Appendix B -- Application guidance

Portfolio application

B1

This Standard specifies the accounting for an individual lease. However, as a practical expedient, an entity may apply this Standard to a portfolio of leases with similar characteristics if the entity reasonably expects that the effects on the financial statements of applying this Standard to the portfolio would not differ materially from applying this Standard to the individual leases within that portfolio. If accounting for a portfolio, an entity shall use estimates and assumptions that reflect the size and composition of the portfolio.

Combination of contracts

B2

In applying this Standard, an entity shall combine two or more contracts entered into at or near the same time with the same counterparty (or related parties of the counterparty), and account for the contracts as a single contract if one or more of the following criteria are met:

(a) the contracts are negotiated as a package with an overall commercial objective that cannot be understood without considering the contracts together;

(b) the amount of consideration to be paid in one contract depends on the price or performance of the other contract; or

(c) the rights to use underlying assets conveyed in the contracts (or some rights to use underlying assets conveyed in each of the contracts) form a single lease component as described in paragraph B32.

Recognition exemption: leases for which the underlying asset is of low value (paragraphs 5–8)

B3

Except as specified in paragraph B7, this Standard permits a lessee to apply paragraph 6 to account for leases for which the underlying asset is of low value. A lessee shall assess the value of an underlying asset based on the value of the asset when it is new, regardless of the age of the asset being leased.

B4

The assessment of whether an underlying asset is of low value is performed on an absolute basis. Leases of low-value assets qualify for the accounting treatment in paragraph 6 regardless of whether those leases are material to the lessee. The assessment is not affected by the size, nature or circumstances of the lessee. Accordingly, different lessees are expected to reach the same conclusions about whether a particular underlying asset is of low value.

B5

An underlying asset can be of low value only if:

(a) the lessee can benefit from use of the underlying asset on its own or together with other resources that are readily available to the lessee; and

(b) the underlying asset is not highly dependent on, or highly interrelated with, other assets.

B6

A lease of an underlying asset does not qualify as a lease of a low-value asset if the nature of the asset is such that, when new, the asset is typically not of low value. For example, leases of cars would not qualify as leases of low-value assets because a new car would typically not be of low value.

B7

If a lessee subleases an asset, or expects to sublease an asset, the head lease does not qualify as a lease of a low-value asset.

B8

Examples of low-value underlying assets can include tablet and personal computers, small items of office furniture and telephones.

Identifying a lease (paragraphs 9–11)

B9

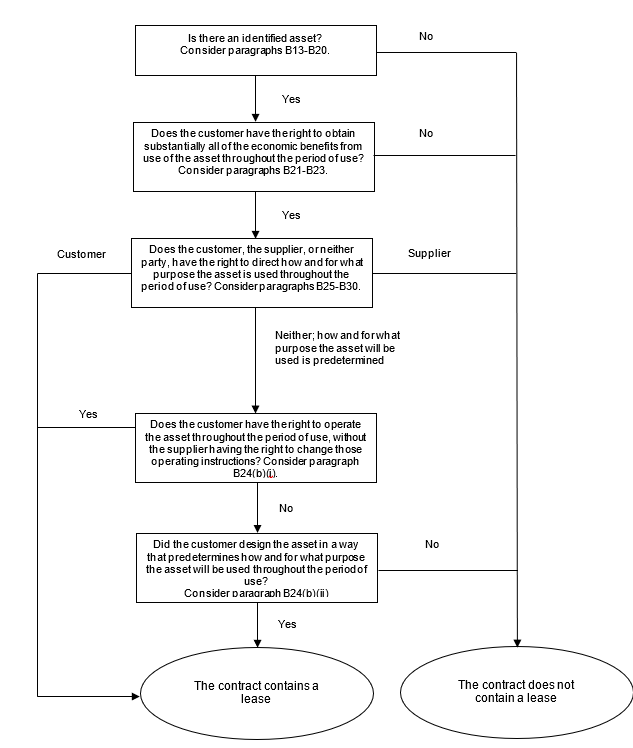

To assess whether a contract conveys the right to control the use of an identified asset (see paragraphs B13–B20) for a period of time, an entity shall assess whether, throughout the period of use, the customer has both of the following:

(a) the right to obtain substantially all of the economic benefits from use of the identified asset (as described in paragraphs B21–B23); and

(b) the right to direct the use of the identified asset (as described in paragraphs B24–B30).

B10

If the customer has the right to control the use of an identified asset for only a portion of the term of the contract, the contract contains a lease for that portion of the term.

B11

A contract to receive goods or services may be entered into by a joint arrangement, or on behalf of a joint arrangement, as defined in AASB 11 Joint Arrangements. In this case, the joint arrangement is considered to be the customer in the contract. Accordingly, in assessing whether such a contract contains a lease, an entity shall assess whether the joint arrangement has the right to control the use of an identified asset throughout the period of use.

B12

An entity shall assess whether a contract contains a lease for each potential separate lease component. Refer to paragraph B32 for guidance on separate lease components.

Identified asset

B13

An asset is typically identified by being explicitly specified in a contract. However, an asset can also be identified by being implicitly specified at the time that the asset is made available for use by the customer.

Substantive substitution rights

B14

Even if an asset is specified, a customer does not have the right to use an identified asset if the supplier has the substantive right to substitute the asset throughout the period of use. A supplier’s right to substitute an asset is substantive only if both of the following conditions exist:

(a) the supplier has the practical ability to substitute alternative assets throughout the period of use (for example, the customer cannot prevent the supplier from substituting the asset and alternative assets are readily available to the supplier or could be sourced by the supplier within a reasonable period of time); and

(b) the supplier would benefit economically from the exercise of its right to substitute the asset (ie the economic benefits associated with substituting the asset are expected to exceed the costs associated with substituting the asset).

B14

Even if an asset is specified, a customer does not have the right to use an identified asset if the supplier has the substantive right to substitute the asset throughout the period of use. A supplier’s right to substitute an asset is substantive only if both of the following conditions exist:

(a) the supplier has the practical ability to substitute alternative assets throughout the period of use (for example, the customer cannot prevent the supplier from substituting the asset and alternative assets are readily available to the supplier or could be sourced by the supplier within a reasonable period of time); and

(b) the supplier would benefit economically from the exercise of its right to substitute the asset (ie the economic benefits associated with substituting the asset are expected to exceed the costs associated with substituting the asset).

B15

If the supplier has a right or an obligation to substitute the asset only on or after either a particular date or the occurrence of a specified event, the supplier’s substitution right is not substantive because the supplier does not have the practical ability to substitute alternative assets throughout the period of use.

B16

An entity’s evaluation of whether a supplier’s substitution right is substantive is based on facts and circumstances at inception of the contract and shall exclude consideration of future events that, at inception of the contract, are not considered likely to occur. Examples of future events that, at inception of the contract, would not be considered likely to occur and, thus, should be excluded from the evaluation include:

(a) an agreement by a future customer to pay an above market rate for use of the asset;

(b) the introduction of new technology that is not substantially developed at inception of the contract;

(c) a substantial difference between the customer’s use of the asset, or the performance of the asset, and the use or performance considered likely at inception of the contract; and

(d) a substantial difference between the market price of the asset during the period of use, and the market price considered likely at inception of the contract.

B17

If the asset is located at the customer’s premises or elsewhere, the costs associated with substitution are generally higher than when located at the supplier’s premises and, therefore, are more likely to exceed the benefits associated with substituting the asset.

B18

The supplier’s right or obligation to substitute the asset for repairs and maintenance, if the asset is not operating properly or if a technical upgrade becomes available does not preclude the customer from having the right to use an identified asset.

B19

If the customer cannot readily determine whether the supplier has a substantive substitution right, the customer shall presume that any substitution right is not substantive.

Portions of assets

B20

A capacity portion of an asset is an identified asset if it is physically distinct (for example, a floor of a building). A capacity or other portion of an asset that is not physically distinct (for example, a capacity portion of a fibre optic cable) is not an identified asset, unless it represents substantially all of the capacity of the asset and thereby provides the customer with the right to obtain substantially all of the economic benefits from use of the asset.

B20

A capacity portion of an asset is an identified asset if it is physically distinct (for example, a floor of a building). A capacity or other portion of an asset that is not physically distinct (for example, a capacity portion of a fibre optic cable) is not an identified asset, unless it represents substantially all of the capacity of the asset and thereby provides the customer with the right to obtain substantially all of the economic benefits from use of the asset.

Right to obtain economic benefits from use

B21

To control the use of an identified asset, a customer is required to have the right to obtain substantially all of the economic benefits from use of the asset throughout the period of use (for example, by having exclusive use of the asset throughout that period). A customer can obtain economic benefits from use of an asset directly or indirectly in many ways, such as by using, holding or sub-leasing the asset. The economic benefits from use of an asset include its primary output and by-products (including potential cash flows derived from these items), and other economic benefits from using the asset that could be realised from a commercial transaction with a third party.

B22

When assessing the right to obtain substantially all of the economic benefits from use of an asset, an entity shall consider the economic benefits that result from use of the asset within the defined scope of a customer’s right to use the asset (see paragraph B30). For example:

(a) if a contract limits the use of a motor vehicle to only one particular territory during the period of use, an entity shall consider only the economic benefits from use of the motor vehicle within that territory, and not beyond.

(b) if a contract specifies that a customer can drive a motor vehicle only up to a particular number of miles during the period of use, an entity shall consider only the economic benefits from use of the motor vehicle for the permitted mileage, and not beyond.

B23

If a contract requires a customer to pay the supplier or another party a portion of the cash flows derived from use of an asset as consideration, those cash flows paid as consideration shall be considered to be part of the economic benefits that the customer obtains from use of the asset. For example, if the customer is required to pay the supplier a percentage of sales from use of retail space as consideration for that use, that requirement does not prevent the customer from having the right to obtain substantially all of the economic benefits from use of the retail space. This is because the cash flows arising from those sales are considered to be economic benefits that the customer obtains from use of the retail space, a portion of which it then pays to the supplier as consideration for the right to use that space.

Right to direct the use

B24

A customer has the right to direct the use of an identified asset throughout the period of use only if either:

(a) the customer has the right to direct how and for what purpose the asset is used throughout the period of use (as described in paragraphs B25–B30); or

(b) the relevant decisions about how and for what purpose the asset is used are predetermined and:

(i) the customer has the right to operate the asset (or to direct others to operate the asset in a manner that it determines) throughout the period of use, without the supplier having the right to change those operating instructions; or

(ii) the customer designed the asset (or specific aspects of the asset) in a way that predetermines how and for what purpose the asset will be used throughout the period of use.

How and for what purpose the asset is used

B25

A customer has the right to direct how and for what purpose the asset is used if, within the scope of its right of use defined in the contract, it can change how and for what purpose the asset is used throughout the period of use. In making this assessment, an entity considers the decision-making rights that are most relevant to changing how and for what purpose the asset is used throughout the period of use. Decision-making rights are relevant when they affect the economic benefits to be derived from use. The decision-making rights that are most relevant are likely to be different for different contracts, depending on the nature of the asset and the terms and conditions of the contract.

B25

A customer has the right to direct how and for what purpose the asset is used if, within the scope of its right of use defined in the contract, it can change how and for what purpose the asset is used throughout the period of use. In making this assessment, an entity considers the decision-making rights that are most relevant to changing how and for what purpose the asset is used throughout the period of use. Decision-making rights are relevant when they affect the economic benefits to be derived from use. The decision-making rights that are most relevant are likely to be different for different contracts, depending on the nature of the asset and the terms and conditions of the contract.

B26

Examples of decision-making rights that, depending on the circumstances, grant the right to change how and for what purpose the asset is used, within the defined scope of the customer’s right of use, include:

(a) rights to change the type of output that is produced by the asset (for example, to decide whether to use a shipping container to transport goods or for storage, or to decide upon the mix of products sold from retail space);

(b) rights to change when the output is produced (for example, to decide when an item of machinery or a power plant will be used);

(c) rights to change where the output is produced (for example, to decide upon the destination of a truck or a ship, or to decide where an item of equipment is used); and

(d) rights to change whether the output is produced, and the quantity of that output (for example, to decide whether to produce energy from a power plant and how much energy to produce from that power plant).

B27

Examples of decision-making rights that do not grant the right to change how and for what purpose the asset is used include rights that are limited to operating or maintaining the asset. Such rights can be held by the customer or the supplier. Although rights such as those to operate or maintain an asset are often essential to the efficient use of an asset, they are not rights to direct how and for what purpose the asset is used and are often dependent on the decisions about how and for what purpose the asset is used. However, rights to operate an asset may grant the customer the right to direct the use of the asset if the relevant decisions about how and for what purpose the asset is used are predetermined (see paragraph B24(b)(i)).

Decisions determined during and before the period of use

B28

The relevant decisions about how and for what purpose the asset is used can be predetermined in a number of ways. For example, the relevant decisions can be predetermined by the design of the asset or by contractual restrictions on the use of the asset.

B29

In assessing whether a customer has the right to direct the use of an asset, an entity shall consider only rights to make decisions about the use of the asset during the period of use, unless the customer designed the asset (or specific aspects of the asset) as described in paragraph B24(b)(ii). Consequently, unless the conditions in paragraph B24(b)(ii) exist, an entity shall not consider decisions that are predetermined before the period of use. For example, if a customer is able only to specify the output of an asset before the period of use, the customer does not have the right to direct the use of that asset. The ability to specify the output in a contract before the period of use, without any other decision-making rights relating to the use of the asset, gives a customer the same rights as any customer that purchases goods or services.

Protective Rights

B30

A contract may include terms and conditions designed to protect the supplier’s interest in the asset or other assets, to protect its personnel, or to ensure the supplier’s compliance with laws or regulations. These are examples of protective rights. For example, a contract may (i) specify the maximum amount of use of an asset or limit where or when the customer can use the asset, (ii) require a customer to follow particular operating practices, or (iii) require a customer to inform the supplier of changes in how an asset will be used. Protective rights typically define the scope of the customer’s right of use but do not, in isolation, prevent the customer from having the right to direct the use of an asset.

B31

The following flowchart may assist entities in making the assessment of whether a contract is, or contains, a lease.

Separating components of a contract (paragraphs 12–17)

B32

The right to use an underlying asset is a separate lease component if both:

(a) the lessee can benefit from use of the underlying asset either on its own or together with other resources that are readily available to the lessee. Readily available resources are goods or services that are sold or leased separately (by the lessor or other suppliers) or resources that the lessee has already obtained (from the lessor or from other transactions or events); and

(b) the underlying asset is neither highly dependent on, nor highly interrelated with, the other underlying assets in the contract. For example, the fact that a lessee could decide not to lease the underlying asset without significantly affecting its rights to use other underlying assets in the contract might indicate that the underlying asset is not highly dependent on, or highly interrelated with, those other underlying assets.

B33

A contract may include an amount payable by the lessee for activities and costs that do not transfer a good or service to the lessee. For example, a lessor may include in the total amount payable a charge for administrative tasks, or other costs it incurs associated with the lease, that do not transfer a good or service to the lessee. Such amounts payable do not give rise to a separate component of the contract, but are considered to be part of the total consideration that is allocated to the separately identified components of the contract.

Lease term (paragraphs 18–21)

B34

In determining the lease term and assessing the length of the non-cancellable period of a lease, an entity shall apply the definition of a contract and determine the period for which the contract is enforceable. A lease is no longer enforceable when the lessee and the lessor each has the right to terminate the lease without permission from the other party with no more than an insignificant penalty.

B35

If only a lessee has the right to terminate a lease, that right is considered to be an option to terminate the lease available to the lessee that an entity considers when determining the lease term. If only a lessor has the right to terminate a lease, the non-cancellable period of the lease includes the period covered by the option to terminate the lease.

B36

The lease term begins at the commencement date and includes any rent-free periods provided to the lessee by the lessor.

B37

At the commencement date, an entity assesses whether the lessee is reasonably certain to exercise an option to extend the lease or to purchase the underlying asset, or not to exercise an option to terminate the lease. The entity considers all relevant facts and circumstances that create an economic incentive for the lessee to exercise, or not to exercise, the option, including any expected changes in facts and circumstances from the commencement date until the exercise date of the option. Examples of factors to consider include, but are not limited to:

(a) contractual terms and conditions for the optional periods compared with market rates, such as:

(i) the amount of payments for the lease in any optional period;

(ii) the amount of any variable payments for the lease or other contingent payments, such as payments resulting from termination penalties and residual value guarantees; and

(iii) the terms and conditions of any options that are exercisable after initial optional periods (for example, a purchase option that is exercisable at the end of an extension period at a rate that is currently below market rates).

(b) significant leasehold improvements undertaken (or expected to be undertaken) over the term of the contract that are expected to have significant economic benefit for the lessee when the option to extend or terminate the lease, or to purchase the underlying asset, becomes exercisable;

(c) costs relating to the termination of the lease, such as negotiation costs, relocation costs, costs of identifying another underlying asset suitable for the lessee’s needs, costs of integrating a new asset into the lessee’s operations, or termination penalties and similar costs, including costs associated with returning the underlying asset in a contractually specified condition or to a contractually specified location;

(d) the importance of that underlying asset to the lessee’s operations, considering, for example, whether the underlying asset is a specialised asset, the location of the underlying asset and the availability of suitable alternatives; and

(e) conditionality associated with exercising the option (ie when the option can be exercised only if one or more conditions are met), and the likelihood that those conditions will exist.

B38

An option to extend or terminate a lease may be combined with one or more other contractual features (for example, a residual value guarantee) such that the lessee guarantees the lessor a minimum or fixed cash return that is substantially the same regardless of whether the option is exercised. In such cases, and notwithstanding the guidance on in-substance fixed payments in paragraph B42, an entity shall assume that the lessee is reasonably certain to exercise the option to extend the lease, or not to exercise the option to terminate the lease.

B39

The shorter the non-cancellable period of a lease, the more likely a lessee is to exercise an option to extend the lease or not to exercise an option to terminate the lease. This is because the costs associated with obtaining a replacement asset are likely to be proportionately higher the shorter the non-cancellable period.

B40

A lessee’s past practice regarding the period over which it has typically used particular types of assets (whether leased or owned), and its economic reasons for doing so, may provide information that is helpful in assessing whether the lessee is reasonably certain to exercise, or not to exercise, an option. For example, if a lessee has typically used particular types of assets for a particular period of time or if the lessee has a practice of frequently exercising options on leases of particular types of underlying assets, the lessee shall consider the economic reasons for that past practice in assessing whether it is reasonably certain to exercise an option on leases of those assets.

B41

Paragraph 20 specifies that, after the commencement date, a lessee reassesses the lease term upon the occurrence of a significant event or a significant change in circumstances that is within the control of the lessee and affects whether the lessee is reasonably certain to exercise an option not previously included in its determination of the lease term, or not to exercise an option previously included in its determination of the lease term. Examples of significant events or changes in circumstances include:

(a) significant leasehold improvements not anticipated at the commencement date that are expected to have significant economic benefit for the lessee when the option to extend or terminate the lease, or to purchase the underlying asset, becomes exercisable;

(b) a significant modification to, or customisation of, the underlying asset that was not anticipated at the commencement date;

(c) the inception of a sublease of the underlying asset for a period beyond the end of the previously determined lease term; and

(d) a business decision of the lessee that is directly relevant to exercising, or not exercising, an option (for example, a decision to extend the lease of a complementary asset, to dispose of an alternative asset or to dispose of a business unit within which the right-of-use asset is employed).

In-substance fixed lease payments (paragraphs 27(a), 36(c) and 70(a))

B42

Lease payments include any in-substance fixed lease payments. In-substance fixed lease payments are payments that may, in form, contain variability but that, in substance, are unavoidable. In-substance fixed lease payments exist, for example, if:

(a) payments are structured as variable lease payments, but there is no genuine variability in those payments. Those payments contain variable clauses that do not have real economic substance. Examples of those types of payments include:

(i) payments that must be made only if an asset is proven to be capable of operating during the lease, or only if an event occurs that has no genuine possibility of not occurring; or

(ii) payments that are initially structured as variable lease payments linked to the use of the underlying asset but for which the variability will be resolved at some point after the commencement date so that the payments become fixed for the remainder of the lease term. Those payments become in-substance fixed payments when the variability is resolved.

(b) there is more than one set of payments that a lessee could make, but only one of those sets of payments is realistic. In this case, an entity shall consider the realistic set of payments to be lease payments.

(c) there is more than one realistic set of payments that a lessee could make, but it must make at least one of those sets of payments. In this case, an entity shall consider the set of payments that aggregates to the lowest amount (on a discounted basis) to be lease payments.

Lessee involvement with the underlying asset before the commencement date

Costs of the lessee relating to the construction or design of the underlying asset

B43

An entity may negotiate a lease before the underlying asset is available for use by the lessee. For some leases, the underlying asset may need to be constructed or redesigned for use by the lessee. Depending on the terms and conditions of the contract, a lessee may be required to make payments relating to the construction or design of the asset.

B44

If a lessee incurs costs relating to the construction or design of an underlying asset, the lessee shall account for those costs applying other applicable Standards, such as AASB 116. Costs relating to the construction or design of an underlying asset do not include payments made by the lessee for the right to use the underlying asset. Payments for the right to use an underlying asset are payments for a lease, regardless of the timing of those payments.

Legal title to the underlying asset

B45

A lessee may obtain legal title to an underlying asset before that legal title is transferred to the lessor and the asset is leased to the lessee. Obtaining legal title does not in itself determine how to account for the transaction.

B46

If the lessee controls (or obtains control of) the underlying asset before that asset is transferred to the lessor, the transaction is a sale and leaseback transaction that is accounted for applying paragraphs 98–103.

B47

However, if the lessee does not obtain control of the underlying asset before the asset is transferred to the lessor, the transaction is not a sale and leaseback transaction. For example, this may be the case if a manufacturer, a lessor and a lessee negotiate a transaction for the purchase of an asset from the manufacturer by the lessor, which is in turn leased to the lessee. The lessee may obtain legal title to the underlying asset before legal title transfers to the lessor. In this case, if the lessee obtains legal title to the underlying asset but does not obtain control of the asset before it is transferred to the lessor, the transaction is not accounted for as a sale and leaseback transaction, but as a lease.

Lessee disclosures (paragraph 59)

B48

In determining whether additional information about leasing activities is necessary to meet the disclosure objective in paragraph 51, a lessee shall consider:

(a) whether that information is relevant to users of financial statements. A lessee shall provide additional information specified in paragraph 59 only if that information is expected to be relevant to users of financial statements. In this context, this is likely to be the case if it helps those users to understand:

(i) the flexibility provided by leases. Leases may provide flexibility if, for example, a lessee can reduce its exposure by exercising termination options or renewing leases with favourable terms and conditions.

(ii) restrictions imposed by leases. Leases may impose restrictions, for example, by requiring the lessee to maintain particular financial ratios.

(iii) sensitivity of reported information to key variables. Reported information may be sensitive to, for example, future variable lease payments.

(iv) exposure to other risks arising from leases.

(v) deviations from industry practice. Such deviations may include, for example, unusual or unique lease terms and conditions that affect a lessee’s lease portfolio.

(b) whether that information is apparent from information either presented in the primary financial statements or disclosed in the notes. A lessee need not duplicate information that is already presented elsewhere in the financial statements.

B49

Additional information relating to variable lease payments that, depending on the circumstances, may be needed to satisfy the disclosure objective in paragraph 51 could include information that helps users of financial statements to assess, for example:

(a) the lessee’s reasons for using variable lease payments and the prevalence of those payments;

(b) the relative magnitude of variable lease payments to fixed payments;

(c) key variables upon which variable lease payments depend and how payments are expected to vary in response to changes in those key variables; and

(d) other operational and financial effects of variable lease payments.

B50

Additional information relating to extension options or termination options that, depending on the circumstances, may be needed to satisfy the disclosure objective in paragraph 51 could include information that helps users of financial statements to assess, for example:

(a) the lessee’s reasons for using extension options or termination options and the prevalence of those options;

(b) the relative magnitude of optional lease payments to lease payments;

(c) the prevalence of the exercise of options that were not included in the measurement of lease liabilities; and

(d) other operational and financial effects of those options.

B51

Additional information relating to residual value guarantees that, depending on the circumstances, may be needed to satisfy the disclosure objective in paragraph 51 could include information that helps users of financial statements to assess, for example:

(a) the lessee’s reasons for providing residual value guarantees and the prevalence of those guarantees;

(b) the magnitude of a lessee’s exposure to residual value risk;

(c) the nature of underlying assets for which those guarantees are provided; and

(d) other operational and financial effects of those guarantees.

B52

Additional information relating to sale and leaseback transactions that, depending on the circumstances, may be needed to satisfy the disclosure objective in paragraph 51 could include information that helps users of financial statements to assess, for example:

(a) the lessee’s reasons for sale and leaseback transactions and the prevalence of those transactions;

(b) key terms and conditions of individual sale and leaseback transactions;

(c) payments not included in the measurement of lease liabilities; and

(d) the cash flow effect of sale and leaseback transactions in the reporting period.

Lessor lease classification (paragraphs 61–66)

B53

The classification of leases for lessors in this Standard is based on the extent to which the lease transfers the risks and rewards incidental to ownership of an underlying asset. Risks include the possibilities of losses from idle capacity or technological obsolescence and of variations in return because of changing economic conditions. Rewards may be represented by the expectation of profitable operation over the underlying asset’s economic life and of gain from appreciation in value or realisation of a residual value.

B54

A lease contract may include terms and conditions to adjust the lease payments for particular changes that occur between the inception date and the commencement date (such as a change in the lessor’s cost of the underlying asset or a change in the lessor’s cost of financing the lease). In that case, for the purposes of classifying the lease, the effect of any such changes shall be deemed to have taken place at the inception date.

B55

When a lease includes both land and buildings elements, a lessor shall assess the classification of each element as a finance lease or an operating lease separately applying paragraphs 62–66 and B53–B54. In determining whether the land element is an operating lease or a finance lease, an important consideration is that land normally has an indefinite economic life.

B56

Whenever necessary in order to classify and account for a lease of land and buildings, a lessor shall allocate lease payments (including any lump-sum upfront payments) between the land and the buildings elements in proportion to the relative fair values of the leasehold interests in the land element and buildings element of the lease at the inception date. If the lease payments cannot be allocated reliably between these two elements, the entire lease is classified as a finance lease, unless it is clear that both elements are operating leases, in which case the entire lease is classified as an operating lease.

B57

For a lease of land and buildings in which the amount for the land element is immaterial to the lease, a lessor may treat the land and buildings as a single unit for the purpose of lease classification and classify it as a finance lease or an operating lease applying paragraphs 62–66 and B53–B54. In such a case, a lessor shall regard the economic life of the buildings as the economic life of the entire underlying asset.

Sublease classification

B58

In classifying a sublease, an intermediate lessor shall classify the sublease as a finance lease or an operating lease as follows:

(a) if the head lease is a short-term lease that the entity, as a lessee, has accounted for applying paragraph 6, the sublease shall be classified as an operating lease.

(b) otherwise, the sublease shall be classified by reference to the right-of-use asset arising from the head lease, rather than by reference to the underlying asset (for example, the item of property, plant or equipment that is the subject of the lease).