The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles for recognition and measurement in complete or condensed financial statements for an interim period.

Preamble

Pronouncement

This compiled Standard applies to annual periods beginning on or after 1 July 2021 but before 1 January 2023. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 21 July 2021 by the staff of the Australian Accounting Standards Board.

Compilation no. 5

Compilation date: 30 June 2021

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

Australian Accounting Standard AASB 134 Interim Financial Reporting (as amended) is set out in paragraphs 1 – 58. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 134 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IAS 34

AASB 134 Interim Financial Reporting as amended incorporates IAS 34 Interim Financial Reporting as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IAS 34) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB 134 also comply with IAS 34.

Not-for-profit entities’ compliance with IAS 34 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IAS 34.

Tier 2

Entities preparing general purpose financial statements under Australian Accounting Standards – Simplified Disclosures (Tier 2) will not be in compliance with IFRS Standards.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Accounting Standard AASB 134

The Australian Accounting Standards Board made Accounting Standard AASB 134 Interim Financial Reporting under section 334 of the Corporations Act 2001 on 7 August 2015.

This compiled version of AASB 134 applies to annual periods beginning on or after 1 July 2021 but before 1 January 2023. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles for recognition and measurement in complete or condensed financial statements for an interim period. Timely and reliable interim financial reporting improves the ability of investors, creditors, and others to understand an entity’s capacity to generate earnings and cash flows and its financial condition and liquidity.

Scope

1

This Standard does not mandate which entities should be required to publish interim financial reports, how frequently, or how soon after the end of an interim period. However, governments, securities regulators, stock exchanges, and accountancy bodies often require entities whose debt or equity securities are publicly traded to publish interim financial reports. This Standard applies if an entity is required or elects to publish an interim financial report in accordance with Australian Accounting Standards. The International Accounting Standards Committee[1] encourages publicly traded entities to provide interim financial reports that conform to the recognition, measurement, and disclosure principles set out in this Standard. Specifically, publicly traded entities are encouraged:

(a) to provide interim financial reports at least as of the end of the first half of their financial year; and

(b) to make their interim financial reports available not later than 60 days after the end of the interim period.

AusCF1

AusCF paragraphs and footnotes included in this Standard apply only to:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in AASB 1048 Interpretation of Standards).

Such entities are referred to as ‘AusCF entities’. For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting (as set out in paragraph Aus1.1 of the Conceptual Framework) shall not apply AusCF paragraphs or footnotes.

Aus1.1

Under the Corporations Act, disclosing entities are required to prepare half-year financial reports. Disclosing entities may also voluntarily prepare other general purpose interim financial reports. This Standard prescribes the form and content of general purpose interim financial reports, including half-year financial reports prepared by disclosing entities.

Aus1.2

Interim financial reports that are intended to be special purpose financial reports do not fall within the scope of this Standard. However, interim financial reports that are purported to be special purpose financial reports but have the characteristics of general purpose financial statements fall within the scope of this Standard. Interim financial reports that are widely available but lack the characteristics of general purpose financial statements are not regarded as general purpose financial statements. An example is selected interim summary financial information, such as turnover and profit, voluntarily released by some entities. In some cases, professional judgement is needed to determine whether particular interim financial reports are general purpose financial statements.

2

Each financial report, annual or interim, is evaluated on its own for conformity to Australian Accounting Standards. The fact that an entity may not have provided interim financial reports during a particular financial year or may have provided interim financial reports that do not comply with this Standard does not prevent the entity’s annual financial statements from conforming to Australian Accounting Standards if they otherwise do so.

Aus2.1

This Standard does not apply to interim financial reports for the General Government Sector of each government.

3

If an entity’s interim financial report is described as complying with Australian Accounting Standards, it must comply with all of the requirements of this Standard. Paragraph 19 requires certain disclosures in that regard.

The International Accounting Standards Committee was succeeded by the International Accounting Standards Board, which began operations in 2001.

Definitions

4

The following terms are used in this Standard with the meanings specified:

4[1]

Interim period is a financial reporting period shorter than a full financial year.

4[2]

Interim financial report means a financial report containing either a complete set of financial statements (as described in AASB 101 Presentation of Financial Statements) or a set of condensed financial statements (as described in this Standard) for an interim period.

Content of an interim financial report

5

AASB 101 defines a complete set of financial statements as including the following components:

(a) a statement of financial position as at the end of the period;

(b) a statement of profit or loss and other comprehensive income for the period;

(c) a statement of changes in equity for the period;

(d) a statement of cash flows for the period;

(e) notes, comprising significant accounting policies and other explanatory information;

(ea) comparative information in respect of the preceding period as specified in paragraphs 38 and 38A of AASB 101; and

(f) a statement of financial position as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements in accordance with paragraphs 40A–40D of AASB 101.

An entity may use titles for the statements other than those used in this Standard. For example, an entity may use the title ‘statement of comprehensive income’ instead of ‘statement of profit or loss and other comprehensive income’.

6

In the interest of timeliness and cost considerations and to avoid repetition of information previously reported, an entity may be required to or may elect to provide less information at interim dates as compared with its annual financial statements. This Standard defines the minimum content of an interim financial report as including condensed financial statements and selected explanatory notes. The interim financial report is intended to provide an update on the latest complete set of annual financial statements. Accordingly, it focuses on new activities, events, and circumstances and does not duplicate information previously reported.

7

Nothing in this Standard is intended to prohibit or discourage an entity from publishing a complete set of financial statements (as described in AASB 101) in its interim financial report, rather than condensed financial statements and selected explanatory notes. Nor does this Standard prohibit or discourage an entity from including in condensed interim financial statements more than the minimum line items or selected explanatory notes as set out in this Standard. The recognition and measurement guidance in this Standard applies also to complete financial statements for an interim period, and such statements would include all of the disclosures required by this Standard (particularly the selected note disclosures in paragraph 16A) as well as those required by other Australian Accounting Standards.

Minimum components of an interim financial report

8

An interim financial report shall include, at a minimum, the following components:

(a) a condensed statement of financial position;

(b) a condensed statement or condensed statements of profit or loss and other comprehensive income;

(c) a condensed statement of changes in equity;

(d) a condensed statement of cash flows; and

(e) selected explanatory notes.

8A

If an entity presents items of profit or loss in a separate statement as described in paragraph 10A of AASB 101, it presents interim condensed information from that statement.

Form and content of interim financial statements

9

If an entity publishes a complete set of financial statements in its interim financial report, the form and content of those statements shall conform to the requirements of AASB 101 for a complete set of financial statements.

10

If an entity publishes a set of condensed financial statements in its interim financial report, those condensed statements shall include, at a minimum, each of the headings and subtotals that were included in its most recent annual financial statements and the selected explanatory notes as required by this Standard. Additional line items or notes shall be included if their omission would make the condensed interim financial statements misleading.

11A

If an entity presents items of profit or loss in a separate statement as described in paragraph 10A of AASB 101, it presents basic and diluted earnings per share in that statement.

12

AASB 101 provides guidance on the structure of financial statements. The Implementation Guidance for IAS 1 illustrates ways in which the statement of financial position, statement of comprehensive income and statement of changes in equity may be presented.

13

[Deleted]

14

An interim financial report is prepared on a consolidated basis if the entity’s most recent annual financial statements were consolidated statements. The parent’s separate financial statements are not consistent or comparable with the consolidated statements in the most recent annual financial report. If an entity’s annual financial report included the parent’s separate financial statements in addition to consolidated financial statements, this Standard neither requires nor prohibits the inclusion of the parent’s separate statements in the entity’s interim financial report.

Significant events and transactions

15

An entity shall include in its interim financial report an explanation of events and transactions that are significant to an understanding of the changes in financial position and performance of the entity since the end of the last annual reporting period. Information disclosed in relation to those events and transactions shall update the relevant information presented in the most recent annual financial report.

15A

A user of an entity’s interim financial report will have access to the most recent annual financial report of that entity. Therefore, it is unnecessary for the notes to an interim financial report to provide relatively insignificant updates to the information that was reported in the notes in the most recent annual financial report.

15B

The following is a list of events and transactions for which disclosures would be required if they are significant: the list is not exhaustive.

(a) the write-down of inventories to net realisable value and the reversal of such a write-down;

(b) recognition of a loss from the impairment of financial assets, property, plant and equipment, intangible assets, assets arising from contracts with customers, or other assets, and the reversal of such an impairment loss;

(c) the reversal of any provisions for the costs of restructuring;

(d) acquisitions and disposals of items of property, plant and equipment;

(e) commitments for the purchase of property, plant and equipment;

(f) litigation settlements;

(g) corrections of prior period errors;

(h) changes in the business or economic circumstances that affect the fair value of the entity’s financial assets and financial liabilities, whether those assets or liabilities are recognised at fair value or amortised cost;

(i) any loan default or breach of a loan agreement that has not been remedied on or before the end of the reporting period;

(j) related party transactions;

(k) transfers between levels of the fair value hierarchy used in measuring the fair value of financial instruments;

(l) changes in the classification of financial assets as a result of a change in the purpose or use of those assets; and

(m) changes in contingent liabilities or contingent assets.

15C

Individual Australian Accounting Standards provide guidance regarding disclosure requirements for many of the items listed in paragraph 15B. When an event or transaction is significant to an understanding of the changes in an entity’s financial position or performance since the last annual reporting period, its interim financial report should provide an explanation of and an update to the relevant information included in the financial statements of the last annual reporting period.

16

[Deleted]

Other disclosures

16A

In addition to disclosing significant events and transactions in accordance with paragraphs 15–15C, an entity shall include the following information, in the notes to its interim financial statements or elsewhere in the interim financial report. The following disclosures shall be given either in the interim financial statements or incorporated by cross-reference from the interim financial statements to some other statement (such as management commentary or risk report) that is available to users of the financial statements on the same terms as the interim financial statements and at the same time. If users of the financial statements do not have access to the information incorporated by cross-reference on the same terms and at the same time, the interim financial report is incomplete. The information shall normally be reported on a financial year-to-date basis.

(a) a statement that the same accounting policies and methods of computation are followed in the interim financial statements as compared with the most recent annual financial statements or, if those policies or methods have been changed, a description of the nature and effect of the change.

(b) explanatory comments about the seasonality or cyclicality of interim operations.

(c) the nature and amount of items affecting assets, liabilities, equity, net income or cash flows that are unusual because of their nature, size or incidence.

(d) the nature and amount of changes in estimates of amounts reported in prior interim periods of the current financial year or changes in estimates of amounts reported in prior financial years.

(e) issues, repurchases and repayments of debt and equity securities.

(f) dividends paid (aggregate or per share) separately for ordinary shares and other shares.

(g) the following segment information (disclosure of segment information is required in an entity’s interim financial report only if AASB 8 Operating Segments requires that entity to disclose segment information in its annual financial statements):

(i) revenues from external customers, if included in the measure of segment profit or loss reviewed by the chief operating decision maker or otherwise regularly provided to the chief operating decision maker.

(ii) intersegment revenues, if included in the measure of segment profit or loss reviewed by the chief operating decision maker or otherwise regularly provided to the chief operating decision maker.

(iii) a measure of segment profit or loss.

(iv) a measure of total assets and liabilities for a particular reportable segment if such amounts are regularly provided to the chief operating decision maker and if there has been a material change from the amount disclosed in the last annual financial statements for that reportable segment.

(v) a description of differences from the last annual financial statements in the basis of segmentation or in the basis of measurement of segment profit or loss.

(vi) a reconciliation of the total of the reportable segments’ measures of profit or loss to the entity’s profit or loss before tax expense (tax income) and discontinued operations. However, if an entity allocates to reportable segments items such as tax expense (tax income), the entity may reconcile the total of the segments’ measures of profit or loss to profit or loss after those items. Material reconciling items shall be separately identified and described in that reconciliation.

(h) events after the interim period that have not been reflected in the financial statements for the interim period.

(i) the effect of changes in the composition of the entity during the interim period, including business combinations, obtaining or losing control of subsidiaries and long-term investments, restructurings, and discontinued operations. In the case of business combinations, the entity shall disclose the information required by AASB 3 Business Combinations.

(j) for financial instruments, the disclosures about fair value required by paragraphs 91–93(h), 94–96, 98 and 99 of AASB 13 Fair Value Measurement and paragraphs 25, 26 and 28–30 of AASB 7 Financial Instruments: Disclosures.

(k) for entities becoming, or ceasing to be, investment entities, as defined in AASB 10 Consolidated Financial Statements, the disclosures in AASB 12 Disclosure of Interests in Other Entities paragraph 9B.

(l) the disaggregation of revenue from contracts with customers required by paragraphs 114–115 of AASB 15 Revenue from Contracts with Customers.

17–18

[Deleted]

Disclosure of compliance with Australian Accounting Standards

19

If an entity’s interim financial report is in compliance with this Standard, that fact shall be disclosed. An interim financial report shall not be described as complying with Australian Accounting Standards unless it complies with all the requirements of Australian Accounting Standards.

Periods for which interim financial statements are required to be presented

20

Interim reports shall include interim financial statements (condensed or complete) for periods as follows:

(a) statement of financial position as of the end of the current interim period and a comparative statement of financial position as of the end of the immediately preceding financial year.

(b) statements of profit or loss and other comprehensive income for the current interim period and cumulatively for the current financial year to date, with comparative statements of profit or loss and other comprehensive income for the comparable interim periods (current and year-to-date) of the immediately preceding financial year. As permitted by AASB 101, an interim report may present for each period a statement or statements of profit or loss and other comprehensive income.

(c) statement of changes in equity cumulatively for the current financial year to date, with a comparative statement for the comparable year-to-date period of the immediately preceding financial year.

(d) statement of cash flows cumulatively for the current financial year to date, with a comparative statement for the comparable year-to-date period of the immediately preceding financial year.

21

For an entity whose business is highly seasonal, financial information for the twelve months up to the end of the interim period and comparative information for the prior twelve-month period may be useful. Accordingly, entities whose business is highly seasonal are encouraged to consider reporting such information in addition to the information called for in the preceding paragraph.

22

Part A of the illustrative examples accompanying this Standard illustrates the periods required to be presented by an entity that reports half-yearly and an entity that reports quarterly.

Materiality

23

In deciding how to recognise, measure, classify, or disclose an item for interim financial reporting purposes, materiality shall be assessed in relation to the interim period financial data. In making assessments of materiality, it shall be recognised that interim measurements may rely on estimates to a greater extent than measurements of annual financial data.

24

AASB 101 defines material information and requires separate disclosure of material items, including (for example) discontinued operations, and AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors requires disclosure of changes in accounting estimates, errors, and changes in accounting policies. The two Standards do not contain quantified guidance as to materiality.

25

While judgement is always required in assessing materiality, this Standard bases the recognition and disclosure decision on data for the interim period by itself for reasons of understandability of the interim figures. Thus, for example, unusual items, changes in accounting policies or estimates, and errors are recognised and disclosed on the basis of materiality in relation to interim period data to avoid misleading inferences that might result from non-disclosure. The overriding goal is to ensure that an interim financial report includes all information that is relevant to understanding an entity’s financial position and performance during the interim period.

This paragraph was amended by AASB 2008-5 Amendments to Australian Accounting Standards arising from the Annual Improvements Project issued in July 2008 to clarify the scope of AASB 134.

Disclosure in annual financial statements

26

If an estimate of an amount reported in an interim period is changed significantly during the final interim period of the financial year but a separate financial report is not published for that final interim period, the nature and amount of that change in estimate shall be disclosed in a note to the annual financial statements for that financial year.

27

AASB 108 requires disclosure of the nature and (if practicable) the amount of a change in estimate that either has a material effect in the current period or is expected to have a material effect in subsequent periods. Paragraph 16A(d) of this Standard requires similar disclosure in an interim financial report. Examples include changes in estimate in the final interim period relating to inventory write-downs, restructurings, or impairment losses that were reported in an earlier interim period of the financial year. The disclosure required by the preceding paragraph is consistent with the AASB 108 requirement and is intended to be narrow in scope—relating only to the change in estimate. An entity is not required to include additional interim period financial information in its annual financial statements.

Recognition and measurement

Same accounting policies as annual

28

An entity shall apply the same accounting policies in its interim financial statements as are applied in its annual financial statements, except for accounting policy changes made after the date of the most recent annual financial statements that are to be reflected in the next annual financial statements. However, the frequency of an entity’s reporting (annual, half-yearly, or quarterly) shall not affect the measurement of its annual results. To achieve that objective, measurements for interim reporting purposes shall be made on a year-to-date basis.

29

Requiring that an entity apply the same accounting policies in its interim financial statements as in its annual statements may seem to suggest that interim period measurements are made as if each interim period stands alone as an independent reporting period. However, by providing that the frequency of an entity’s reporting shall not affect the measurement of its annual results, paragraph 28 acknowledges that an interim period is a part of a larger financial year. Year-to-date measurements may involve changes in estimates of amounts reported in prior interim periods of the current financial year. But the principles for recognising assets, liabilities, income, and expenses for interim periods are the same as in annual financial statements.

30

To illustrate:

(a) the principles for recognising and measuring losses from inventory write-downs, restructurings, or impairments in an interim period are the same as those that an entity would follow if it prepared only annual financial statements. However, if such items are recognised and measured in one interim period and the estimate changes in a subsequent interim period of that financial year, the original estimate is changed in the subsequent interim period either by accrual of an additional amount of loss or by reversal of the previously recognised amount;

(b) a cost that does not meet the definition of an asset at the end of an interim period is not deferred in the statement of financial position either to await future information as to whether it has met the definition of an asset or to smooth earnings over interim periods within a financial year; and

(c) income tax expense is recognised in each interim period based on the best estimate of the weighted average annual income tax rate expected for the full financial year. Amounts accrued for income tax expense in one interim period may have to be adjusted in a subsequent interim period of that financial year if the estimate of the annual income tax rate changes.

31

Under the Conceptual Framework for Financial Reporting (Conceptual Framework) (as identified in AASB 1048 Interpretation of Standards), recognition is the process of capturing, for inclusion in the statement of financial position or the statement(s) of financial performance, an item that meets the definition of one of the elements of the financial statements. The definitions of assets, liabilities, income, and expenses are fundamental to recognition, at the end of both annual and interim financial reporting periods.

AusCF31

Notwithstanding paragraph 31, in respect of AusCF entities, under the Framework for the Preparation and Presentation of Financial Statements (the Framework) (as identified in AASB 1048 Interpretation of Standards)[AusCF3], recognition is the ‘process of incorporating in the balance sheet or income statement an item that meets the definition of an element and satisfies the criteria for recognition’. The definitions of assets, liabilities, income, and expenses are fundamental to recognition, at the end of both annual and interim financial reporting periods.

32

For assets, the same tests of future economic benefits apply at interim dates and at the end of an entity’s financial year. Costs that, by their nature, would not qualify as assets at financial year-end would not qualify at interim dates either. Similarly, a liability at the end of an interim reporting period must represent an existing obligation at that date, just as it must at the end of an annual reporting period.

33

An essential characteristic of income (revenue) and expenses is that the related inflows and outflows of assets and liabilities have already taken place. If those inflows or outflows have taken place, the related revenue and expense are recognised; otherwise they are not recognised. The Conceptual Framework does not allow the recognition of items in the statement of financial position which do not meet the definition of assets or liabilities.

AusCF33

Notwithstanding paragraph 33, in respect of AusCF entities, an essential characteristic of income (revenue) and expenses is that the related inflows and outflows of assets and liabilities have already taken place. If those inflows or outflows have taken place, the related revenue and expense are recognised; otherwise they are not recognised. The Framework says that ‘expenses are recognised in the income statement when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably … [The] Framework does not allow the recognition of items in the balance sheet which do not meet the definition of assets or liabilities.’

34

In measuring the assets, liabilities, income, expenses, and cash flows reported in its financial statements, an entity that reports only annually is able to take into account information that becomes available throughout the financial year. Its measurements are, in effect, on a year-to-date basis.

35

An entity that reports half-yearly uses information available by mid-year or shortly thereafter in making the measurements in its financial statements for the first six-month period and information available by year-end or shortly thereafter for the twelve-month period. The twelve-month measurements will reflect possible changes in estimates of amounts reported for the first six-month period. The amounts reported in the interim financial report for the first six-month period are not retrospectively adjusted. Paragraphs 16A(d) and 26 require, however, that the nature and amount of any significant changes in estimates be disclosed.

36

An entity that reports more frequently than half-yearly measures income and expenses on a year-to-date basis for each interim period using information available when each set of financial statements is being prepared. Amounts of income and expenses reported in the current interim period will reflect any changes in estimates of amounts reported in prior interim periods of the financial year. The amounts reported in prior interim periods are not retrospectively adjusted. Paragraphs 16A(d) and 26 require, however, that the nature and amount of any significant changes in estimates be disclosed.

Revenues received seasonally, cyclically, or occasionally

37

Revenues that are received seasonally, cyclically, or occasionally within a financial year shall not be anticipated or deferred as of an interim date if anticipation or deferral would not be appropriate at the end of the entity’s financial year.

38

Examples include dividend revenue, royalties, and government grants. Additionally, some entities consistently earn more revenues in certain interim periods of a financial year than in other interim periods, for example, seasonal revenues of retailers. Such revenues are recognised when they occur.

Costs incurred unevenly during the financial year

39

Costs that are incurred unevenly during an entity’s financial year shall be anticipated or deferred for interim reporting purposes if, and only if, it is also appropriate to anticipate or defer that type of cost at the end of the financial year.

Applying the recognition and measurement principles

40

Part B of the illustrative examples accompanying this Standard provides examples of applying the general recognition and measurement principles set out in paragraphs 28–39.

Use of estimates

41

The measurement procedures to be followed in an interim financial report shall be designed to ensure that the resulting information is reliable and that all material financial information that is relevant to an understanding of the financial position or performance of the entity is appropriately disclosed. While measurements in both annual and interim financial reports are often based on reasonable estimates, the preparation of interim financial reports generally will require a greater use of estimation methods than annual financial reports.

42

Part C of the illustrative examples accompanying this Standard provides examples of the use of estimates in interim periods.

In December 2013 the AASB amended the Framework for the Preparation and Presentation of Financial Statements.

Restatement of previously reported interim periods

43

A change in accounting policy, other than one for which the transition is specified by a new Australian Accounting Standard, shall be reflected by:

(a) restating the financial statements of prior interim periods of the current financial year and the comparable interim periods of any prior financial years that will be restated in the annual financial statements in accordance with AASB 108; or

(b) when it is impracticable to determine the cumulative effect at the beginning of the financial year of applying a new accounting policy to all prior periods, adjusting the financial statements of prior interim periods of the current financial year, and comparable interim periods of prior financial years to apply the new accounting policy prospectively from the earliest date practicable.

44

One objective of the preceding principle is to ensure that a single accounting policy is applied to a particular class of transactions throughout an entire financial year. Under AASB 108, a change in accounting policy is reflected by retrospective application, with restatement of prior period financial data as far back as is practicable. However, if the cumulative amount of the adjustment relating to prior financial years is impracticable to determine, then under AASB 108 the new policy is applied prospectively from the earliest date practicable. The effect of the principle in paragraph 43 is to require that within the current financial year any change in accounting policy is applied either retrospectively or, if that is not practicable, prospectively, from no later than the beginning of the financial year.

45

To allow accounting changes to be reflected as of an interim date within the financial year would allow two differing accounting policies to be applied to a particular class of transactions within a single financial year. The result would be interim allocation difficulties, obscured operating results, and complicated analysis and understandability of interim period information.

Effective date

46

This Standard becomes operative for financial statements covering periods beginning on or after 1 January 2018. Earlier application is encouraged for periods beginning on or after 1 January 2014 but before 1 January 2018.

47–54

[Deleted by the AASB]

55

AASB 2014-5 Amendments to Australian Accounting Standards arising from AASB 15, issued in December 2014, amended paragraphs 15B and 16A in the previous version of this Standard. An entity shall apply those amendments when it applies AASB 15.

56

AASB 2015-1 Amendments to Australian Accounting Standards – Annual Improvements to Australian Accounting Standards 2012–2014 Cycle, issued in January 2015, amended paragraph 16A in the previous version of this Standard. An entity shall apply that amendment retrospectively in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors for annual periods beginning on or after 1 January 2016. Earlier application is permitted. If an entity applies the amendment for an earlier period it shall disclose that fact.

57

AASB 2015-2 Amendments to Australian Accounting Standards – Disclosure Initiative: Amendments to AASB 101, issued in January 2015, amended paragraph 5 in the previous version of this Standard. An entity shall apply that amendment for annual periods beginning on or after 1 January 2016. Earlier application of that amendment is permitted.

58

AASB 2018-7 Amendments to Australian Accounting Standards – Definition of Material, issued in December 2018, amended paragraph 24. An entity shall apply those amendments prospectively for annual periods beginning on or after 1 January 2020. Earlier application is permitted. If an entity applies those amendments for an earlier period, it shall disclose that fact. An entity shall apply those amendments when it applies the amendments to the definition of material in paragraph 7 of AASB 101 and paragraphs 5 and 6 of AASB 108.

58

AASB 2019-1 Amendments to Australian Accounting Standards – References to the Conceptual Framework, issued in 2019, added AusCF paragraphs and amended paragraphs 31, 33 and B23. An entity shall apply those amendments for annual periods beginning on or after 1 January 2020. Earlier application is permitted if at the same time an entity also applies all other amendments made by AASB 2019-1. An entity shall apply the amendments to AASB 134 retrospectively in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. However, if an entity determines that retrospective application would be impracticable or would involve undue cost or effort, it shall apply the amendments to AASB 134 by reference to paragraphs 43–45 of this Standard and paragraphs 23–28, 50–53 and 54F of AASB 108.

Withdrawal of AASB pronouncements

Aus57.2

This Standard repeals AASB 134 Interim Financial Reporting issued in July 2004. Despite the repeal, after the time this Standard starts to apply under section 334 of the Corporations Act (either generally or in relation to an individual entity), the repealed Standard continues to apply in relation to any period ending before that time as if the repeal had not occurred.

[Note: When this Standard applies under section 334 of the Corporations Act (either generally or in relation to an individual entity), it supersedes the application of the repealed Standard.]

Illustrative examples

These illustrative examples accompany, but are not part of, AASB 134.

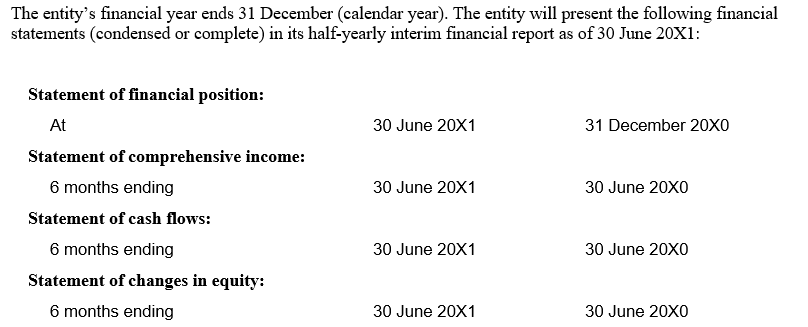

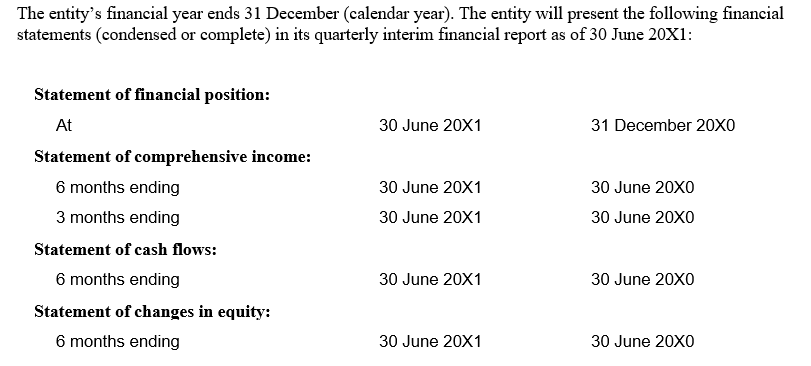

A Illustration of periods required to be presented

The following examples illustrate application of the principle in paragraph 20.

Entity publishes interim financial reports half-yearly

A1

Entity publishes interim financial reports quarterly

A2

B Examples of applying the recognition and measurement principles

The following are examples of applying the general recognition and measurement principles set out in paragraphs 28–39.

Employer payroll taxes and insurance contributions

B1

If employer payroll taxes or contributions to government-sponsored insurance funds are assessed on an annual basis, the employer’s related expense is recognised in interim periods using an estimated average annual effective payroll tax or contribution rate, even though a large portion of the payments may be made early in the financial year. A common example is an employer payroll tax or insurance contribution that is imposed up to a certain maximum level of earnings per employee. For higher income employees, the maximum income is reached before the end of the financial year, and the employer makes no further payments through the end of the year.

Major planned periodic maintenance or overhaul

B2

The cost of a planned major periodic maintenance or overhaul or other seasonal expenditure that is expected to occur late in the year is not anticipated for interim reporting purposes unless an event has caused the entity to have a legal or constructive obligation. The mere intention or necessity to incur expenditure related to the future is not sufficient to give rise to an obligation.

Provisions

B3

A provision is recognised when an entity has no realistic alternative but to make a transfer of economic benefits as a result of an event that has created a legal or constructive obligation. The amount of the obligation is adjusted upward or downward, with a corresponding loss or gain recognised in profit or loss, if the entity’s best estimate of the amount of the obligation changes.

B4

The Standard requires that an entity apply the same criteria for recognising and measuring a provision at an interim date as it would at the end of its financial year. The existence or non-existence of an obligation to transfer benefits is not a function of the length of the reporting period. It is a question of fact.

Year-end bonuses

B5

The nature of year-end bonuses varies widely. Some are earned simply by continued employment during a time period. Some bonuses are earned based on a monthly, quarterly, or annual measure of operating result. They may be purely discretionary, contractual, or based on years of historical precedent.

B6

A bonus is anticipated for interim reporting purposes if, and only if, (a) the bonus is a legal obligation or past practice would make the bonus a constructive obligation for which the entity has no realistic alternative but to make the payments, and (b) a reliable estimate of the obligation can be made. AASB 119 Employee Benefits provides guidance.

Variable lease payments

B7

Variable lease payments based on sales can be an example of a legal or constructive obligation that is recognised as a liability. If a lease provides for variable payments based on the lessee achieving a certain level of annual sales, an obligation can arise in the interim periods of the financial year before the required annual level of sales has been achieved, if that required level of sales is expected to be achieved and the entity, therefore, has no realistic alternative but to make the future lease payment.

Intangible assets

B8

An entity will apply the definition and recognition criteria for an intangible asset in the same way in an interim period as in an annual period. Costs incurred before the recognition criteria for an intangible asset are met are recognised as an expense. Costs incurred after the specific point in time at which the criteria are met are recognised as part of the cost of an intangible asset. ‘Deferring’ costs as assets in an interim statement of financial position in the hope that the recognition criteria will be met later in the financial year is not justified.

Pensions

B9

Pension cost for an interim period is calculated on a year-to-date basis by using the actuarially determined pension cost rate at the end of the prior financial year, adjusted for significant market fluctuations since that time and for significant one-off events, such as plan amendments, curtailments and settlements.

Vacations, holidays, and other short-term compensated absences

B10

Accumulating paid absences are those that are carried forward and can be used in future periods if the current period’s entitlement is not used in full. AASB 119 Employee Benefits requires that an entity measure the expected cost of and obligation for accumulating paid absences at the amount the entity expects to pay as a result of the unused entitlement that has accumulated at the end of the reporting period. That principle is also applied at the end of interim financial reporting periods. Conversely, an entity recognises no expense or liability for non-accumulating paid absences at the end of an interim reporting period, just as it recognises none at the end of an annual reporting period.

Other planned but irregularly occurring costs

B11

An entity’s budget may include certain costs expected to be incurred irregularly during the financial year, such as charitable contributions and employee training costs. Those costs generally are discretionary even though they are planned and tend to recur from year to year. Recognising an obligation at the end of an interim financial reporting period for such costs that have not yet been incurred generally is not consistent with the definition of a liability.

Measuring interim income tax expense

B12

Interim period income tax expense is accrued using the tax rate that would be applicable to expected total annual earnings, that is, the estimated average annual effective income tax rate applied to the pre-tax income of the interim period.

B13

This is consistent with the basic concept set out in paragraph 28 that the same accounting recognition and measurement principles shall be applied in an interim financial report as are applied in annual financial statements. Income taxes are assessed on an annual basis. Interim period income tax expense is calculated by applying to an interim period’s pre-tax income the tax rate that would be applicable to expected total annual earnings, that is, the estimated average annual effective income tax rate. That estimated average annual rate would reflect a blend of the progressive tax rate structure expected to be applicable to the full year’s earnings including enacted or substantively enacted changes in the income tax rates scheduled to take effect later in the financial year. AASB 112 Income Taxes provides guidance on substantively enacted changes in tax rates. The estimated average annual income tax rate would be re-estimated on a year-to-date basis, consistent with paragraph 28 of the Standard. Paragraph 16A requires disclosure of a significant change in estimate.

B14

To the extent practicable, a separate estimated average annual effective income tax rate is determined for each taxing jurisdiction and applied individually to the interim period pre-tax income of each jurisdiction. Similarly, if different income tax rates apply to different categories of income (such as capital gains or income earned in particular industries), to the extent practicable a separate rate is applied to each individual category of interim period pre-tax income. While that degree of precision is desirable, it may not be achievable in all cases, and a weighted average of rates across jurisdictions or across categories of income is used if it is a reasonable approximation of the effect of using more specific rates.

B15

To illustrate the application of the foregoing principle, an entity reporting quarterly expects to earn 10,000 pre-tax each quarter and operates in a jurisdiction with a tax rate of 20 per cent on the first 20,000 of annual earnings and 30 per cent on all additional earnings. Actual earnings match expectations. The following table shows the amount of income tax expense that is reported in each quarter:

|

1st Quarter |

2nd Quarter |

3rd Quarter |

4th Quarter |

Annual |

|

|

Tax expense |

2,500 |

2,500 |

2,500 |

2,500 |

10,000 |

10,000 of tax is expected to be payable for the full year on 40,000 of pre-tax income.

B16

As another illustration, an entity reports quarterly, earns 15,000 pre-tax profit in the first quarter but expects to incur losses of 5,000 in each of the three remaining quarters (thus having zero income for the year), and operates in a jurisdiction in which its estimated average annual income tax rate is expected to be 20 per cent. The following table shows the amount of income tax expense that is reported in each quarter:

|

1st Quarter |

2nd Quarter |

3rd Quarter |

4th Quarter |

Annual |

|

|

Tax expense |

3,000 |

(1,000) |

(1,000) |

(1,000) |

0 |

Difference in financial reporting year and tax year

B17

If the financial reporting year and the income tax year differ, income tax expense for the interim periods of that financial reporting year is measured using separate weighted average estimated effective tax rates for each of the income tax years applied to the portion of pre-tax income earned in each of those income tax years.

B18

To illustrate, an entity’s financial reporting year ends 30 June and it reports quarterly. Its taxable year ends 31 December. For the financial year that begins 1 July, Year 1 and ends 30 June, Year 2, the entity earns 10,000 pre-tax each quarter. The estimated average annual income tax rate is 30 per cent in Year 1 and 40 per cent in Year 2.

|

Quarter ending 30 Sept |

Quarter ending 31 Dec |

Quarter ending 31 Mar |

Quarter ending 30 June |

Year ending 30 June |

|

|

Year 1 |

Year 1 |

Year 2 |

Year 2 |

Year 2 |

|

|

Tax expense |

3,000 |

3,000 |

4,000 |

4,000 |

14,000 |

Tax credits

B19

Some tax jurisdictions give taxpayers credits against the tax payable based on amounts of capital expenditures, exports, research and development expenditures, or other bases. Anticipated tax benefits of this type for the full year are generally reflected in computing the estimated annual effective income tax rate, because those credits are granted and calculated on an annual basis under most tax laws and regulations. On the other hand, tax benefits that relate to a one-off event are recognised in computing income tax expense in that interim period, in the same way that special tax rates applicable to particular categories of income are not blended into a single effective annual tax rate. Moreover, in some jurisdictions tax benefits or credits, including those related to capital expenditures and levels of exports, while reported on the income tax return, are more similar to a government grant and are recognised in the interim period in which they arise.

Tax loss and tax credit carrybacks and carryforwards

B20

The benefits of a tax loss carryback are reflected in the interim period in which the related tax loss occurs. AASB 112 provides that ‘the benefit relating to a tax loss that can be carried back to recover current tax of a previous period shall be recognised as an asset’. A corresponding reduction of tax expense or increase of tax income is also recognised.

B21

AASB 112 provides that ‘a deferred tax asset shall be recognised for the carryforward of unused tax losses and unused tax credits to the extent that it is probable that future taxable profit will be available against which the unused tax losses and unused tax credits can be utilised’. AASB 112 provides criteria for assessing the probability of taxable profit against which the unused tax losses and credits can be utilised. Those criteria are applied at the end of each interim period and, if they are met, the effect of the tax loss carryforward is reflected in the computation of the estimated average annual effective income tax rate.

B22

To illustrate, an entity that reports quarterly has an operating loss carryforward of 10,000 for income tax purposes at the start of the current financial year for which a deferred tax asset has not been recognised. The entity earns 10,000 in the first quarter of the current year and expects to earn 10,000 in each of the three remaining quarters. Excluding the carryforward, the estimated average annual income tax rate is expected to be 40 per cent. Tax expense is as follows:

|

|

1st |

2nd |

3rd |

4th |

Annual |

|

Tax expense |

3,000 |

3,000 |

3,000 |

3,000 |

12,000 |

Contractual or anticipated purchase price changes

B23

Volume rebates or discounts and other contractual changes in the prices of raw materials, labour, or other purchased goods and services are anticipated in interim periods, by both the payer and the recipient, if it is probable that they have been earned or will take effect. Thus, contractual rebates and discounts are anticipated but discretionary rebates and discounts are not anticipated because the resulting asset or liability would not satisfy the conditions in the Framework[4] that an asset must be a resource controlled by the entity as a result of a past event and that a liability must be a present obligation whose settlement is expected to result in an outflow of resources.

Depreciation and amortisation

B24

Depreciation and amortisation for an interim period is based only on assets owned during that interim period. It does not take into account asset acquisitions or dispositions planned for later in the financial year.

Inventories

B25

Inventories are measured for interim financial reporting by the same principles as at financial year-end. AASB 102 Inventories establishes standards for recognising and measuring inventories. Inventories pose particular problems at the end of any financial reporting period because of the need to determine inventory quantities, costs, and net realisable values. Nonetheless, the same measurement principles are applied for interim inventories. To save cost and time, entities often use estimates to measure inventories at interim dates to a greater extent than at the end of annual reporting periods. Following are examples of how to apply the net realisable value test at an interim date and how to treat manufacturing variances at interim dates.

Net realisable value of inventories

B26

The net realisable value of inventories is determined by reference to selling prices and related costs to complete and dispose at interim dates. An entity will reverse a write-down to net realisable value in a subsequent interim period only if it would be appropriate to do so at the end of the financial year.

B27

[Deleted]

Interim period manufacturing cost variances

B28

Price, efficiency, spending, and volume variances of a manufacturing entity are recognised in income at interim reporting dates to the same extent that those variances are recognised in income at financial year-end. Deferral of variances that are expected to be absorbed by year-end is not appropriate because it could result in reporting inventory at the interim date at more or less than its portion of the actual cost of manufacture.

Foreign currency translation gains and losses

B29

Foreign currency translation gains and losses are measured for interim financial reporting by the same principles as at financial year-end.

B30

AASB 121 The Effects of Changes in Foreign Exchange Rates specifies how to translate the financial statements for foreign operations into the presentation currency, including guidelines for using average or closing foreign exchange rates and guidelines for recognising the resulting adjustments in profit or loss, or in other comprehensive income. Consistently with AASB 121, the actual average and closing rates for the interim period are used. Entities do not anticipate some future changes in foreign exchange rates in the remainder of the current financial year in translating foreign operations at an interim date.

B31

If AASB 121 requires translation adjustments to be recognised as income or expense in the period in which they arise, that principle is applied during each interim period. Entities do not defer some foreign currency translation adjustments at an interim date if the adjustment is expected to reverse before the end of the financial year.

Interim financial reporting in hyperinflationary economies

B32

Interim financial reports in hyperinflationary economies are prepared by the same principles as at financial year-end.

B33

AASB 129 Financial Reporting in Hyperinflationary Economies requires that the financial statements of an entity that reports in the currency of a hyperinflationary economy be stated in terms of the measuring unit current at the end of the reporting period, and the gain or loss on the net monetary position is included in net income. Also, comparative financial data reported for prior periods are restated to the current measuring unit.

B34

Entities follow those same principles at interim dates, thereby presenting all interim data in the measuring unit as of the end of the interim period, with the resulting gain or loss on the net monetary position included in the interim period’s net income. Entities do not annualise the recognition of the gain or loss. Nor do they use an estimated annual inflation rate in preparing an interim financial report in a hyperinflationary economy.

Impairment of assets

B35

AASB 136 Impairment of Assets requires that an impairment loss be recognised if the recoverable amount has declined below carrying amount.

B36

This Standard requires that an entity apply the same impairment testing, recognition, and reversal criteria at an interim date as it would at the end of its financial year. That does not mean, however, that an entity must necessarily make a detailed impairment calculation at the end of each interim period. Rather, an entity will review for indications of significant impairment since the end of the most recent financial year to determine whether such a calculation is needed.

C Examples of the use of estimates

The following examples illustrate application of the principle in paragraph 41.

C1

Inventories: Full stock-taking and valuation procedures may not be required for inventories at interim dates, although it may be done at financial year-end. It may be sufficient to make estimates at interim dates based on sales margins.

C2

Classifications of current and non-current assets and liabilities: Entities may do a more thorough investigation for classifying assets and liabilities as current or non-current at annual reporting dates than at interim dates.

C3

Provisions: Determination of the appropriate amount of a provision (such as a provision for warranties, environmental costs, and site restoration costs) may be complex and often costly and time-consuming. Entities sometimes engage outside experts to assist in the annual calculations. Making similar estimates at interim dates often entails updating of the prior annual provision rather than the engaging of outside experts to do a new calculation.

C4

Pensions: AASB 119 Employee Benefits requires an entity to determine the present value of defined benefit obligations and the fair value of plan assets at the end of each reporting period and encourages an entity to involve a professionally qualified actuary in measurement of the obligations. For interim reporting purposes, reliable measurement is often obtainable by extrapolation of the latest actuarial valuation.

C5

Income taxes: Entities may calculate income tax expense and deferred income tax liability at annual dates by applying the tax rate for each individual jurisdiction to measures of income for each jurisdiction. Paragraph B14 acknowledges that while that degree of precision is desirable at interim reporting dates as well, it may not be achievable in all cases, and a weighted average of rates across jurisdictions or across categories of income is used if it is a reasonable approximation of the effect of using more specific rates.

C6

Contingencies: The measurement of contingencies may involve the opinions of legal experts or other advisers. Formal reports from independent experts are sometimes obtained with respect to contingencies. Such opinions about litigation, claims, assessments, and other contingencies and uncertainties may or may not also be needed at interim dates.

C7

Revaluations and fair value accounting: AASB 116 Property, Plant and Equipment allows an entity to choose as its accounting policy the revaluation model whereby items of property, plant and equipment are revalued to fair value. AASB 16 Leases allows a lessee to measure right-of-use assets applying the revaluation model in AASB 116 if those right-of-use assets relate to a class of property, plant and equipment to which the lessee applies the revaluation model in AASB 116. Similarly, AASB 140 Investment Property requires an entity to measure the fair value of investment property. For those measurements, an entity may rely on professionally qualified valuers at annual reporting dates though not at interim reporting dates.

C8

Intercompany reconciliations: Some intercompany balances that are reconciled on a detailed level in preparing consolidated financial statements at financial year-end might be reconciled at a less detailed level in preparing consolidated financial statements at an interim date.

C9

Specialised industries: Because of complexity, costliness, and time, interim period measurements in specialised industries might be less precise than at financial year-end. An example would be calculation of insurance reserves by insurance companies.

The reference to the Framework is to the Framework for the Preparation and Presentation of Financial Statements adopted by the AASB in 2004.

Compilation details

Accounting Standard AASB 134 Interim Financial Reporting (as amended)

Compilation details are not part of AASB 134.

This compiled Standard applies to annual periods beginning on or after 1 July 2021 but before 1 January 2023. It takes into account amendments up to and including 6 March 2020 and was prepared on 21 July 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 134 (August 2015) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments to Standard

Table of amendments to illustrative examples

Deleted IAS 34 text

Deleted IAS 34 text is not part of AASB 134.

47

IAS 1 (as revised in 2007) amended the terminology used throughout IFRSs. In addition it amended paragraphs 4, 5, 8, 11, 12 and 20, deleted paragraph 13 and added paragraphs 8A and 11A. An entity shall apply those amendments for annual periods beginning on or after 1 January 2009. If an entity applies IAS 1 (revised 2007) for an earlier period, the amendments shall be applied for that earlier period.

48

IFRS 3 (as revised in 2008) amended paragraph 16(i). An entity shall apply that amendment for annual periods beginning on or after 1 July 2009. If an entity applies IFRS 3 (revised 2008) for an earlier period, the amendment shall also be applied for that earlier period.

49

Paragraphs 15, 27, 35 and 36 were amended, paragraphs 15A–15C and 16A were added and paragraphs 16–18 were deleted by Improvements to IFRSs in May 2010. An entity shall apply those amendments for annual periods beginning on or after 1 January 2011. Earlier application is permitted. If an entity applies the amendments for an earlier period it shall disclose that fact.

50

IFRS 13, issued in May 2011, added paragraph 16A(j). An entity shall apply that amendment when it applies IFRS 13.

51

Presentation of Items of Other Comprehensive Income (Amendments to IAS 1), issued in June 2011, amended paragraphs 8, 8A, 11A and 20. An entity shall apply those amendments when it applies IAS 1 as amended in June 2011.

52

Annual Improvements 2009–2011 Cycle, issued in May 2012, amended paragraph 5 as a consequential amendment derived from the amendment to IAS 1 Presentation of Financial Statements. An entity shall apply that amendment retrospectively in accordance with IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors for annual periods beginning on or after 1 January 2013. Earlier application is permitted. If an entity applies that amendment for an earlier period it shall disclose that fact.

53

Annual Improvements 2009–2011 Cycle, issued in May 2012, amended paragraph 16A. An entity shall apply that amendment retrospectively in accordance with IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors for annual periods beginning on or after 1 January 2013. Earlier application is permitted. If an entity applies that amendment for an earlier period it shall disclose that fact.

54

Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27), issued in October 2012, amended paragraph 16A. An entity shall apply that amendment for annual periods beginning on or after 1 January 2014. Earlier application of Investment Entities is permitted. If an entity applies that amendment earlier it shall also apply all amendments included in Investment Entities at the same time.