The objective of this Standard is to specify principles for reporting financial information by function or activity by local governments and financial information about service costs and achievements by government departments.

Preamble

Pronouncement

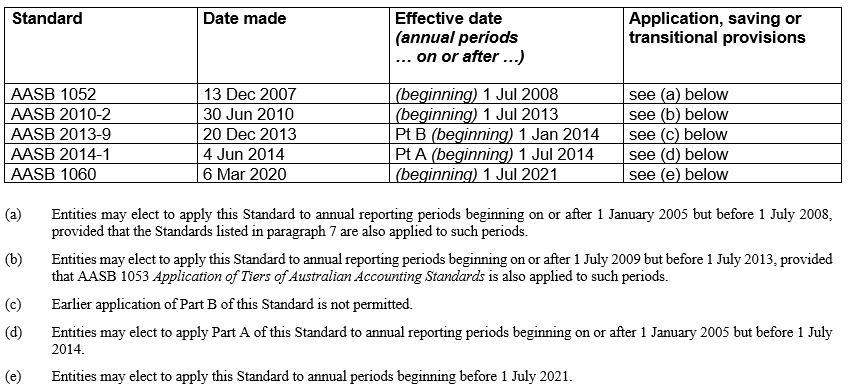

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. Earlier application is permitted for annual reporting periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1052 Disaggregated Disclosures (as amended) is set out in paragraphs 1 – 21 and Appendix B. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 1052 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with international pronouncements

This Standard contains relevant requirements relating to reporting of disaggregated information by local governments and government departments that have been relocated from AAS 27 Financial Reporting by Local Governments and AAS 29 Financial Reporting by Government Departments in substantially unamended form (with some exceptions, as noted in Appendix A). Accordingly, the development of this Standard did not involve consideration of International Public Sector Accounting Standards (IPSAS) issued by the International Public Sector Accounting Standards Board or International Financial Reporting Standards (IFRS Standards) issued by the International Accounting Standards Board.

The longer-term review of disaggregated disclosures for local governments and government departments will involve consideration of International pronouncements.

AASB 1052 and IPSAS

IPSAS 18 Segment Reporting addresses segment reporting issues and specifies requirements for all public sector entities other than government business enterprises. It contains more detailed requirements and guidance than this Standard. For example, IPSAS 18:

(a) defines a segment as a distinguishable activity or group of activities of an entity for which it is appropriate to separately report financial information for the purpose of evaluating the entity’s past performance in achieving its objectives and making decisions about the future allocation of resources;

(b) provides detailed guidance on determining segments;

(c) requires specific disclosures about segments, including segment revenue, expenses, assets, liabilities and capital expenditure; and

(d) requires assets that are jointly used by two or more segments to be allocated to segments only if their related revenues and expenses are also allocated to those segments.

AASB 1052 and IFRS Standards

IFRS 8 Operating Segments does not apply to the general purpose financial statements of local governments and government departments. IFRS 8 specifies requirements that differ substantially from the requirements in this Standard.

Accounting Standard AASB 1052

The Australian Accounting Standards Board made Accounting Standard AASB 1052 Disaggregated Disclosures on 13 December 2007.

This compiled version of AASB 1052 applies to annual reporting periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

1

The objective of this Standard is to specify principles for reporting:

(a) financial information by function or activity by local governments; and

(b) financial information about service costs and achievements by government departments.

2

Disclosures made in accordance with this Standard provide users with information relevant to assessing the performance of a local government or government department, including accountability for resources entrusted to it.

Application

3

Subject to paragraphs 4 and 5, this Standard applies to general purpose financial statements of local governments and government departments.

4

Paragraphs 11 to 14 only apply to general purpose financial statements of local governments.

5

Paragraphs 15 to 21 only apply to general purpose financial statements of government departments.

6

This Standard applies to annual reporting periods beginning on or after 1 July 2008.

[Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

7

This Standard may be applied to annual reporting periods beginning on or after 1 January 2005 but before 1 July 2008, provided there is early adoption for the same annual reporting period of the following pronouncements being issued at about the same time, as applicable:

(a) AASB 1004 Contributions;

(b) AASB 1049 Whole of Government and General Government Sector Financial Reporting;

(c) AASB 1050 Administered Items;

(d) AASB 1051 Land Under Roads;

(e) AASB 2007-9 Amendments to Australian Accounting Standards arising from the Review of AASs 27, 29 and 31; and

(f) AASB Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities.

8

This Standard does not specify disaggregated disclosure requirements for whole of governments or General Government Sectors (GGSs). The requirements for disaggregated disclosures for whole of governments and GGSs are contained in AASB 1049.

9

[Deleted by the AASB]

10

When applicable, this Standard, together with the Standards referred to in paragraph 7, supersede:

(a) AAS 27 Financial Reporting by Local Governments as issued in June 1996, as amended; and

(b) AAS 29 Financial Reporting by Government Departments as issued in June 1998, as amended.

Classification according to function or activity by local governments

Paragraphs 11 to 14 only apply to local governments.

11

The complete set of financial statements of a local government shall disclose in respect of each broad function or activity:

(a) by way of note:

(i) the nature and objectives of that function/activity; and

(ii) the carrying amount of assets that are reliably attributable to that function/activity; and

(b) by way of note or otherwise:

(i) income for the reporting period that is reliably attributable to that function/activity, with component revenues from related grants disclosed separately as a component thereof; and

(ii) expenses for the reporting period that are reliably attributable to that function/activity.

12

The information provided by way of note in accordance with paragraph 11 shall be aggregated and reconciled to agree with the related information in the financial statements of the local government.

13

This Standard requires disclosure of information about the assets, income and expenses of the local government according to the broad functions or activities of the local government, whether they be related to service delivery or undertaken for commercial objectives. Disclosure of this information assists users in identifying the resources committed to particular functions/activities of the local government, the costs of service delivery that are reliably attributable to those functions/activities, and the extent to which the local government has recovered those costs from income that is reliably attributable to those functions/activities. Function/activity classification of financial information will also assist users in assessing the significance of any financial or non-financial performance indicators reported by the local government.

14

AASB 8 Operating Segments is not applicable to local governments. The bases considered appropriate for identifying broad functions or activities of local governments would not necessarily accord with the criteria for identification of segments contained in that Standard. However, preparers of the complete set of financial statements may find that the guidance contained in that Standard is useful in identifying the income, expenses and assets that are reliably attributable to the broad functions or activities of the local government.

Disclosure of service costs and achievements by government departments

Paragraphs 15 to 21 only apply to government departments.

15

The complete set of financial statements of a government department shall disclose:

(a) in summarised form, the identity and purpose of each major activity undertaken by the government department during the reporting period;

(b) if not otherwise disclosed in, or in conjunction with, the government department’s complete set of financial statements, a summary of the government department’s objectives;

(c) expenses reliably attributable to each of the activities identified in (a) above, showing separately each major class of expenses; and

(d) income reliably attributable to each of the activities identified in (a) above, showing separately user charges, income from government and other income by major class of income.

16

The complete set of financial statements of a government department shall also disclose the assets deployed and liabilities incurred that are reliably attributable to each of the activities identified in paragraph 15(a).

17

Government departments are required to achieve service delivery as well as financial objectives. Accordingly, a government department’s performance is assessed by reference to the effectiveness, economy and efficiency with which the government department achieves its service delivery and financial objectives. Financial information is therefore only a subset of the information necessary to enable an adequate assessment of a government department’s performance. Accordingly, the complete set of financial statements is presented as part of an annual report that discloses information about such matters as the government department’s objectives and service delivery achievements during the reporting period. To enhance the quality of information available for assessing performance, paragraph 15 requires that a summary of the government department’s objectives be disclosed in the complete set of financial statements where the government department’s annual report does not include this disclosure.

18

Paragraphs 15 and 16 require disclosure of information about the expenses, income, assets and liabilities attributable to the major activities of a government department for the reporting period. This information is relevant in assessing the effectiveness, efficiency and economy of operations and of resource allocation decisions. It is also necessary for reviewing existing expenditure commitments and service delivery arrangements, and for considering the long-term funding implications of new initiatives.

19

However, in some instances it may not be possible to reliably attribute all expenses, income, assets and liabilities to each of the major activities of a government department. Paragraphs 15 and 16 require that the complete set of financial statements of a government department only disclose, on an activity by activity basis, information about the expenses, income, assets and liabilities that can be reliably attributed to major activities.

Identifying major activities of government departments

20

Judgement is required to identify those activities of a government department that warrant separate disclosure in the complete set of financial statements. Exercising this judgement involves a consideration of the following:

(a) the objectives of the government department;

(b) the likely users of the general purpose financial statements;

(c) the activity level that may be relevant to users’ assessments of the performance of the government department; and

(d) the concept of materiality. AASB 101 Presentation of Financial Statements and AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors define an item as material if its omission or misstatement could influence the economic decisions of users of the financial statements.

Appendix A -- Comparison of AASB 1052 with AASs 27 and 29

This Appendix accompanies, but is not part of, AASB 1052.

This Standard reproduces the material relating to disaggregated disclosures contained in AAS 27 and AAS 29, except that:

(a) Appendix 1 to AAS 27 contained an illustrative example of the disclosures required in respect of the broad functions/activities of a local government. This Standard does not provide an illustration;

(b) AAS 29 (paragraph 12.7.2) encouraged a government department to disclose the assets deployed and liabilities incurred that are reliably attributable to each of its activities. This Standard (paragraph 16) requires such disclosure; and

(c) this Standard (paragraph 21) notes that its principles are used in satisfying the requirement in AASB 1050 Administered Items to disclose administered income and expenses attributable to a government department’s activities. AASs 27 and 29 contained no such reference.

The following table provides source references to paragraphs 11–21 of this Standard, most of which were derived from AASs 27 and 29. It is provided to facilitate an understanding of, and assist in the application of, the requirements in this Standard.

|

Paragraph in AASB 1052 |

Relevant source paragraphs in AASs 27 & 29 |

|

86–89 of AAS 27 |

|

|

12.7–12.7.4 of AAS 29 |

|

|

New paragraph |

Appendix B -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusB1

Paragraphs 15–21 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Compilation details

Accounting Standard AASB 1052 Disaggregated Disclosures (as amended)

Compilation details are not part of AASB 1052.

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1052 (December 2007) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments