Illustrative examples

These examples accompany, but are not part of, AASB Interpretation 14.

Example 1—Effect of the minimum funding requirement when there is an AASB 119 surplus and the minimum funding contributions payable are fully refundable to the entity

IE1

An entity has a funding level on the minimum funding requirement basis (which is measured on a different basis from that required under AASB 119) of 82 per cent in Plan A. Under the minimum funding requirements, the entity is required to increase the funding level to 95 per cent immediately. As a result, the entity has a statutory obligation at the end of the reporting period to contribute 200 to Plan A immediately. The plan rules permit a full refund of any surplus to the entity at the end of the life of the plan. The year-end valuations for Plan A are set out below.

|

Fair value of assets |

1,200 |

|

|

Present value of defined benefit obligation under AASB 119 |

(1,100) |

|

|

Surplus |

100 |

|

|

|

|

|

Application of requirements

IE2

Paragraph 24 of Interpretation 14 requires the entity to recognise a liability to the extent that the contributions payable are not fully available. Payment of the contributions of 200 will increase the AASB 119 surplus from 100 to 300. Under the rules of the plan this amount will be fully refundable to the entity with no associated costs. Therefore, no liability is recognised for the obligation to pay the contributions and the net defined benefit asset is 100.

Example 2—Effect of a minimum funding requirement when there is an AASB 119 deficit and the minimum funding contributions payable would not be fully available

IE3

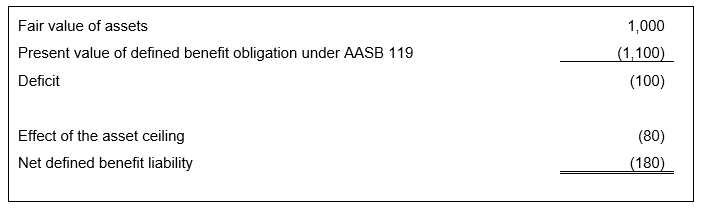

An entity has a funding level on the minimum funding requirement basis (which is measured on a different basis from that required under AASB 119) of 77 per cent in Plan B. Under the minimum funding requirements, the entity is required to increase the funding level to 100 per cent immediately. As a result, the entity has a statutory obligation at the end of the reporting period to pay additional contributions of 300 to Plan B. The plan rules permit a maximum refund of 60 per cent of the AASB 119 surplus to the entity and the entity is not permitted to reduce its contributions below a specified level which happens to equal the AASB 119 service cost. The year-end valuations for Plan B are set out below.

|

Fair value of assets |

1,000 |

|

|

Present value of defined benefit obligation under AASB 119 |

(1,100) |

|

|

Deficit |

(100) |

|

|

|

|

|

Application of requirements

IE4

The payment of 300 would change the AASB 119 deficit of 100 to a surplus of 200. Of this 200, 60 per cent (120) is refundable.

IE5

Therefore, of the contributions of 300, 100 eliminates the AASB 119 deficit and 120 (60 per cent of 200) is available as an economic benefit. The remaining 80 (40 per cent of 200) of the contributions paid is not available to the entity.

IE6

Paragraph 24 of Interpretation 14 requires the entity to recognise a liability to the extent that the additional contributions payable are not available to it.

IE7

Therefore, the net defined benefit liability is 180, comprising the deficit of 100 plus the additional liability of 80 resulting from the requirements in paragraph 24 of Interpretation 14. No other liability is recognised in respect of the statutory obligation to pay contributions of 300.

Summary

IE8

When the contributions of 300 are paid, the net defined benefit asset will be 120.

Example 3—Effect of a minimum funding requirement when the contributions payable would not be fully available and the effect on the economic benefit available as a future contribution reduction

IE9

An entity has a funding level on the minimum funding basis (which it measures on a different basis from that required by AASB 119) of 95 per cent in Plan C. The minimum funding requirements require the entity to pay contributions to increase the funding level to 100 per cent over the next three years. The contributions are required to make good the deficit on the minimum funding basis (shortfall) and to cover future service.

IE10

Plan C also has an AASB 119 surplus at the end of the reporting period of 50, which cannot be refunded to the entity under any circumstances.

IE11

The nominal amounts of contributions required to satisfy the minimum funding requirements in respect of the shortfall and the future service for the next three years are set out below.

|

Year |

Total contributions for minimum funding requirement |

Contributions required to make good the shortfall |

Contributions required to cover future service |

|

1 |

135 |

120 |

15 |

|

2 |

125 |

112 |

13 |

|

3 |

115 |

104 |

11 |

Application of requirements

IE12

The entity’s present obligation in respect of services already received includes the contributions required to make good the shortfall but does not include the contributions required to cover future service.

IE13

The present value of the entity’s obligation, assuming a discount rate of 6 per cent per year, is approximately 300, calculated as follows:

[120/(1.06) + 112/(1.06)2 + 104/(1.06)3]

IE14

When these contributions are paid into the plan, the AASB 119 surplus (ie the fair value of assets less the present value of the defined benefit obligation) would, other things being equal, increase from 50 to 350 (300 + 50).

IE15

However, the surplus is not refundable although an asset may be available as a future contribution reduction.

IE16

In accordance with paragraph 20 of Interpretation 14, the economic benefit available as a reduction in future contributions is the sum of:

(a) any amount that reduces future minimum funding requirement contributions for future service because the entity made a prepayment (ie paid the amount before being required to do so); and

(b) the estimated future service cost in each period in accordance with paragraphs 16 and 17, less the estimated minimum funding requirement contributions that would be required for future service in those periods if there were no prepayment as described in (a).

IE17

In this example there is no prepayment as described in paragraph 20(a). The amounts available as a reduction in future contributions when applying paragraph 20(b) are set out below.

|

Year |

AASB 119 service cost |

Minimum contributions required to cover future service |

Amount available as contribution reduction |

|

1 |

13 |

15 |

(2) |

|

2 |

13 |

13 |

0 |

|

3 |

13 |

11 |

2 |

|

4+ |

13 |

9 |

4 |

IE18

Assuming a discount rate of 6 per cent, the present value of the economic benefit available as a future contribution reduction is therefore equal to:

(2)/(1.06) + 0/(1.06)2 + 2/(1.06)3 + 4/(1.06)4 ... = 56

Thus in accordance with paragraph 58(b) of AASB 119, the present value of the economic benefit available from future contribution reductions is limited to 56.

IE19

Paragraph 24 of Interpretation 14 requires the entity to recognise a liability to the extent that the additional contributions payable will not be fully available. Therefore, the effect of the asset ceiling is 294 (50 + 300 – 56).

IE20

The entity recognises a net defined benefit liability of 244 in the statement of financial position. No other liability is recognised in respect of the obligation to make contributions to fund the minimum funding shortfall.

Summary

|

Surplus |

50 |

|

|

|

|

|

|

Net defined benefit asset (before consideration of the minimum funding requirement) |

50 |

|

|

|

|

|

|

Effect of the asset ceiling |

(294) |

|

|

|

|

|

|

Net defined benefit liability |

(244) |

|

|

|

|

|

IE21

When the contributions of 300 are paid into the plan, the net defined benefit asset will become 56 (300 – 244).

Example 4—Effect of a prepayment when a minimum funding requirement exceeds the expected future service charge

IE22

An entity is required to fund Plan D so that no deficit arises on the minimum funding basis. The entity is required to pay minimum funding requirement contributions to cover the service cost in each period determined on the minimum funding basis.

IE23

Plan D has an AASB 119 surplus of 35 at the beginning of 20X1. This example assumes that the discount rate and expected return on assets are 0 per cent, and that the plan cannot refund the surplus to the entity under any circumstances but can use the surplus for reductions of future contributions.

IE24

The minimum contributions required to cover future service are 15 for each of the next five years. The expected AASB 119 service cost is 10 in each year.

IE25

The entity makes a prepayment of 30 at the beginning of 20X1 in respect of years 20X1 and 20X2, increasing its surplus at the beginning of 20X1 to 65. That prepayment reduces the future contributions it expects to make in the following two years, as follows:

|

Year |

AASB 119 service cost |

Minimum funding requirement contribution before prepayment |

Minimum funding requirement contribution after prepayment |

|

20X1 |

10 |

15 |

0 |

|

20X2 |

10 |

15 |

0 |

|

20X3 |

10 |

15 |

15 |

|

20X4 |

10 |

15 |

15 |

|

20X5 |

10 |

15 |

15 |

|

Total |

50 |

75 |

45 |

Application of requirements

IE26

In accordance with paragraphs 20 and 22 of Interpretation 14, at the beginning of 20X1, the economic benefit available as a reduction in future contributions is the sum of:

(a) 30, being the prepayment of the minimum funding requirement contributions; and

(b) nil. The estimated minimum funding requirement contributions required for future service would be 75 if there was no prepayment. Those contributions exceed the estimated future service cost (50); therefore the entity cannot use any part of the surplus of 35 noted in paragraph IE23 (see paragraph 22).

IE27

Assuming a discount rate of 0 per cent, the present value of the economic benefit available as a reduction in future contributions is equal to 30. Thus in accordance with paragraph 64 of AASB 119 the entity recognises a net defined benefit asset of 30 (because this is lower than the AASB 119 surplus of 65).