition to Australian Accounting Standards.

B8A

If it is impracticable to assess a modified time value of money element in accordance with paragraphs B4.1.9B–B4.1.9D of AASB 9 on the basis of the facts and circumstances that exist at the date of transition to Australian Accounting Standards, an entity shall assess the contractual cash flow characteristics of that financial asset on the basis of the facts and circumstances that existed at the date of transition to Australian Accounting Standards without taking into account the requirements related to the modification of the time value of money element in paragraphs B4.1.9B–B4.1.9D of AASB 9. (In this case, the entity shall also apply paragraph 42R of AASB 7 but references to ‘paragraph 7.2.4 of AASB 9’ shall be read to mean this paragraph and references to ‘initial recognition of the financial asset’ shall be read to mean ‘at the date of transition to Australian Accounting Standards’.)

B8B

If it is impracticable to assess whether the fair value of a prepayment feature is insignificant in accordance with paragraph B4.1.12(c) of AASB 9 on the basis of the facts and circumstances that exist at the date of transition to Australian Accounting Standards, an entity shall assess the contractual cash flow characteristics of that financial asset on the basis of the facts and circumstances that existed at the date of transition to Australian Accounting Standards without taking into account the exception for prepayment features in paragraph B4.1.12 of AASB 9. (In this case, the entity shall also apply paragraph 42S of AASB 7 but references to ‘paragraph 7.2.5 of AASB 9’ shall be read to mean this paragraph and references to ‘initial recognition of the financial asset’ shall be read to mean ‘at the date of transition to Australian Accounting Standards’.)

B8C

If it is impracticable (as defined in AASB 108) for an entity to apply retrospectively the effective interest method in AASB 9, the fair value of the financial asset or the financial liability at the date of transition to Australian Accounting Standards shall be the new gross carrying amount of that financial asset or the new amortised cost of that financial liability at the date of transition to Australian Accounting Standards.

Impairment of financial assets

B8D

An entity shall apply the impairment requirements in Section 5.5 of AASB 9 retrospectively subject to paragraphs B8E–B8G and E1–E2.

B8E

At the date of transition to Australian Accounting Standards, an entity shall use reasonable and supportable information that is available without undue cost or effort to determine the credit risk at the date that financial instruments were initially recognised (or for loan commitments and financial guarantee contracts the date that the entity became a party to the irrevocable commitment in accordance with paragraph 5.5.6 of AASB 9) and compare that to the credit risk at the date of transition to Australian Accounting Standards (also see paragraphs B7.2.2–B7.2.3 of AASB 9).

B8F

When determining whether there has been a significant increase in credit risk since initial recognition, an entity may apply:

(a) the requirements in paragraph 5.5.10 and B5.5.22–B5.5.24 of AASB 9; and

(b) the rebuttable presumption in paragraph 5.5.11 of AASB 9 for contractual payments that are more than 30 days past due if an entity will apply the impairment requirements by identifying significant increases in credit risk since initial recognition for those financial instruments on the basis of past due information.

B8G

If, at the date of transition to Australian Accounting Standards, determining whether there has been a significant increase in credit risk since the initial recognition of a financial instrument would require undue cost or effort, an entity shall recognise a loss allowance at an amount equal to lifetime expected credit losses at each reporting date until that financial instrument is derecognised (unless that financial instrument is low credit risk at a reporting date, in which case paragraph B8F(a) applies).

Embedded derivatives

B9

A first-time adopter shall assess whether an embedded derivative is required to be separated from the host contract and accounted for as a derivative on the basis of the conditions that existed at the later of the date it first became a party to the contract and the date a reassessment is required by paragraph B4.3.11 of AASB 9.

Government loans

B10

A first-time adopter shall classify all government loans received as a financial liability or an equity instrument in accordance with AASB 132 Financial Instruments: Presentation. Except as permitted by paragraph B11, a first-time adopter shall apply the requirements in AASB 9 Financial Instruments and AASB 120 Accounting for Government Grants and Disclosure of Government Assistance prospectively to government loans existing at the date of transition to Australian Accounting Standards and shall not recognise the corresponding benefit of the government loan at a below-market rate of interest as a government grant. Consequently, if a first-time adopter did not, under its previous GAAP, recognise and measure a government loan at a below-market rate of interest on a basis consistent with Australian-Accounting-Standards requirements, it shall use its previous GAAP carrying amount of the loan at the date of transition to Australian Accounting Standards as the carrying amount of the loan in the opening Australian-Accounting-Standards statement of financial position. An entity shall apply AASB 9 to the measurement of such loans after the date of transition to Australian Accounting Standards.

B11

Despite paragraph B10, an entity may apply the requirements in AASB 9 and AASB 120 retrospectively to any government loan originated before the date of transition to Australian Accounting Standards, provided that the information needed to do so had been obtained at the time of initially accounting for that loan.

B12

The requirements and guidance in paragraphs B10 and B11 do not preclude an entity from being able to use the exemptions described in paragraphs D19–D19C relating to the designation of previously recognised financial instruments at fair value through profit or loss.

Appendix C -- Exemptions for business combinations

This appendix is an integral part of the Standard. An entity shall apply the following requirements to business combinations that the entity recognised before the date of transition to Australian Accounting Standards. This Appendix should only be applied to business combinations within the scope of AASB 3 Business Combinations.

C1

A first-time adopter may elect not to apply AASB 3 retrospectively to past business combinations (business combinations that occurred before the date of transition to Australian Accounting Standards). However, if a first-time adopter restates any business combination to comply with AASB 3, it shall restate all later business combinations and shall also apply AASB 10 from that same date. For example, if a first-time adopter elects to restate a business combination that occurred on 30 June 20X6, it shall restate all business combinations that occurred between 30 June 20X6 and the date of transition to Australian Accounting Standards, and it shall also apply AASB 10 from 30 June 20X6.

C2

An entity need not apply AASB 121 The Effects of Changes in Foreign Exchange Rates retrospectively to fair value adjustments and goodwill arising in business combinations that occurred before the date of transition to Australian Accounting Standards. If the entity does not apply AASB 121 retrospectively to those fair value adjustments and goodwill, it shall treat them as assets and liabilities of the entity rather than as assets and liabilities of the acquiree. Therefore, those goodwill and fair value adjustments either are already expressed in the entity’s functional currency or are non-monetary foreign currency items, which are reported using the exchange rate applied in accordance with previous GAAP.

C3

An entity may apply AASB 121 retrospectively to fair value adjustments and goodwill arising in either:

(a) all business combinations that occurred before the date of transition to Australian Accounting Standards; or

(b) all business combinations that the entity elects to restate to comply with AASB 3, as permitted by paragraph C1 above.

C4

If a first-time adopter does not apply AASB 3 retrospectively to a past business combination, this has the following consequences for that business combination:

(a) The first-time adopter shall keep the same classification (as an acquisition by the legal acquirer, a reverse acquisition by the legal acquiree, or a uniting of interests) as in its previous GAAP financial statements.

(b) The first-time adopter shall recognise all its assets and liabilities at the date of transition to Australian Accounting Standards that were acquired or assumed in a past business combination, other than:

(i) some financial assets and financial liabilities derecognised in accordance with previous GAAP (see paragraph B2); and

(ii) assets, including goodwill, and liabilities that were not recognised in the acquirer’s consolidated statement of financial position in accordance with previous GAAP and also would not qualify for recognition in accordance with Australian Accounting Standards in the separate statement of financial position of the acquiree (see (f)–(i) below).

The first-time adopter shall recognise any resulting change by adjusting retained earnings (or, if appropriate, another category of equity), unless the change results from the recognition of an intangible asset that was previously subsumed within goodwill (see (g)(i) below).

(c) The first-time adopter shall exclude from its opening Australian-Accounting-Standards statement of financial position any item recognised in accordance with previous GAAP that does not qualify for recognition as an asset or liability under Australian Accounting Standards. The first-time adopter shall account for the resulting change as follows:

(i) the first-time adopter may have classified a past business combination as an acquisition and recognised as an intangible asset an item that does not qualify for recognition as an asset in accordance with AASB 138 Intangible Assets. It shall reclassify that item (and, if any, the related deferred tax and non-controlling interests) as part of goodwill (unless it deducted goodwill directly from equity in accordance with previous GAAP, see (g)(i) and (i) below).

(ii) the first-time adopter shall recognise all other resulting changes in retained earnings.[2]

(d) Australian Accounting Standards require subsequent measurement of some assets and liabilities on a basis that is not based on original cost, such as fair value. The first-time adopter shall measure these assets and liabilities on that basis in its opening Australian-Accounting-Standards statement of financial position, even if they were acquired or assumed in a past business combination. It shall recognise any resulting change in the carrying amount by adjusting retained earnings (or, if appropriate, another category of equity), rather than goodwill.

(e) Immediately after the business combination, the carrying amount in accordance with previous GAAP of assets acquired and liabilities assumed in that business combination shall be their deemed cost in accordance with Australian Accounting Standards at that date. If Australian Accounting Standards require a cost-based measurement of those assets and liabilities at a later date, that deemed cost shall be the basis for cost-based depreciation or amortisation from the date of the business combination.

(f) If an asset acquired, or liability assumed, in a past business combination was not recognised in accordance with previous GAAP, it does not have a deemed cost of zero in the opening Australian-Accounting-Standards statement of financial position. Instead, the acquirer shall recognise and measure it in its consolidated statement of financial position on the basis that Australian Accounting Standards would require in the statement of financial position of the acquiree. To illustrate: if the acquirer had not, in accordance with its previous GAAP, capitalised leases acquired in a past business combination in which the acquiree was a lessee, it shall capitalise those leases in its consolidated financial statements, as AASB 16 Leases would require the acquiree to do in its Australian-Accounting-Standards statement of financial position. Similarly, if the acquirer had not, in accordance with its previous GAAP, recognised a contingent liability that still exists at the date of transition to Australian Accounting Standards, the acquirer shall recognise that contingent liability at that date unless AASB 137 Provisions, Contingent Liabilities and Contingent Assets would prohibit its recognition in the financial statements of the acquiree. Conversely, if an asset or liability was subsumed in goodwill in accordance with previous GAAP but would have been recognised separately under AASB 3, that asset or liability remains in goodwill unless Australian Accounting Standards would require its recognition in the financial statements of the acquiree.

(g) The carrying amount of goodwill in the opening Australian-Accounting-Standards statement of financial position shall be its carrying amount in accordance with previous GAAP at the date of transition to Australian Accounting Standards, after the following two adjustments:

(i) If required by (c)(i) above, the first-time adopter shall increase the carrying amount of goodwill when it reclassifies an item that it recognised as an intangible asset in accordance with previous GAAP. Similarly, if (f) above requires the first-time adopter to recognise an intangible asset that was subsumed in recognised goodwill in accordance with previous GAAP, the first-time adopter shall decrease the carrying amount of goodwill accordingly (and, if applicable, adjust deferred tax and non-controlling interests).

(ii) Regardless of whether there is any indication that the goodwill may be impaired, the first-time adopter shall apply AASB 136 in testing the goodwill for impairment at the date of transition to Australian Accounting Standards and in recognising any resulting impairment loss in retained earnings (or, if so required by AASB 136, in revaluation surplus). The impairment test shall be based on conditions at the date of transition to Australian Accounting Standards.

(h) No other adjustments shall be made to the carrying amount of goodwill at the date of transition to Australian Accounting Standards. For example, the first-time adopter shall not restate the carrying amount of goodwill:

(i) to exclude in-process research and development acquired in that business combination (unless the related intangible asset would qualify for recognition in accordance with AASB 138 in the statement of financial position of the acquiree);

(ii) to adjust previous amortisation of goodwill;

(iii) to reverse adjustments to goodwill that AASB 3 would not permit, but were made in accordance with previous GAAP because of adjustments to assets and liabilities between the date of the business combination and the date of transition to Australian Accounting Standards.

(i) If the first-time adopter recognised goodwill in accordance with previous GAAP as a deduction from equity:

(i) it shall not recognise that goodwill in its opening Australian-Accounting-Standards statement of financial position. Furthermore, it shall not reclassify that goodwill to profit or loss if it disposes of the subsidiary or if the investment in the subsidiary becomes impaired.

(ii) adjustments resulting from the subsequent resolution of a contingency affecting the purchase consideration shall be recognised in retained earnings.

(j) In accordance with its previous GAAP, the first-time adopter may not have consolidated a subsidiary acquired in a past business combination (for example, because the parent did not regard it as a subsidiary in accordance with previous GAAP or did not prepare consolidated financial statements). The first-time adopter shall adjust the carrying amounts of the subsidiary’s assets and liabilities to the amounts that Australian Accounting Standards would require in the subsidiary’s statement of financial position. The deemed cost of goodwill equals the difference at the date of transition to Australian Accounting Standards between:

(i) the parent’s interest in those adjusted carrying amounts; and

(ii) the cost in the parent’s separate financial statements of its investment in the subsidiary.

(k) The measurement of non-controlling interests and deferred tax follows from the measurement of other assets and liabilities. Therefore, the above adjustments to recognised assets and liabilities affect non-controlling interests and deferred tax.

C5

The exemption for past business combinations also applies to past acquisitions of investments in associates, interests in joint ventures and interests in joint operations in which the activity of the joint operation constitutes a business, as defined in AASB 3. Furthermore, the date selected for paragraph C1 applies equally for all such acquisitions.

Such changes include reclassifications from or to intangible assets if goodwill was not recognised in accordance with previous GAAP as an asset. This arises if, in accordance with previous GAAP, the entity (a) deducted goodwill directly from equity or (b) did not treat the business combination as an acquisition.

Appendix D -- Exemptions from other Australian Accounting Standards

This appendix is an integral part of the Standard.

D1

An entity may elect to use one or more of the following exemptions:

(a) share-based payment transactions (paragraphs D2 and D3);

(b) insurance contracts (paragraph D4);

(c) deemed cost (paragraphs D5–D8B);

(d) leases (paragraphs D9 and D9B–D9E);

(e) [deleted]

(f) cumulative translation differences (paragraphs D12 and D13);

(g) investments in subsidiaries, joint ventures and associates (paragraphs D14–D15A);

(h) assets and liabilities of subsidiaries, associates and joint ventures (paragraphs D16 and D17);

(i) compound financial instruments (paragraph D18);

(j) designation of previously recognised financial instruments (paragraphs D19–D19C);

(k) fair value measurement of financial assets or financial liabilities at initial recognition (paragraph D20);

(l) decommissioning liabilities included in the cost of property, plant and equipment (paragraphs D21 and D21A);

(m) financial assets or intangible assets accounted for in accordance with Interpretation 12 Service Concession Arrangements as identified in AASB 1048 Interpretation of Standards (paragraph D22);

(n) borrowing costs (paragraph D23);

(o) transfers of assets from customers (paragraph D24);

(p) extinguishing financial liabilities with equity instruments (paragraph D25);

(q) severe hyperinflation (paragraphs D26–D30);

(r) joint arrangements (paragraph D31);

(s) stripping costs in the production phase of a surface mine (paragraph D32);

(t) designation of contracts to buy or sell a non-financial item (paragraph D33);

(u) revenue (paragraphs D34 and D35); and

(v) foreign currency transactions and advance consideration (paragraph D36).

An entity shall not apply these exemptions by analogy to other items.

Share-based payment transactions

D2

A first-time adopter is encouraged, but not required, to apply AASB 2 Share-based Payment to equity instruments that were granted on or before 7 November 2002. A first-time adopter is also encouraged, but not required, to apply AASB 2 to equity instruments that were granted after 7 November 2002 and vested before the later of (a) the date of transition to Australian Accounting Standards and (b) 1 January 2005. However, if a first-time adopter elects to apply AASB 2 to such equity instruments, it may do so only if the entity has disclosed publicly the fair value of those equity instruments, determined at the measurement date, as defined in AASB 2. For all grants of equity instruments to which AASB 2 has not been applied (eg equity instruments granted on or before 7 November 2002), a first-time adopter shall nevertheless disclose the information required by paragraphs 44 and 45 of AASB 2. If a first-time adopter modifies the terms or conditions of a grant of equity instruments to which AASB 2 has not been applied, the entity is not required to apply paragraphs 26–29 of AASB 2 if the modification occurred before the date of transition to Australian Accounting Standards.

D3

A first-time adopter is encouraged, but not required, to apply AASB 2 to liabilities arising from share-based payment transactions that were settled before the date of transition to Australian Accounting Standards. A first-time adopter is also encouraged, but not required, to apply AASB 2 to liabilities that were settled before 1 January 2005. For liabilities to which AASB 2 is applied, a first-time adopter is not required to restate comparative information to the extent that the information relates to a period or date that is earlier than 7 November 2002.

Insurance contracts

Deemed cost

D5

An entity may elect to measure an item of property, plant and equipment at the date of transition to Australian Accounting Standards at its fair value and use that fair value as its deemed cost at that date.

D6

A first-time adopter may elect to use a previous GAAP revaluation of an item of property, plant and equipment at, or before, the date of transition to Australian Accounting Standards as deemed cost at the date of the revaluation, if the revaluation was, at the date of the revaluation, broadly comparable to:

(a) fair value; or

(b) cost or depreciated cost in accordance with Australian Accounting Standards, adjusted to reflect, for example, changes in a general or specific price index.

D7

The elections in paragraphs D5 and D6 are also available for:

(a) investment property, if an entity elects to use the cost model in AASB 140 Investment Property;

(aa) right-of-use assets (AASB 16 Leases); and

(b) intangible assets that meet:

(i) the recognition criteria in AASB 138 (including reliable measurement of original cost); and

(ii) the criteria in AASB 138 for revaluation (including the existence of an active market).

An entity shall not use these elections for other assets or for liabilities.

AusD7.1

Notwithstanding paragraphs D5–D7, where a lessee is a not-for-profit entity, the entity may elect to measure a class of right-of-use assets arising under leases that had at inception significantly below-market terms and conditions principally to enable the entity to further its objectives at fair value at the beginning of the current period presented in the entity’s first Australian-Accounting-Standards financial statements or at the previous GAAP valuation if that valuation broadly reflects that fair value.

D8

A first-time adopter may have established a deemed cost in accordance with previous GAAP for some or all of its assets and liabilities by measuring them at their fair value at one particular date because of an event such as a privatisation or initial public offering.

(a) If the measurement date is at or before the date of transition to Australian Accounting Standards, the entity may use such event-driven fair value measurements as deemed cost for Australian Accounting Standards at the date of that measurement.

(b) If the measurement date is after the date of transition to Australian Accounting Standards, but during the period covered by the first Australian-Accounting-Standards financial statements, the event-driven fair value measurements may be used as deemed cost when the event occurs. An entity shall recognise the resulting adjustments directly in retained earnings (or if appropriate, another category of equity) at the measurement date. At the date of transition to Australian Accounting Standards, the entity shall either establish the deemed cost by applying the criteria in paragraphs D5–D7 or measure assets and liabilities in accordance with the other requirements in this Standard.

D8A

Under some national accounting requirements exploration and development costs for oil and gas properties in the development or production phases are accounted for in cost centres that include all properties in a large geographical area. A first-time adopter using such accounting under previous GAAP may elect to measure oil and gas assets at the date of transition to Australian Accounting Standards on the following basis:

(a) exploration and evaluation assets at the amount determined under the entity’s previous GAAP; and

(b) assets in the development or production phases at the amount determined for the cost centre under the entity’s previous GAAP. The entity shall allocate this amount to the cost centre’s underlying assets pro rata using reserve volumes or reserve values as of that date.

The entity shall test exploration and evaluation assets and assets in the development and production phases for impairment at the date of transition to Australian Accounting Standards in accordance with AASB 6 Exploration for and Evaluation of Mineral Resources or AASB 136 respectively and, if necessary, reduce the amount determined in accordance with (a) or (b) above. For the purposes of this paragraph, oil and gas assets comprise only those assets used in the exploration, evaluation, development or production of oil and gas.

D8B

Some entities hold items of property, plant and equipment, right-of-use assets or intangible assets that are used, or were previously used, in operations subject to rate regulation. The carrying amount of such items might include amounts that were determined under previous GAAP but do not qualify for capitalisation in accordance with Australian Accounting Standards. If this is the case, a first-time adopter may elect to use the previous GAAP carrying amount of such an item at the date of transition to Australian Accounting Standards as deemed cost. If an entity applies this exemption to an item, it need not apply it to all items. At the date of transition to Australian Accounting Standards, an entity shall test for impairment in accordance with AASB 136 each item for which this exemption is used. For the purposes of this paragraph, operations are subject to rate regulation if they are governed by a framework for establishing the prices that can be charged to customers for goods or services and that framework is subject to oversight and/or approval by a rate regulator (as defined in AASB 14 Regulatory Deferral Accounts).

Leases

D9

A first-time adopter may assess whether a contract existing at the date of transition to Australian Accounting Standards contains a lease by applying paragraphs 9–11 of AASB 16 to those contracts on the basis of facts and circumstances existing at that date.

D9A

[Deleted]

D9B

When a first-time adopter that is a lessee recognises lease liabilities and right-of-use assets, it may apply the following approach to all of its leases (subject to the practical expedients described in paragraph D9D):

(a) measure a lease liability at the date of transition to Australian Accounting Standards. A lessee following this approach shall measure that lease liability at the present value of the remaining lease payments (see paragraph D9E), discounted using the lessee’s incremental borrowing rate (see paragraph D9E) at the date of transition to Australian Accounting Standards.

(b) measure a right-of-use asset at the date of transition to Australian Accounting Standards. The lessee shall choose, on a lease-by-lease basis, to measure that right-of-use asset at either:

(i) its carrying amount as if AASB 16 had been applied since the commencement date of the lease (see paragraph D9E), but discounted using the lessee’s incremental borrowing rate at the date of transition to Australian Accounting Standards; or

(ii) an amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments relating to that lease recognised in the statement of financial position immediately before the date of transition to Australian Accounting Standards.

(c) apply AASB 136 to right-of-use assets at the date of transition to Australian Accounting Standards.

D9C

Notwithstanding the requirements in paragraph D9B, a first-time adopter that is a lessee shall measure the right-of-use asset at fair value at the date of transition to Australian Accounting Standards for leases that meet the definition of investment property in AASB 140 and are measured using the fair value model in AASB 140 from the date of transition to Australian Accounting Standards.

D9D

A first-time adopter that is a lessee may do one or more of the following at the date of transition to Australian Accounting Standards, applied on a lease-by-lease basis:

(a) apply a single discount rate to a portfolio of leases with reasonably similar characteristics (for example, a similar remaining lease term for a similar class of underlying asset in a similar economic environment).

(b) elect not to apply the requirements in paragraph D9B to leases for which the lease term (see paragraph D9E) ends within 12 months of the date of transition to Australian Accounting Standards. Instead, the entity shall account for (including disclosure of information about) these leases as if they were short-term leases accounted for in accordance with paragraph 6 of AASB 16.

(c) elect not to apply the requirements in paragraph D9B to leases for which the underlying asset is of low value (as described in paragraphs B3–B8 of AASB 16). Instead, the entity shall account for (including disclosure of information about) these leases in accordance with paragraph 6 of AASB 16.

(d) exclude initial direct costs (see paragraph D9E) from the measurement of the right-of-use asset at the date of transition to Australian Accounting Standards.

(e) use hindsight, such as in determining the lease term if the contract contains options to extend or terminate the lease.

AusD9D.1

Notwithstanding paragraphs D9B–D9D, where a lessee is a not-for-profit entity and the lease had at inception significantly below-market terms and conditions principally to enable the entity to further its objectives, all references in those paragraphs to the date of transition to Australian Accounting Standards shall be read as referring to the beginning of the current period presented in the entity’s first Australian-Accounting-Standards financial statements. Consequently, the entity shall measure the lease liability and the right-of-use asset at that date.

AusD9D.2

Where a lessee is a not-for-profit entity and elects to measure at fair value in accordance with paragraph AusD7.1 a class of right-of-use assets arising under leases that had at inception significantly below-market terms and conditions principally to enable the entity to further its objectives, the entity shall also recognise any related items in accordance with paragraph 9 of AASB 1058 Income of Not-for-Profit Entities. Any income arising shall be recognised as an adjustment to the opening balance of retained earnings (or another component of equity, as appropriate) at the beginning of the current period presented in the entity’s first Australian-Accounting-Standards financial statements.

D9E

Lease payments, lessee, lessee’s incremental borrowing rate, commencement date of the lease, initial direct costs and lease term are defined terms in AASB 16 and are used in this Standard with the same meaning.

D10–D11

[Deleted]

Cumulative translation differences

D12

AASB 121 requires an entity:

(a) to recognise some translation differences in other comprehensive income and accumulate these in a separate component of equity; and

(b) on disposal of a foreign operation, to reclassify the cumulative translation difference for that foreign operation (including, if applicable, gains and losses on related hedges) from equity to profit or loss as part of the gain or loss on disposal.

D13

However, a first-time adopter need not comply with these requirements for cumulative translation differences that existed at the date of transition to Australian Accounting Standards. If a first-time adopter uses this exemption:

(a) the cumulative translation differences for all foreign operations are deemed to be zero at the date of transition to Australian Accounting Standards; and

(b) the gain or loss on a subsequent disposal of any foreign operation shall exclude translation differences that arose before the date of transition to Australian Accounting Standards and shall include later translation differences.

Investments in subsidiaries, joint ventures and associates

D15

If a first-time adopter measures such an investment at cost in accordance with AASB 127, it shall measure that investment at one of the following amounts in its separate opening Australian-Accounting-Standards statement of financial position:

(a) cost determined in accordance with AASB 127; or

(b) deemed cost. The deemed cost of such an investment shall be its:

(i) fair value at the entity’s date of transition to Australian Accounting Standards in its separate financial statements; or

(ii) previous GAAP carrying amount at that date.

A first-time adopter may choose either (i) or (ii) above to measure its investment in each subsidiary, joint venture or associate that it elects to measure using a deemed cost.

D15A

If a first-time adopter accounts for such an investment using the equity method procedures as described in AASB 128:

(a) the first-time adopter applies the exemption for past business combinations (Appendix C) to the acquisition of the investment.

(b) if the entity becomes a first-time adopter for its separate financial statements earlier than for its consolidated financial statements, and

(i) later than its parent, the entity shall apply paragraph D16 in its separate financial statements.

(ii) later than its subsidiary, the entity shall apply paragraph D17 in its separate financial statements.

Assets and liabilities of subsidiaries, associates and joint ventures

D16

If a subsidiary becomes a first-time adopter later than its parent, the subsidiary shall, in its financial statements, measure its assets and liabilities at either:

(a) the carrying amounts that would be included in the parent’s consolidated financial statements, based on the parent’s date of transition to Australian Accounting Standards, if no adjustments were made for consolidation procedures and for the effects of the business combination in which the parent acquired the subsidiary (this election is not available to a subsidiary of an investment entity, as defined in AASB 10, that is required to be measured at fair value through profit or loss); or

(b) the carrying amounts required by the rest of this Standard, based on the subsidiary’s date of transition to Australian Accounting Standards. These carrying amounts could differ from those described in (a):