The objective of this Standard is to provide an up-to-date listing of Australian Interpretations and to ensure the effectiveness of references in Australian Accounting Standards to Australian Interpretations and to the Framework for the Preparation and Presentation of Financial Statements and the Conceptual Framework for Financial Reporting.

Preamble

Pronouncement

Obtaining a copy of this Accounting Standard

This Standard is available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2024

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgement of the source. Requests and enquiries concerning reproduction and rights should be addressed to The Managing Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1048 Interpretation of Standards is set out in paragraphs 1–13. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 1048 is to be read in the context of other Australian Accounting Standards, including AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Preface

Introduction

The Australian Accounting Standards Board (AASB) is an Australian Government entity under the Australian Securities and Investments Commission Act 2001. The AASB develops, issues and maintains Australian Accounting Standards, including Interpretations. These are to be applied by:

(a) entities required by the Corporations Act 2001 to prepare financial reports;

(b) governments in preparing financial statements for the whole of government and the General Government Sector (GGS); and

(c) entities in the private or public for-profit or not-for-profit sectors that are reporting entities or that prepare general purpose financial statements.

AASB 1053 Application of Tiers of Australian Accounting Standards establishes a differential reporting framework consisting of two tiers of reporting requirements for preparing general purpose financial statements:

(a) Tier 1: Australian Accounting Standards; and

(b) Tier 2: Australian Accounting Standards – Simplified Disclosures.

What does this Standard require?

This Standard identifies the Australian Interpretations and classifies them into two groups: those that correspond to an International Accounting Standards Board (IASB) Interpretation and those that do not. Entities are required to apply each relevant Australian Interpretation in preparing financial statements that are within the scope of the Standard.

In respect of the first group (Table 1), it is necessary for those Australian Interpretations, where relevant, to be applied in order for an entity to be able to make an explicit and unreserved statement of compliance with International Financial Reporting Standards (IFRS Accounting Standards). The IASB defines IFRS Accounting Standards to include both IFRIC and SIC Interpretations.

In the second group (Table 2), this Standard lists the other Australian Interpretations, which do not correspond to the IASB Interpretations, to assist financial statement preparers and users to identify the other authoritative pronouncements necessary for compliance in the Australian context.

This Standard (see Tables 3 and AusCF3) also updates references to conceptual framework pronouncements in other Standards to refer to amended versions of the pronouncements, as identified in this Standard.

The Standard will be reissued or amended when necessary to keep the Tables up to date.

When does it apply?

This Standard is applicable to annual reporting periods ending on or after 31 December 2024 (see paragraph 2). Earlier application is permitted as specified in paragraph 3, subject to paragraphs 7, 9, 11 and AusCF11 of this Standard.

What are the changes?

This Standard (issued in November 2024) supersedes the previous version of AASB 1048, issued in December 2020.

The main differences between the previous version and this version include:

(a) the removal from the tables of versions of Interpretations and conceptual framework pronouncements that do not apply to any of the reporting periods to which this Standard mandatorily applies (see paragraph 2), including Interpretation 1047 Professional Indemnity Claims Liabilities in Medical Defence Organisations, which has been superseded by AASB 17 Insurance Contracts;

(b) the addition of amended versions of Interpretations in Tables 1 and 2, where applicable to any reporting period to which this Standard mandatorily applies. This reflects amended versions of Interpretations arising as a result of the consequential amendments in Appendix D of AASB 18 Presentation and Disclosure in Financial Statements and the editorial corrections set out in AASB 2021-7 Amendments to Australian Accounting Standards – Effective Date of Amendments to AASB 10 and AASB 128 and Editorial Corrections; and

(c) the addition of an amended version of the Conceptual Framework for Financial Reporting in Table 3 as a result of an editorial correction set out in AASB 2021-7.

Why have we issued this Standard?

This Standard clarifies that all Australian Interpretations have the same authoritative status. Those that incorporate the IASB Interpretations must be applied to achieve compliance with IFRS Accounting Standards. Australian Interpretations issued by the AASB comprise both AASB and UIG Interpretations. UIG Interpretations were developed by the Urgent Issues Group, a former committee of the AASB.

This Standard also updates references in other Standards to the Conceptual Framework for Financial Reporting and the Framework for the Preparation and Presentation of Financial Statements to subsequent versions.

Need for a Service Standard

Australian Interpretations

In the Australian context, Australian Interpretations do not have the same legal status as Standards (delegated legislation) and are treated as ‘external documents’ by the Acts Interpretation Act 1901 and the Legislation Act 2003. Although references in one Standard to a second Standard are ambulatory (automatically moving forward to refer to the most recently-issued version of the second Standard), references in a Standard to external documents are stationary (being fixed in time to refer to the contents of the external document when the Standard was issued). A simple reference to an Australian Interpretation in a Standard can refer only to the Interpretation that existed when the Standard was issued. It cannot refer to any revised version of the Interpretation that may exist at a later reporting date. However, a Standard can refer to a second Standard and, when the first Standard is applied at a later reporting date, the reference will be to the then-current version of the second Standard, even if it has been reissued since the first Standard was issued.

The service Standard approach, as applied to Australian Interpretations, involves issuing this Standard to list the versions of Australian Interpretations, and referring to this Standard in every other Standard where necessary to refer to an Interpretation. This enables references to the Interpretations in all other Standards to be updated by reissuing the service Standard.

This approach preserves the status of Australian Interpretations as ‘external documents’ referred to in a Standard. It does not treat the Interpretations as delegated legislation or confer ambulatory status on the reference. In each Standard where there is a need to refer to an Australian Interpretation, the reference will be to this Standard, phrased as “Interpretation [number] [title] as identified in AASB 1048” (or similar). This reference, being to another Standard, is ambulatory and will refer to the version of this Standard that is in force from time to time. AASB 1048 itself will contain the direct references to the external documents and will be reissued periodically.

This approach to clarifying the status of Australian Interpretations ensures there is no difference between the status in the hierarchy accorded to Interpretations in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors compared with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors.

Australian conceptual framework

In the Australian context, an Australian conceptual framework pronouncement, such as the Conceptual Framework for Financial Reporting and the Framework for the Preparation and Presentation of Financial Statements, also does not have the same legal status as a Standard (delegated legislation) and, like Interpretations, is treated as an ‘external document’ by the Acts Interpretation Act 1901 and the Legislation Act 2003.

The service Standard approach, as applied to the Australian conceptual framework, involves issuing this Standard to update references to conceptual framework pronouncements in other Standards. This approach preserves the status of such pronouncements as ‘external documents’ referred to in a Standard. It does not treat the pronouncements as delegated legislation or confer ambulatory status on the reference.

Comparison with international pronouncements

There is no International Accounting Standards Board (IASB) Standard that directly corresponds to AASB 1048. However, Table 1 in AASB 1048 (see paragraph 6) contains a list of Australian Interpretations identifying the corresponding IASB Interpretations.

Tier 1

For-profit entities complying with the Australian Interpretations designated in this Standard as corresponding to the IASB Interpretations also comply with the Interpretations referred to by the IASB in its definition of International Financial Reporting Standards (IFRS Accounting Standards).

Not-for-profit entities’ compliance with IASB Interpretations will depend on whether any “Aus” paragraphs or Interpretations that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IASB Interpretations.

Tier 2

Entities preparing general purpose financial statements under Australian Accounting Standards – Simplified Disclosures (Tier 2) will not be in compliance with all IASB Interpretations.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Conceptual frameworks

In relation to references to the Conceptual Framework for Financial Reporting and the Framework for the Preparation and Presentation of Financial Statements in other Standards, the approach taken in this Standard to clarifying the applicable framework pronouncement ensures there is no difference between the version of the conceptual framework referred to in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors and in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, and in other Standards.

Accounting Standard AASB 1048

The Australian Accounting Standards Board makes Accounting Standard AASB 1048 Interpretation of Standards (November 2024) under section 334 of the Corporations Act 2001.

Keith Kendall

Chair – AASB

Dated 7 November 2024

Objective

1

The objective of this Standard is to provide an up-to-date listing of Australian Interpretations and conceptual framework pronouncements to ensure the effectiveness of references in Australian Accounting Standards to Australian Interpretations and to the Framework for the Preparation and Presentation of Financial Statements (Framework) and the Conceptual Framework for Financial Reporting (Conceptual Framework). AASB and UIG Interpretations are referred to collectively in this Standard as Australian Interpretations.

AusCF1

AusCF paragraphs included in this Standard apply only to:

(a) not-for-profit entities; and

(b) for-profit entities that are not applying the Conceptual Framework for Financial Reporting (as identified in this Standard).

Such entities are referred to as ‘AusCF entities’. For AusCF entities, the term ‘reporting entity’ is defined in AASB 1057 Application of Australian Accounting Standards and Statement of Accounting Concepts SAC 1 Definition of the Reporting Entity also applies. For-profit entities applying the Conceptual Framework for Financial Reporting (as set out in paragraph Aus1.1 of the Conceptual Framework) shall not apply AusCF paragraphs.

Interpretations

4

This Standard refers to all Australian Interpretations currently approved by the AASB and applicable to any period[1] specified in paragraph 2 (by either mandatory or early application), classified according to whether they correspond to Interpretations adopted by the International Accounting Standards Board (IASB).

Periods no longer than 18 months.

5

For ease of presentation, the Australian Interpretations are set out in two separate tables: in paragraph 6, Table 1 lists those corresponding to IASB Interpretations and, in paragraph 8, Table 2 lists the other Interpretations. Each row in each of the Tables 1 and 2 is to be treated as a separate provision of this Standard.

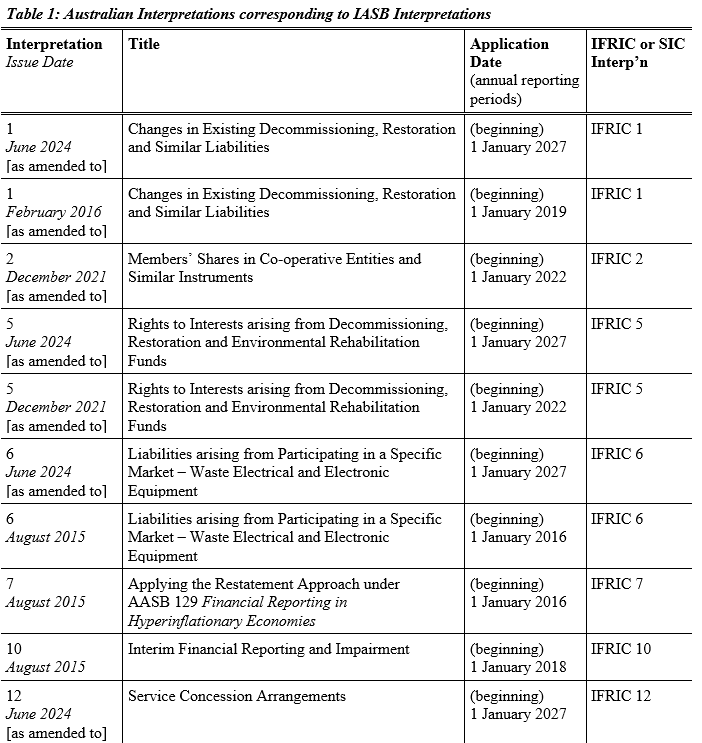

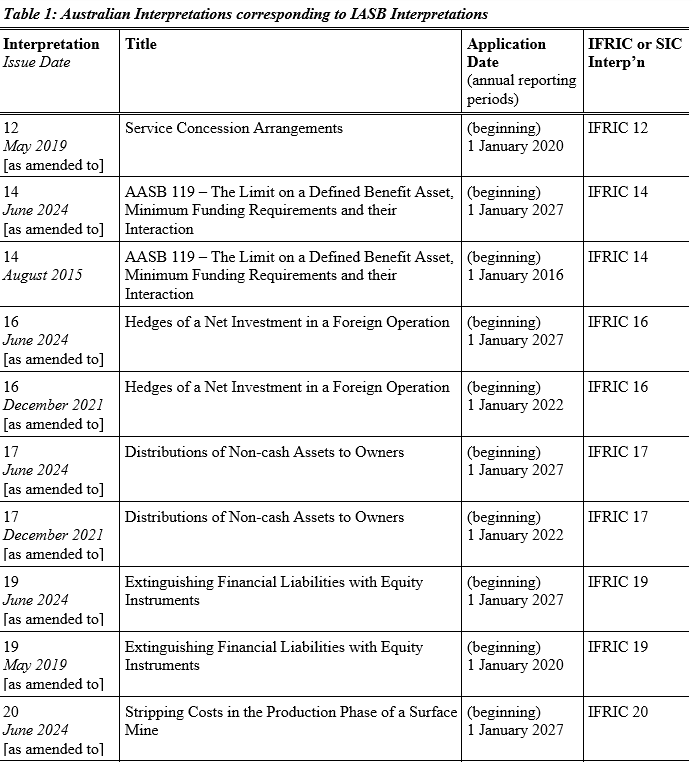

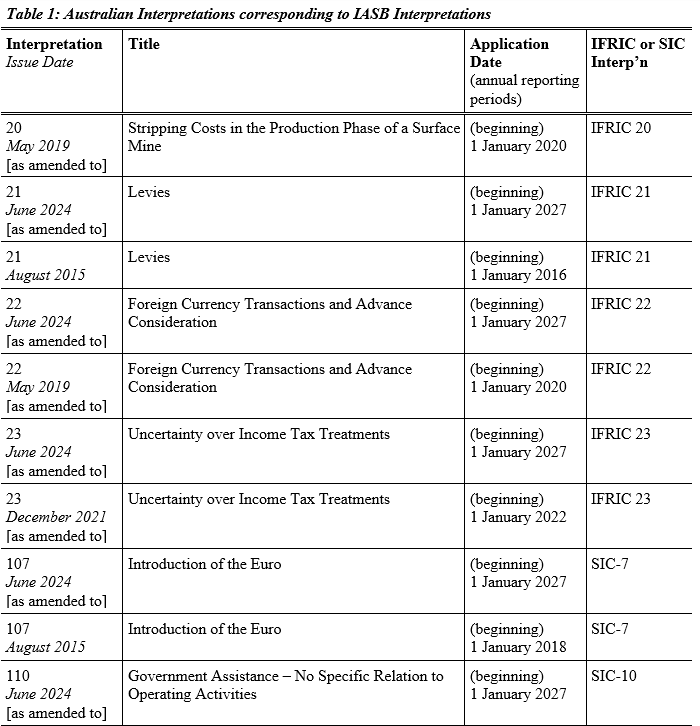

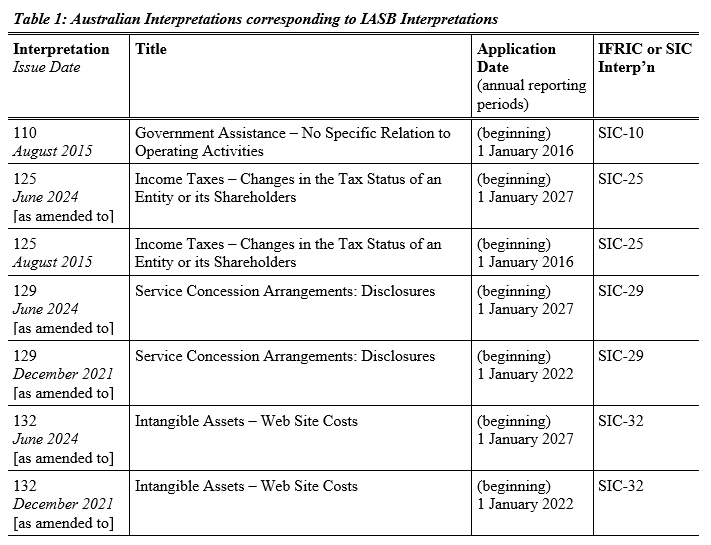

Australian Interpretations corresponding to IASB Interpretations

6

An entity shall apply each relevant Australian Interpretation listed in Table 1 below.

7

The principal application date listed in Table 1 for each Interpretation is a reference to annual reporting periods beginning or ending (as indicated) on or after the date specified. An entity may elect to apply an individual Interpretation to annual reporting periods in advance of that stated for the Interpretation in Table 1, subject to any early application requirements of the Interpretation.

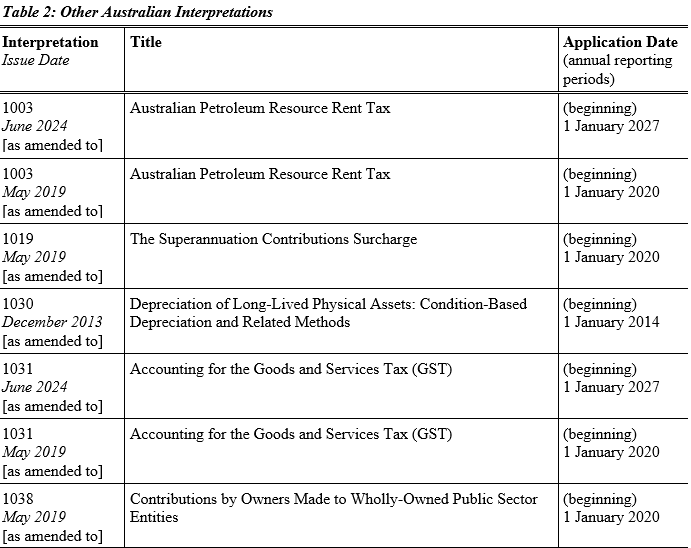

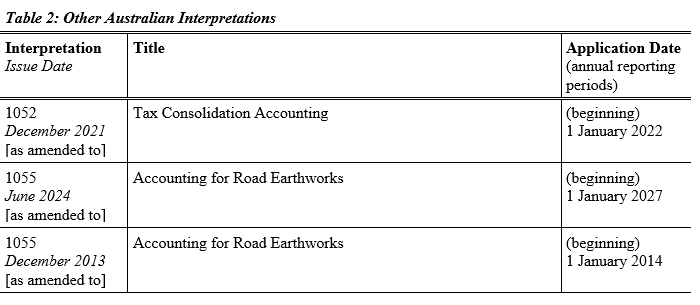

Other Australian Interpretations

8

An entity shall apply each relevant Australian Interpretation listed in Table 2 below.

9

The principal application date listed in Table 2 for each Interpretation is a reference to annual reporting periods beginning or ending (as indicated) on or after the date specified. An entity may elect to apply an individual Interpretation to annual reporting periods in advance of that stated for the Interpretation in Table 2, subject to any early application requirements of the Interpretation.

Conceptual framework

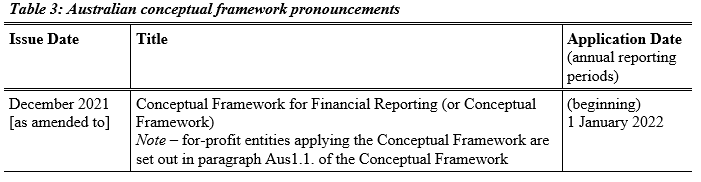

10

Each reference to the Conceptual Framework for Financial Reporting (or Conceptual Framework) in other Australian Accounting Standards (including Interpretations) is taken to be a reference to the relevant pronouncement listed in Table 3 below. Each row in Table 3 is to be treated as a separate provision of this Standard.

AusCF10

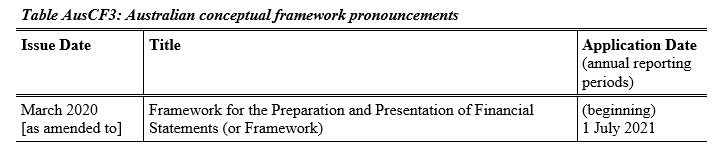

Notwithstanding paragraph 10, in respect of AusCF entities, each reference to the Framework for the Preparation and Presentation of Financial Statements (or Framework) in other Australian Accounting Standards (including Interpretations) is taken to be a reference to the relevant pronouncement listed in Table AusCF3 below. Each row in Table AusCF3 is to be treated as a separate provision of this Standard.

11

This Standard updates references to the Conceptual Framework in Australian Accounting Standards (including Interpretations) to the relevant amended version of the Conceptual Framework. The principal application date listed in each row of Table 3 is a reference to annual reporting periods beginning or ending (as indicated) on or after the date specified. An entity may elect to apply an amended version of the pronouncement to annual reporting periods in advance of that stated in Table 3, subject to any early application paragraphs.

AusCF11

Notwithstanding paragraph 11, in respect of AusCF entities, this Standard updates references to the Framework in Australian Accounting Standards (including Interpretations) to the relevant amended version of the Framework. The principal application date listed in each row of Table AusCF3 is a reference to annual reporting periods beginning or ending (as indicated) on or after the date specified. An entity may elect to apply an amended version of the pronouncement to annual reporting periods in advance of that stated in Table AusCF3, subject to any early application paragraphs.

Withdrawal of AASB pronouncements

13

This Standard repeals AASB 1048 Interpretation of Standards issued in December 2020. Despite the repeal, after the time this Standard starts to apply under section 334 of the Corporations Act (either generally or in relation to an individual entity), the repealed Standard continues to apply in relation to any period ending before that time as if the repeal had not occurred.

[Note: When this Standard applies under section 334 of the Corporations Act (either generally or in relation to an individual entity), it supersedes the application of the repealed Standard.]