This Interpretation addresses the accounting for internal expenditure on the development and operation of an entity’s own web site for internal or external access.

Preamble

Pronouncement

This compiled Interpretation applies to annual periods beginning on or after 1 January 2020. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 January 2020. It incorporates relevant amendments made up to and including 21 May 2019.

Prepared on 2 March 2020 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Interpretations

Compiled versions of Interpretations, original Interpretations and amending pronouncements (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2020

This compiled AASB Interpretation contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

AASB Interpretation 132 Intangible Assets—Web Site Costs (as amended) is set out in paragraphs AusCF1 – Aus10.3. Interpretations are listed in Australian Accounting Standard AASB 1048 Interpretation of Standards and AASB 1057 Application of Australian Accounting Standards sets out their application. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with SIC-32

AASB Interpretation 132 Intangible Assets—Web Site Costs as amended incorporates Interpretation SIC-32 Intangible Assets—Web Site Costs as issued and amended by the International Accounting Standards Board (IASB). Australian‑specific paragraphs (which are not included in SIC-32) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB Interpretation 132 also comply with SIC-32.

Not-for-profit entities’ compliance with SIC-32 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with SIC‑32.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

AASB Interpretation 132

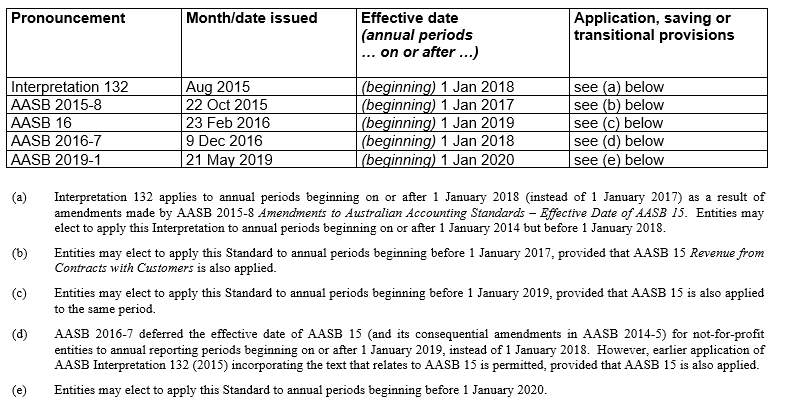

Interpretation 132 was issued in August 2015.

This compiled version of Interpretation 132 applies to annual periods beginning on or after 1 January 2020. It incorporates relevant amendments contained in other AASB pronouncements up to and including 21 May 2019 (see Compilation Details).

Issue

AusCF1

AusCF paragraphs and footnotes included in this Standard apply only to:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

Such entities are referred to as ‘AusCF entities’. For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting (as set out in paragraph Aus1.1 of the Conceptual Framework) shall not apply AusCF paragraphs or footnotes.

1

An entity may incur internal expenditure on the development and operation of its own web site for internal or external access. A web site designed for external access may be used for various purposes such as to promote and advertise an entity’s own products and services, provide electronic services, and sell products and services. A web site designed for internal access may be used to store company policies and customer details, and search relevant information.

2

The stages of a web site’s development can be described as follows:

(a) Planning—includes undertaking feasibility studies, defining objectives and specifications, evaluating alternatives and selecting preferences.

(b) Application and Infrastructure Development—includes obtaining a domain name, purchasing and developing hardware and operating software, installing developed applications and stress testing.

(c) Graphical Design Development—includes designing the appearance of web pages.

(d) Content Development—includes creating, purchasing, preparing and uploading information, either textual or graphical in nature, on the web site before the completion of the web site’s development. This information may either be stored in separate databases that are integrated into (or accessed from) the web site or coded directly into the web pages.

3

Once development of a web site has been completed, the Operating stage begins. During this stage, an entity maintains and enhances the applications, infrastructure, graphical design and content of the web site.

4

When accounting for internal expenditure on the development and operation of an entity’s own web site for internal or external access, the issues are:

(a) whether the web site is an internally generated intangible asset that is subject to the requirements of AASB 138; and

(b) the appropriate accounting treatment of such expenditure.

5

This Interpretation does not apply to expenditure on purchasing, developing, and operating hardware (eg web servers, staging servers, production servers and Internet connections) of a web site. Such expenditure is accounted for under AASB 116. Additionally, when an entity incurs expenditure on an Internet service provider hosting the entity’s web site, the expenditure is recognised as an expense under AASB 101.88 and the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards) when the services are received.

AusCF5

Notwithstanding paragraph 5, in respect of AusCF entities, this Interpretation does not apply to expenditure on purchasing, developing, and operating hardware (eg web servers, staging servers, production servers and Internet connections) of a web site. Such expenditure is accounted for under AASB 116. Additionally, when an entity incurs expenditure on an Internet service provider hosting the entity’s web site, the expenditure is recognised as an expense under AASB 101.88 and the Framework for the Preparation and Presentation of Financial Statements (as identified in AASB 1048 Interpretation of Standards)[AusCF1] when the services are received.

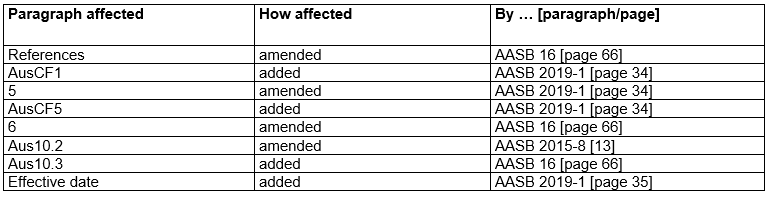

6

AASB 138 does not apply to intangible assets held by an entity for sale in the ordinary course of business (see AASB 102 and AASB 15) or leases of intangible assets accounted for in accordance with AASB 16. Accordingly, this Interpretation does not apply to expenditure on the development or operation of a web site (or web site software) for sale to another entity or that is accounted for in accordance with AASB 16.

In December 2013 the AASB amended the Framework for the Preparation and Presentation of Financial Statements.

Consensus

7

An entity’s own web site that arises from development and is for internal or external access is an internally generated intangible asset that is subject to the requirements of AASB 138.

8

A web site arising from development shall be recognised as an intangible asset if, and only if, in addition to complying with the general requirements described in AASB 138.21 for recognition and initial measurement, an entity can satisfy the requirements in AASB 138.57. In particular, an entity may be able to satisfy the requirement to demonstrate how its web site will generate probable future economic benefits in accordance with AASB 138.57(d) when, for example, the web site is capable of generating revenues, including direct revenues from enabling orders to be placed. An entity is not able to demonstrate how a web site developed solely or primarily for promoting and advertising its own products and services will generate probable future economic benefits, and consequently all expenditure on developing such a web site shall be recognised as an expense when incurred.

9

Any internal expenditure on the development and operation of an entity’s own web site shall be accounted for in accordance with AASB 138. The nature of each activity for which expenditure is incurred (eg training employees and maintaining the web site) and the web site’s stage of development or post-development shall be evaluated to determine the appropriate accounting treatment (additional guidance is provided in the illustrative example accompanying this Interpretation). For example:

(a) the Planning stage is similar in nature to the research phase in AASB 138.54–.56. Expenditure incurred in this stage shall be recognised as an expense when it is incurred.

(b) the Application and Infrastructure Development stage, the Graphical Design stage and the Content Development stage, to the extent that content is developed for purposes other than to advertise and promote an entity’s own products and services, are similar in nature to the development phase in AASB 138.57–.64. Expenditure incurred in these stages shall be included in the cost of a web site recognised as an intangible asset in accordance with paragraph 8 of this Interpretation when the expenditure can be directly attributed and is necessary to creating, producing or preparing the web site for it to be capable of operating in the manner intended by management. For example, expenditure on purchasing or creating content (other than content that advertises and promotes an entity’s own products and services) specifically for a web site, or expenditure to enable use of the content (eg a fee for acquiring a licence to reproduce) on the web site, shall be included in the cost of development when this condition is met. However, in accordance with AASB 138.71, expenditure on an intangible item that was initially recognised as an expense in previous financial statements shall not be recognised as part of the cost of an intangible asset at a later date (eg if the costs of a copyright have been fully amortised, and the content is subsequently provided on a web site).

(c) expenditure incurred in the Content Development stage, to the extent that content is developed to advertise and promote an entity’s own products and services (eg digital photographs of products), shall be recognised as an expense when incurred in accordance with AASB 138.69(c). For example, when accounting for expenditure on professional services for taking digital photographs of an entity’s own products and for enhancing their display, expenditure shall be recognised as an expense as the professional services are received during the process, not when the digital photographs are displayed on the web site.

(d) the Operating stage begins once development of a web site is complete. Expenditure incurred in this stage shall be recognised as an expense when it is incurred unless it meets the recognition criteria in AASB 138.18.

10

A web site that is recognised as an intangible asset under paragraph 8 of this Interpretation shall be measured after initial recognition by applying the requirements of AASB 138.72–.87. The best estimate of a web site’s useful life shall be short.

Effective date

[Deleted by the AASB]

Aus10.2

This Interpretation applies to annual periods beginning on or after 1 January 2018. Earlier application is permitted for periods beginning on or after 1 January 2014 but before 1 January 2018.

Aus10.3

AASB 16, issued in February 2016, amended paragraph 6. An entity shall apply that amendment when it applies AASB 16.

AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework, issued in 2019, added AusCF paragraphs and amended paragraph 5. An entity shall apply the amendments for annual periods beginning on or after 1 January 2020. Earlier application is permitted if at the same time an entity also applies all other amendments made by AASB 2019-1. An entity shall apply the amendments to Interpretation 132 retrospectively in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. However, if an entity determines that retrospective application would be impracticable or would involve undue cost or effort, it shall apply the amendments to Interpretation 132 by reference to paragraphs 23–28, 50–53 and 54F of AASB 108.

Illustrative example

This example accompanies, but is not part of, AASB Interpretation 132. Its purpose is to illustrate examples of expenditure that occur during each of the stages described in paragraphs 2 and 3 of Interpretation 132 and illustrate application of Interpretation 132 to assist in clarifying its meaning. It is not intended to be a comprehensive checklist of expenditure that might be incurred.

Example application of Interpretation 132

|

Stage/nature of expenditure |

Accounting treatment |

|

Planning |

|

|

• undertaking feasibility studies • defining hardware and software specifications • evaluating alternative products and suppliers • selecting preferences |

Recognise as an expense when incurred in accordance with AASB 138.54 |

|

Application and infrastructure development |

|

|

• purchasing or developing hardware |

Apply the requirements of AASB 116 |

|

• obtaining a domain name • developing operating software (eg operating system and server software) • developing code for the application • installing developed applications on the web server • stress testing |

Recognise as an expense when incurred, unless the expenditure can be directly attributed to preparing the web site to operate in the manner intended by management, and the web site meets the recognition criteria in AASB 138.21 and AASB 138.57(a) |

|

Graphical design development |

|

|

• designing the appearance (eg layout and colour) of web pages |

Recognise as an expense when incurred, unless the expenditure can be directly attributed to preparing the web site to operate in the manner intended by management, and the web site meets the recognition criteria in AASB 138.21 and AASB 138.57(a) |

|

Content development |

|

|

• creating, purchasing, preparing (eg creating links and identifying tags), and uploading information, either textual or graphical in nature, on the web site before the completion of the web site’s development. Examples of content include information about an entity, products or services offered for sale, and topics that subscribers access |

Recognise as an expense when incurred in accordance with AASB 138.69(c) to the extent that content is developed to advertise and promote an entity’s own products and services (eg digital photographs of products). Otherwise, recognise as an expense when incurred, unless the expenditure can be directly attributed to preparing the web site to operate in the manner intended by management, and the web site meets the recognition criteria in AASB 138.21 and AASB 138.57(a) |

|

Operating |

|

|

• updating graphics and revising content • adding new functions, features and content • registering the web site with search engines • backing up data • reviewing security access • analysing usage of the web site |

Assess whether it meets the definition of an intangible asset and the recognition criteria set out in AASB 138.18, in which case the expenditure is recognised in the carrying amount of the web site asset |

|

Other |

|

|

• selling, administrative and other general overhead expenditure unless it can be directly attributed to preparing the web site for use to operate in the manner intended by management • clearly identified inefficiencies and initial operating losses incurred before the web site achieves planned performance [eg false start testing] • training employees to operate the web site |

Recognise as an expense when incurred in accordance with AASB 138.65–.70 |

|

(a) All expenditure on developing a web site solely or primarily for promoting and advertising an entity’s own products and services is recognised as an expense when incurred in accordance with AASB 138.68. |

|

Compilation details

AASB Interpretation 132 Intangible Assets—Web Site Costs (as amended)

Compilation details are not part of Interpretation 132.

This compiled Interpretation applies to annual periods beginning on or after 1 January 2020. It takes into account amendments up to and including 21 May 2019 and was prepared on 2 March 2020 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Interpretation issued by the AASB. Instead, it is a representation of Interpretation 132 (August 2015) as amended by other pronouncements, which are listed in the table below.

Table of pronouncements

Table of amendments

Basis for Conclusions on SIC-32

SIC-32 Intangible Assets—Web Site Costs

This Basis for Conclusions accompanies, but is not part of, AASB Interpretation 132. An SIC Basis for Conclusions may be amended to reflect any additional requirements in the AASB Interpretation or AASB Accounting Standards.

[The original text has been marked up to reflect the revision of IAS 16 in 2003 and the subsequent issue of IFRS 3: new text is underlined and deleted text is struck through.]

11

An intangible asset is defined in IAS 38.87 as an identifiable non-monetary asset without physical substance held for use in the production or supply of goods or services, for rental to others, or for administrative purposes. IAS 38.98 provides computer software as a common example of an intangible asset. By analogy, a web site is another example of an intangible asset.

12

IAS 38.6856 requires expenditure on an intangible item to be recognised as an expense when incurred unless it forms part of the cost of an intangible asset that meets the recognition criteria in IAS 38.18–.6755. IAS 38.6957 requires expenditure on start-up activities to be recognised as an expense when incurred. An entity developing its own web site for internal or external access is not undertaking a start-up activity to the extent that an internally generated intangible asset is created. The requirements and guidance in IAS 38.52–.6740.55, in addition to the general requirements described in IAS 38.2119 for recognition and initial measurement of an intangible asset, apply to expenditure incurred on the development of an entity’s own web site. As described in IAS 38.65–.6753–.55, the cost of a web site recognised as an internally generated intangible asset comprises all expenditure that can be directly attributed, or allocated on a reasonable and consistent basis, and is necessary to creating, producing and preparing the asset for it to be capable of operating in the manner intended by management its intended use.

13

IAS 38.5442 requires expenditure on research (or on the research phase of an internal project) to be recognised as an expense when incurred. The examples provided in IAS 38.5644 are similar to the activities undertaken in the Planning stage of a web site’s development. Consequently, expenditure incurred in the Planning stage of a web site’s development is recognised as an expense when incurred.

14

IAS 38.5745 requires an intangible asset arising from the development phase of an internal project to be recognised only if an entity can demonstrate fulfilment of the six criteria specified. One of the criteria is to demonstrate how a web site will generate probable future economic benefits (IAS 38.5745(d)). IAS 38.6048 indicates that this criterion is met by assessing the economic benefits to be received from the web site and using the principles in IAS 36 Impairment of Assets, which considers the present value of estimated future cash flows from continuing use of the web site. Future economic benefits flowing from an intangible asset, as stated in IAS 38.17, may include revenue from the sale of products or services, cost savings, or other benefits resulting from the use of the asset by the entity. Therefore, future economic benefits from a web site may be assessed when the web site is capable of generating revenues. A web site developed solely or primarily for advertising and promoting an entity’s own products and services is not recognised as an intangible asset, because the entity cannot demonstrate the future economic benefits that will flow. Consequently, all expenditure on developing a web site solely or primarily for promoting and advertising an entity’s own products and services is recognised as an expense when incurred.

15

Under IAS 38.2119, an intangible asset is recognised if, and only if, it meets specified criteria. IAS 38.6553 indicates that the cost of an internally generated intangible asset is the sum of expenditure incurred from the date when the intangible asset first meets the specified recognition criteria. When an entity acquires or creates content for purposes other than to advertise and promote an entity’s own products and services, it may be possible to identify an intangible asset (eg a licence or a copyright) separate from a web site. However, a separate asset is not recognised when expenditure is directly attributed, or allocated on a reasonable and consistent basis, to creating, producing, and preparing the web site for it to be capable of operating in the manner intended by management its intended use — the expenditure is included in the cost of developing the web site.

16

IAS 38.6957(c) requires expenditure on advertising and promotional activities to be recognised as an expense when incurred. Expenditure incurred on developing content that advertises and promotes an entity’s own products and services (eg digital photographs of products) is an advertising and promotional activity, and consequently recognised as an expense when incurred in accordance with IAS 38.57(c).

17

Once development of a web site is complete, an enterprise begins the activities described in the Operating stage. Subsequent expenditure to enhance or maintain an enterprise’s own web site is recognised as an expense when incurred unless it meets the recognition criteria in IAS 38.60. IAS 38.61 explains that if the expenditure is required to maintain the asset at its originally assessed standard of performance, then the expenditure is recognised as an expense when incurred.[1] Once development of a web site is complete, an entity begins the activities described in the Operating stage. Subsequent expenditure to enhance or maintain an entity’s own web site is recognised as an expense when incurred unless it meets the recognition criteria in IAS 38.18. IAS 38.20 explains that most subsequent expenditures are likely to maintain the future economic benefits embodied in an existing intangible asset rather than meet the definition of an intangible asset and the recognition criteria set out in IAS 38. In addition, it is often difficult to attribute subsequent expenditure directly to a particular intangible asset rather than to the business as a whole. Therefore, only rarely will subsequent expenditure—expenditure incurred after the initial recognition of a purchased intangible asset or after completion of an internally generated intangible asset—be recognised in the carrying amount of an asset.[2]

IAS 16 Property, Plant and Equipment as revised by the IASB in 2003 requires all subsequent costs to be covered by its general recognition principle and eliminated the requirement to reference the originally assessed standard of performance. IAS 38 was amended as a consequence of the change to IAS 16 and the paragraphs specifically referred to were eliminated. This paragraph has been struck through to avoid any confusion.

The new text was added by IFRS 3 Business Combinations in 2004.

18

An intangible asset is measured after initial recognition by applying the requirements of IAS 38.72–.8763–.78. The revaluation model Allowed Alternative Treatment in IAS 38.7564 is applied only when the fair value of an intangible asset can be determined by reference to an active market.[3] However, as an active market is unlikely to exist for web sites, the cost model Benchmark Treatment applies. Additionally, since IAS 38.84 states that an intangible asset always has a finite useful life, a web site that is recognised as an asset is amortised over the best estimate of its useful life under IAS 38.79. As as indicated in IAS 38.9281, many intangible assets are susceptible to technological obsolescence, and given the history of rapid changes in technology, the useful life of web sites will be short.

IFRS 13 Fair Value Measurement, issued in May 2011, defines fair value and contains the requirements for measuring fair value. IFRS 13 defines an active market.

Amended reference to the Conceptual Framework

19

Following the issue of the revised Conceptual Framework for Financial Reporting in 2018 (2018 Conceptual Framework), the Board issued Amendments to References to the Conceptual Framework in IFRS Standards. In SIC‑32, that document replaced a reference in paragraph 5 to the Framework for the Preparation and Presentation of Financial Statements adopted by the Board in 2001 (Framework) with a reference to the 2018 Conceptual Framework. The Board does not expect that replacement to have a significant effect on the application of the Interpretation. Paragraph 5 describes the accounting for expenditure excluded from the scope of the Interpretation. That paragraph also states that this type of expenditure—expenditure on an Internet service provider hosting the entity’s web site—is recognised as an expense, so the amendment will not affect the accounting treatment.

Deleted SIC-32 text

Deleted SIC-32 text is not part of AASB Interpretation 132.

Date of consensus

May 2001

Effective date

This Interpretation becomes effective on 25 March 2002. The effects of adopting this Interpretation shall be accounted for using the transition requirements in the version of IAS 38 that was issued in 1998. Therefore, when a web site does not meet the criteria for recognition as an intangible asset, but was previously recognised as an asset, the item shall be derecognised at the date when this Interpretation becomes effective. When a web site exists and the expenditure to develop it meets the criteria for recognition as an intangible asset, but was not previously recognised as an asset, the intangible asset shall not be recognised at the date when this Interpretation becomes effective. When a web site exists and the expenditure to develop it meets the criteria for recognition as an intangible asset, was previously recognised as an asset and initially measured at cost, the amount initially recognised is deemed to have been properly determined.

IAS 1 (as revised in 2007) amended the terminology used throughout IFRSs. In addition it amended paragraph 5. An entity shall apply those amendments for annual periods beginning on or after 1 January 2009. If an entity applies IAS 1 (revised 2007) for an earlier period, the amendments shall be applied for that earlier period.

IFRS 15 Revenue from Contracts with Customers, issued in May 2014, amended the ‘References’ section and paragraph 6. An entity shall apply that amendment when it applies IFRS 15.