The objective of this Standard is to specify budgetary disclosure requirements for the whole of government, General Government Sector (GGS) and not-for-profit entities within the GGS of each government.

Preamble

Pronouncement

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. Earlier application is permitted for annual reporting periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1055 Budgetary Reporting (as amended) is set out in paragraphs 1 – 15 and Appendices A and B. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 1055 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with international pronouncements

AASB 1055 and International Public Sector Accounting Standards

International Public Sector Accounting Standards (IPSAS) are issued by the International Public Sector Accounting Standards Board (IPSASB).

IPSAS 24 Presentation of Budget Information in Financial Statements applies to public sector entities that are required or elect to make their approved budget(s) publicly available. This is a broader scope than AASB 1055, which applies to the whole of government, the General Government Sector (GGS) and not-for-profit entities within the GGS in respect of budgetary information presented to parliament.

There are basic differences in the requirements of the Standards as well. For example, IPSAS 24 gives primacy to the budget basis of presentation and classification over the accounting basis of presentation and classification adopted in AASB 1055 and also permits explanations of variances being disclosed outside the financial report.

AASB 1055 requires disclosure of the original presented budget but acknowledges that revised budgets might also be disclosed, whereas IPSAS 24 requires both the initial approved budget and the final approved budget to be disclosed. AASB 1055 requires disclosure of explanations of major variances between actual and original budget amounts, whereas IPSAS 24 requires disclosure of explanations of material variances between actual amounts and the amounts in the budget for which the entity is held publicly accountable (which may be either the original or the final budget). AASB 1055 does not require disclosure of explanations for changes between the original and the final budget.

AASB 1055 requires the budget information to relate to the reporting period, whereas IPSAS 24 does not have such a restriction and contemplates multi-year budget periods.

AASB 1055 and International Financial Reporting Standards

There is no specific Standard issued by the International Accounting Standards Board dealing with budgetary information to be included in:

(a) whole of government general purpose financial statements (which AASB 1055 limits to the Australian Government and State and Territory Governments);

(b) the financial statements of the General Government Sector of a government; or

(c) the general purpose financial statements of not-for-profit entities within the GGS.

Accounting Standard AASB 1055

The Australian Accounting Standards Board made Accounting Standard AASB 1055 Budgetary Reporting on 5 March 2013.

This compiled version of AASB 1055 applies to annual reporting periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

1

The objective of this Standard is to specify budgetary disclosure requirements for the whole of government, General Government Sector (GGS) and not-for-profit entities within the GGS of each government. Disclosures made in accordance with this Standard provide users with information relevant to assessing performance of an entity, including accountability for resources entrusted to it.

Application and Scope

2

[Deleted by the AASB]

3

This Standard applies to annual reporting periods beginning on or after 1 July 2014.

[Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

4

This Standard may be applied to annual reporting periods beginning before 1 July 2014, provided that AASB 2013-1 Amendments to AASB 1049 – Relocation of Budgetary Reporting Requirements is also applied to the same period.

5

[Deleted by the AASB]

Budgetary Information

6

Where an entity’s budgeted:

(a) statement of financial position;

(b) statement of profit or loss and other comprehensive income;

(c) statement of changes in equity; or

(d) statement of cash flows;

reflecting controlled items is presented to parliament and is separately identified as relating to that entity, the entity shall disclose for the reporting period:

(e) that original budgeted financial statement presented to parliament, presented and classified on a basis that is consistent with the presentation and classification adopted in the corresponding financial statement prepared in accordance with Australian Accounting Standards; and

(f) explanations of major variances between the actual amounts presented in the financial statements and the corresponding original budget amounts.

7

Where an entity within the GGS’s budgeted financial information reflecting major classes of administered income and expenses, or major classes of administered assets and liabilities, is presented to parliament and is separately identified as relating to that entity, the entity shall disclose for the reporting period:

(a) that original budgeted financial information presented to parliament, presented and classified on a basis that is consistent with the presentation and classification adopted for the corresponding information about administered items disclosed in accordance with AASB 1050 Administered Items; and

(b) explanations of major variances between the actual amounts disclosed in the financial statements in accordance with AASB 1050 and the corresponding original budget amounts.

8

Comparative budgetary information in respect of the previous period need not be disclosed.

9

The original budget is the first budget presented to parliament in respect of the reporting period.

10

Under AASB 101 Presentation of Financial Statements an entity may present a statement of profit or loss and other comprehensive income as:

(a) a single statement of profit or loss and other comprehensive income, with profit or loss and other comprehensive income presented in two sections; or

(b) the profit or loss section in a separate statement of profit or loss, and a separate statement presenting comprehensive income that begins with profit or loss.

AASB 1049 Whole of Government and General Government Sector Financial Reporting limits the presentation of the statement of profit or loss and other comprehensive income of a GGS and a whole of government to the format described in (a) above. Accordingly, if a GGS or whole of government budget presented to parliament is in the format described in (b), in accordance with paragraph 6(e) of this Standard, that budgeted information would need to be restated for disclosure purposes to align with the format described in (a).

11

Any revised budget that is presented to parliament during the reporting period may be disclosed in the financial statements in addition to the original budget and might need to be referred to in explanations of major variances as noted in paragraph 15.

12

Information provided in accordance with paragraph 6 or 7 facilitates users of financial statements (including taxpayers) making and evaluating decisions about the allocation of scarce resources and for assessing the discharge of an entity’s accountability. The budget information is disclosed on the same presentation and classification bases adopted for the corresponding actual information in the financial statements, to facilitate a comparison of actual outcomes against the budget. Accordingly:

(a) in relation to controlled items, to the extent the presentation and classification bases adopted in the budget presented to parliament are not consistent with the corresponding financial statements, the budget presented to parliament is restated for disclosure purposes to align with the presentation and classification bases adopted in the corresponding financial statements. As such, the budget information may be presented in the corresponding financial statements; and

(b) in relation to administered items of entities within the GGS, to the extent the presentation and classification bases adopted in the budget presented to parliament are not consistent with the corresponding information about administered items disclosed in accordance with AASB 1050, the budget presented to parliament is restated for disclosure purposes to align with the presentation and classification bases adopted for the corresponding information about administered items disclosed in accordance with AASB 1050. As such, the budget information may be disclosed with the corresponding information about administered items, including where the corresponding information about administered items is disclosed with the financial statements.

13

Budgeted financial information reflecting administered income and expenses, or assets and liabilities, presented to parliament that is subject to the requirements of paragraph 7 would, consistent with AASB 1050, at a minimum, contain information about major classes of administered income and expenses, or major classes of administered assets and liabilities. Accordingly, if the budgeted information of an entity within a GGS is presented to parliament only at a more highly summarised level, for example, budgeted aggregate of administered income and expenses, that entity would not be required to report the budgetary information specified in paragraph 7. Similarly, the requirements in paragraph 6 do not apply where parliament only receives information about an entity’s budgeted controlled items at a more highly summarised level than the level of information required by Australian Accounting Standards to be presented in the financial statements.

14

The budgetary reporting requirements in this Standard only apply to an entity within the GGS where budgeted information about controlled or administered items is separately identified as relating to that entity within the budgetary information presented to parliament. Accordingly, for example, where:

(a) a consolidated GGS budget presented to parliament incorporates a budget of an entity within the GGS in a way that the individual entity’s budget is not separately identified as relating to that entity; and

(b) a separate individual budget is not presented to parliament for that entity;

that entity’s budget is not regarded as having been presented to parliament and therefore the entity is not required to report the budgetary information specified in this Standard.

15

The explanations of major variances required to be disclosed by paragraph 6(f) or 7(b) are those relevant to an assessment of the discharge of accountability and to an analysis of performance of an entity, not merely focusing on the numerical differences between original budget and actual amounts. They include high-level explanations of the causes of major variances rather than merely the nature of the variances. Furthermore, if revised budgets are presented to parliament, even when there are no major numerical differences between the original budget and actual amounts, an entity might need to have regard to those revised budgets and include explanations for major numerical differences between them and actual amounts. Such explanations are made when they are relevant for the assessment of the discharge of accountability and to an analysis of the performance of an entity.

Appendix A -- Defined terms

This appendix is an integral part of AASB 1055.

ABS GFS Manual

A[1]

Australian Bureau of Statistics (ABS) publications Australian System of Government Finance Statistics: Concepts, Sources and Methods, 2005 (ABS Catalogue no. 5514.0) and Amendments to Australian System of Government Finance Statistics, 2005 (ABS Catalogue No. 5514.0) published on the ABS website.

entity within the GGS

A[2]

Any legal, administrative, or fiduciary arrangement, organisational structure or other party (including a person) within the GGS having the capacity to deploy scarce resources in order to achieve objectives.

General Government Sector (GGS)

A[3]

Institutional sector comprising all government units and non-profit institutions controlled and mainly financed by government. Defined in the ABS GFS Manual (Glossary, page 256).

government

A[4]

The Australian Government, the Government of the Australian Capital Territory, New South Wales, the Northern Territory, Queensland, South Australia, Tasmania, Victoria or Western Australia.

government units

A[5]

Unique kinds of legal entities established by political processes which have legislative, judicial or executive authority over other institutional units within a given area and which: (i) provide goods and services to the community and/or individuals free of charge or at prices that are not economically significant; and (ii) redistribute income and wealth by means of taxes and other compulsory transfers. Defined in the ABS GFS Manual (Glossary, page 257).

institutional unit

A[6]

An economic entity that is capable, in its own right, of owning assets, incurring liabilities and engaging in economic activities and in transactions with other entities. Defined in the ABS GFS Manual (Glossary, page 257).

non-profit institution

A[7]

A legal or social entity that is created for the purpose of producing or distributing goods and services but is not permitted to be a source of income, profit or other financial gain for the units that establish, control or finance it. Defined in the ABS GFS Manual (Glossary, page 260).

Appendix B -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusB1

Paragraphs 6–8 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Compilation details

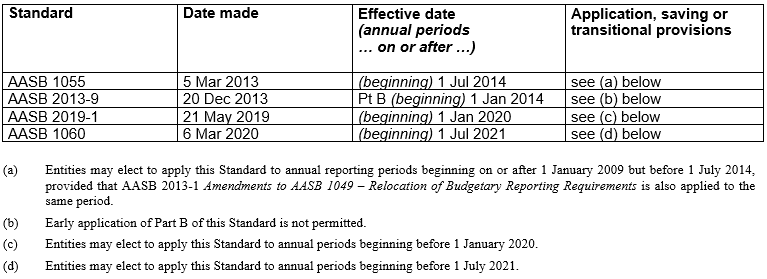

Accounting Standard AASB 1055 Budgetary Reporting (as amended)

Compilation details are not part of AASB 1055.

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1055 (March 2013) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments