Interpretations

4

This Standard refers to all Australian Interpretations currently approved by the AASB and applicable to any period[1] specified in paragraph 2 (by either mandatory or early application), classified according to whether they correspond to Interpretations adopted by the International Accounting Standards Board (IASB).

Periods no longer than 18 months.

5

For ease of presentation, the Australian Interpretations are set out in two separate tables: in paragraph 6, Table 1 lists those corresponding to IASB Interpretations and, in paragraph 8, Table 2 lists the other Interpretations. Each row in each of the Tables 1 and 2 is to be treated as a separate provision of this Standard.

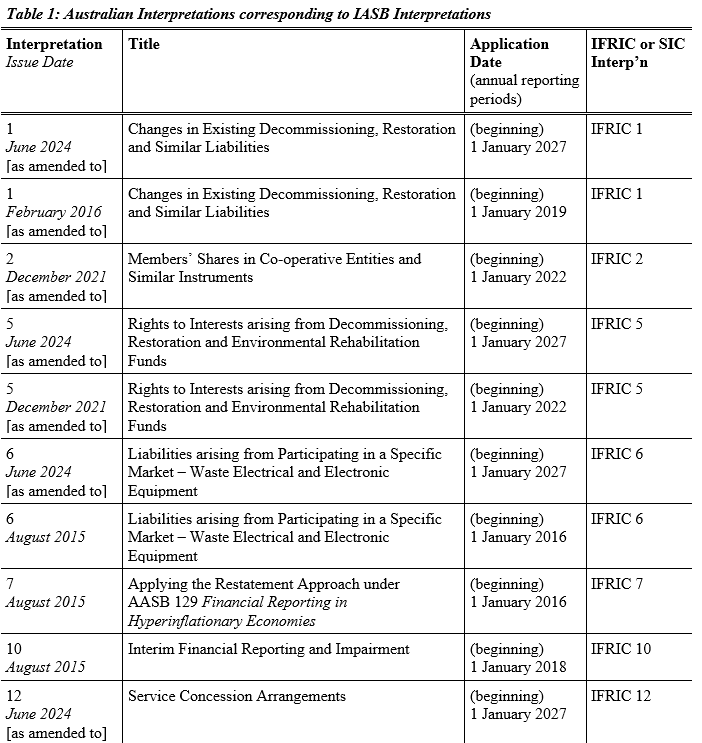

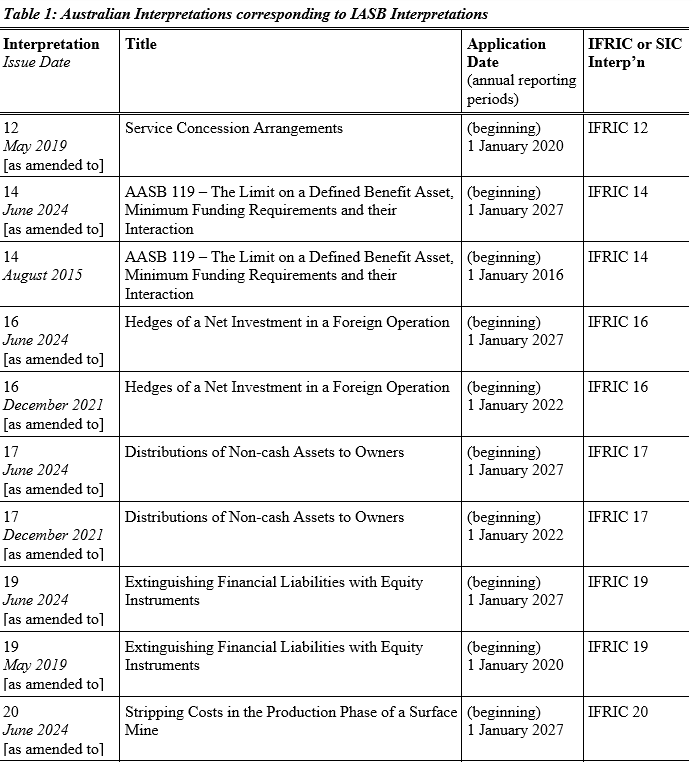

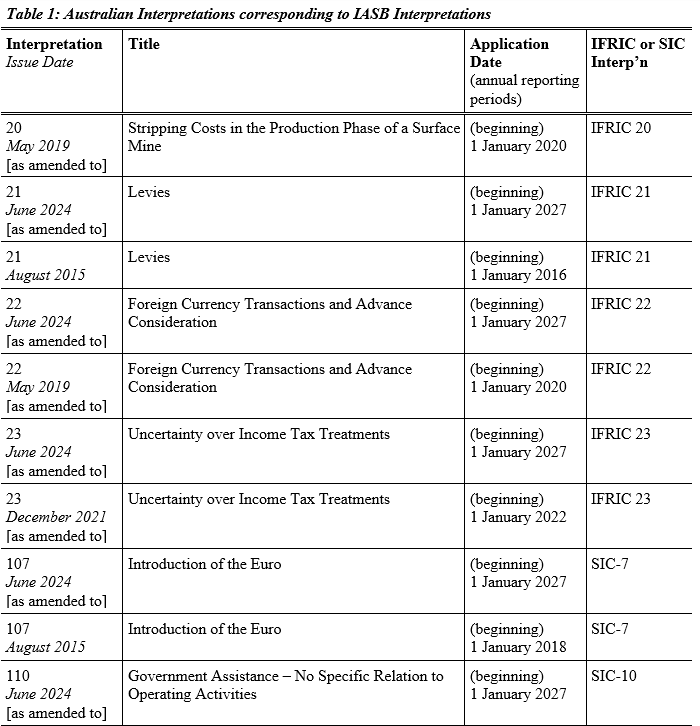

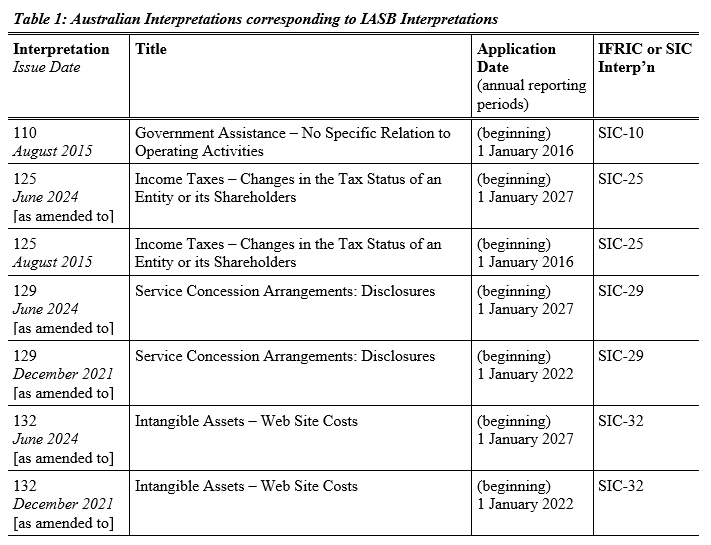

Australian Interpretations corresponding to IASB Interpretations

6

An entity shall apply each relevant Australian Interpretation listed in Table 1 below.

7

The principal application date listed in Table 1 for each Interpretation is a reference to annual reporting periods beginning or ending (as indicated) on or after the date specified. An entity may elect to apply an individual Interpretation to annual reporting periods in advance of that stated for the Interpretation in Table 1, subject to any early application requirements of the Interpretation.

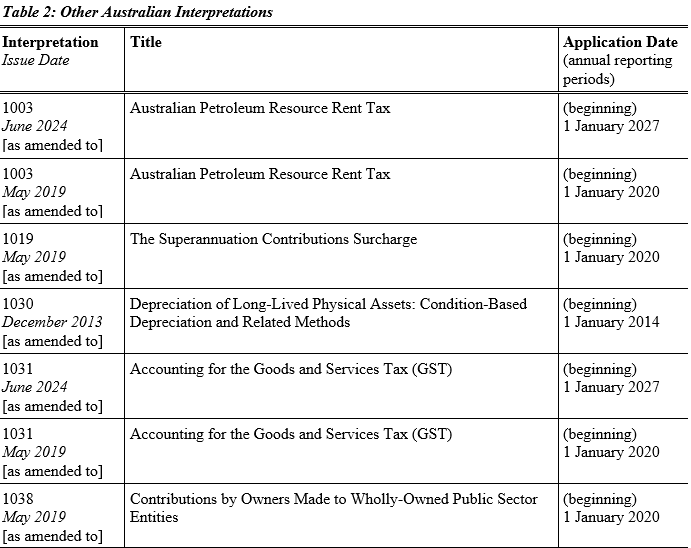

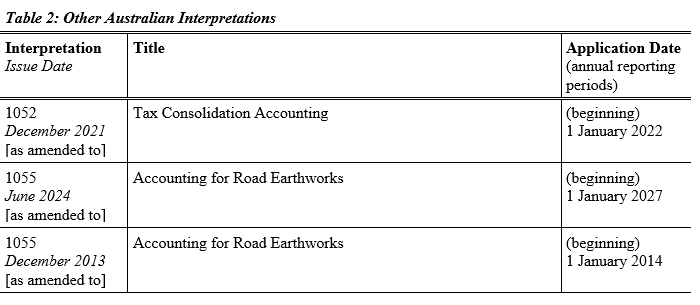

Other Australian Interpretations

8

An entity shall apply each relevant Australian Interpretation listed in Table 2 below.

9

The principal application date listed in Table 2 for each Interpretation is a reference to annual reporting periods beginning or ending (as indicated) on or after the date specified. An entity may elect to apply an individual Interpretation to annual reporting periods in advance of that stated for the Interpretation in Table 2, subject to any early application requirements of the Interpretation.