This Standard establishes disclosure requirements applicable to entities that are preparing general purpose financial statements and elect to apply the Tier 2 reporting requirements under AASB 1053 Application of Tiers of Australian Accounting Standards.

Preamble

Pronouncement

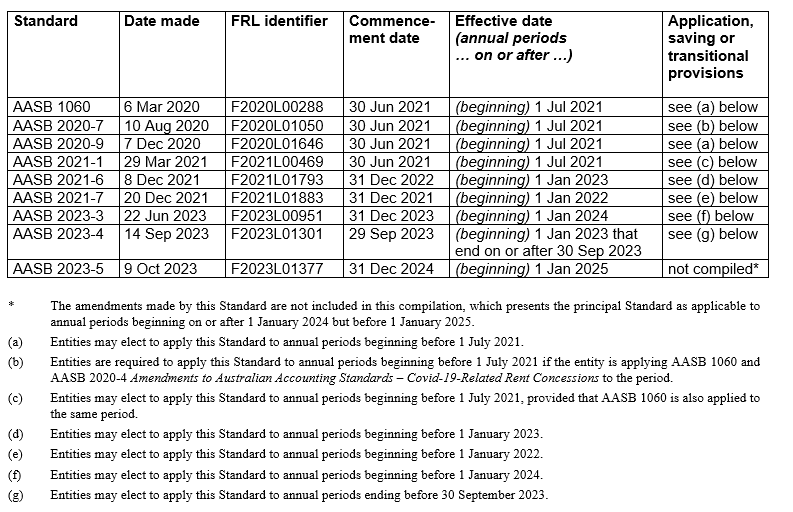

This compiled Standard applies to annual periods beginning on or after 1 January 2024 but before 1 January 2025. Earlier application is permitted for annual periods ending before 1 January 2024. It incorporates relevant amendments made up to and including 14 September 2023.

Prepared on 18 December 2023 by the staff of the Australian Accounting Standards Board.

Compilation no. 5

Compilation date: 31 December 2023

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2023

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The Managing Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

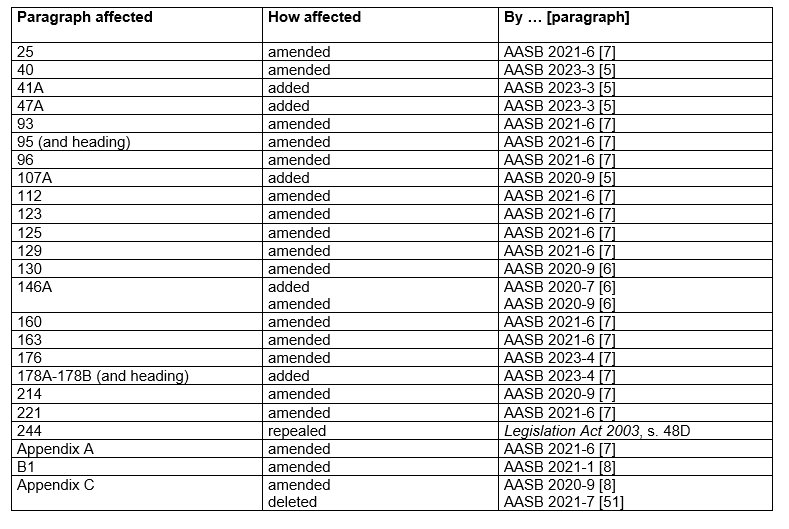

Australian Accounting Standard AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities(as amended) is set out in paragraphs 1 – 243 and Appendices A – C. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the Standard. AASB 1060 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Accounting Standard AASB 1060

The Australian Accounting Standards Board made Accounting Standard AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities under section 334 of the Corporations Act 2001 on 6 March 2020.

This compiled version of AASB 1060 applies to annual periods beginning on or after 1 January 2024 but before 1 January 2025. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 14 September 2023 (see Compilation Details).

Objective

1

This Standard establishes disclosure requirements applicable to entities that are preparing general purpose financial statements and elect to apply the Tier 2 reporting requirements under AASB 1053 Application of Tiers of Australian Accounting Standards.

2

Except to the extent specifically addressed in this Standard, the definitions and presentation requirements of other Australian Accounting Standards continue to apply. Entities are permitted to refer to other Standards for guidance on the requirements in this Standard, including AASB 7 Financial Instruments: Disclosures, AASB 12 Disclosure of Interests in Other Entities, AASB 101 Presentation of Financial Statements, AASB 107 Statement of Cash Flows and AASB 124 Related Party Disclosures.

Scope

3

This Standard applies to all entities that elect to apply Tier 2: Australian Accounting Standards – Simplified Disclosures under AASB 1053, including those that present consolidated financial statements in accordance with AASB 10 Consolidated Financial Statements and those that present separate financial statements in accordance with AASB 127 Separate Financial Statements. However, this Standard does not apply to the structure and content of condensed interim financial statements prepared in accordance with AASB 134 Interim Financial Reporting.

4

Entities applying this Standard are required to apply all the recognition and measurement requirements in Australian Accounting Standards[1] and apply this Standard in relation to disclosure requirements only.

The term ‘Australian Accounting Standards’ refers to Standards (including Interpretations) made by the AASB that apply to any reporting period beginning on or after 1 January 2005. In this context, the term encompasses Australian Accounting Standards – Simplified Disclosures, which some entities are permitted to apply in accordance with AASB 1053 Application of Tiers of Australian Accounting Standards in preparing general purpose financial statements.

5

This Standard uses terminology that is suitable for profit-oriented entities, including public sector business entities. If entities with not-for-profit activities in the private sector or the public sector apply this Standard, they may need to amend the descriptions used for particular line items in the financial statements and for the financial statements themselves.

6

Similarly, entities that do not have equity as defined in AASB 132 Financial Instruments: Presentation (eg some mutual funds) and entities whose share capital is not equity (eg some co-operative entities) may need to adapt the financial statement presentation of members’ or unitholders’ interests.

7

AusCF paragraphs and footnotes included in this Standard apply only to:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

Such entities are referred to as ‘AusCF entities’. For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting (as set out in paragraph Aus1.1 of the Conceptual Framework) shall not apply AusCF paragraphs or footnotes.

Tier 2 disclosures

Financial Statement Presentation

Scope

8

This section explains fair presentation of financial statements, what compliance with Australian Accounting Standards, including this Standard, requires and what a complete set of financial statements is. [IFRS for SMEs Standard paragraph 3.1]

Corresponding AASB Standard: AASB 101 Presentation of Financial Statements.

Fair presentation

9

Financial statements shall present fairly the financial position, financial performance and cash flows of an entity. Fair presentation requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Conceptual Framework for Financial Reporting:

(a) The application of the recognition and measurement requirements in Australian Accounting Standards and the disclosures in this Standard, with additional disclosure when necessary, is presumed to result in financial statements that achieve a fair presentation of the financial position, financial performance and cash flows of Tier 2 entities.

(b) As explained in paragraph 13 of AASB 1053, this Standard does not apply to an entity with public accountability.

The additional disclosures referred to in (a) are necessary when compliance with the specific requirements in this Standard is insufficient to enable users to understand the effect of particular transactions, other events and conditions on the entity’s financial position and financial performance. [Based on IFRS for SMEs Standard paragraph 3.2]

AusCF9

Notwithstanding paragraph 9, in respect of AusCF entities, financial statements shall present fairly the financial position, financial performance and cash flows of an entity. Fair presentation requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Framework for the Preparation and Presentation of Financial Statements:

(a) The application of the recognition and measurement requirements in Australian Accounting Standards and the disclosures in this Standard, with additional disclosure when necessary, is presumed to result in financial statements that achieve a fair presentation of the financial position, financial performance and cash flows of Tier 2 entities.

(b) As explained in paragraph 13 of AASB 1053, this Standard does not apply to an entity with public accountability.

The additional disclosures referred to in (a) are necessary when compliance with the specific requirements in this Standard is insufficient to enable users to understand the effect of particular transactions, other events and conditions on the entity’s financial position and financial performance.

Compliance with Australian Accounting Standards – Simplified Disclosures

10

An entity whose financial statements comply with the recognition and measurement requirements in Australian Accounting Standards, the presentation requirements in those Standards as modified by this Standard, and the disclosure requirements in this Standard shall make an explicit and unreserved statement of such compliance in the notes. Financial statements shall not be described as complying with Australian Accounting Standards – Simplified Disclosures unless they comply with all of these requirements. [Based on IFRS for SMEs Standard paragraph 3.3]

11

An entity shall disclose in the notes:

(a) the statutory basis or other reporting framework, if any, under which the financial statements are prepared; and

(b) whether, for the purposes of preparing the financial statements, it is a for-profit or not-for-profit entity.

12

Entities applying Australian Accounting Standards – Simplified Disclosures shall not depart from a requirement in an Australian Accounting Standard, including this Standard.

13

In the extremely rare circumstances when management concludes that compliance with a recognition and measurement requirement in an Australian Accounting Standard, or a presentation and disclosure requirement in this Standard, would be so misleading that it would conflict with the objective of financial statements set out in the Conceptual Framework for Financial Reporting, but the relevant regulatory framework prohibits departure from the requirement, the entity shall, to the maximum extent possible, reduce the perceived misleading aspects of compliance by disclosing the following:

(a) the title of the Australian Accounting Standard in question, the nature of the requirement and the reason why management has concluded that complying with that requirement is so misleading in the circumstances that it conflicts with the objective of financial statements set out in the Conceptual Framework for Financial Reporting; and

(b) for each period presented, the adjustments to each item in the financial statements that management has concluded would be necessary to achieve a fair presentation.

[Based on IFRS for SMEs Standard paragraph 3.7]

AusCF13

Notwithstanding paragraph 13, in respect of AusCF entities, in the extremely rare circumstances when management concludes that compliance with a recognition and measurement requirement in an Australian Accounting Standard, or a presentation and disclosure requirement in this Standard, would be so misleading that it would conflict with the objective of financial statements set out in the Framework for the Preparation and Presentation of Financial Statements, but the relevant regulatory framework prohibits departure from the requirement, the entity shall, to the maximum extent possible, reduce the perceived misleading aspects of compliance by disclosing the following:

(a) the title of the Australian Accounting Standard in question, the nature of the requirement and the reason why management has concluded that complying with that requirement is so misleading in the circumstances that it conflicts with the objective of financial statements set out in the Framework for the Preparation and Presentation of Financial Statements; and

(b) for each period presented, the adjustments to each item in the financial statements that management has concluded would be necessary to achieve a fair presentation.

Going concern

14

When preparing financial statements, the management of an entity using Australian Accounting Standards – Simplified Disclosures shall make an assessment of the entity’s ability to continue as a going concern. An entity is a going concern unless management either intends to liquidate the entity or to cease operations, or has no realistic alternative but to do so. In assessing whether the going concern assumption is appropriate, management takes into account all available information about the future, which is at least, but is not limited to, twelve months from the reporting date. [IFRS for SMEs Standard paragraph 3.8]

15

When management is aware, in making its assessment, of material uncertainties related to events or conditions that cast significant doubt upon the entity’s ability to continue as a going concern, the entity shall disclose those uncertainties. When an entity does not prepare financial statements on a going concern basis, it shall disclose that fact, together with the basis on which it prepared the financial statements and the reason why the entity is not regarded as a going concern. [IFRS for SMEs Standard paragraph 3.9]

Frequency of reporting

16

An entity shall present a complete set of financial statements (including comparative information – see paragraph 20) at least annually. When the end of an entity’s reporting period changes and the annual financial statements are presented for a period longer or shorter than one year, the entity shall disclose the following:

(a) that fact;

(b) the reason for using a longer or shorter period; and

(c) the fact that comparative amounts presented in the financial statements (including the related notes) are not entirely comparable.

[IFRS for SMEs Standard paragraph 3.10]

Consistency of presentation

17

An entity shall retain the presentation and classification of items in the financial statements from one period to the next unless:

(a) it is apparent, following a significant change in the nature of the entity’s operations or a review of its financial statements, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors; or

(b) Australian Accounting Standards – Simplified Disclosures require a change in presentation.

[IFRS for SMEs Standard paragraph 3.11]

18

When the presentation or classification of items in the financial statements is changed, an entity shall reclassify comparative amounts unless the reclassification is impracticable. When comparative amounts are reclassified, an entity shall disclose the following:

(a) the nature of the reclassification;

(b) the amount of each item or class of items that is reclassified; and

(c) the reason for the reclassification.

[IFRS for SMEs Standard paragraph 3.12]

19

If it is impracticable to reclassify comparative amounts, an entity shall disclose why reclassification was not practicable. [IFRS for SMEs Standard paragraph 3.13]

Comparative information

20

Except when this Standard permits or requires otherwise, an entity shall disclose comparative information in respect of the previous comparable period for all amounts presented in the current period’s financial statements. An entity shall include comparative information for narrative and descriptive information when it is relevant to an understanding of the current period’s financial statements. [IFRS for SMEs Standard paragraph 3.14]

Materiality and aggregation

21

An entity shall present separately each material class of similar items. An entity shall present separately items of a dissimilar nature or function unless they are immaterial. [IFRS for SMEs Standard paragraph 3.15]

22

Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity. [Based on IFRS for SMEs Standard paragraph 3.16]

Complete set of financial statements

25

A complete set of financial statements of an entity shall include all of the following:

(a) a statement of financial position as at the reporting date;

(b) either:

(i) a single statement of profit or loss and other comprehensive income for the reporting period displaying all items of income and expense recognised during the period including those items recognised in determining profit or loss (which is a subtotal in the statement of comprehensive income) and items of other comprehensive income; or

(ii) a separate statement of profit or loss and a separate statement of comprehensive income. If an entity chooses to present both a statement of profit or loss and a statement of comprehensive income, the statement of comprehensive income begins with profit or loss and then displays the items of other comprehensive income;

(c) a statement of changes in equity for the reporting period;

(d) a statement of cash flows for the reporting period; and

(e) notes, comprising material accounting policy information and other explanatory information.

[Based on IFRS for SMEs Standard paragraph 3.17]

26

If the only changes to equity during the periods for which financial statements are presented arise from profit or loss, payment of dividends, corrections of prior period errors, and changes in accounting policy, the entity may present a single statement of income and retained earnings in place of the statement of comprehensive income and statement of changes in equity (see paragraph 62). [IFRS for SMEs Standard paragraph 3.18]

27

If an entity has no items of other comprehensive income in any of the periods for which financial statements are presented, it may present only a statement of profit or loss or it may present a statement of comprehensive income in which the ‘bottom line’ is labelled ‘profit or loss’. [IFRS for SMEs Standard paragraph 3.19]

28

Because paragraph 20 requires comparative amounts in respect of the previous period for all amounts presented in the financial statements, a complete set of financial statements means that an entity shall present, as a minimum, two of each of the required financial statements and related notes. [IFRS for SMEs Standard paragraph 3.20]

29

In a complete set of financial statements, an entity shall present each financial statement with equal prominence. [IFRS for SMEs Standard paragraph 3.21]

30

An entity may use titles for the financial statements other than those used in this Standard as long as they are not misleading. [IFRS for SMEs Standard paragraph 3.22]

Identification of the financial statements

31

An entity shall clearly identify each of the financial statements and the notes and distinguish them from other information in the same document. In addition, an entity shall display the following information prominently and repeat it when necessary for an understanding of the information presented:

(a) the name of the reporting entity and any change in its name since the end of the preceding reporting period;

(b) whether the financial statements cover the individual entity or a group of entities;

(c) the date of the end of the reporting period and the period covered by the financial statements;

(d) the presentation currency, as defined in AASB 121 The Effects of Changes in Foreign Exchange Rates; and

(e) the level of rounding, if any, used in presenting amounts in the financial statements.

[IFRS for SMEs Standard paragraph 3.23]

32

An entity shall disclose the following, if not disclosed elsewhere in information published with the financial statements:

(a) the domicile and legal form of the entity, its country of incorporation and the address of its registered office (or principal place of business, if different from the registered office); and

(b) a description of the nature of the entity’s operations and its principal activities.

[IFRS for SMEs Standard paragraph 3.24]

Presentation of information not required by this Standard

33

This Standard does not address presentation of segment information (AASB 8 Operating Segments), earnings per share (AASB 133 Earnings per Share), or interim financial reports (AASB 134). An entity making such disclosures shall apply the relevant Standards in preparing and presenting the information. [IFRS for SMEs Standard paragraph 3.25]

Statement of Financial Position

Scope of this section

34

This section sets out the information that is to be presented in a statement of financial position and how to present it. The statement of financial position (sometimes called the balance sheet) presents an entity’s assets, liabilities and equity as of a specific date – the end of the reporting period. [IFRS for SMEs Standard paragraph 4.1]

Corresponding AASB Standard: AASB 101 Presentation of Financial Statements.

Information to be presented in the statement of financial position

35

As a minimum, the statement of financial position shall include line items that present the following amounts:

(a) cash and cash equivalents;

(b) trade and other receivables;

(c) financial assets (excluding amounts shown under (a), (b), (i) and (j));

(d) inventories;

(e) property, plant and equipment;

(f) investment property;

(g) intangible assets;

(h) biological assets;

(i) investments in associates;

(j) investments in joint ventures;

(k) trade and other payables;

(l) financial liabilities (excluding amounts shown under (k) and (o));

(m) liabilities and assets for current tax;

(n) deferred tax liabilities and deferred tax assets (these shall always be classified as non-current);

(o) provisions;

(p) non-controlling interests, presented within equity separately from the equity attributable to the owners of the parent;

(q) equity attributable to the owners of the parent;

(r) the total of assets classified as held for sale and assets included in disposal groups classified as held for sale in accordance with AASB 5 Non-current Assets Held for Sale and Discontinued Operations; and

(s) liabilities included in disposal groups classified as held for sale in accordance with AASB 5.

[Based on IFRS for SMEs Standard paragraph 4.2]

36

An entity shall present additional line items, headings and subtotals in the statement of financial position when such presentation is relevant to an understanding of the entity’s financial position. [IFRS for SMEs Standard paragraph 4.3]

Current/non-current distinction

37

An entity shall present current and non-current assets, and current and non-current liabilities, as separate classifications in its statement of financial position in accordance with paragraphs 38–41, except when a presentation based on liquidity provides information that is reliable and more relevant. When that exception applies, all assets and liabilities shall be presented in order of approximate liquidity (ascending or descending). [IFRS for SMEs Standard paragraph 4.4]

Current assets

38

An entity shall classify an asset as current when:

(a) it expects to realise the asset, or intends to sell or consume it, in the entity’s normal operating cycle;

(b) it holds the asset primarily for the purpose of trading;

(c) it expects to realise the asset within twelve months after the reporting date; or

(d) the asset is cash or a cash equivalent, unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date.

[IFRS for SMEs Standard paragraph 4.5]

39

An entity shall classify all other assets as non-current. When the entity’s normal operating cycle is not clearly identifiable, its duration is assumed to be twelve months. [IFRS for SMEs Standard paragraph 4.6]

Current liabilities

40

An entity shall classify a liability as current when:

(a) it expects to settle the liability in the entity’s normal operating cycle;

(b) it holds the liability primarily for the purpose of trading;

(c) the liability is due to be settled within twelve months after the reporting date; or

(d) the entity does not have right at the reporting date to defer settlement of the liability for at least twelve months after the reporting date.

[Based on IFRS for SMEs Standard paragraph 4.7]

41A

Terms of a liability that could, at the option of the counterparty, result in its settlement by the transfer of the entity’s own equity instruments do not affect its classification as current or non-current if, applying AASB 132 Financial Instruments: Presentation, the entity classifies the option as an equity instrument, recognising it separately from the liability as an equity component of a compound financial instrument.

Sequencing of items and format of items in the statement of financial position

42

This Standard does not prescribe the sequence or format in which items are to be presented. Paragraph 35 simply provides a list of items that are sufficiently different in nature or function to warrant separate presentation in the statement of financial position. In addition:

(a) line items are included when the size, nature or function of an item or aggregation of similar items is such that separate presentation is relevant to an understanding of the entity’s financial position; and

(b) the descriptions used and the sequencing of items or aggregation of similar items may be amended according to the nature of the entity and its transactions, to provide information that is relevant to an understanding of the entity’s financial position.

[IFRS for SMEs Standard paragraph 4.9]

43

The judgement on whether additional items are presented separately is based on an assessment of all of the following:

(a) the amounts, nature and liquidity of assets;

(b) the function of assets within the entity; and

(c) the amounts, nature and timing of liabilities.

[IFRS for SMEs Standard paragraph 4.10]

Information to be presented either in the statement of financial position or in the notes

44

An entity shall disclose, either in the statement of financial position or in the notes, further subclassifications of the line items presented, classified in a manner appropriate to the entity’s operation. This includes for example:

(a) property, plant and equipment in classifications appropriate to the entity;

(b) trade and other receivables showing separately amounts due from related parties, amounts due from other parties and contract assets from contracts with customers;

(c) inventories, showing separately amounts of inventories:

(i) held for sale in the ordinary course of business;

(ii) in the process of production for such sale; and

(iii) in the form of materials or supplies to be consumed in the production process or in the rendering of services.

(d) trade and other payables, showing separately amounts payable to trade suppliers, amounts payable to related parties, contract liabilities from contracts with customers and accruals;

(e) provisions for employee benefits and other provisions; and

(f) classes of equity, such as paid-in capital, share premium, retained earnings and items of income and expense that, as required by Australian Accounting Standards, are recognised in other comprehensive income and presented separately in equity.

[Based on IFRS for SMEs Standard paragraph 4.11]

45

An entity with share capital shall disclose the following, either in the statement of financial position or in the notes:

(a) for each class of share capital:

(i) the number of shares authorised;

(ii) the number of shares issued and fully paid, and issued but not fully paid;

(iii) par value per share or that the shares have no par value;

(iv) a reconciliation of the number of shares outstanding at the beginning and at the end of the period. This reconciliation need not be presented for prior periods;

(v) the rights, preferences and restrictions attaching to that class including restrictions on the distribution of dividends and the repayment of capital;

(vi) shares in the entity held by the entity or by its subsidiaries or associates; and

(vii) shares reserved for issue under options and contracts for the sale of shares, including the terms and amounts; and

(b) a description of each reserve within equity.

[IFRS for SMEs Standard paragraph 4.12]

46

An entity without share capital, such as a partnership or trust, shall disclose information equivalent to that required by paragraph 45(a), showing changes during the period in each category of equity, and the rights, preferences and restrictions attaching to each category of equity. [IFRS for SMEs Standard paragraph 4.13]

47

If, at the reporting date, an entity has any assets classified as held for sale, or assets and liabilities that are included in a disposal group that is classified as held for sale, the entity shall disclose the following information:

(a) a description of the asset(s) or the group of assets and liabilities; and

(b) a description of the facts and circumstances of the sale, or leading to the expected disposal, and the expected manner and timing of that disposal.

[Based on IFRS for SMEs Standard paragraph 4.14]

47A

In applying paragraph 40, an entity might classify liabilities arising from loan arrangements as non‑current when the entity’s right to defer settlement of those liabilities is subject to the entity complying with covenants within twelve months after the reporting date. In such situations, the entity shall disclose information in the notes that enables users of financial statements to understand the risk that the liabilities could become repayable within twelve months after the reporting date, including:

(a) information about the covenants (including the nature of the covenants and when the entity is required to comply with them) and the carrying amount of related liabilities; and

(b) facts and circumstances, if any, that indicate the entity may have difficulty complying with the covenants - for example, the entity having acted during or after the reporting period to avoid or mitigate a potential breach. Such facts and circumstances could also include the fact that the entity would not have complied with the covenants if they were to be assessed for compliance based on the entity’s circumstances at the reporting date.

Statement of Profit or Loss and Other Comprehensive Income

Scope of this section

48

This section requires an entity to present its total comprehensive income for a period—ie its financial performance for the period—in one or two financial statements. It sets out the information that is to be presented in those statements or in the notes and how to present it. [Based on IFRS for SMEs Standard paragraph 5.1]

Corresponding AASB Standard: AASB 101 Presentation of Financial Statements.

Presentation of total comprehensive income

49

An entity shall present its total comprehensive income for a period either:

(a) in a single statement of profit or loss and other comprehensive income, in which case the statement of comprehensive income presents all items of income and expense recognised in the period; or

(b) in two statements—a statement of profit or loss and a statement of comprehensive income—in which case the statement of profit or loss presents all items of income and expense recognised in the period except those that are recognised in total comprehensive income outside of profit or loss as permitted or required by other Australian Accounting Standards.

[IFRS for SMEs Standard paragraph 5.2]

50

A change from the single-statement approach to the two-statement approach, or vice versa, is a change in accounting policy to which AASB 108 applies. [IFRS for SMEs Standard paragraph 5.3]

Single-statement approach

51

Under the single-statement approach, the statement of profit or loss and other comprehensive income shall include all items of income and expense recognised in a period unless other Australian Accounting Standards require otherwise. Australian Accounting Standards provide different treatment for the following circumstances:

(a) the effects of corrections of errors and changes in accounting policies are presented as retrospective adjustments of prior periods instead of as part of profit or loss in the period in which they arise (see AASB 108); and

(b) items of other comprehensive income are recognised as part of total comprehensive income, outside of profit or loss, when they arise.

[Based on IFRS for SMEs Standard paragraph 5.4]

52

As a minimum, an entity shall include, in the statement(s) presenting profit or loss and other comprehensive income, line items that present the following amounts for the period:

(a) revenue;

(b) finance costs;

(c) share of the profit or loss of investments in associates and joint ventures accounted for using the equity method (see AASB 128 Investments in Associates and Joint Ventures);

(d) tax expense;

(e) a single amount for the total of:

(i) discontinued operations (see AASB 5 Non-current Assets Held for Sale and Discontinued Operations); and

(ii) the post-tax gain or loss attributable to an impairment, or reversal of an impairment, of the assets in the discontinued operation (see AASB 5), both at the time and subsequent to being classified as a discontinued operation and to the disposal of the net assets constituting the discontinued operation;

(f) profit or loss (if an entity has no items of other comprehensive income, this line need not be presented);

(g) each item of other comprehensive income (see paragraph 51(b)) classified by nature (excluding amounts in (h)). Such items shall be grouped into those that, in accordance with other Australian Accounting Standards:

(i) will not be reclassified subsequently to profit or loss; and

(ii) will be reclassified subsequently to profit or loss when specific conditions are met;

(h) share of the other comprehensive income of associates and joint ventures accounted for by the equity method; and

(i) total comprehensive income (if an entity has no items of other comprehensive income, it may use another term for this line such as profit or loss).

[Based on IFRS for SMEs Standard paragraph 5.5]

53

An entity shall disclose separately the following items in the statement(s) presenting profit or loss and other comprehensive income as allocations for the period:

(a) profit or loss for the period attributable to:

(i) non-controlling interests; and

(ii) owners of the parent; and

(b) total comprehensive income for the period attributable to:

(i) non-controlling interests; and

(ii) owners of the parent.

[IFRS for SMEs Standard paragraph 5.6]

Two-statement approach

54

Under the two-statement approach, the statement of profit or loss shall display, as a minimum, line items that present the amounts in paragraph 52(a)–52(f) for the period, with profit or loss as the last line. The statement of comprehensive income shall begin with profit or loss as its first line and shall display, as a minimum, line items that present the amounts in paragraph 52(g)–52(i) and paragraph 53 for the period. [IFRS for SMEs Standard paragraph 5.7]

Requirements applicable to both approaches

55

Under AASB 108, the effects of corrections of errors and changes in accounting policies are presented as retrospective adjustments of prior periods instead of as part of profit or loss in the period in which they arise. [IFRS for SMEs Standard paragraph 5.8]

57

An entity shall not present or describe any items of income and expense as ‘extraordinary items’ in the statement(s) presenting profit or loss and other comprehensive income (or in the statement of profit or loss, if presented) or in the notes. [IFRS for SMEs Standard paragraph 5.10]

Analysis of expenses

58

An entity shall present in the statement of profit or loss and other comprehensive income or in the notes an analysis of expenses using a classification based on either the nature of expenses or the function of expenses within the entity, whichever provides information that is reliable and more relevant.

Analysis by nature of expense

(a) Under this method of classification, expenses are aggregated in the statement(s) of profit and loss and other comprehensive income according to their nature (for example, depreciation, purchases of materials, transport costs, employee benefits and advertising costs) and are not reallocated among various functions within the entity.

Analysis by function of expense

(b) Under this method of classification, expenses are aggregated according to their function as part of cost of sales or, for example, the costs of distribution or administrative activities. At a minimum, an entity discloses its cost of sales under this method separately from other expenses.

[Based on IFRS for SMEs Standard paragraph 5.11]

Statement of Changes in Equity and Statement of Income and Retained Earnings

Scope of this section

59

This section sets out requirements for presenting the changes in an entity’s equity for a period, either in a statement of changes in equity or, if specified conditions are met and an entity chooses, in a statement of income and retained earnings. [IFRS for SMEs Standard paragraph 6.1]

Corresponding AASB Standard: AASB 101 Presentation of Financial Statements.

Statement of changes in equity

Purpose

60

The statement of changes in equity presents an entity’s profit or loss for a reporting period, other comprehensive income for the period, the effects of changes in accounting policies and corrections of errors recognised in the period and the amounts of investments by, and dividends and other distributions to, owners in their capacity as owners during the period. [IFRS for SMEs Standard paragraph 6.2]

Information to be presented in the statement of changes in equity

61

The statement of changes in equity includes the following information:

(a) total comprehensive income for the period, showing separately the total amounts attributable to owners of the parent and to non-controlling interests;

(b) for each component of equity, the effects of retrospective application or retrospective restatement recognised in accordance with AASB 108; and

(c) for each component of equity, a reconciliation between the carrying amount at the beginning and the end of the period, separately disclosing changes resulting from:

(i) profit or loss;

(ii) other comprehensive income; and

(iii) the amounts of investments by, and dividends and other distributions to, owners in their capacity as owners, showing separately issues of shares, treasury share transactions, dividends and other distributions to owners and changes in ownership interests in subsidiaries that do not result in a loss of control.

[IFRS for SMEs Standard paragraph 6.3]

Statement of income and retained earnings

Purpose

62

The statement of income and retained earnings presents an entity’s profit or loss and changes in retained earnings for a reporting period. Paragraph 26 permits an entity to present a statement of income and retained earnings in place of a statement of comprehensive income and a statement of changes in equity if the only changes to its equity during the periods for which financial statements are presented arise from profit or loss, payment of dividends, corrections of prior period errors, and changes in accounting policy. [IFRS for SMEs Standard paragraph 6.4]

Information to be presented in the statement of income and retained earnings

63

An entity shall present, in the statement of income and retained earnings, the following items in addition to the information required by the section covering the Statement of Profit or Loss and Other Comprehensive Income:

(a) retained earnings at the beginning of the reporting period;

(b) dividends declared and paid or payable during the period;

(c) restatements of retained earnings for corrections of prior period errors;

(d) restatements of retained earnings for changes in accounting policy; and

(e) retained earnings at the end of the reporting period.

[IFRS for SMEs Standard paragraph 6.5]

Statement of Cash Flows

Scope of this section

64

This section sets out the information that is to be presented in a statement of cash flows and how to present it. The statement of cash flows provides information about the changes in cash and cash equivalents of an entity for a reporting period, showing separately changes from operating activities, investing activities and financing activities. [IFRS for SMEs Standard paragraph 7.1]

Corresponding AASB Standard: AASB 107 Statement of Cash Flows.

Cash equivalents

65

Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value. They are held to meet short-term cash commitments instead of for investment or other purposes. Consequently, an investment normally qualifies as a cash equivalent only when it has a short maturity of, say, three months or less from the date of acquisition. Bank overdrafts are normally considered financing activities similar to borrowings. However, if they are repayable on demand and form an integral part of an entity’s cash management, bank overdrafts are a component of cash and cash equivalents. [IFRS for SMEs Standard paragraph 7.2]

Information to be presented in the statement of cash flows

66

An entity shall present a statement of cash flows that presents cash flows for a reporting period classified by operating activities, investing activities and financing activities. [IFRS for SMEs Standard paragraph 7.3]

Operating activities

67

Operating activities are the principal revenue-producing activities of the entity. Consequently, cash flows from operating activities generally result from the transactions and other events and conditions that enter into the determination of profit or loss. Examples of cash flows from operating activities are:

(a) cash receipts from the sale of goods and the rendering of services;

(b) cash receipts from royalties, fees, commissions and other revenue;

(c) cash payments to suppliers for goods and services;

(d) cash payments to and on behalf of employees;

(e) cash payments or refunds of income tax, unless they can be specifically identified with financing and investing activities; and

(f) cash receipts and payments from investments, loans and other contracts held for dealing or trading purposes, which are similar to inventory acquired specifically for resale.

Some transactions, such as the sale of an item of plant by a manufacturing entity, may give rise to a gain or loss that is included in profit or loss. However, the cash flows relating to such transactions are cash flows from investing activities. [IFRS for SMEs Standard paragraph 7.4]

Investing activities

68

Investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. Examples of cash flows arising from investing activities are:

(a) cash payments to acquire property, plant and equipment (including self-constructed property, plant and equipment), intangible assets and other long-term assets;

(b) cash receipts from sales of property, plant and equipment, intangibles and other long-term assets;

(c) cash payments to acquire equity or debt instruments of other entities and interests in joint ventures (other than payments for those instruments classified as cash equivalents or held for dealing or trading);

(d) cash receipts from sales of equity or debt instruments of other entities and interests in joint ventures (other than receipts for those instruments classified as cash equivalents or held for dealing or trading);

(e) cash advances and loans made to other parties;

(f) cash receipts from the repayment of advances and loans made to other parties;

(g) cash payments for futures contracts, forward contracts, option contracts and swap contracts, except when the contracts are held for dealing or trading, or the payments are classified as financing activities; and

(h) cash receipts from futures contracts, forward contracts, option contracts and swap contracts, except when the contracts are held for dealing or trading, or the receipts are classified as financing activities.

When a contract is accounted for as a hedge (see AASB 9 Financial Instruments and AASB 139 Financial Instruments: Recognition and Measurement), an entity shall classify the cash flows of the contract in the same manner as the cash flows of the item being hedged. [IFRS for SMEs Standard paragraph 7.5]

Financing activities

69

Financing activities are activities that result in changes in the size and composition of the contributed equity and borrowings of an entity. Examples of cash flows arising from financing activities are:

(a) cash proceeds from issuing shares or other equity instruments;

(b) cash payments to owners to acquire or redeem the entity’s shares;

(c) cash proceeds from issuing debentures, loans, notes, bonds, mortgages and other short-term or long-term borrowings;

(d) cash repayments of amounts borrowed; and

(e) cash payments by a lessee for the reduction of the outstanding liability relating to a lease.

[IFRS for SMEs Standard paragraph 7.6]

Reporting cash flows from operating activities

70

An entity shall present cash flows from operating activities using either:

(a) the indirect method, whereby profit or loss is adjusted for the effects of non-cash transactions, any deferrals or accruals of past or future operating cash receipts or payments and items of income or expense associated with investing or financing cash flows; or

(b) the direct method, whereby major classes of gross cash receipts and gross cash payments are disclosed.

[IFRS for SMEs Standard paragraph 7.7]

Indirect method

71

Under the indirect method, the net cash flow from operating activities is determined by adjusting profit or loss for the effects of:

(a) changes during the period in inventories and operating receivables and payables;

(b) non-cash items such as depreciation, provisions, deferred tax, accrued income (expenses) not yet received (paid) in cash, unrealised foreign currency gains and losses, undistributed profits of associates and non-controlling interests; and

(c) all other items for which the cash effects relate to investing or financing.

[IFRS for SMEs Standard paragraph 7.8]

72

Alternatively, the net cash flow from operating activities may be presented under the indirect method by showing the revenues and expenses disclosed in the statement of comprehensive income and the changes during the period in inventories and operating receivables and payables.

Direct method

73

Under the direct method, net cash flow from operating activities is presented by disclosing information about major classes of gross cash receipts and gross cash payments. Such information may be obtained either:

(a) from the accounting records of the entity; or

(b) by adjusting sales, cost of sales and other items in the statement of comprehensive income (or the statement of profit or loss, if presented) for:

(i) changes during the period in inventories and operating receivables and payables;

(ii) other non-cash items; and

(iii) other items for which the cash effects are investing or financing cash flows.

[IFRS for SMEs Standard paragraph 7.9]

Reporting cash flows from investing and financing activities

74

An entity shall present separately major classes of gross cash receipts and gross cash payments arising from investing and financing activities. The aggregate cash flows arising from acquisitions and from disposals of subsidiaries or other business units shall be presented separately and classified as investing activities. [IFRS for SMEs Standard paragraph 7.10]

Reporting cash flows on a net basis

75

Cash flows arising from the following operating, investing or financing activities may be reported on a net basis:

(a) cash receipts and payments on behalf of customers when the cash flows reflect the activities of the customer rather than those of the entity; and

(b) cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are short.

76

Examples of cash receipts and payments referred to in paragraph 75(a) are:

(a) the acceptance and repayment of demand deposits of a bank;

(b) funds held for customers by an investment entity; and

(c) rents collected on behalf of, and paid over to, the owners of properties.

77

Examples of cash receipts and payments referred to in paragraph 75(b) are advances made for, and the repayment of:

(a) principal amounts relating to credit card customers;

(b) the purchase and sale of investments; and

(c) other short-term borrowings, for example, those which have a maturity period of three months or less.

78

Cash flows arising from each of the following activities of a financial institution may be reported on a net basis:

(a) cash receipts and payments for the acceptance and repayment of deposits with a fixed maturity date;

(b) the placement of deposits with and withdrawal of deposits from other financial institutions; and

(c) cash advances and loans made to customers and the repayment of those advances and loans.

Foreign currency cash flows

79

An entity shall record cash flows arising from transactions in a foreign currency in the entity’s functional currency by applying to the foreign currency amount the exchange rate between the functional currency and the foreign currency at the date of the cash flow. Paragraph 40 in AASB 121 explains when an exchange rate that approximates the actual rate can be used. [IFRS for SMEs Standard paragraph 7.11]

81

Unrealised gains and losses arising from changes in foreign currency exchange rates are not cash flows. However, to reconcile cash and cash equivalents at the beginning and the end of the period, the effect of exchange rate changes on cash and cash equivalents held or due in a foreign currency must be presented in the statement of cash flows. Consequently, the entity shall remeasure cash and cash equivalents held during the reporting period (such as amounts of foreign currency held and foreign currency bank accounts) at period-end exchange rates. The entity shall present the resulting unrealised gain or loss separately from cash flows from operating, investing and financing activities. [IFRS for SMEs Standard paragraph 7.13]

Interest and dividends

82

An entity shall present separately cash flows from interest and dividends received and paid. The entity shall classify cash flows consistently from period to period as operating, investing or financing activities. [IFRS for SMEs Standard paragraph 7.14]

83

An entity may classify interest paid and interest and dividends received as operating cash flows because they are included in profit or loss. Alternatively, the entity may classify interest paid and interest and dividends received as financing cash flows and investing cash flows respectively, because they are costs of obtaining financial resources or returns on investments. [IFRS for SMEs Standard paragraph 7.15]

Income tax

85

An entity shall present separately cash flows arising from income tax and shall classify them as cash flows from operating activities unless they can be specifically identified with financing and investing activities. When tax cash flows are allocated over more than one class of activity, the entity shall disclose the total amount of taxes paid. [IFRS for SMEs Standard paragraph 7.17]

Non-cash transactions

86

An entity shall exclude from the statement of cash flows investing and financing transactions that do not require the use of cash or cash equivalents. An entity shall disclose such transactions elsewhere in the financial statements in a way that provides all the relevant information about those investing and financing activities. [IFRS for SMEs Standard paragraph 7.18]

87

Many investing and financing activities do not have a direct impact on current cash flows even though they affect the capital and asset structure of an entity. The exclusion of non-cash transactions from the statement of cash flows is consistent with the objective of a statement of cash flows because these items do not involve cash flows in the current period. Examples of non-cash transactions are:

(a) the acquisition of assets either by assuming directly related liabilities or by means of a lease;

(b) the acquisition of an entity by means of an equity issue; and

(c) the conversion of debt to equity.

[IFRS for SMEs Standard paragraph 7.19]

Components of cash and cash equivalents

88

An entity shall present the components of cash and cash equivalents and shall present a reconciliation of the amounts presented in the statement of cash flows to the equivalent items presented in the statement of financial position. However, an entity is not required to present this reconciliation if the amount of cash and cash equivalents presented in the statement of cash flows is identical to the amount similarly described in the statement of financial position. [IFRS for SMEs Standard paragraph 7.20]

Other disclosures

89

An entity shall disclose, together with a commentary by management, the amount of significant cash and cash equivalent balances held by the entity that are not available for use by the entity. Cash and cash equivalents held by an entity may not be available for use by the entity because of, among other reasons, foreign exchange controls or legal restrictions. [IFRS for SMEs Standard paragraph 7.21]

Notes to the Financial Statements

Corresponding AASB Standard: AASB 101 Presentation of Financial Statements.

Structure of the notes

91

The notes shall:

(a) present information about the basis of preparation of the financial statements and the specific accounting policies used, in accordance with paragraphs 95–97;

(b) disclose the information required by this Standard that is not presented elsewhere in the financial statements; and

(c) provide information that is not presented elsewhere in the financial statements but is relevant to an understanding of any of them.

[IFRS for SMEs Standard paragraph 8.2]

92

An entity shall, as far as practicable, present the notes in a systematic manner. An entity shall cross-reference each item in the financial statements to any related information in the notes. [IFRS for SMEs Standard paragraph 8.3]

93

Examples of systematic ordering or grouping of the notes include:

(a) giving prominence to the areas of its activities that the entity considers to be most relevant to an understanding of its financial performance and financial position, such as grouping together information about particular operating activities;

(b) grouping together information about items measured similarly such as assets measured at fair value; or

(c) following the order of the line items in the statement(s) of profit or loss and other comprehensive income and the statement of financial position, such as:

(i) statement of compliance with Australian Accounting Standards – Simplified Disclosures (see paragraph 10);

(ii) material accounting policy information (see paragraph 95);

(iii) supporting information for items presented in the statements of financial position and in the statement(s) of profit or loss and other comprehensive income, and in the statements of changes in equity and of cash flows, in the order in which each statement and each line item is presented; and

(iv) other disclosures, including:

(1) contingent liabilities (see paragraph 154) and unrecognised contractual commitments; and

(2) non-financial disclosures.

[Based on IFRS for SMEs Standard paragraph 8.4]

94

An entity may present notes providing information about the basis of preparation of the financial statements and specific accounting policies as a separate section of the financial statements.

Disclosure of accounting policy information

95

An entity shall disclose material accounting policy information (see Appendix A). Accounting policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements.

[Based on IFRS for SMEs Standard paragraph 8.5]

Information about judgements

96

An entity shall disclose, in the material accounting policy information or other notes, the judgements, apart from those involving estimations (see paragraph 97), that management has made in the process of applying the entity’s accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

[Based on IFRS for SMEs Standard paragraph 8.6]

Information about key sources of estimation uncertainty

97

An entity shall disclose in the notes information about the key assumptions concerning the future, and other key sources of estimation uncertainty at the reporting date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year. In respect of those assets and liabilities, the notes shall include details of:

(a) their nature; and

(b) their carrying amount as at the end of the reporting period.

[IFRS for SMEs Standard paragraph 8.7]

Audit fees

98

An entity shall disclose fees to each auditor or reviewer, including any network firm, separately for:

(a) the audit or review of the financial statements; and

(b) all other services performed during the reporting period.

99

For paragraph 98, an entity shall describe the nature of other services.

Imputation credits

100

The term ‘imputation credits’ is used in paragraphs 101-103 to also mean ‘franking credits’. The disclosures required by paragraphs 101 and 103 shall be made separately in respect of any New Zealand imputation credits and any Australian imputation credits.

101

An entity shall disclose the amount of imputation credits available for use in subsequent reporting periods.

102

For the purposes of determining the amount required to be disclosed in accordance with paragraph 101, entities may have:

(a) imputation credits that will arise from the payment of the amount of the provision for income tax;

(b) imputation debits that will arise from the payment of dividends recognised as a liability at the reporting date; and

(c) imputation credits that will arise from the receipt of dividends recognised as receivables at the reporting date.

103

Where there are different classes of investors with different entitlements to imputation credits, disclosures shall be made about the nature of those entitlements for each class where this is relevant to an understanding of them.

Consolidated and Separate Financial Statements

Disclosures in consolidated financial statements

104

The following disclosures shall be made in consolidated financial statements:

(a) the fact that the statements are consolidated financial statements;

(b) the basis for concluding that control exists when the parent does not own, directly or indirectly through subsidiaries, more than half of the voting power;

(c) any difference in the reporting date of the financial statements of the parent and its subsidiaries used in the preparation of the consolidated financial statements; and

(d) the nature and extent of any significant restrictions (for example resulting from borrowing arrangements or regulatory requirements) on the ability of subsidiaries to transfer funds to the parent in the form of cash dividends or to repay loans.

[IFRS for SMEs Standard paragraph 9.23]

Disclosures in separate financial statements

105

When a parent, an investor in an associate or a venturer with an interest in a joint venture prepares separate financial statements, those separate financial statements shall disclose:

(a) that the statements are separate financial statements; and

(b) a description of the methods used to account for the investments in subsidiaries, joint ventures and associates,

and shall identify the consolidated financial statements or other primary financial statements to which they relate.

[IFRS for SMEs Standard paragraph 9.27]

Accounting Policies, Estimates and Errors

Disclosure of a change in accounting policy

106

Subject to paragraph 107, when initial application of an Australian Accounting Standard has an effect on the current period or any prior period, or might have an effect on future periods, an entity shall disclose the following:

(a) the nature of the change in accounting policy;

(b) for the current period and each prior period presented, to the extent practicable, the amount of the adjustment for each financial statement line item affected;

(c) the amount of the adjustment relating to periods before those presented, to the extent practicable; and

(d) an explanation if it is impracticable to determine the amounts to be disclosed in (b) or (c).

Financial statements of subsequent periods need not repeat these disclosures.

[Based on IFRS for SMEs Standard paragraph 10.13]

Corresponding AASB Standard: AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors.

107

Where an entity has selected a transition option under another Standard and there are specific transition disclosure requirements in that Standard, the entity shall apply the full transition disclosure requirements in that Standard instead of the requirements in paragraph 106.

107A

In the reporting period in which an entity first applies AASB 2020-8 Amendments to Australian Accounting Standards – Interest Rate Benchmark Reform – Phase 2, the entity is not required to disclose the information that would otherwise be required by paragraph 106(b) in respect of the accounting policy changes made in applying AASB 2020-8.

108

When a voluntary change in accounting policy has an effect on the current period or any prior period, an entity shall disclose the following:

(a) the nature of the change in accounting policy;

(b) the reasons why applying the new accounting policy provides reliable and more relevant information;

(c) to the extent practicable, the amount of the adjustment for each financial statement line item affected, shown separately:

(i) for the current period;

(ii) for each prior period presented; and

(iii) in the aggregate for periods before those presented; and

(d) an explanation if it is impracticable to determine the amounts to be disclosed in (c).

Financial statements of subsequent periods need not repeat these disclosures.

[IFRS for SMEs Standard paragraph 10.14]

Disclosure of a change in estimate

109

An entity shall disclose the nature of any change in an accounting estimate and the effect of the change on assets, liabilities, income and expense for the current period. If it is practicable for the entity to estimate the effect of the change in one or more future periods, the entity shall disclose those estimates. [IFRS for SMEs Standard paragraph 10.18]

Disclosure of prior period errors

110

An entity shall disclose the following about prior period errors:

(a) the nature of the prior period error;

(b) for each prior period presented, to the extent practicable, the amount of the correction for each financial statement line item affected;

(c) to the extent practicable, the amount of the correction at the beginning of the earliest prior period presented; and

(d) an explanation if it is not practicable to determine the amounts to be disclosed in (b) or (c).

Financial statements of subsequent periods need not repeat these disclosures.

[IFRS for SMEs Standard paragraph 10.23]

Basic Financial Instruments

111

The disclosures required in this Section apply to all financial instruments within the scope of AASB 9. In addition, if the entity uses hedge accounting, it shall make the additional disclosures in paragraphs 120–122.

Disclosure of accounting policies for financial instruments

112

In accordance with paragraph 95, an entity shall disclose material accounting policy information. Information about the measurement basis (or bases) for financial instruments used in preparing the financial statements is expected to be material accounting policy information.

[Based on IFRS for SMEs Standard paragraph 11.40]

Statement of financial position—categories of financial assets and financial liabilities

113

An entity shall disclose the carrying amounts of each of the following categories of financial assets and financial liabilities at the reporting date, in total, either in the statement of financial position or in the notes:

(a) financial assets measured at fair value through profit or loss;

(b) financial assets measured at amortised cost;

(c) financial liabilities measured at fair value through profit or loss;

(d) financial liabilities measured at amortised cost; and

(e) financial assets measured at fair value through other comprehensive income, showing separately:

(i) financial assets that are measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of AASB 9; and

(ii) investments in equity instruments designated as such upon initial recognition in accordance with paragraph 5.7.5 of AASB 9.

[Based on IFRS for SMEs Standard paragraph 11.41]

Derecognition

116

If an entity has transferred financial assets to another party in a transaction that does not qualify for derecognition (see paragraph 3.2.15 of AASB 9), the entity shall disclose the following for each class of such financial assets:

(a) the nature of the assets;

(b) the nature of the risks and rewards of ownership to which the entity remains exposed; and

(c) the carrying amounts of the assets and of any associated liabilities that the entity continues to recognise.

[IFRS for SMEs Standard paragraph 11.45]

Collateral

117

When an entity has pledged financial assets as collateral for liabilities or contingent liabilities, it shall disclose the following:

(a) the carrying amount of the financial assets pledged as collateral; and

(b) the terms and conditions relating to its pledge.

[IFRS for SMEs Standard paragraph 11.46]

Defaults and breaches on loans payable

118

For loans payable recognised at the reporting date for which there is a breach of terms or a default of principal, interest, sinking fund or redemption terms that have not been remedied by the reporting date, an entity shall disclose the following:

(a) details of that breach or default;

(b) the carrying amount of the related loans payable at the reporting date; and

(c) whether the breach or default was remedied, or the terms of the loans payable were renegotiated, before the financial statements were authorised for issue.

[IFRS for SMEs Standard paragraph 11.47]

Items of income, expense, gains or losses

119

An entity shall disclose the following items of income, expense, gains or losses:

(a) income, expense, gains or losses, including changes in fair value, recognised on:

(i) financial assets measured at fair value through profit or loss;

(ii) financial liabilities measured at fair value through profit or loss;

(iii) financial assets measured at amortised cost;

(iv) financial liabilities measured at amortised cost;

(v) investments in equity instruments designated at fair value through other comprehensive income in accordance with paragraph 5.7.5 of AASB 9; and

(vi) financial assets measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of AASB 9, showing separately the amount of gain or loss recognised in other comprehensive income during the period and the amount reclassified upon derecognition from accumulated other comprehensive income to profit or loss for the period;

(b) total interest income and total interest expense (calculated using the effective interest method) for financial assets or financial liabilities that are not measured at fair value through profit or loss; and

(c) the amount of any impairment loss for each class of financial asset.

[Based on IFRS for SMEs Standard paragraph 11.48]

Other Financial Instrument Issues – Hedging Disclosures

120

An entity shall disclose the following separately for each category of risk exposures that it decides to hedge and for which hedge accounting is applied:

(a) a description of the hedge;

(b) a description of the financial instruments designated as hedging instruments and their fair values at the reporting date; and

(c) the nature of the risks being hedged, including a description of the hedged item.

[Based on IFRS for SMEs Standard paragraph 12.27]

121

For fair value hedges, the entity shall disclose the following:

(a) the amount of the change in fair value of the hedging instrument recognised in profit or loss for the period; and

(b) the amount of the change in fair value of the hedged item recognised in profit or loss for the period.

[Based on IFRS for SMEs Standard paragraph 12.28]

122

For cash flow hedges and hedges of a net investment in a foreign operation, an entity shall disclose the following:

(a) the periods when the cash flows are expected to occur and when they are expected to affect profit or loss;

(b) a description of any forecast transaction for which hedge accounting had previously been used, but which is no longer expected to occur;

(c) the amount of the change in fair value of the hedging instrument that was recognised in other comprehensive income during the period;

(d) the amount that was reclassified to profit or loss for the period; and

(e) the amount of any excess of the cumulative change in fair value of the hedging instrument over the cumulative change in the fair value of the expected cash flows that was recognised in profit or loss for the period.

[Based on IFRS for SMEs Standard paragraph 12.29]

Inventories

123

An entity shall disclose the following:

(a) material accounting policy information about the measurement of inventories, including the cost formula used;

(b) the total carrying amount of inventories and the carrying amount in classifications appropriate to the entity;

(c) the amount of inventories recognised as an expense during the period;

(d) impairment losses recognised or reversed in profit or loss in accordance with AASB 102 Inventories; and

(e) the total carrying amount of inventories pledged as security for liabilities.

[Based on IFRS for SMEs Standard paragraph 13.22]

Corresponding AASB Standard: AASB 102 Inventories.

124

Not-for-profit entities shall disclose the basis on which any loss of service potential of inventories held for distribution is assessed, or the bases when more than one basis is used, in addition to the information required by paragraph 123.

Investments in Associates

125

An entity shall disclose the following:

(a) material accounting policy information for investments in associates;

(b) the carrying amount of investments in associates (see paragraph 35(i)); and

(c) the fair value of investments in associates accounted for using the equity method for which there are published price quotations.

[Based on IFRS for SMEs Standard paragraph 14.12]

127

For investments in associates accounted for by the equity method, an investor shall disclose separately its share of the profit or loss of such associates and its share of any discontinued operations of such associates. [IFRS for SMEs Standard paragraph 14.14]

128

For investments in associates accounted for in accordance with AASB 9, an investor shall make the disclosures required by paragraphs 113–115. [Based on IFRS for SMEs Standard paragraph 14.15]

Investments in Joint Ventures

129

An entity shall disclose the following:

(a) material accounting policy information for recognising its interests in joint ventures;

(b) the carrying amount of investments in joint ventures (see paragraph 35(j));

(c) the fair value of investments in joint ventures accounted for using the equity method for which there are published price quotations; and

(d) the aggregate amount of its commitments relating to joint ventures, including its share in the capital commitments that have been incurred jointly with other venturers, as well as its share of the capital commitments of the joint ventures themselves.

[Based on IFRS for SMEs Standard paragraph 15.19]

130

For joint ventures accounted for in accordance with the equity method, the venturer shall also make the disclosures required by paragraph 127 for equity method investments. [IFRS for SMEs Standard paragraph 15.20]

131

For joint ventures accounted for in accordance with AASB 9, the venturer shall make the disclosures required by paragraphs 113–115. [Based on IFRS for SMEs Standard paragraph 15.21]

Investment Property at Fair Value

132

An entity shall disclose the following for all investment property accounted for at fair value through profit or loss (paragraph 33 of AASB 140 Investment Property):

(a) the methods and significant assumptions applied in determining the fair value of investment property;

(b) the extent to which the fair value of investment property (as measured or disclosed in the financial statements) is based on a valuation by an independent valuer who holds a recognised and relevant professional qualification and has recent experience in the location and class of the investment property being valued. If there has been no such valuation, that fact shall be disclosed;

(c) the existence and amounts of restrictions on the realisability of investment property or the remittance of income and proceeds of disposal;

(d) contractual obligations to purchase, construct or develop investment property or for repairs, maintenance or enhancements; and

(e) a reconciliation between the carrying amounts of investment property at the beginning and end of the period, showing separately:

(i) additions, disclosing separately those additions resulting from acquisitions through business combinations;

(ii) net gains or losses from fair value adjustments;

(iii) transfers to and from investment property carried at cost less accumulated depreciation and impairment (see paragraph 57 of AASB 140);

(iv) transfers to and from inventories and owner-occupied property; and

(v) other changes.

This reconciliation need not be presented for prior periods. [IFRS for SMEs Standard paragraph 16.10]

Corresponding AASB Standard: AASB 140 Investment Property.

133

1n accordance with the section covering Leases, the owner of an investment property provides lessors’ disclosures about leases into which it has entered. A lessee that holds a right-of-use asset that is an investment property provides lessees’ disclosures as required by that section for any leases into which it has entered. [Based on IFRS for SMEs Standard paragraph 16.11]

Property, Plant and Equipment and Investment Property at Cost

134

An entity shall disclose the following for each class of property, plant and equipment determined in accordance with paragraph 44(a) and separately for investment property carried at cost less accumulated depreciation and impairment: