This Interpretation applies to all post-employment defined benefits and other long-term employee defined benefits.

Preamble

Pronouncement

Obtaining a copy of this Accounting Interpretation

This Interpretation is available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7637

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2015

This AASB Interpretation contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The Director of Finance and Administration, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

AASB Interpretation 14 AASB 119 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction is set out in paragraphs 1 – Aus29.1. Interpretations are listed in Australian Accounting Standard AASB 1048 Interpretation of Standards and AASB 1057 Application of Australian Accounting Standards sets out their application. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IFRIC 14

AASB Interpretation 14 AASB 119 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction incorporates Interpretation IFRIC 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction issued by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IFRIC 14) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB Interpretation 14 also comply with IFRIC 14.

Not-for-profit entities’ compliance with IFRIC 14 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IFRIC 14.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Background

1

Paragraph 64 of AASB 119 limits the measurement of a net defined benefit asset to the lower of the surplus in the defined benefit plan and the asset ceiling. Paragraph 8 of AASB 119 defines the asset ceiling as ‘the present value of any economic benefits available in the form of refunds from the plan or reductions in future contributions to the plan’. Questions have arisen about when refunds or reductions in future contributions should be regarded as available, particularly when a minimum funding requirement exists.

2

Minimum funding requirements exist in many countries to improve the security of the post-employment benefit promise made to members of an employee benefit plan. Such requirements normally stipulate a minimum amount or level of contributions that must be made to a plan over a given period. Therefore, a minimum funding requirement may limit the ability of the entity to reduce future contributions.

3

Further, the limit on the measurement of a defined benefit asset may cause a minimum funding requirement to be onerous. Normally, a requirement to make contributions to a plan would not affect the measurement of the defined benefit asset or liability. This is because the contributions, once paid, will become plan assets and so the additional net liability is nil. However, a minimum funding requirement may give rise to a liability if the required contributions will not be available to the entity once they have been paid.

3A

In November 2009 the International Accounting Standards Board amended IFRIC 14 to remove an unintended consequence arising from the treatment of prepayments of future contributions in some circumstances when there is a minimum funding requirement.

Issues

6

The issues addressed in this Interpretation are:

(a) when refunds or reductions in future contributions should be regarded as available in accordance with the definition of the asset ceiling in paragraph 8 of AASB 119.

(b) how a minimum funding requirement might affect the availability of reductions in future contributions.

(c) when a minimum funding requirement might give rise to a liability.

Consensus

Availability of a refund or reduction in future contributions

7

An entity shall determine the availability of a refund or a reduction in future contributions in accordance with the terms and conditions of the plan and any statutory requirements in the jurisdiction of the plan.

8

An economic benefit, in the form of a refund or a reduction in future contributions, is available if the entity can realise it at some point during the life of the plan or when the plan liabilities are settled. In particular, such an economic benefit may be available even if it is not realisable immediately at the end of the reporting period.

9

The economic benefit available does not depend on how the entity intends to use the surplus. An entity shall determine the maximum economic benefit that is available from refunds, reductions in future contributions or a combination of both. An entity shall not recognise economic benefits from a combination of refunds and reductions in future contributions based on assumptions that are mutually exclusive.

10

In accordance with AASB 101, the entity shall disclose information about the key sources of estimation uncertainty at the end of the reporting period that have a significant risk of causing a material adjustment to the carrying amount of the net asset or liability recognised in the statement of financial position. This might include disclosure of any restrictions on the current realisability of the surplus or disclosure of the basis used to determine the amount of the economic benefit available.

The economic benefit available as a refund

The right to a refund

11

A refund is available to an entity only if the entity has an unconditional right to a refund:

(a) during the life of the plan, without assuming that the plan liabilities must be settled in order to obtain the refund (eg in some jurisdictions, the entity may have a right to a refund during the life of the plan, irrespective of whether the plan liabilities are settled); or

(b) assuming the gradual settlement of the plan liabilities over time until all members have left the plan; or

(c) assuming the full settlement of the plan liabilities in a single event (ie as a plan wind-up).

An unconditional right to a refund can exist whatever the funding level of a plan at the end of the reporting period.

11

A refund is available to an entity only if the entity has an unconditional right to a refund:

(a) during the life of the plan, without assuming that the plan liabilities must be settled in order to obtain the refund (eg in some jurisdictions, the entity may have a right to a refund during the life of the plan, irrespective of whether the plan liabilities are settled); or

(b) assuming the gradual settlement of the plan liabilities over time until all members have left the plan; or

(c) assuming the full settlement of the plan liabilities in a single event (ie as a plan wind-up).

An unconditional right to a refund can exist whatever the funding level of a plan at the end of the reporting period.

12

If the entity’s right to a refund of a surplus depends on the occurrence or non-occurrence of one or more uncertain future events not wholly within its control, the entity does not have an unconditional right and shall not recognise an asset.

Measurement of the economic benefit

13

An entity shall measure the economic benefit available as a refund as the amount of the surplus at the end of the reporting period (being the fair value of the plan assets less the present value of the defined benefit obligation) that the entity has a right to receive as a refund, less any associated costs. For instance, if a refund would be subject to a tax other than income tax, an entity shall measure the amount of the refund net of the tax.

13

An entity shall measure the economic benefit available as a refund as the amount of the surplus at the end of the reporting period (being the fair value of the plan assets less the present value of the defined benefit obligation) that the entity has a right to receive as a refund, less any associated costs. For instance, if a refund would be subject to a tax other than income tax, an entity shall measure the amount of the refund net of the tax.

14

In measuring the amount of a refund available when the plan is wound up (paragraph 11(c)), an entity shall include the costs to the plan of settling the plan liabilities and making the refund. For example, an entity shall deduct professional fees if these are paid by the plan rather than the entity, and the costs of any insurance premiums that may be required to secure the liability on wind-up.

15

If the amount of a refund is determined as the full amount or a proportion of the surplus, rather than a fixed amount, an entity shall make no adjustment for the time value of money, even if the refund is realisable only at a future date.

The economic benefit available as a contribution reduction

16

If there is no minimum funding requirement for contributions relating to future service, the economic benefit available as a reduction in future contributions is the future service cost to the entity for each period over the shorter of the expected life of the plan and the expected life of the entity. The future service cost to the entity excludes amounts that will be borne by employees.

17

An entity shall determine the future service costs using assumptions consistent with those used to determine the defined benefit obligation and with the situation that exists at the end of the reporting period as determined by AASB 119. Therefore, an entity shall assume no change to the benefits to be provided by a plan in the future until the plan is amended and shall assume a stable workforce in the future unless the entity makes a reduction in the number of employees covered by the plan. In the latter case, the assumption about the future workforce shall include the reduction.

The effect of a minimum funding requirement on the economic benefit available as a reduction in future contributions

18

An entity shall analyse any minimum funding requirement at a given date into contributions that are required to cover (a) any existing shortfall for past service on the minimum funding basis and (b) future service.

19

Contributions to cover any existing shortfall on the minimum funding basis in respect of services already received do not affect future contributions for future service. They may give rise to a liability in accordance with paragraphs 23–26.

20

If there is a minimum funding requirement for contributions relating to future service, the economic benefit available as a reduction in future contributions is the sum of:

(a) any amount that reduces future minimum funding requirement contributions for future service because the entity made a prepayment (ie paid the amount before being required to do so); and

(b) the estimated future service cost in each period in accordance with paragraphs 16 and 17, less the estimated minimum funding requirement contributions that would be required for future service in those periods if there were no prepayment as described in (a).

21

An entity shall estimate the future minimum funding requirement contributions for future service taking into account the effect of any existing surplus determined using the minimum funding basis but excluding the prepayment described in paragraph 20(a). An entity shall use assumptions consistent with the minimum funding basis and, for any factors not specified by that basis, assumptions consistent with those used to determine the defined benefit obligation and with the situation that exists at the end of the reporting period as determined by AASB 119. The estimate shall include any changes expected as a result of the entity paying the minimum contributions when they are due. However, the estimate shall not include the effect of expected changes in the terms and conditions of the minimum funding basis that are not substantively enacted or contractually agreed at the end of the reporting period.

22

When an entity determines the amount described in paragraph 20(b), if the future minimum funding requirement contributions for future service exceed the future AASB 119 service cost in any given period, that excess reduces the amount of the economic benefit available as a reduction in future contributions. However, the amount described in paragraph 20(b) can never be less than zero.

When a minimum funding requirement may give rise to a liability

23

If an entity has an obligation under a minimum funding requirement to pay contributions to cover an existing shortfall on the minimum funding basis in respect of services already received, the entity shall determine whether the contributions payable will be available as a refund or reduction in future contributions after they are paid into the plan.

24

To the extent that the contributions payable will not be available after they are paid into the plan, the entity shall recognise a liability when the obligation arises. The liability shall reduce the net defined benefit asset or increase the net defined benefit liability so that no gain or loss is expected to result from applying paragraph 64 of AASB 119 when the contributions are paid.

25–26

[Deleted]

Effective date

27

An entity shall apply this Interpretation for annual periods beginning on or after 1 January 2016. Earlier application is permitted for periods beginning on or after 1 January 2014 but before 1 January 2016. If an entity applies this Interpretation for a period beginning before 1 January 2016, it shall disclose that fact.

27A–27C

[Deleted by the AASB]

Transition

28

An entity shall apply this Interpretation from the beginning of the first period presented in the first financial statements to which the Interpretation applies. An entity shall recognise any initial adjustment arising from the application of this Interpretation in retained earnings at the beginning of that period.

Aus28.1

Paragraph 28 and the first sentence of paragraph 29 shall not be applied by an entity that has previously applied Interpretation 14, unless required to do so by a Standard or another Interpretation.

29

An entity shall apply the amendments in paragraphs 3A, 16–18 and 20–22 in the previous version of this Interpretation from the beginning of the earliest comparative period presented in the first financial statements in which the entity applies this Interpretation. If the entity had previously applied this Interpretation before it applies the amendments, it shall recognise the adjustment resulting from the application of the amendments in retained earnings at the beginning of the earliest comparative period presented.

Illustrative examples

These examples accompany, but are not part of, AASB Interpretation 14.

Example 1—Effect of the minimum funding requirement when there is an AASB 119 surplus and the minimum funding contributions payable are fully refundable to the entity

IE1

An entity has a funding level on the minimum funding requirement basis (which is measured on a different basis from that required under AASB 119) of 82 per cent in Plan A. Under the minimum funding requirements, the entity is required to increase the funding level to 95 per cent immediately. As a result, the entity has a statutory obligation at the end of the reporting period to contribute 200 to Plan A immediately. The plan rules permit a full refund of any surplus to the entity at the end of the life of the plan. The year-end valuations for Plan A are set out below.

|

Fair value of assets |

1,200 |

|

|

Present value of defined benefit obligation under AASB 119 |

(1,100) |

|

|

Surplus |

100 |

|

|

|

|

|

Application of requirements

IE2

Paragraph 24 of Interpretation 14 requires the entity to recognise a liability to the extent that the contributions payable are not fully available. Payment of the contributions of 200 will increase the AASB 119 surplus from 100 to 300. Under the rules of the plan this amount will be fully refundable to the entity with no associated costs. Therefore, no liability is recognised for the obligation to pay the contributions and the net defined benefit asset is 100.

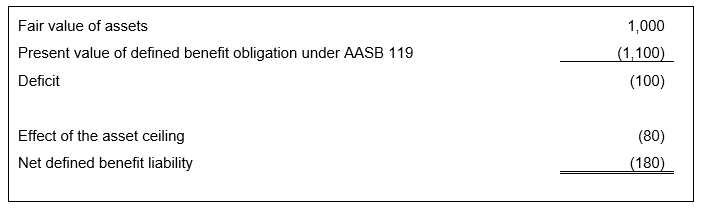

Example 2—Effect of a minimum funding requirement when there is an AASB 119 deficit and the minimum funding contributions payable would not be fully available

IE3

An entity has a funding level on the minimum funding requirement basis (which is measured on a different basis from that required under AASB 119) of 77 per cent in Plan B. Under the minimum funding requirements, the entity is required to increase the funding level to 100 per cent immediately. As a result, the entity has a statutory obligation at the end of the reporting period to pay additional contributions of 300 to Plan B. The plan rules permit a maximum refund of 60 per cent of the AASB 119 surplus to the entity and the entity is not permitted to reduce its contributions below a specified level which happens to equal the AASB 119 service cost. The year-end valuations for Plan B are set out below.

|

Fair value of assets |

1,000 |

|

|

Present value of defined benefit obligation under AASB 119 |

(1,100) |

|

|

Deficit |

(100) |

|

|

|

|

|

Application of requirements

IE4

The payment of 300 would change the AASB 119 deficit of 100 to a surplus of 200. Of this 200, 60 per cent (120) is refundable.

IE5

Therefore, of the contributions of 300, 100 eliminates the AASB 119 deficit and 120 (60 per cent of 200) is available as an economic benefit. The remaining 80 (40 per cent of 200) of the contributions paid is not available to the entity.

IE6

Paragraph 24 of Interpretation 14 requires the entity to recognise a liability to the extent that the additional contributions payable are not available to it.

IE7

Therefore, the net defined benefit liability is 180, comprising the deficit of 100 plus the additional liability of 80 resulting from the requirements in paragraph 24 of Interpretation 14. No other liability is recognised in respect of the statutory obligation to pay contributions of 300.

Summary

IE8

When the contributions of 300 are paid, the net defined benefit asset will be 120.

Example 3—Effect of a minimum funding requirement when the contributions payable would not be fully available and the effect on the economic benefit available as a future contribution reduction

IE9

An entity has a funding level on the minimum funding basis (which it measures on a different basis from that required by AASB 119) of 95 per cent in Plan C. The minimum funding requirements require the entity to pay contributions to increase the funding level to 100 per cent over the next three years. The contributions are required to make good the deficit on the minimum funding basis (shortfall) and to cover future service.

IE10

Plan C also has an AASB 119 surplus at the end of the reporting period of 50, which cannot be refunded to the entity under any circumstances.

IE11

The nominal amounts of contributions required to satisfy the minimum funding requirements in respect of the shortfall and the future service for the next three years are set out below.

|

Year |

Total contributions for minimum funding requirement |

Contributions required to make good the shortfall |

Contributions required to cover future service |

|

1 |

135 |

120 |

15 |

|

2 |

125 |

112 |

13 |

|

3 |

115 |

104 |

11 |

Application of requirements

IE12

The entity’s present obligation in respect of services already received includes the contributions required to make good the shortfall but does not include the contributions required to cover future service.

IE13

The present value of the entity’s obligation, assuming a discount rate of 6 per cent per year, is approximately 300, calculated as follows:

[120/(1.06) + 112/(1.06)2 + 104/(1.06)3]

IE14

When these contributions are paid into the plan, the AASB 119 surplus (ie the fair value of assets less the present value of the defined benefit obligation) would, other things being equal, increase from 50 to 350 (300 + 50).

IE15

However, the surplus is not refundable although an asset may be available as a future contribution reduction.

IE16

In accordance with paragraph 20 of Interpretation 14, the economic benefit available as a reduction in future contributions is the sum of:

(a) any amount that reduces future minimum funding requirement contributions for future service because the entity made a prepayment (ie paid the amount before being required to do so); and

(b) the estimated future service cost in each period in accordance with paragraphs 16 and 17, less the estimated minimum funding requirement contributions that would be required for future service in those periods if there were no prepayment as described in (a).

IE17

In this example there is no prepayment as described in paragraph 20(a). The amounts available as a reduction in future contributions when applying paragraph 20(b) are set out below.

|

Year |

AASB 119 service cost |

Minimum contributions required to cover future service |

Amount available as contribution reduction |

|

1 |

13 |

15 |

(2) |

|

2 |

13 |

13 |

0 |

|

3 |

13 |

11 |

2 |

|

4+ |

13 |

9 |

4 |

IE18

Assuming a discount rate of 6 per cent, the present value of the economic benefit available as a future contribution reduction is therefore equal to:

(2)/(1.06) + 0/(1.06)2 + 2/(1.06)3 + 4/(1.06)4 ... = 56

Thus in accordance with paragraph 58(b) of AASB 119, the present value of the economic benefit available from future contribution reductions is limited to 56.

IE19

Paragraph 24 of Interpretation 14 requires the entity to recognise a liability to the extent that the additional contributions payable will not be fully available. Therefore, the effect of the asset ceiling is 294 (50 + 300 – 56).

IE20

The entity recognises a net defined benefit liability of 244 in the statement of financial position. No other liability is recognised in respect of the obligation to make contributions to fund the minimum funding shortfall.

Summary

|

Surplus |

50 |

|

|

|

|

|

|

Net defined benefit asset (before consideration of the minimum funding requirement) |

50 |

|

|

|

|

|

|

Effect of the asset ceiling |

(294) |

|

|

|

|

|

|

Net defined benefit liability |

(244) |

|

|

|

|

|

IE21

When the contributions of 300 are paid into the plan, the net defined benefit asset will become 56 (300 – 244).

Example 4—Effect of a prepayment when a minimum funding requirement exceeds the expected future service charge

IE22

An entity is required to fund Plan D so that no deficit arises on the minimum funding basis. The entity is required to pay minimum funding requirement contributions to cover the service cost in each period determined on the minimum funding basis.

IE23

Plan D has an AASB 119 surplus of 35 at the beginning of 20X1. This example assumes that the discount rate and expected return on assets are 0 per cent, and that the plan cannot refund the surplus to the entity under any circumstances but can use the surplus for reductions of future contributions.

IE24

The minimum contributions required to cover future service are 15 for each of the next five years. The expected AASB 119 service cost is 10 in each year.

IE25

The entity makes a prepayment of 30 at the beginning of 20X1 in respect of years 20X1 and 20X2, increasing its surplus at the beginning of 20X1 to 65. That prepayment reduces the future contributions it expects to make in the following two years, as follows:

|

Year |

AASB 119 service cost |

Minimum funding requirement contribution before prepayment |

Minimum funding requirement contribution after prepayment |

|

20X1 |

10 |

15 |

0 |

|

20X2 |

10 |

15 |

0 |

|

20X3 |

10 |

15 |

15 |

|

20X4 |

10 |

15 |

15 |

|

20X5 |

10 |

15 |

15 |

|

Total |

50 |

75 |

45 |

Application of requirements

IE26

In accordance with paragraphs 20 and 22 of Interpretation 14, at the beginning of 20X1, the economic benefit available as a reduction in future contributions is the sum of:

(a) 30, being the prepayment of the minimum funding requirement contributions; and

(b) nil. The estimated minimum funding requirement contributions required for future service would be 75 if there was no prepayment. Those contributions exceed the estimated future service cost (50); therefore the entity cannot use any part of the surplus of 35 noted in paragraph IE23 (see paragraph 22).

IE27

Assuming a discount rate of 0 per cent, the present value of the economic benefit available as a reduction in future contributions is equal to 30. Thus in accordance with paragraph 64 of AASB 119 the entity recognises a net defined benefit asset of 30 (because this is lower than the AASB 119 surplus of 65).

Basis for Conclusions on IFRIC 14

IFRIC 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction

This Basis for Conclusions accompanies, but is not part of, AASB Interpretation 14. An IFRIC Basis for Conclusions may be amended to reflect any additional requirements in the AASB Interpretation or AASB Accounting Standards.

The original text has been marked up to reflect the revision of IAS 1 Presentation of Financial Statements in 2007: new text is underlined and deleted text is struck through.

BC1

This Basis for Conclusions summarises the IFRIC’s considerations in reaching its consensus. Individual IFRIC members gave greater weight to some factors than to others.

BC2

The IFRIC noted that practice varies significantly with regard to the treatment of the effect of a minimum funding requirement on the limit placed by paragraph 64 of IAS 19 Employee Benefits on the amount of a defined benefit asset. The IFRIC therefore decided to include this issue on its agenda. In considering the issue, the IFRIC also became aware of the need for general guidance on determining the limit on the measurement of the defined benefit asset, and for guidance on when that limit makes a minimum funding requirement onerous.

BC3

The IFRIC published D19 IAS 19—The Asset Ceiling: Availability of Economic Benefits and Minimum Funding Requirements in August 2006. In response, the IFRIC received 48 comment letters.

BC3A

In November 2009 the International Accounting Standards Board amended IFRIC 14 to remove an unintended consequence arising from the treatment of prepayments in some circumstances when there is a minimum funding requirement (see paragraphs BC30A–BC30D).

Definition of a minimum funding requirement

BC4

D19 referred to statutory or contractual minimum funding requirements. Respondents to D19 asked for further guidance on what constituted a minimum funding requirement. The IFRIC decided to clarify that for the purpose of the Interpretation a minimum funding requirement is any requirement for the entity to make contributions to fund a post-employment or other long-term defined benefit plan.

Interaction between IAS 19 and minimum funding requirements

BC5

Funding requirements would not normally affect the accounting for a plan under IAS 19. However, paragraph 64 of IAS 19 limits the amount of the net defined benefit asset to the available economic benefit. The interaction of a minimum funding requirement and this limit has two possible effects:

(a) the minimum funding requirement may restrict the economic benefits available as a reduction in future contributions, and

(b) the limit may make the minimum funding requirement onerous because contributions payable under the requirement in respect of services already received may not be available once they have been paid, either as a refund or as a reduction in future contributions.

BC6

These effects raised general questions about the availability of economic benefits in the form of a refund or a reduction in future contributions.

Availability of the economic benefit

BC7

One view of ‘available’ would limit the economic benefit to the amount that is realisable immediately at the end of the reporting period balance sheet date.

BC8

The IFRIC disagreed with this view. The Framework[1] defines an asset as a resource ‘from which future economic benefits are expected to flow to the entity’. Therefore, it is not necessary for the economic benefit to be realisable immediately. Indeed, a reduction in future contributions cannot be realisable immediately.

The reference to the Framework is to IASC’s Framework for the Preparation and Presentation of Financial Statements, adopted by the IASB in 2001. In September 2010 the IASB replaced the Framework with the Conceptual Framework for Financial Reporting.

BC9

The IFRIC concluded that a refund or reduction in future contributions is available if it could be realisable at some point during the life of the plan or when the plan liability is settled. Respondents to D19 were largely supportive of this conclusion.

BC10

In the responses to D19, some argued that an entity may expect to use the surplus to give improved benefits. Others noted that future actuarial losses might reduce or eliminate the surplus. In either case there would be no refund or reduction in future contributions. The IFRIC noted that the existence of an asset at the end of the reporting period balance sheet date depends on whether the entity has the right to obtain a refund or reduction in future contributions. The existence of the asset at that date is not affected by possible future changes to the amount of the surplus. If future events occur that change the amount of the surplus, their effects are recognised when they occur. Accordingly, if the entity decides to improve benefits, or future losses in the plan reduce the surplus, the consequences are recognised when the decision is made or the losses occur. The IFRIC noted that such events of future periods do not affect the existence or measurement of the asset at the end of the reporting period balance sheet date.

The asset available as a refund of a surplus

BC11

The IFRIC noted that a refund of a surplus could potentially be obtained in three ways:

(a) during the life of the plan, without assuming that the plan liabilities have to be settled in order to get the refund (eg in some jurisdictions, the entity may have a right to a refund during the life of the plan, irrespective of whether the plan liabilities are settled); or

(b) assuming the gradual settlement of the plan liabilities over time until all members have left the plan; or

(c) assuming the full settlement of the plan liabilities in a single event (ie as a plan wind-up).

BC12

The IFRIC concluded that all three ways should be considered in determining whether an economic benefit was available to the entity. Some respondents to D19 raised the question of when an entity controls an asset that arises from the availability of a refund, in particular if a refund would be available only if a third party (for example the plan trustees) gave its approval. The IFRIC concluded that an entity controlled the asset only if the entity has an unconditional right to the refund. If that right depends on actions by a third party, the entity does not have an unconditional right.

BC13

If the plan liability is settled by an immediate wind-up, the costs associated with the wind-up may be significant. One reason for this may be that the cost of annuities available on the market is expected to be significantly higher than that implied by the IAS 19 basis. Other costs include the legal and other professional fees expected to be incurred during the winding-up process. Accordingly, a plan with an apparent surplus may not be able to recover any of that surplus on wind-up.

BC14

The IFRIC noted that the available surplus should be measured at the amount that the entity could receive from the plan. The IFRIC decided that in determining the amount of the refund available on wind-up of the plan, the amount of the costs associated with the settlement and refund should be deducted if paid by the plan.

BC15

The IFRIC noted that the costs of settling the plan liability would be dependent on the facts and circumstances of the plan and it decided not to issue any specific guidance in this respect.

BC16

The IFRIC also noted that the present value of the defined benefit obligation and the fair value of assets are both measured on a present value basis[2] and therefore take into account the timing of the future cash flows. The IFRIC concluded that no further adjustment for the time value of money needs to be made when measuring the amount of a refund determined as the full amount or a proportion of the surplus that is realisable at a future date.

IFRS 13 Fair Value Measurement, issued in May 2011, defines fair value and contains the requirements for measuring fair value. IFRS 13 does not specify a particular valuation technique for measuring the fair value of plan assets.

The asset available in the form of a future contribution reduction

BC17

The IFRIC decided that the amount of the contribution reduction available to the entity should be measured with reference to the amount that the entity would have been required to pay had there been no surplus. The IFRIC concluded that is represented by the cost to the entity of accruing benefits in the plan, in other words by the future IAS 19 service cost. Respondents to D19 broadly supported this conclusion.

BC18

When the issue of the availability of reductions in future contributions was first raised with the IFRIC, some expressed the view that an entity should recognise an asset only to the extent that there was a formal agreement between the trustees and the entity specifying contributions payable lower than the IAS 19 service cost. The IFRIC disagreed, concluding instead that an entity is entitled to assume that, in general, it will not be required to make contributions to a plan in order to maintain a surplus and hence that it will be able to reduce contributions if the plan has a surplus. (The effects of a minimum funding requirement on this assumption are discussed below.)

BC19

The IFRIC considered the assumptions that underlie the calculation of the future service cost. In respect of the discount rate, IAS 19 requires the measurement of the present value of the future contribution reduction to be based on the same discount rate as that used to determine the present value of the defined benefit obligation.

BC20

The IFRIC considered whether the term over which the contribution reduction should be calculated should be restricted to the expected future working lifetime of the active membership. The IFRIC disagreed with that view. The IFRIC noted that the entity could derive economic benefit from a reduction in contributions beyond that period. The IFRIC also noted that increasing the term of the calculation has a decreasing effect on the incremental changes to the asset because the reductions in contributions are discounted to a present value. Thus, for plans with a large surplus and no possibility of receiving a refund, the available asset will be limited even if the term of the calculation extends beyond the expected future working lifetime of the active membership to the expected life of the plan. This is consistent with paragraph BC77 of the Basis for Conclusions on IAS 19[3], which states that ‘the limit [on the measurement of the defined benefit asset] is likely to come into play only where … the plan is very mature and has a very large surplus that is more than large enough to eliminate all future contributions and cannot be returned to the entity’ (emphasis added). If the contribution reduction were determined by considering only the term of the expected future working lifetime of the active membership, the limit on the measurement of the defined benefit asset would come into play much more frequently.

As a result of the amendments to IAS 19 in June 2011, paragraph BC77 was deleted.

BC21

Most respondents to D19 were supportive of this view. However, some argued that the term should be the shorter of the expected life of the plan and the expected life of the entity. The IFRIC agreed that the entity could not derive economic benefits from a reduction in contributions beyond its own expected life and has amended the Interpretation accordingly.

BC22

Next, the IFRIC considered what assumptions should be made about a future workforce. D19 proposed that the assumptions for the demographic profile of the future workforce should be consistent with the assumptions underlying the calculation of the present value of the defined benefit obligation at the end of the reporting period balance sheet date. Some respondents noted that the calculation of service costs for future periods requires assumptions that are not required for the calculation of the defined benefit obligation. In particular, the assumptions underlying the present value of the defined benefit obligation calculation do not include an explicit assumption for new entrants.

BC23

The IFRIC agreed that this is the case. The IFRIC noted that assumptions are needed in respect of the size of the future workforce and future benefits provided by the plan. The IFRIC decided that the future service cost should be based on the situation that exists at the end of the reporting period balance sheet date determined in accordance with IAS 19. Therefore, increases in the size of the workforce or the benefits provided by the plan should not be anticipated. Decreases in the size of the workforce or the benefits should be included in the assumptions for the future service cost at the same time as they are treated as curtailments in accordance with IAS 19.

The effect of a minimum funding requirement on the economic benefit available as a refund

BC24

The IFRIC considered whether a minimum funding requirement to make contributions to a plan in force at the end of the reporting period balance sheet date would restrict the extent to which a refund of surplus is available. The IFRIC noted that there is an implicit assumption in IAS 19 that the specified assumptions represent the best estimate of the eventual outcome of the plan in economic terms, while a requirement to make additional contributions is often a prudent approach designed to build in a risk margin for adverse circumstances. Moreover, when there are no members left in the plan, the minimum funding requirement would have no effect. This would leave the IAS 19 surplus available. To the extent that the entity has a right to this eventual surplus, the IAS 19 surplus would be available to the entity, regardless of the minimum funding restrictions in force at the end of the reporting period balance sheet date. The IFRIC therefore concluded that the existence of a minimum funding requirement may affect the timing of a refund but does not affect whether it is ultimately available to the entity.

The effect of a minimum funding requirement on the economic benefit available as a reduction in future contributions

BC25

The entity’s minimum funding requirements at a given date can be analysed into the contributions that are required to cover (a) an existing shortfall for past service on the minimum funding basis and (b) future service.

BC26

Contributions required to cover an existing shortfall may give rise to a liability, as discussed in paragraphs BC31–BC37 below. But they do not affect the availability of a reduction in future contributions for future service.

BC27

In contrast, future contribution requirements in respect of future service do not generate an additional liability at the end of the reporting period balance sheet date because they do not relate to past services received by the entity. However, they may reduce the extent to which the entity can benefit from a reduction in future contributions. Therefore, the IFRIC decided that the available asset from a contribution reduction should be calculated as the present value of the IAS 19 future service cost less the minimum funding contribution requirement in respect of future service in each year.

BC28

If the minimum funding contribution requirement is consistently greater than the IAS 19 future service cost, that calculation may be thought to imply that a liability exists. However, as noted above, an entity has no liability at the end of the reporting period balance sheet date in respect of minimum funding requirements that relate to future service. The economic benefit available from a reduction in future contributions can be nil, but it can never be a negative amount.

BC29

The respondents to D19 were largely supportive of these conclusions.

BC30

The IFRIC noted that future changes to regulations on minimum funding requirements might affect the available surplus. However, the IFRIC decided that, just as the future service cost was determined on the basis of the situation existing at the end of the reporting period balance sheet date, so should the effect of a minimum funding requirement. The IFRIC concluded that when determining the amount of an asset that might be available as a reduction in future contributions, an entity should not consider whether the minimum funding requirement might change in the future. The respondents to D19 were largely supportive of these conclusions.

Prepayments of a minimum funding requirement

BC30A

If an entity has prepaid future minimum funding requirement contributions and that prepayment will reduce future contributions, the prepayment generates economic benefits for the entity. However, to the extent that the future minimum funding requirement contributions exceeded future service costs, the original version of IFRIC 14 did not permit entities to consider those economic benefits in measuring a defined benefit asset. After issuing IFRIC 14, the Board reviewed the treatment of such prepayments. The Board concluded that such a prepayment provides an economic benefit to the entity by relieving the entity of an obligation to pay future minimum funding requirement contributions that exceed future service cost. Therefore, considering those economic benefits in measuring a defined benefit asset would convey more useful information to users of financial statements. In May 2009 the Board published that conclusion in an exposure draft Prepayments of a Minimum Funding Requirement. After considering the responses to that exposure draft, the Board amended IFRIC 14 by issuing Prepayments of a Minimum Funding Requirement in November 2009.

BC30B

Some respondents noted that the amendments increase the effect of funding considerations on the measurement of a defined benefit asset and liability and questioned whether funding considerations should ever affect the measurement. However, the Board noted that the sole purpose of the amendments was to eliminate an unintended consequence in IFRIC 14. Thus, the Board did not re-debate the fundamental conclusion of IFRIC 14 that funding is relevant to the measurement when an entity cannot recover the additional cost of a minimum funding requirement in excess of the IAS 19 service cost.

BC30C

Many respondents noted that the proposals made the assessment of the economic benefit available from a prepayment different from the assessment for a surplus arising from actuarial gains. Most agreed that a prepayment created an asset, but questioned why the Board did not extend the underlying principle to other surpluses that could be used to reduce future payments of minimum funding requirement contributions.

BC30D

The Board did not extend the scope of the amendments to surpluses arising from actuarial gains because such an approach would need further thought and the Board did not want to delay the amendments for prepayments. However, the Board may consider the matter further in a future comprehensive review of pension cost accounting.

Onerous minimum funding requirements

BC31

Minimum funding requirements for contributions to cover an existing minimum funding shortfall create an obligation for the entity at the end of the reporting period balance sheet date because they relate to past service. Nonetheless, usually minimum funding requirements do not affect the measurement of the defined benefit asset or liability under IAS 19. This is because the contributions, once paid, become plan assets and the additional net liability for the funding requirement is nil. However, the IFRIC noted that the limit on the measurement of the defined benefit asset in paragraph 64 of IAS 19 may make the funding obligation onerous, as follows.

BC32

If an entity is obliged to make contributions and some or all of those contributions will not subsequently be available as an economic benefit, it follows that when the contributions are made the entity will not be able to recognise an asset to that extent. However, the resulting loss to the entity does not arise on the payment of the contributions but earlier, at the point at which the obligation to pay arises.

BC33

Therefore, the IFRIC concluded that when an entity has an obligation under a minimum funding requirement to make additional contributions to a plan in respect of services already received, the entity should reduce the balance sheet asset or increase the liability recognised in the statement of financial position to the extent that the minimum funding contributions payable to the plan will not be available to the entity either as a refund or a reduction in future contributions.

BC34

Respondents to D19 broadly supported this conclusion. But some questioned whether the draft Interpretation extended the application of paragraph 64 of IAS 19 too far. They argued that it should apply only when an entity has a defined benefit asset. In particular, it should not be used to classify a funding requirement as onerous, thereby creating an additional liability to be recognised beyond that arising from the other requirements of IAS 19. Others agreed that such a liability existed, but questioned whether it fell within the scope of IAS 19 rather than IAS 37 Provisions, Contingent Liabilities and Contingent Assets.

BC35

The IFRIC did not agree that the Interpretation extends the application of paragraph 64 of IAS 19. Rather, it applies the principles in IAS 37 relating to onerous contracts in the context of the requirements of IAS 19, including paragraph 64. On the question whether the liability falls within the scope of IAS 19 or IAS 37, the IFRIC noted that employee benefits are excluded from the scope of IAS 37. The IFRIC therefore confirmed that the interaction of a minimum funding requirement and the limit on the measurement of the defined benefit asset could result in a decrease in a defined benefit asset or an increase in a defined benefit liability.

BC36–BC37

[Deleted]

Transitional provisions

BC38

In D19, the IFRIC proposed that the draft Interpretation should be applied retrospectively. The draft Interpretation required immediate recognition of all adjustments relating to the minimum funding requirements. The IFRIC therefore argued that retrospective application would be straightforward.

BC39

Respondents to D19 noted that paragraph 58A[4] of IAS 19 causes the limit on the defined benefit asset to affect the deferred recognition of actuarial gains and losses. Retrospective application of the Interpretation could change the amount of that limit for previous periods, thereby also changing the deferred recognition of actuarial gains and losses. Calculating these revised amounts retrospectively over the life of the plan would be costly and of little benefit to users of financial statements.

IAS 19 (as amended in June 2011) eliminated deferred recognition of actuarial gains and losses and deleted paragraph 58A.

BC40

The IFRIC agreed with this view. The IFRIC therefore amended the transitional provisions so that IFRIC 14 is to be applied only from the beginning of the first period presented in the financial statements for annual periods beginning on or after the effective date.

Summary of changes from D19

BC41

The Interpretation has been altered in the following significant respects since it was exposed for comment as D19:

(a) The issue of when an entity controls an asset arising from the availability of a refund has been clarified (paragraphs BC10 and BC12).

(b) Requirements relating to the assumptions underlying the measurement of a reduction in future contributions have been clarified (paragraphs BC22 and BC23).

(c) The transitional requirements have been changed from retrospective application to application from the beginning of the first period presented in the first financial statements to which the Interpretation applies (paragraphs BC38–BC40).

(d) In November 2009 the Board amended IFRIC 14 to require entities to recognise as an economic benefit any prepayment of minimum funding requirement contributions. At the same time, the Board removed references to ‘present value’ from paragraphs 16, 17, 20 and 22 and ‘the surplus in the plan’ from paragraph 16 because these references duplicated references in paragraph 64 of IAS 19. The Board also amended the term ‘future accrual of benefits’ to ‘future service’ for consistency with the rest of IAS 19.

(e) In June 2011 the Board issued an amended IAS 19 that eliminated the deferred recognition of actuarial gains and losses. As a consequence of that amendment, the Board deleted paragraphs 25 and 26, amended paragraphs 1, 6, 17, 24 and amended Examples 1–4 in the illustrative examples accompanying IFRIC 14. As a result of those changes paragraphs BC36 and BC37 of this Basis for Conclusions were deleted and paragraph BC5 was amended. Lastly, cross-references to IAS 19 were updated.

Deleted IFRIC 14 text

Deleted IFRIC 14 text is not part of AASB Interpretation 14.

27A

IAS 1 (as revised in 2007) amended the terminology used throughout IFRSs. In addition it amended paragraph 26. An entity shall apply those amendments for annual periods beginning on or after 1 January 2009. If an entity applies IAS 1 (revised 2007) for an earlier period, the amendments shall be applied for that earlier period.

27B

Prepayments of a Minimum Funding Requirement added paragraph 3A and amended paragraphs 16–18 and 20–22. An entity shall apply those amendments for annual periods beginning on or after 1 January 2011. Earlier application is permitted. If an entity applies the amendments for an earlier period, it shall disclose that fact.

27C

IAS 19 (as amended in 2011) amended paragraphs 1, 6, 17 and 24 and deleted paragraphs 25 and 26. An entity shall apply those amendments when it applies IAS 19 (as amended in 2011).