This Standard applies to recognised and unrecognised financial instruments. Recognised financial instruments include financial assets and financial liabilities that are within the scope of AASB 9. Unrecognised financial instruments include some financial instruments that, although outside the scope of AASB 9, are within the scope of this Standard.

Preamble

Pronouncement

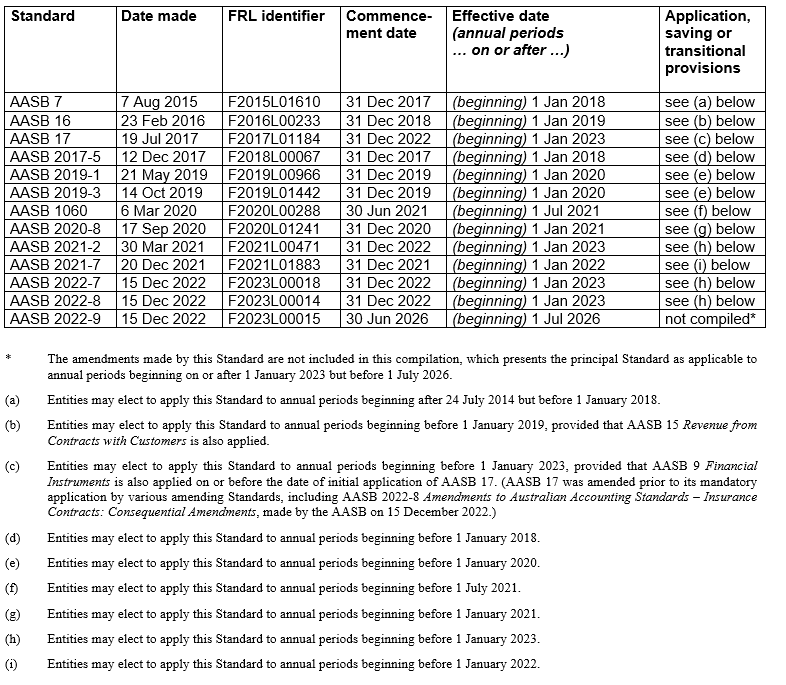

This compiled Standard applies to annual periods beginning on or after 1 January 2023 but before 1 July 2026. Earlier application is permitted for annual periods beginning after 24 July 2014 but before 1 January 2023. It incorporates relevant amendments made up to and including 15 December 2022.

Prepared on 6 April 2023 by the staff of the Australian Accounting Standards Board.

Compilation no. 7

Compilation date: 31 December 2022

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2023

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The Managing Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

Australian Accounting Standard AASB 7 Financial Instruments: Disclosures (as amended) is set out in paragraphs 1 – Aus45.2 and Appendices A, B and D. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the Standard. AASB 7 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IFRS 7

AASB 7 Financial Instruments: Disclosures as amended incorporates IFRS 7 Financial Instruments: Disclosures as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IFRS 7) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB 7 also comply with IFRS 7.

Not-for-profit entities’ compliance with IFRS 7 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IFRS 7.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Accounting Standard AASB 7

The Australian Accounting Standards Board made Accounting Standard AASB 7 Financial Instruments: Disclosures under section 334 of the Corporations Act 2001 on 7 August 2015.

This compiled version of AASB 7 applies to annual periods beginning on or after 1 January 2023 but before 1 July 2026. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 15 December 2022 (see Compilation Details).

Objective

1

The objective of this Standard is to require entities to provide disclosures in their financial statements that enable users to evaluate:

(a) the significance of financial instruments for the entity’s financial position and performance; and

(b) the nature and extent of risks arising from financial instruments to which the entity is exposed during the period and at the end of the reporting period, and how the entity manages those risks.

AusCF1

AusCF entities are:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting are set out in paragraph Aus1.1 of the Conceptual Framework.

Scope

3

This Standard shall be applied by all entities to all types of financial instruments, except:

(a) those interests in subsidiaries, associates or joint ventures that are accounted for in accordance with AASB 10 Consolidated Financial Statements, AASB 127 Separate Financial Statements or AASB 128 Investments in Associates and Joint Ventures. However, in some cases, AASB 10, AASB 127 or AASB 128 require or permit an entity to account for an interest in a subsidiary, associate or joint venture using AASB 9; in those cases, entities shall apply the requirements of this Standard and, for those measured at fair value, the requirements of AASB 13 Fair Value Measurement. Entities shall also apply this Standard to all derivatives linked to interests in subsidiaries, associates or joint ventures unless the derivative meets the definition of an equity instrument in AASB 132.

(b) employers’ rights and obligations arising from employee benefit plans, to which AASB 119 Employee Benefits applies.

(c) [deleted]

(d) insurance contracts as defined in AASB 17 Insurance Contracts or investment contracts with discretionary participation features within the scope of AASB 17. However, this Standard applies to:

(i) derivatives that are embedded in contracts within the scope of AASB 17, if AASB 9 requires the entity to account for them separately.

(ii) investment components that are separated from contracts within the scope of AASB 17, if AASB 17 requires such separation, unless the separated investment component is an investment contract with discretionary participation features.

(iii) an issuer’s rights and obligations arising under insurance contracts that meet the definition of financial guarantee contracts if the issuer applies AASB 9 in recognising and measuring the contracts. However, the issuer shall apply AASB 17 if the issuer elects, in accordance with paragraph 7(e) of AASB 17, to apply AASB 17 in recognising and measuring the contracts.

(iv) an entity’s rights and obligations that are financial instruments arising under credit card contracts, or similar contracts that provide credit or payment arrangements, that an entity issues that meet the definition of an insurance contract if the entity applies AASB 9 to those rights and obligations in accordance with paragraph 7(h) of AASB 17 and paragraph 2.1(e)(iv) of AASB 9.

(v) an entity’s rights and obligations that are financial instruments arising under insurance contracts that an entity issues that limit the compensation for insured events to the amount otherwise required to settle the policyholder’s obligation created by the contract, if the entity elects, in accordance with paragraph 8A of AASB 17, to apply AASB 9 instead of AASB 17 to such contracts.

(e) financial instruments, contracts and obligations under share-based payment transactions to which AASB 2 Share-based Payment applies, except that this Standard applies to contracts within the scope of AASB 9.

(f) instruments that are required to be classified as equity instruments in accordance with paragraphs 16A and 16B or paragraphs 16C and 16D of AASB 132.

Aus3.1

Further to paragraph 3, public sector entities shall not apply this Standard to insurance contracts as defined in AASB 4 Insurance Contracts. However, a public sector entity shall apply this Standard to:

(a) derivatives that are embedded in insurance contracts if AASB 9 requires the entity to account for them separately; and

(b) financial guarantee contracts if the entity applies AASB 9 in recognising and measuring the contracts, in accordance with paragraph 4(d) of AASB 4.

4

This Standard applies to recognised and unrecognised financial instruments. Recognised financial instruments include financial assets and financial liabilities that are within the scope of AASB 9. Unrecognised financial instruments include some financial instruments that, although outside the scope of AASB 9, are within the scope of this Standard.

5

This Standard applies to contracts to buy or sell a non-financial item that are within the scope of AASB 9.

5A

The credit risk disclosure requirements in paragraphs 35A–35N apply to those rights that AASB 15 Revenue from Contracts with Customers specifies are accounted for in accordance with AASB 9 for the purposes of recognising impairment gains or losses. Any reference to financial assets or financial instruments in these paragraphs shall include those rights unless otherwise specified.

Classes of financial instruments and level of disclosure

6

When this Standard requires disclosures by class of financial instrument, an entity shall group financial instruments into classes that are appropriate to the nature of the information disclosed and that take into account the characteristics of those financial instruments. An entity shall provide sufficient information to permit reconciliation to the line items presented in the statement of financial position.

Significance of financial instruments for financial position and performance

7

An entity shall disclose information that enables users of its financial statements to evaluate the significance of financial instruments for its financial position and performance.

Statement of financial position

Categories of financial assets and financial liabilities

8

The carrying amounts of each of the following categories, as specified in AASB 9, shall be disclosed either in the statement of financial position or in the notes:

(a) financial assets measured at fair value through profit or loss, showing separately (i) those designated as such upon initial recognition or subsequently in accordance with paragraph 6.7.1 of AASB 9; (ii) those measured as such in accordance with the election in paragraph 3.3.5 of AASB 9; (iii) those measured as such in accordance with the election in paragraph 33A of AASB 132 and (iv) those mandatorily measured at fair value through profit or loss in accordance with AASB 9.

(b–d) [deleted]

(e) financial liabilities at fair value through profit or loss, showing separately (i) those designated as such upon initial recognition or subsequently in accordance with paragraph 6.7.1 of AASB 9 and (ii) those that meet the definition of held for trading in AASB 9.

(f) financial assets measured at amortised cost.

(g) financial liabilities measured at amortised cost.

(h) financial assets measured at fair value through other comprehensive income, showing separately (i) financial assets that are measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of AASB 9; and (ii) investments in equity instruments designated as such upon initial recognition in accordance with paragraph 5.7.5 of AASB 9.

Financial assets or financial liabilities at fair value through profit or loss

9

If the entity has designated as measured at fair value through profit or loss a financial asset (or group of financial assets) that would otherwise be measured at fair value through other comprehensive income or amortised cost, it shall disclose:

(a) the maximum exposure to credit risk (see paragraph 36(a)) of the financial asset (or group of financial assets) at the end of the reporting period.

(b) the amount by which any related credit derivatives or similar instruments mitigate that maximum exposure to credit risk (see paragraph 36(b)).

(c) the amount of change, during the period and cumulatively, in the fair value of the financial asset (or group of financial assets) that is attributable to changes in the credit risk of the financial asset determined either:

(i) as the amount of change in its fair value that is not attributable to changes in market conditions that give rise to market risk; or

(ii) using an alternative method the entity believes more faithfully represents the amount of change in its fair value that is attributable to changes in the credit risk of the asset.

Changes in market conditions that give rise to market risk include changes in an observed (benchmark) interest rate, commodity price, foreign exchange rate or index of prices or rates.

(d) the amount of the change in the fair value of any related credit derivatives or similar instruments that has occurred during the period and cumulatively since the financial asset was designated.

10

If the entity has designated a financial liability as at fair value through profit or loss in accordance with paragraph 4.2.2 of AASB 9 and is required to present the effects of changes in that liability’s credit risk in other comprehensive income (see paragraph 5.7.7 of AASB 9), it shall disclose:

(a) the amount of change, cumulatively, in the fair value of the financial liability that is attributable to changes in the credit risk of that liability (see paragraphs B5.7.13–B5.7.20 of AASB 9 for guidance on determining the effects of changes in a liability’s credit risk).

(b) the difference between the financial liability’s carrying amount and the amount the entity would be contractually required to pay at maturity to the holder of the obligation.

(c) any transfers of the cumulative gain or loss within equity during the period including the reason for such transfers.

(d) if a liability is derecognised during the period, the amount (if any) presented in other comprehensive income that was realised at derecognition.

10A

If an entity has designated a financial liability as at fair value through profit or loss in accordance with paragraph 4.2.2 of AASB 9 and is required to present all changes in the fair value of that liability (including the effects of changes in the credit risk of the liability) in profit or loss (see paragraphs 5.7.7 and 5.7.8 of AASB 9), it shall disclose:

(a) the amount of change, during the period and cumulatively, in the fair value of the financial liability that is attributable to changes in the credit risk of that liability (see paragraphs B5.7.13–B5.7.20 of AASB 9 for guidance on determining the effects of changes in a liability’s credit risk); and

(b) the difference between the financial liability’s carrying amount and the amount the entity would be contractually required to pay at maturity to the holder of the obligation.

11

The entity shall also disclose:

(a) a detailed description of the methods used to comply with the requirements in paragraphs 9(c), 10(a) and 10A(a) and paragraph 5.7.7(a) of AASB 9, including an explanation of why the method is appropriate.

(b) if the entity believes that the disclosure it has given, either in the statement of financial position or in the notes, to comply with the requirements in paragraph 9(c), 10(a) or 10A(a) or paragraph 5.7.7(a) of AASB 9 does not faithfully represent the change in the fair value of the financial asset or financial liability attributable to changes in its credit risk, the reasons for reaching this conclusion and the factors it believes are relevant.

(c) a detailed description of the methodology or methodologies used to determine whether presenting the effects of changes in a liability’s credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss (see paragraphs 5.7.7 and 5.7.8 of AASB 9). If an entity is required to present the effects of changes in a liability’s credit risk in profit or loss (see paragraph 5.7.8 of AASB 9), the disclosure must include a detailed description of the economic relationship described in paragraph B5.7.6 of AASB 9.

Investments in equity instruments designated at fair value through other comprehensive income

11A

If an entity has designated investments in equity instruments to be measured at fair value through other comprehensive income, as permitted by paragraph 5.7.5 of AASB 9, it shall disclose:

(a) which investments in equity instruments have been designated to be measured at fair value through other comprehensive income.

(b) the reasons for using this presentation alternative.

(c) the fair value of each such investment at the end of the reporting period.

(d) dividends recognised during the period, showing separately those related to investments derecognised during the reporting period and those related to investments held at the end of the reporting period.

(e) any transfers of the cumulative gain or loss within equity during the period including the reason for such transfers.

11B

If an entity derecognised investments in equity instruments measured at fair value through other comprehensive income during the reporting period, it shall disclose:

(a) the reasons for disposing of the investments.

(b) the fair value of the investments at the date of derecognition.

(c) the cumulative gain or loss on disposal.

Reclassification

12–12A

[Deleted]

12B

An entity shall disclose if, in the current or previous reporting periods, it has reclassified any financial assets in accordance with paragraph 4.4.1 of AASB 9. For each such event, an entity shall disclose:

(a) the date of reclassification.

(b) a detailed explanation of the change in business model and a qualitative description of its effect on the entity’s financial statements.

(c) the amount reclassified into and out of each category.

12C

For each reporting period following reclassification until derecognition, an entity shall disclose for assets reclassified out of the fair value through profit or loss category so that they are measured at amortised cost or fair value through other comprehensive income in accordance with paragraph 4.4.1 of AASB 9:

(a) the effective interest rate determined on the date of reclassification; and

(b) the interest revenue recognised.

12D

If, since its last annual reporting date, an entity has reclassified financial assets out of the fair value through other comprehensive income category so that they are measured at amortised cost or out of the fair value through profit or loss category so that they are measured at amortised cost or fair value through other comprehensive income it shall disclose:

(a) the fair value of the financial assets at the end of the reporting period; and

(b) the fair value gain or loss that would have been recognised in profit or loss or other comprehensive income during the reporting period if the financial assets had not been reclassified.

13

[Deleted]

Offsetting financial assets and financial liabilities

13A

The disclosures in paragraphs 13B–13E supplement the other disclosure requirements of this Standard and are required for all recognised financial instruments that are set off in accordance with paragraph 42 of AASB 132. These disclosures also apply to recognised financial instruments that are subject to an enforceable master netting arrangement or similar agreement, irrespective of whether they are set off in accordance with paragraph 42 of AASB 132.

13B

An entity shall disclose information to enable users of its financial statements to evaluate the effect or potential effect of netting arrangements on the entity’s financial position. This includes the effect or potential effect of rights of set-off associated with the entity’s recognised financial assets and recognised financial liabilities that are within the scope of paragraph 13A.

13C

To meet the objective in paragraph 13B, an entity shall disclose, at the end of the reporting period, the following quantitative information separately for recognised financial assets and recognised financial liabilities that are within the scope of paragraph 13A:

(a) the gross amounts of those recognised financial assets and recognised financial liabilities;

(b) the amounts that are set off in accordance with the criteria in paragraph 42 of AASB 132 when determining the net amounts presented in the statement of financial position;

(c) the net amounts presented in the statement of financial position;

(d) the amounts subject to an enforceable master netting arrangement or similar agreement that are not otherwise included in paragraph 13C(b), including:

(i) amounts related to recognised financial instruments that do not meet some or all of the offsetting criteria in paragraph 42 of AASB 132; and

(ii) amounts related to financial collateral (including cash collateral); and

(e) the net amount after deducting the amounts in (d) from the amounts in (c) above.

The information required by this paragraph shall be presented in a tabular format, separately for financial assets and financial liabilities, unless another format is more appropriate.

13D

The total amount disclosed in accordance with paragraph 13C(d) for an instrument shall be limited to the amount in paragraph 13C(c) for that instrument.

13E

An entity shall include a description in the disclosures of the rights of set-off associated with the entity’s recognised financial assets and recognised financial liabilities subject to enforceable master netting arrangements and similar agreements that are disclosed in accordance with paragraph 13C(d), including the nature of those rights.

13F

If the information required by paragraphs 13B–13E is disclosed in more than one note to the financial statements, an entity shall cross-refer between those notes.

Collateral

14

An entity shall disclose:

(a) the carrying amount of financial assets it has pledged as collateral for liabilities or contingent liabilities, including amounts that have been reclassified in accordance with paragraph 3.2.23(a) of AASB 9; and

(b) the terms and conditions relating to its pledge.

15

When an entity holds collateral (of financial or non-financial assets) and is permitted to sell or repledge the collateral in the absence of default by the owner of the collateral, it shall disclose:

(a) the fair value of the collateral held;

(b) the fair value of any such collateral sold or repledged, and whether the entity has an obligation to return it; and

(c) the terms and conditions associated with its use of the collateral.

Allowance account for credit losses

16

[Deleted]

16A

The carrying amount of financial assets measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of AASB 9 is not reduced by a loss allowance and an entity shall not present the loss allowance separately in the statement of financial position as a reduction of the carrying amount of the financial asset. However, an entity shall disclose the loss allowance in the notes to the financial statements.

Compound financial instruments with multiple embedded derivatives

17

If an entity has issued an instrument that contains both a liability and an equity component (see paragraph 28 of AASB 132) and the instrument has multiple embedded derivatives whose values are interdependent (such as a callable convertible debt instrument), it shall disclose the existence of those features.

Defaults and breaches

18

For loans payable recognised at the end of the reporting period, an entity shall disclose:

(a) details of any defaults during the period of principal, interest, sinking fund, or redemption terms of those loans payable;

(b) the carrying amount of the loans payable in default at the end of the reporting period; and

(c) whether the default was remedied, or the terms of the loans payable were renegotiated, before the financial statements were authorised for issue.

19

If, during the period, there were breaches of loan agreement terms other than those described in paragraph 18, an entity shall disclose the same information as required by paragraph 18 if those breaches permitted the lender to demand accelerated repayment (unless the breaches were remedied, or the terms of the loan were renegotiated, on or before the end of the reporting period).

Statement of comprehensive income

Items of income, expense, gains or losses

20

An entity shall disclose the following items of income, expense, gains or losses either in the statement of comprehensive income or in the notes:

(a) net gains or net losses on:

(i) financial assets or financial liabilities measured at fair value through profit or loss, showing separately those on financial assets or financial liabilities designated as such upon initial recognition or subsequently in accordance with paragraph 6.7.1 of AASB 9, and those on financial assets or financial liabilities that are mandatorily measured at fair value through profit or loss in accordance with AASB 9 (eg financial liabilities that meet the definition of held for trading in AASB 9). For financial liabilities designated as at fair value through profit or loss, an entity shall show separately the amount of gain or loss recognised in other comprehensive income and the amount recognised in profit or loss.

(ii–iv) [deleted]

(v) financial liabilities measured at amortised cost.

(vi) financial assets measured at amortised cost.

(vii) investments in equity instruments designated at fair value through other comprehensive income in accordance with paragraph 5.7.5 of AASB 9.

(viii) financial assets measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of AASB 9, showing separately the amount of gain or loss recognised in other comprehensive income during the period and the amount reclassified upon derecognition from accumulated other comprehensive income to profit or loss for the period.

(b) total interest revenue and total interest expense (calculated using the effective interest method) for financial assets that are measured at amortised cost or that are measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of AASB 9 (showing these amounts separately); or financial liabilities that are not measured at fair value through profit or loss.

(c) fee income and expense (other than amounts included in determining the effective interest rate) arising from:

(i) financial assets and financial liabilities that are not at fair value through profit or loss; and

(ii) trust and other fiduciary activities that result in the holding or investing of assets on behalf of individuals, trusts, retirement benefit plans, and other institutions.

(d) [deleted]

(e) [deleted]

20A

An entity shall disclose an analysis of the gain or loss recognised in the statement of comprehensive income arising from the derecognition of financial assets measured at amortised cost, showing separately gains and losses arising from derecognition of those financial assets. This disclosure shall include the reasons for derecognising those financial assets.

Other disclosures

Accounting policies

21

In accordance with paragraph 117 of AASB 101 Presentation of Financial Statements, an entity discloses material accounting policy information. Information about the measurement basis (or bases) for financial instruments used in preparing the financial statements is expected to be material accounting policy information.

Hedge accounting

21A

An entity shall apply the disclosure requirements in paragraphs 21B–24F for those risk exposures that an entity hedges and for which it elects to apply hedge accounting. Hedge accounting disclosures shall provide information about:

(a) an entity’s risk management strategy and how it is applied to manage risk;

(b) how the entity’s hedging activities may affect the amount, timing and uncertainty of its future cash flows; and

(c) the effect that hedge accounting has had on the entity’s statement of financial position, statement of comprehensive income and statement of changes in equity.

21B

An entity shall present the required disclosures in a single note or separate section in its financial statements. However, an entity need not duplicate information that is already presented elsewhere, provided that the information is incorporated by cross-reference from the financial statements to some other statement, such as a management commentary or risk report, that is available to users of the financial statements on the same terms as the financial statements and at the same time. Without the information incorporated by cross-reference, the financial statements are incomplete.

21C

When paragraphs 22A–24F require the entity to separate by risk category the information disclosed, the entity shall determine each risk category on the basis of the risk exposures an entity decides to hedge and for which hedge accounting is applied. An entity shall determine risk categories consistently for all hedge accounting disclosures.

21D

To meet the objectives in paragraph 21A, an entity shall (except as otherwise specified below) determine how much detail to disclose, how much emphasis to place on different aspects of the disclosure requirements, the appropriate level of aggregation or disaggregation, and whether users of financial statements need additional explanations to evaluate the quantitative information disclosed. However, an entity shall use the same level of aggregation or disaggregation it uses for disclosure requirements of related information in this Standard and AASB 13 Fair Value Measurement.

The risk management strategy

22

[Deleted]

22

[Deleted]

22A

An entity shall explain its risk management strategy for each risk category of risk exposures that it decides to hedge and for which hedge accounting is applied. This explanation should enable users of financial statements to evaluate (for example):

(a) how each risk arises.

(b) how the entity manages each risk; this includes whether the entity hedges an item in its entirety for all risks or hedges a risk component (or components) of an item and why.

(c) the extent of risk exposures that the entity manages.

22B

To meet the requirements in paragraph 22A, the information should include (but is not limited to) a description of:

(a) the hedging instruments that are used (and how they are used) to hedge risk exposures;

(b) how the entity determines the economic relationship between the hedged item and the hedging instrument for the purpose of assessing hedge effectiveness; and

(c) how the entity establishes the hedge ratio and what the sources of hedge ineffectiveness are.

22C

When an entity designates a specific risk component as a hedged item (see paragraph 6.3.7 of AASB 9) it shall provide, in addition to the disclosures required by paragraphs 22A and 22B, qualitative or quantitative information about:

(a) how the entity determined the risk component that is designated as the hedged item (including a description of the nature of the relationship between the risk component and the item as a whole); and

(b) how the risk component relates to the item in its entirety (for example, the designated risk component historically covered on average 80 per cent of the changes in fair value of the item as a whole).

The amount, timing and uncertainty of future cash flows

23

[Deleted]

23

[Deleted]

23A

Unless exempted by paragraph 23C, an entity shall disclose by risk category quantitative information to allow users of its financial statements to evaluate the terms and conditions of hedging instruments and how they affect the amount, timing and uncertainty of future cash flows of the entity.

23B

To meet the requirement in paragraph 23A, an entity shall provide a breakdown that discloses:

(a) a profile of the timing of the nominal amount of the hedging instrument; and

(b) if applicable, the average price or rate (for example strike or forward prices etc) of the hedging instrument.

23C

In situations in which an entity frequently resets (ie discontinues and restarts) hedging relationships because both the hedging instrument and the hedged item frequently change (ie the entity uses a dynamic process in which both the exposure and the hedging instruments used to manage that exposure do not remain the same for long—such as in the example in paragraph B6.5.24(b) of AASB 9) the entity:

(a) is exempt from providing the disclosures required by paragraphs 23A and 23B.

(b) shall disclose:

(i) information about what the ultimate risk management strategy is in relation to those hedging relationships;

(ii) a description of how it reflects its risk management strategy by using hedge accounting and designating those particular hedging relationships; and

(iii) an indication of how frequently the hedging relationships are discontinued and restarted as part of the entity’s process in relation to those hedging relationships.

23D

An entity shall disclose by risk category a description of the sources of hedge ineffectiveness that are expected to affect the hedging relationship during its term.

23E

If other sources of hedge ineffectiveness emerge in a hedging relationship, an entity shall disclose those sources by risk category and explain the resulting hedge ineffectiveness.

23F

For cash flow hedges, an entity shall disclose a description of any forecast transaction for which hedge accounting had been used in the previous period, but which is no longer expected to occur.

The effects of hedge accounting on financial position and performance

24

[Deleted]

24

[Deleted]

24A

An entity shall disclose, in a tabular format, the following amounts related to items designated as hedging instruments separately by risk category for each type of hedge (fair value hedge, cash flow hedge or hedge of a net investment in a foreign operation):

(a) the carrying amount of the hedging instruments (financial assets separately from financial liabilities);

(b) the line item in the statement of financial position that includes the hedging instrument;

(c) the change in fair value of the hedging instrument used as the basis for recognising hedge ineffectiveness for the period; and

(d) the nominal amounts (including quantities such as tonnes or cubic metres) of the hedging instruments.

24B

An entity shall disclose, in a tabular format, the following amounts related to hedged items separately by risk category for the types of hedges as follows:

(a) for fair value hedges:

(i) the carrying amount of the hedged item recognised in the statement of financial position (presenting assets separately from liabilities);

(ii) the accumulated amount of fair value hedge adjustments on the hedged item included in the carrying amount of the hedged item recognised in the statement of financial position (presenting assets separately from liabilities);

(iii) the line item in the statement of financial position that includes the hedged item;

(iv) the change in value of the hedged item used as the basis for recognising hedge ineffectiveness for the period; and

(v) the accumulated amount of fair value hedge adjustments remaining in the statement of financial position for any hedged items that have ceased to be adjusted for hedging gains and losses in accordance with paragraph 6.5.10 of AASB 9.

(b) for cash flow hedges and hedges of a net investment in a foreign operation:

(i) the change in value of the hedged item used as the basis for recognising hedge ineffectiveness for the period (ie for cash flow hedges the change in value used to determine the recognised hedge ineffectiveness in accordance with paragraph 6.5.11(c) of AASB 9);

(ii) the balances in the cash flow hedge reserve and the foreign currency translation reserve for continuing hedges that are accounted for in accordance with paragraphs 6.5.11 and 6.5.13(a) of AASB 9; and

(iii) the balances remaining in the cash flow hedge reserve and the foreign currency translation reserve from any hedging relationships for which hedge accounting is no longer applied.

24C

An entity shall disclose, in a tabular format, the following amounts separately by risk category for the types of hedges as follows:

(a) for fair value hedges:

(i) hedge ineffectiveness—ie the difference between the hedging gains or losses of the hedging instrument and the hedged item—recognised in profit or loss (or other comprehensive income for hedges of an equity instrument for which an entity has elected to present changes in fair value in other comprehensive income in accordance with paragraph 5.7.5 of AASB 9); and

(ii) the line item in the statement of comprehensive income that includes the recognised hedge ineffectiveness.

(b) for cash flow hedges and hedges of a net investment in a foreign operation:

(i) hedging gains or losses of the reporting period that were recognised in other comprehensive income;

(ii) hedge ineffectiveness recognised in profit or loss;

(iii) the line item in the statement of comprehensive income that includes the recognised hedge ineffectiveness;

(iv) the amount reclassified from the cash flow hedge reserve or the foreign currency translation reserve into profit or loss as a reclassification adjustment (see AASB 101) (differentiating between amounts for which hedge accounting had previously been used, but for which the hedged future cash flows are no longer expected to occur, and amounts that have been transferred because the hedged item has affected profit or loss);

(v) the line item in the statement of comprehensive income that includes the reclassification adjustment (see AASB 101); and

(vi) for hedges of net positions, the hedging gains or losses recognised in a separate line item in the statement of comprehensive income (see paragraph 6.6.4 of AASB 9).

24D

When the volume of hedging relationships to which the exemption in paragraph 23C applies is unrepresentative of normal volumes during the period (ie the volume at the reporting date does not reflect the volumes during the period) an entity shall disclose that fact and the reason it believes the volumes are unrepresentative.

24E

An entity shall provide a reconciliation of each component of equity and an analysis of other comprehensive income in accordance with AASB 101 that, taken together:

(a) differentiates, at a minimum, between the amounts that relate to the disclosures in paragraph 24C(b)(i) and (b)(iv) as well as the amounts accounted for in accordance with paragraph 6.5.11(d)(i) and (d)(iii) of AASB 9;

(b) differentiates between the amounts associated with the time value of options that hedge transaction related hedged items and the amounts associated with the time value of options that hedge time-period related hedged items when an entity accounts for the time value of an option in accordance with paragraph 6.5.15 of AASB 9; and

(c) differentiates between the amounts associated with forward elements of forward contracts and the foreign currency basis spreads of financial instruments that hedge transaction related hedged items, and the amounts associated with forward elements of forward contracts and the foreign currency basis spreads of financial instruments that hedge time-period related hedged items when an entity accounts for those amounts in accordance with paragraph 6.5.16 of AASB 9.

24F

An entity shall disclose the information required in paragraph 24E separately by risk category. This disaggregation by risk may be provided in the notes to the financial statements.

Option to designate a credit exposure as measured at fair value through profit or loss

24G

If an entity designated a financial instrument, or a proportion of it, as measured at fair value through profit or loss because it uses a credit derivative to manage the credit risk of that financial instrument it shall disclose:

(a) for credit derivatives that have been used to manage the credit risk of financial instruments designated as measured at fair value through profit or loss in accordance with paragraph 6.7.1 of AASB 9, a reconciliation of each of the nominal amount and the fair value at the beginning and at the end of the period;

(b) the gain or loss recognised in profit or loss on designation of a financial instrument, or a proportion of it, as measured at fair value through profit or loss in accordance with paragraph 6.7.1 of AASB 9; and

(c) on discontinuation of measuring a financial instrument, or a proportion of it, at fair value through profit or loss, that financial instrument’s fair value that has become the new carrying amount in accordance with paragraph 6.7.4 of AASB 9 and the related nominal or principal amount (except for providing comparative information in accordance with AASB 101, an entity does not need to continue this disclosure in subsequent periods).

24G

If an entity designated a financial instrument, or a proportion of it, as measured at fair value through profit or loss because it uses a credit derivative to manage the credit risk of that financial instrument it shall disclose:

(a) for credit derivatives that have been used to manage the credit risk of financial instruments designated as measured at fair value through profit or loss in accordance with paragraph 6.7.1 of AASB 9, a reconciliation of each of the nominal amount and the fair value at the beginning and at the end of the period;

(b) the gain or loss recognised in profit or loss on designation of a financial instrument, or a proportion of it, as measured at fair value through profit or loss in accordance with paragraph 6.7.1 of AASB 9; and

(c) on discontinuation of measuring a financial instrument, or a proportion of it, at fair value through profit or loss, that financial instrument’s fair value that has become the new carrying amount in accordance with paragraph 6.7.4 of AASB 9 and the related nominal or principal amount (except for providing comparative information in accordance with AASB 101, an entity does not need to continue this disclosure in subsequent periods).

Uncertainty arising from interest rate benchmark reform

24H

For hedging relationships to which an entity applies the exceptions set out in paragraphs 6.8.4–6.8.12 of AASB 9 or paragraphs 102D–102N of AASB 139, an entity shall disclose:

(a) the significant interest rate benchmarks to which the entity’s hedging relationships are exposed;

(b) the extent of the risk exposure the entity manages that is directly affected by the interest rate benchmark reform;

(c) how the entity is managing the process to transition to alternative benchmark rates;

(d) a description of significant assumptions or judgements the entity made in applying these paragraphs (for example, assumptions or judgements about when the uncertainty arising from interest rate benchmark reform is no longer present with respect to the timing and the amount of the interest rate benchmark-based cash flows); and

(e) the nominal amount of the hedging instruments in those hedging relationships

24H

For hedging relationships to which an entity applies the exceptions set out in paragraphs 6.8.4–6.8.12 of AASB 9 or paragraphs 102D–102N of AASB 139, an entity shall disclose:

(a) the significant interest rate benchmarks to which the entity’s hedging relationships are exposed;

(b) the extent of the risk exposure the entity manages that is directly affected by the interest rate benchmark reform;

(c) how the entity is managing the process to transition to alternative benchmark rates;

(d) a description of significant assumptions or judgements the entity made in applying these paragraphs (for example, assumptions or judgements about when the uncertainty arising from interest rate benchmark reform is no longer present with respect to the timing and the amount of the interest rate benchmark-based cash flows); and

(e) the nominal amount of the hedging instruments in those hedging relationships

Additional disclosures related to interest rate benchmark reform

24I

To enable users of financial statements to understand the effect of interest rate benchmark reform on an entity’s financial instruments and risk management strategy, an entity shall disclose information about:

(a) the nature and extent of risks to which the entity is exposed arising from financial instruments subject to interest rate benchmark reform, and how the entity manages these risks; and

(b) the entity’s progress in completing the transition to alternative benchmark rates, and how the entity is managing the transition.

24J

To meet the objectives in paragraph 24I, an entity shall disclose:

(a) how the entity is managing the transition to alternative benchmark rates, its progress at the reporting date and the risks to which it is exposed arising from financial instruments because of the transition;

(b) disaggregated by significant interest rate benchmark subject to interest rate benchmark reform, quantitative information about financial instruments that have yet to transition to an alternative benchmark rate as at the end of the reporting period, showing separately:

(i) non-derivative financial assets;

(ii) non-derivative financial liabilities; and

(iii) derivatives; and

(c) if the risks identified in paragraph 24J(a) have resulted in changes to an entity’s risk management strategy (see paragraph 22A), a description of these changes.

Fair value

25

Except as set out in paragraph 29, for each class of financial assets and financial liabilities (see paragraph 6), an entity shall disclose the fair value of that class of assets and liabilities in a way that permits it to be compared with its carrying amount.

26

In disclosing fair values, an entity shall group financial assets and financial liabilities into classes, but shall offset them only to the extent that their carrying amounts are offset in the statement of financial position.

27-27B

[Deleted]

28

In some cases, an entity does not recognise a gain or loss on initial recognition of a financial asset or financial liability because the fair value is neither evidenced by a quoted price in an active market for an identical asset or liability (ie a Level 1 input) nor based on a valuation technique that uses only data from observable markets (see paragraph B5.1.2A of AASB 9). In such cases, the entity shall disclose by class of financial asset or financial liability:

(a) its accounting policy for recognising in profit or loss the difference between the fair value at initial recognition and the transaction price to reflect a change in factors (including time) that market participants would take into account when pricing the asset or liability (see paragraph B5.1.2A(b) of AASB 9).

(b) the aggregate difference yet to be recognised in profit or loss at the beginning and end of the period and a reconciliation of changes in the balance of this difference.

(c) why the entity concluded that the transaction price was not the best evidence of fair value, including a description of the evidence that supports the fair value.

29

Disclosures of fair value are not required:

(a) when the carrying amount is a reasonable approximation of fair value, for example, for financial instruments such as short-term trade receivables and payables; or

(b) [deleted]

(c) [deleted]

(d) for lease liabilities.

Aus29.1

Further to paragraph 29, for public sector entities applying AASB 4, disclosures of fair value are not required for a contract containing a discretionary participation feature (as described in AASB 4) if the fair value of that feature cannot be measured reliably. However, an entity shall disclose information to help users of the financial statements make their own judgements about the extent of possible differences between the carrying amount of those contracts and their fair value, including:

(a) the fact that fair value information has not been disclosed for these instruments because their fair value cannot be measured reliably;

(b) a description of the financial instruments, their carrying amount, and an explanation of why fair value cannot be measured reliably;

(c) information about the market for the instruments;

(d) information about whether and how the entity intends to dispose of the financial instruments; and

(e) if financial instruments whose fair value previously could not be reliably measured are derecognised, that fact, their carrying amount at the time of derecognition, and the amount of gain or loss recognised.

30

[Deleted]

Nature and extent of risks arising from financial instruments

31

An entity shall disclose information that enables users of its financial statements to evaluate the nature and extent of risks arising from financial instruments to which the entity is exposed at the end of the reporting period.

32

The disclosures required by paragraphs 33–42 focus on the risks that arise from financial instruments and how they have been managed. These risks typically include, but are not limited to, credit risk, liquidity risk and market risk.

32A

Providing qualitative disclosures in the context of quantitative disclosures enables users to link related disclosures and hence form an overall picture of the nature and extent of risks arising from financial instruments. The interaction between qualitative and quantitative disclosures contributes to disclosure of information in a way that better enables users to evaluate an entity’s exposure to risks.

Qualitative disclosures

33

For each type of risk arising from financial instruments, an entity shall disclose:

(a) the exposures to risk and how they arise;

(b) its objectives, policies and processes for managing the risk and the methods used to measure the risk; and

(c) any changes in (a) or (b) from the previous period.

Quantitative disclosures

34

For each type of risk arising from financial instruments, an entity shall disclose:

(a) summary quantitative data about its exposure to that risk at the end of the reporting period. This disclosure shall be based on the information provided internally to key management personnel of the entity (as defined in AASB 124 Related Party Disclosures), for example the entity’s board of directors or chief executive officer.

(b) the disclosures required by paragraphs 35A–42, to the extent not provided in accordance with (a).

(c) concentrations of risk if not apparent from the disclosures made in accordance with (a) and (b).

35

If the quantitative data disclosed as at the end of the reporting period are unrepresentative of an entity’s exposure to risk during the period, an entity shall provide further information that is representative.

Credit risk

Scope and objectives

35A

An entity shall apply the disclosure requirements in paragraphs 35F–35N to financial instruments to which the impairment requirements in AASB 9 are applied. However:

(a) for trade receivables, contract assets and lease receivables, paragraph 35J(a) applies to those trade receivables, contract assets or lease receivables on which lifetime expected credit losses are recognised in accordance with paragraph 5.5.15 of AASB 9, if those financial assets are modified while more than 30 days past due; and

(b) paragraph 35K(b) does not apply to lease receivables.

35A

An entity shall apply the disclosure requirements in paragraphs 35F–35N to financial instruments to which the impairment requirements in AASB 9 are applied. However:

(a) for trade receivables, contract assets and lease receivables, paragraph 35J(a) applies to those trade receivables, contract assets or lease receivables on which lifetime expected credit losses are recognised in accordance with paragraph 5.5.15 of AASB 9, if those financial assets are modified while more than 30 days past due; and

(b) paragraph 35K(b) does not apply to lease receivables.

35B

The credit risk disclosures made in accordance with paragraphs 35F–35N shall enable users of financial statements to understand the effect of credit risk on the amount, timing and uncertainty of future cash flows. To achieve this objective, credit risk disclosures shall provide:

(a) information about an entity’s credit risk management practices and how they relate to the recognition and measurement of expected credit losses, including the methods, assumptions and information used to measure expected credit losses;

(b) quantitative and qualitative information that allows users of financial statements to evaluate the amounts in the financial statements arising from expected credit losses, including changes in the amount of expected credit losses and the reasons for those changes; and

(c) information about an entity’s credit risk exposure (ie the credit risk inherent in an entity’s financial assets and commitments to extend credit) including significant credit risk concentrations.

35C

An entity need not duplicate information that is already presented elsewhere, provided that the information is incorporated by cross-reference from the financial statements to other statements, such as a management commentary or risk report that is available to users of the financial statements on the same terms as the financial statements and at the same time. Without the information incorporated by cross-reference, the financial statements are incomplete.

35D

To meet the objectives in paragraph 35B, an entity shall (except as otherwise specified) consider how much detail to disclose, how much emphasis to place on different aspects of the disclosure requirements, the appropriate level of aggregation or disaggregation, and whether users of financial statements need additional explanations to evaluate the quantitative information disclosed.

35E

If the disclosures provided in accordance with paragraphs 35F–35N are insufficient to meet the objectives in paragraph 35B, an entity shall disclose additional information that is necessary to meet those objectives.

The credit risk management practices

35F

An entity shall explain its credit risk management practices and how they relate to the recognition and measurement of expected credit losses. To meet this objective an entity shall disclose information that enables users of financial statements to understand and evaluate:

(a) how an entity determined whether the credit risk of financial instruments has increased significantly since initial recognition, including, if and how:

(i) financial instruments are considered to have low credit risk in accordance with paragraph 5.5.10 of AASB 9, including the classes of financial instruments to which it applies; and

(ii) the presumption in paragraph 5.5.11 of AASB 9, that there have been significant increases in credit risk since initial recognition when financial assets are more than 30 days past due, has been rebutted;

(b) an entity’s definitions of default, including the reasons for selecting those definitions;

(c) how the instruments were grouped if expected credit losses were measured on a collective basis;

(d) how an entity determined that financial assets are credit-impaired financial assets;

(e) an entity’s write-off policy, including the indicators that there is no reasonable expectation of recovery and information about the policy for financial assets that are written-off but are still subject to enforcement activity; and

(f) how the requirements in paragraph 5.5.12 of AASB 9 for the modification of contractual cash flows of financial assets have been applied, including how an entity:

(i) determines whether the credit risk on a financial asset that has been modified while the loss allowance was measured at an amount equal to lifetime expected credit losses, has improved to the extent that the loss allowance reverts to being measured at an amount equal to 12-month expected credit losses in accordance with paragraph 5.5.5 of AASB 9; and

(ii) monitors the extent to which the loss allowance on financial assets meeting the criteria in (i) is subsequently remeasured at an amount equal to lifetime expected credit losses in accordance with paragraph 5.5.3 of AASB 9.

35F

An entity shall explain its credit risk management practices and how they relate to the recognition and measurement of expected credit losses. To meet this objective an entity shall disclose information that enables users of financial statements to understand and evaluate:

(a) how an entity determined whether the credit risk of financial instruments has increased significantly since initial recognition, including, if and how:

(i) financial instruments are considered to have low credit risk in accordance with paragraph 5.5.10 of AASB 9, including the classes of financial instruments to which it applies; and

(ii) the presumption in paragraph 5.5.11 of AASB 9, that there have been significant increases in credit risk since initial recognition when financial assets are more than 30 days past due, has been rebutted;

(b) an entity’s definitions of default, including the reasons for selecting those definitions;

(c) how the instruments were grouped if expected credit losses were measured on a collective basis;

(d) how an entity determined that financial assets are credit-impaired financial assets;

(e) an entity’s write-off policy, including the indicators that there is no reasonable expectation of recovery and information about the policy for financial assets that are written-off but are still subject to enforcement activity; and

(f) how the requirements in paragraph 5.5.12 of AASB 9 for the modification of contractual cash flows of financial assets have been applied, including how an entity:

(i) determines whether the credit risk on a financial asset that has been modified while the loss allowance was measured at an amount equal to lifetime expected credit losses, has improved to the extent that the loss allowance reverts to being measured at an amount equal to 12-month expected credit losses in accordance with paragraph 5.5.5 of AASB 9; and

(ii) monitors the extent to which the loss allowance on financial assets meeting the criteria in (i) is subsequently remeasured at an amount equal to lifetime expected credit losses in accordance with paragraph 5.5.3 of AASB 9.

35G

An entity shall explain the inputs, assumptions and estimation techniques used to apply the requirements in Section 5.5 of AASB 9. For this purpose an entity shall disclose:

(a) the basis of inputs and assumptions and the estimation techniques used to:

(i) measure the 12-month and lifetime expected credit losses;

(ii) determine whether the credit risk of financial instruments has increased significantly since initial recognition; and

(iii) determine whether a financial asset is a credit-impaired financial asset.

(b) how forward-looking information has been incorporated into the determination of expected credit losses, including the use of macroeconomic information; and

(c) changes in the estimation techniques or significant assumptions made during the reporting period and the reasons for those changes.

Quantitative and qualitative information about amounts arising from expected credit losses

35H

To explain the changes in the loss allowance and the reasons for those changes, an entity shall provide, by class of financial instrument, a reconciliation from the opening balance to the closing balance of the loss allowance, in a table, showing separately the changes during the period for:

(a) the loss allowance measured at an amount equal to 12-month expected credit losses;

(b) the loss allowance measured at an amount equal to lifetime expected credit losses for:

(i) financial instruments for which credit risk has increased significantly since initial recognition but that are not credit-impaired financial assets;

(ii) financial assets that are credit-impaired at the reporting date (but that are not purchased or originated credit-impaired); and

(iii) trade receivables, contract assets or lease receivables for which the loss allowances are measured in accordance with paragraph 5.5.15 of AASB 9.

(c) financial assets that are purchased or originated credit-impaired. In addition to the reconciliation, an entity shall disclose the total amount of undiscounted expected credit losses at initial recognition on financial assets initially recognised during the reporting period.

35H

To explain the changes in the loss allowance and the reasons for those changes, an entity shall provide, by class of financial instrument, a reconciliation from the opening balance to the closing balance of the loss allowance, in a table, showing separately the changes during the period for:

(a) the loss allowance measured at an amount equal to 12-month expected credit losses;

(b) the loss allowance measured at an amount equal to lifetime expected credit losses for:

(i) financial instruments for which credit risk has increased significantly since initial recognition but that are not credit-impaired financial assets;

(ii) financial assets that are credit-impaired at the reporting date (but that are not purchased or originated credit-impaired); and

(iii) trade receivables, contract assets or lease receivables for which the loss allowances are measured in accordance with paragraph 5.5.15 of AASB 9.

(c) financial assets that are purchased or originated credit-impaired. In addition to the reconciliation, an entity shall disclose the total amount of undiscounted expected credit losses at initial recognition on financial assets initially recognised during the reporting period.

35I

To enable users of financial statements to understand the changes in the loss allowance disclosed in accordance with paragraph 35H, an entity shall provide an explanation of how significant changes in the gross carrying amount of financial instruments during the period contributed to changes in the loss allowance. The information shall be provided separately for financial instruments that represent the loss allowance as listed in paragraph 35H(a)–(c) and shall include relevant qualitative and quantitative information. Examples of changes in the gross carrying amount of financial instruments that contributed to the changes in the loss allowance may include:

(a) changes because of financial instruments originated or acquired during the reporting period;

(b) the modification of contractual cash flows on financial assets that do not result in a derecognition of those financial assets in accordance with AASB 9;

(c) changes because of financial instruments that were derecognised (including those that were written-off) during the reporting period; and

(d) changes arising from whether the loss allowance is measured at an amount equal to 12-month or lifetime expected credit losses.

35J

To enable users of financial statements to understand the nature and effect of modifications of contractual cash flows on financial assets that have not resulted in derecognition and the effect of such modifications on the measurement of expected credit losses, an entity shall disclose:

(a) the amortised cost before the modification and the net modification gain or loss recognised for financial assets for which the contractual cash flows have been modified during the reporting period while they had a loss allowance measured at an amount equal to lifetime expected credit losses; and

(b) the gross carrying amount at the end of the reporting period of financial assets that have been modified since initial recognition at a time when the loss allowance was measured at an amount equal to lifetime expected credit losses and for which the loss allowance has changed during the reporting period to an amount equal to 12-month expected credit losses.

35K

To enable users of financial statements to understand the effect of collateral and other credit enhancements on the amounts arising from expected credit losses, an entity shall disclose by class of financial instrument:

(a) the amount that best represents its maximum exposure to credit risk at the end of the reporting period without taking account of any collateral held or other credit enhancements (eg netting agreements that do not qualify for offset in accordance with AASB 132).

(b) a narrative description of collateral held as security and other credit enhancements, including:

(i) a description of the nature and quality of the collateral held;

(ii) an explanation of any significant changes in the quality of that collateral or credit enhancements as a result of deterioration or changes in the collateral policies of the entity during the reporting period; and

(iii) information about financial instruments for which an entity has not recognised a loss allowance because of the collateral.

(c) quantitative information about the collateral held as security and other credit enhancements (for example, quantification of the extent to which collateral and other credit enhancements mitigate credit risk) for financial assets that are credit-impaired at the reporting date.

35L

An entity shall disclose the contractual amount outstanding on financial assets that were written off during the reporting period and are still subject to enforcement activity.

Credit risk exposure

35M

To enable users of financial statements to assess an entity’s credit risk exposure and understand its significant credit risk concentrations, an entity shall disclose, by credit risk rating grades, the gross carrying amount of financial assets and the exposure to credit risk on loan commitments and financial guarantee contracts. This information shall be provided separately for financial instruments:

(a) for which the loss allowance is measured at an amount equal to 12-month expected credit losses;

(b) for which the loss allowance is measured at an amount equal to lifetime expected credit losses and that are:

(i) financial instruments for which credit risk has increased significantly since initial recognition but that are not credit-impaired financial assets;

(ii) financial assets that are credit-impaired at the reporting date (but that are not purchased or originated credit-impaired); and

(iii) trade receivables, contract assets or lease receivables for which the loss allowances are measured in accordance with paragraph 5.5.15 of AASB 9.

(c) that are purchased or originated credit-impaired financial assets.

35M

To enable users of financial statements to assess an entity’s credit risk exposure and understand its significant credit risk concentrations, an entity shall disclose, by credit risk rating grades, the gross carrying amount of financial assets and the exposure to credit risk on loan commitments and financial guarantee contracts. This information shall be provided separately for financial instruments:

(a) for which the loss allowance is measured at an amount equal to 12-month expected credit losses;

(b) for which the loss allowance is measured at an amount equal to lifetime expected credit losses and that are:

(i) financial instruments for which credit risk has increased significantly since initial recognition but that are not credit-impaired financial assets;

(ii) financial assets that are credit-impaired at the reporting date (but that are not purchased or originated credit-impaired); and

(iii) trade receivables, contract assets or lease receivables for which the loss allowances are measured in accordance with paragraph 5.5.15 of AASB 9.

(c) that are purchased or originated credit-impaired financial assets.

35N

For trade receivables, contract assets and lease receivables to which an entity applies paragraph 5.5.15 of AASB 9, the information provided in accordance with paragraph 35M may be based on a provision matrix (see paragraph B5.5.35 of AASB 9).

36

For all financial instruments within the scope of this Standard, but to which the impairment requirements in AASB 9 are not applied, an entity shall disclose by class of financial instrument:

(a) the amount that best represents its maximum exposure to credit risk at the end of the reporting period without taking account of any collateral held or other credit enhancements (eg netting agreements that do not qualify for offset in accordance with AASB 132); this disclosure is not required for financial instruments whose carrying amount best represents the maximum exposure to credit risk.

(b) a description of collateral held as security and other credit enhancements, and their financial effect (eg quantification of the extent to which collateral and other credit enhancements mitigate credit risk) in respect of the amount that best represents the maximum exposure to credit risk (whether disclosed in accordance with (a) or represented by the carrying amount of a financial instrument).

(c) [deleted]

(d) [deleted]

37

[Deleted]

Collateral and other credit enhancements obtained

38

When an entity obtains financial or non-financial assets during the period by taking possession of collateral it holds as security or calling on other credit enhancements (eg guarantees), and such assets meet the recognition criteria in other Australian Accounting Standards, an entity shall disclose for such assets held at the reporting date:

(a) the nature and carrying amount of the assets; and

(b) when the assets are not readily convertible into cash, its policies for disposing of such assets or for using them in its operations.

38

When an entity obtains financial or non-financial assets during the period by taking possession of collateral it holds as security or calling on other credit enhancements (eg guarantees), and such assets meet the recognition criteria in other Australian Accounting Standards, an entity shall disclose for such assets held at the reporting date:

(a) the nature and carrying amount of the assets; and

(b) when the assets are not readily convertible into cash, its policies for disposing of such assets or for using them in its operations.

Liquidity risk

39

An entity shall disclose:

(a) a maturity analysis for non-derivative financial liabilities (including issued financial guarantee contracts) that shows the remaining contractual maturities.

(b) a maturity analysis for derivative financial liabilities. The maturity analysis shall include the remaining contractual maturities for those derivative financial liabilities for which contractual maturities are essential for an understanding of the timing of the cash flows (see paragraph B11B).

(c) a description of how it manages the liquidity risk inherent in (a) and (b).

Market risk

Sensitivity analysis

40

Unless an entity complies with paragraph 41, it shall disclose:

(a) a sensitivity analysis for each type of market risk to which the entity is exposed at the end of the reporting period, showing how profit or loss and equity would have been affected by changes in the relevant risk variable that were reasonably possible at that date;

(b) the methods and assumptions used in preparing the sensitivity analysis; and

(c) changes from the previous period in the methods and assumptions used, and the reasons for such changes.

40

Unless an entity complies with paragraph 41, it shall disclose:

(a) a sensitivity analysis for each type of market risk to which the entity is exposed at the end of the reporting period, showing how profit or loss and equity would have been affected by changes in the relevant risk variable that were reasonably possible at that date;

(b) the methods and assumptions used in preparing the sensitivity analysis; and

(c) changes from the previous period in the methods and assumptions used, and the reasons for such changes.

41

If an entity prepares a sensitivity analysis, such as value-at-risk, that reflects interdependencies between risk variables (eg interest rates and exchange rates) and uses it to manage financial risks, it may use that sensitivity analysis in place of the analysis specified in paragraph 40. The entity shall also disclose:

(a) an explanation of the method used in preparing such a sensitivity analysis, and of the main parameters and assumptions underlying the data provided; and

(b) an explanation of the objective of the method used and of limitations that may result in the information not fully reflecting the fair value of the assets and liabilities involved.

Other market risk disclosures

42

When the sensitivity analyses disclosed in accordance with paragraph 40 or 41 are unrepresentative of a risk inherent in a financial instrument (for example because the year-end exposure does not reflect the exposure during the year), the entity shall disclose that fact and the reason it believes the sensitivity analyses are unrepresentative.

42

When the sensitivity analyses disclosed in accordance with paragraph 40 or 41 are unrepresentative of a risk inherent in a financial instrument (for example because the year-end exposure does not reflect the exposure during the year), the entity shall disclose that fact and the reason it believes the sensitivity analyses are unrepresentative.

Transfers of financial assets

42A

The disclosure requirements in paragraphs 42B–42H relating to transfers of financial assets supplement the other disclosure requirements of this Standard. An entity shall present the disclosures required by paragraphs 42B–42H in a single note in its financial statements. An entity shall provide the required disclosures for all transferred financial assets that are not derecognised and for any continuing involvement in a transferred asset, existing at the reporting date, irrespective of when the related transfer transaction occurred. For the purposes of applying the disclosure requirements in those paragraphs, an entity transfers all or a part of a financial asset (the transferred financial asset) if, and only if, it either:

(a) transfers the contractual rights to receive the cash flows of that financial asset; or

(b) retains the contractual rights to receive the cash flows of that financial asset, but assumes a contractual obligation to pay the cash flows to one or more recipients in an arrangement.

42B

An entity shall disclose information that enables users of its financial statements:

(a) to understand the relationship between transferred financial assets that are not derecognised in their entirety and the associated liabilities; and

(b) to evaluate the nature of, and risks associated with, the entity’s continuing involvement in derecognised financial assets.

42C

For the purposes of applying the disclosure requirements in paragraphs 42E–42H, an entity has continuing involvement in a transferred financial asset if, as part of the transfer, the entity retains any of the contractual rights or obligations inherent in the transferred financial asset or obtains any new contractual rights or obligations relating to the transferred financial asset. For the purposes of applying the disclosure requirements in paragraphs 42E–42H, the following do not constitute continuing involvement:

(a) normal representations and warranties relating to fraudulent transfer and concepts of reasonableness, good faith and fair dealings that could invalidate a transfer as a result of legal action;

(b) forward, option and other contracts to reacquire the transferred financial asset for which the contract price (or exercise price) is the fair value of the transferred financial asset; or

(c) an arrangement whereby an entity retains the contractual rights to receive the cash flows of a financial asset but assumes a contractual obligation to pay the cash flows to one or more entities and the conditions in paragraph 3.2.5(a)–(c) of AASB 9 are met.

Transferred financial assets that are not derecognised in their entirety

42D

An entity may have transferred financial assets in such a way that part or all of the transferred financial assets do not qualify for derecognition. To meet the objectives set out in paragraph 42B(a), the entity shall disclose at each reporting date for each class of transferred financial assets that are not derecognised in their entirety:

(a) the nature of the transferred assets.

(b) the nature of the risks and rewards of ownership to which the entity is exposed.

(c) a description of the nature of the relationship between the transferred assets and the associated liabilities, including restrictions arising from the transfer on the reporting entity’s use of the transferred assets.