Illustrative examples

These illustrative examples accompany, but are not part of, AASB 1061. They illustrate aspects of AASB 1061, but are not intended to provide interpretative guidance.

IE1

The following examples portray hypothetical situations. They are intended to illustrate how an entity might apply some of the requirements of this Standard to particular types of transactions, on the basis of the limited facts presented. Although some aspects of the examples might be present in actual fact patterns, all relevant facts and circumstances of a particular fact pattern need to be evaluated when applying this Standard.

Assessing loss of service potential

IE2

Examples A, B and C illustrate the requirements in Section 22 on assessing the loss of service potential and related measurement requirements in Section 12.

Example A – Loss of service potential due to spoilage

Entity A operates a food bank. It purchases items of food to be included in food parcels, and also receives donations of food from supermarkets and individuals. Because the amount of donations it receives is unpredictable, it can have a surplus of certain food items.

These food items might suffer a loss of service potential due to their age. As food items lose service potential as their use-by date approaches, if Entity A has more items than are required for the food parcels, it might need to either sell the items at a discount or dispose of them. This is because the items cannot legally be sold or distributed after this date.

At the reporting date, Entity A assesses whether any of the events set out in paragraph 22.2 has occurred in relation to any material inventories of its food items and if so whether the affected items have suffered a loss of service potential as a result.

At the reporting date, Entity A identifies its inventory includes a pallet of fresh food items that have passed their use-by date. In accordance with paragraphs 22.2 and 22.3, as the perishable items are considered spoilt, Entity A determines the recoverable amount of those inventories.

These inventories held for distribution are measured at their cost less any loss of service potential, being their recoverable amount. In accordance with paragraphs 22.5 and 22.6, Entity A estimates the amount of spoilt inventory that it will not be able to use in the food parcels (the loss of service potential) by reference to the assets’ cost, as these items will need to be disposed of rather than sold at a discount. Entity A reduces the carrying amount of the inventories by the quantity identified as spoilt and records a corresponding expense.

There is no loss of service potential to record for donated inventory measured at a nil cost because the items’ recoverable amount cannot be lower than their carrying amounts (nil).

At the reporting date, Entity A also identifies that it holds a pallet of tinned food items that it intends to distribute and that are nearing their best-before date. In accordance with paragraph 22.2, as the perishable items neither have spoilt nor become obsolete (although their quality may have degraded, the items can still be legally sold or distributed), Entity A does not identify or calculate any possible loss of service potential for these inventories. The inventory is not written down and, in accordance with paragraph 12.4(a), is carried at its cost in the statement of financial position.

Entity A further discovers that it has a pallet of surplus pantry staples that are nearing their best-before date. Entity A decides to sell these items at a discount, at which time the items cease to be inventory held for distribution. In accordance with paragraph 12.4, the carrying amount of these items no longer has regard to the items’ loss of service potential. However, similar to inventory held for distribution, their recoverable amount is only estimated if one of the indicators of impairment in paragraph 22.2 is present. Because the surplus pantry staples have neither spoilt nor become obsolete, Entity A does not calculate the recoverable amount (selling price less costs to complete and sell) of these inventories. The inventory is not written down and is carried at its cost in the statement of financial position.

Example B – Loss of service potential due to reduction in external demand for goods or services

Entity B, which has the objective of helping long-term unemployed people find work, runs courses on job interview preparation. Entity B has prepared printed course materials that are provided to all participants, and has sufficient stock for the expected life of the current course. The course materials are classified as inventories held for distribution.

The courses are subsidised by the government, and as a result Entity B is able to offer the courses for no charge.

During the reporting period, as a result of a change of government policy, the courses cease to be subsidised by the government. Entity B has insufficient resources to cover all the costs itself and introduces a small charge for the courses to cover the cost of hiring the venue and providing lunch. Because the small charge is for a nominal amount, Entity B continues to classify the course materials as inventories held for distribution.

Because of the introduction of the small charge, the number of interested participants reduces and Entity B runs the courses less frequently. As a result, it is unlikely that Entity B will be able to use all the existing printed course materials.

At the reporting date, Entity B assesses whether any of the events identified in paragraph 22.2 has occurred in relation to the course materials and if so whether the affected items have suffered a loss of service potential as a result.

Entity B notes that, as a consequence of the change in circumstances, it has suffered a reduction in external demand for its goods or services and the course materials’ capacity to provide services may be affected adversely as a result (thus satisfying the indicator in paragraph 22.2(b)). As required by paragraphs 22.5 and 22.6, Entity B estimates the amount of the course materials that it will not be able to use and adjusts the carrying amount of its inventories of course materials in proportion to the quantity it estimates will remain unused, and records a corresponding expense.

Example C – Loss of service potential due to changed strategy

Entity C’s mission is to help communities in need. Its activities include providing emergency relief supplies such as bottled water, canned food and hygiene kits to communities affected by natural disasters. Entity C maintains a stockpile of these supplies to ensure a rapid response capability.

Following a strategic review, Entity C’s management decides to change its emergency response model from direct distribution to partnering with local organisations that already have supply chains in place to deliver such emergency relief supplies. Consequently, in the future Entity C will no longer need to maintain an inventory of emergency relief supplies.

At the reporting date, Entity C assesses whether any of the impairment events identified in paragraph 22.2 has occurred and if so whether any remaining emergency relief supplies inventory is impaired as a result. Entity C identifies that the entity has changed its strategy but determines it does not result in the inventory’s capacity to provide services being adversely affected. This is because the capacity of the emergency relief supplies to deliver services has itself not changed as their inherent economic benefits are still present, even though those inventories are now excess to Entity C’s needs. For example, Entity C could distribute the inventory to its new partner organisations for on-distribution. Consequently, Entity C determines that no impairment identified in paragraph 22.2 has occurred and, therefore, does not assess further whether the inventory should be written down. The inventory remains carried at its cost to the entity.

Estimating the long-service leave obligation

IE3

Example D illustrates application of the requirements in Section 23 to long-service leave. The amounts and percentages in Example D are assumed for illustrative purposes only and neither indicate a single required method of calculation nor signify benchmark percentages for the probability of long-service leave benefits becoming unconditional to employees.

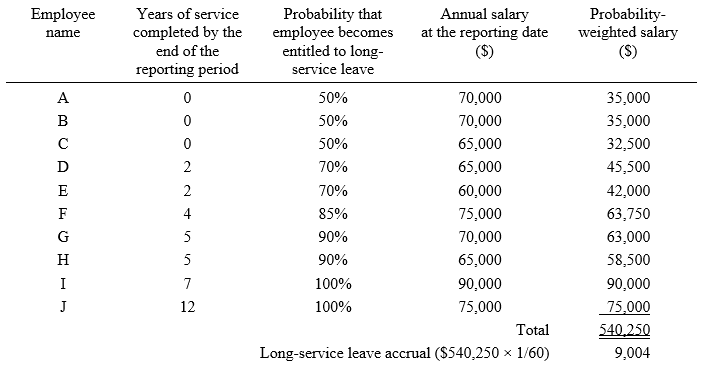

Example D – Long-service leave

Charity D has ten employees with varying years of service. In Charity D’s jurisdiction, an employee becomes entitled to long-service leave once they complete 7 years of continuous employment. The long-service leave benefit is equal to 1/60th of ordinary pay per week for the total period of continuous employment, or 0.867 weeks of leave accrued per year.

When estimating the cost of long-service leave benefits, Charity D takes into account the likelihood that its employees are, or will become, entitled to long-service leave benefits. Charity D does this by estimating its long-service leave obligation by reference to the probability-weighted expected value of the possible outcomes of its ten employees.

Having regard to its experience with employee turnover, and future expectations, Charity D determines the probability that employees will become entitled to long service leave are as follows:

Charity D applies these probabilities to estimate a probability-weighted salary for each employee for the purposes of calculating its long-service leave accrual for the period:

Charity D accrues long-service leave for the reporting period at 1/60th of each employee’s probability-weighted annual remuneration at the reporting date, being $9,004.

In addition to the accrual for services rendered during the period, Charity D also reassesses its opening long-service leave liability and accrues further amounts as necessary to reflect changes in the probability of the leave becoming available to employees and changes in salary since the beginning of the period. For example, because Employee I is still employed by Charity D at the end of the reporting period, the probability that Employee I is entitled to the leave benefit has increased from 95 per cent to 100 per cent. Contrastingly, if Employee I had resigned during the period and before completing the required period of service, the opening leave accrual relating to Employee I would need to be reversed.

Besides payments to employees, entities will often incur employment-related costs such as workers’ compensation insurance premiums and payroll taxes. Liabilities and expenses for employee on-costs are recorded when required by this Standard. For example, if Charity D is subject to payroll tax, it determines whether a liability should be recorded for payroll tax associated with its future long-service leave obligations at the same time as recording the leave accrual.

Recording revenue

IE4

Examples E–I illustrate the requirements in Section 20 for revenue arising from:

(a) fundraising activities;

(b) grants to provide specified services;

(c) grants that management has designated to fund particular services;

(d) grants to construct assets; and

(e) donations to an emergency appeal.

Example E – Fundraising activities

Charity E generates revenue through two main fundraising activities: selling chocolates for cash throughout the year and an annual gala event at which attendees receive entertainment and a meal. The next gala event will be held on 15 July 20X0. The ticket to the gala event, as publicised on Charity E’s website and printed on the ticket, provides an entry to the gala event, dinner and an evening of entertainment. As at 30 June 20X0 (Charity E’s reporting date), Charity E has received $50,000 from the sale of 250 tickets for $200 each.

In accordance with paragraph 20.3(a), Charity E records revenue from the sale of chocolates when the chocolates are transferred to customers, as the parties’ common understanding of Charity E’s commitment in the transaction (to deliver chocolates in exchange) is fulfilled at this time. Where chocolates are transferred immediately at the time of a sale, Charity E will record revenue at the same time as it records the cash receipts from the sales. Charity E discloses revenue from the sales of chocolates in accordance with paragraph 20.21(d) in its financial statements for the reporting period ending 30 June 20X0.

In accordance with paragraphs 20.3(a) and 20.4, in its financial statements for the reporting period ending 30 June 20X0, Charity E records the $50,000 proceeds from sales of tickets to the gala event as a deferred revenue obligation (liability). This is because Charity E and purchasers of the tickets to the gala event have a common understanding, evidenced by information on Charity E’s website and the tickets that in return for the ticket price Charity E will host, after the end of the reporting period, a gala event that includes entertainment and a meal. That common understanding exists regardless of whether there is an enforceable obligation against Charity E to run the gala event that includes all the publicised aspects.

As at 30 June 20X0, the entire amount of the sales proceeds is deferred as a current liability until the gala event is held, since the gala event is to be held within the next 12 months (ie 15 July 20X0). As required by paragraph 20.24, Charity E discloses that it has a deferred revenue obligation of $50,000 that will be satisfied on hosting the gala event.

In accordance with paragraphs 20.5 and 20.8, the deferred revenue obligation is reduced to nil (and revenue is recorded in profit or loss) when the gala event is held on 15 July 20X0.

Example F – Grant to provide specified services

Community Centre F applies for a grant to fund the delivery of IT training sessions for community members. The training sessions will be conducted at regular intervals on the centre’s premises over a two-year period commencing 1 July 20X1. The number of sessions that will be delivered depends on the amount of the grant received.

A grant of $45,000 is received on 15 May 20X1. Community Centre F estimates that each IT training session will cost $2,500 to run. This would allow Community Centre F to deliver 18 IT training sessions for community members during the two-year period. In accordance with paragraph 20.3(a), a deferred revenue obligation (liability) is recorded for the entity’s unsatisfied commitment to provide training sessions on becoming entitled to the grant monies. This is because Community Centre F and the grantor have a common understanding, evidenced by the approved grant application, that Community Centre F will use the received grant monies to provide training sessions (ie perform in a particular manner). That common understanding exists regardless of whether there is an enforceable obligation against Community Centre F to use the funds to provide training sessions.

In accordance with paragraph 20.4, the liability recorded in accordance with paragraph 20.3(a) is measured at $45,000, being the same amount as the asset (grant monies). In accordance with paragraph 20.5, the liability is reduced only when, or as, the commitment is satisfied.

Having regard to paragraph 20.8, Community Centre F determines that its commitment is to deliver training sessions, which will be satisfied as it delivers each IT training session. As at 30 June 20X1, Community Centre F continues to reflect a liability of $45,000 attributable to the grant, because the provision of training sessions had not yet commenced. As Community Centre F expects to deliver the training sessions at regular intervals over the two-year period, in accordance with paragraph 20.25 it classifies $22,500 of the deferred revenue obligation as a current liability and the remaining $22,500 as a non-current liability. In accordance with paragraph 20.5, the deferred revenue obligation is reduced and revenue is recorded as the training sessions are provided.

As at 30 June 20X2, Community Centre F had delivered nine IT training sessions. Accordingly, in its financial statements for the reporting period ending 30 June 20X2, it records revenue of $22,500 and a remaining current liability of $22,500 for the unperformed portion of the commonly understood commitment (being the nine IT training sessions yet to be delivered). As required by paragraph 20.24, Community Centre F discloses that its deferred revenue obligation will be satisfied as it delivers the remaining nine IT training session.

Example G – Grant internally designated to fund particular activities

Community Centre G receives a general purpose grant of $40,000 on 5 May 20X1. The general purpose grant does not specify a time period over which the grant must be spent. Community Centre G’s management decides before the end of its reporting period on 30 June 20X1 to expend the grant monies on a two-year financial literacy training program to be conducted on the Centre’s premises for its beneficiaries. The program will commence on 1 July 20X1.

Community Centre G and the grantor do not have a common understanding that, in return for the grant, Community Centre G will perform in a particular manner that would result in the related transfer or using up of the grant monies or other assets. This is because an entity’s internal expectations or decisions by those charged with governance about how or when an entity expects to use funds received are, by themselves, not sufficient to establish whether the parties have a common understanding that the entity will perform in a particular manner (see paragraph 20.13). In this example, the grantor is not aware that the grant monies are to be spent on delivering a two-year financial literacy training program.

Therefore, in accordance with paragraph 20.3, a deferred revenue obligation is not recorded on receipt of the grant asset (cash) on 5 May 20X1. Rather, in accordance with paragraphs 20.3(b) and 20.4, on 5 May 20X1 Community Centre G records revenue at the same time as it records its receipt of the grant monies, for the same amount ($40,000). As required by paragraph 20.21(c), Community Centre G discloses the grant revenue of $40,000 grouped with other similar grants and donations.

Example H – Grant to construct an asset

Community Centre H applies for a grant of $180,000 to fund most of the cost of constructing an extension to its community hall building, with the remainder of the cost to be met using the Centre’s accumulated funds. The grant of $180,000 is received on 30 June 20X2 and separately identifiable from other funds.

In accordance with paragraph 20.3(a), a deferred revenue obligation (liability) is initially recorded to reflect the entity’s unsatisfied commitment to use the grant monies towards the construction of a building extension. This is because Community Centre H and the grantor have a common understanding, evidenced by the approved grant application, that Community Centre H will apply the grant monies received towards the construction of the specified building extension (ie perform in a particular manner). That common understanding exists regardless of whether there is an enforceable obligation against Community Centre H to use the grant monies only to construct the building extension.

In accordance with paragraph 20.4, the liability recorded in accordance with paragraph 20.3(a) is initially measured at the same amount as the amount recorded for the grant money ($180,000). In accordance with paragraph 20.3, the grant is deferred as a liability until the commitment is satisfied. The liability is reduced in a manner that faithfully represents the amount and pattern of the entity’s satisfaction of its commitment.

On consideration of the terms and conditions of the grant, Community Centre H decides that its commitment to the grantor will be satisfied as the grant money is applied towards the construction of the building extension, rather than on the delivery of a completed extension or as the extension is built. In its financial statements for the reporting period ending 30 June 20X2, Community Centre H records a liability for $180,000 for the grant for the extension of its community hall building in accordance with paragraph 20.3, because it had not yet spent any of the funds received on activities relating to the construction of the building extension. Community Centre H expects it will use up forty percent of the grant monies within twelve months after the reporting date and the balance in the subsequent year. Accordingly, Community Centre H classifies $72,000 of the grant as a current liability, and the remaining $108,000 as a non-current liability.

By 30 June 20X3, Community Centre H had spent $90,000 of the grant monies on the building extension. Accordingly, in its financial statements for the reporting period ending 30 June 20X3, Community Centre H records revenue (categorised as grants for the construction of long-lived assets in accordance with paragraph 20.21(b)) of $90,000. In accordance with paragraph 20.24, the remaining carrying amount of the liability of $90,000 – representing the remaining grant money to be applied towards the community hall building – is classified as a current liability as Community Centre H expects to spend the remaining grant money within the next twelve months after 30 June 20X3.

Alternative scenario 1: Grant is given towards future building works

Assume instead that Community Centre H is provided with a grant to help fund the purchase of a site and construction of a new building, but that an appropriate site had not yet been identified or acquired at the time the grant was made and the grant funds transferred to Community Centre H. In this scenario, Community Centre H has a common understanding with the grantor that the monies are to be used for capital works. In accordance with paragraph 20.3, Community Centre H will record the grant as a deferred revenue obligation because Community Centre H and the grantor have a common understanding that the grant funds will be applied to purchasing a site and constructing a new building.

In accordance with paragraph 20.5, the carrying amount of the deferred revenue obligation will be reduced and revenue would be recorded once (or as) the commitment is satisfied. Community Centre H will need to apply judgement, having regard to the terms and conditions of the grant, to determine when and how its commitment is satisfied, for example whether this is from when the search for a site begins or only from when a site is identified and purchase activity has commenced. The pattern of the entity’s satisfaction of the commitment might be determined to be as ringfenced grant funds are expended, evenly over the acquisition and build period, by reference to the stage of completion of any building works or when the building is completed.

Assume instead that Community Centre H is provided with a grant to help fund the purchase of a site and construction of a new building, but that an appropriate site had not yet been identified or acquired at the time the grant was made and the grant funds transferred to Community Centre H. In this scenario, Community Centre H has a common understanding with the grantor that the monies are to be used for capital works. In accordance with paragraph 20.3, Community Centre H will record the grant as a deferred revenue obligation because Community Centre H and the grantor have a common understanding that the grant funds will be applied to purchasing a site and constructing a new building.

In accordance with paragraph 20.5, the carrying amount of the deferred revenue obligation will be reduced and revenue would be recorded once (or as) the commitment is satisfied. Community Centre H will need to apply judgement, having regard to the terms and conditions of the grant, to determine when and how its commitment is satisfied, for example whether this is from when the search for a site begins or only from when a site is identified and purchase activity has commenced. The pattern of the entity’s satisfaction of the commitment might be determined to be as ringfenced grant funds are expended, evenly over the acquisition and build period, by reference to the stage of completion of any building works or when the building is completed.

Alternative scenario 2: Grant is given after the building extension is complete to help alleviate the costs of capital works

Assume instead that Community Centre H has funded the building extension works itself by taking out a bank loan. After the building extension is complete, Community Centre H receives a grant intended to help alleviate the impact of the costs of these capital works so that these costs do not detract from Community Centre H’s ability to deliver programs. Community Centre H intends to apply the grant monies received to pay down some of its outstanding bank loan.

In this scenario, Community Centre H has a common understanding with the grantor that the monies are to be used towards easing the financial burden of the costs of the building extension. In accordance with paragraphs 20.3 and 20.5, the entity has a deferred revenue obligation and should reduce that obligation in a manner that faithfully represents the amount and pattern of the entity’s satisfaction of its commitments. However, the building works are already completed and the entity’s decision to apply the funds to loan repayments is an internal management decision. Even though the parties share a common understanding about the purpose of the grant, the grant was given to, in effect, support the entity’s operations over an unspecified period of time. For example, Community Centre H might prefer to use these monies to fund a new program that it would not otherwise have been able to run due to the need to fund the loan repayments. Therefore, per paragraph 20.12, Community Centre H records grant revenue simultaneously with receiving the grant monies.

Assume instead that Community Centre H has funded the building extension works itself by taking out a bank loan. After the building extension is complete, Community Centre H receives a grant intended to help alleviate the impact of the costs of these capital works so that these costs do not detract from Community Centre H’s ability to deliver programs. Community Centre H intends to apply the grant monies received to pay down some of its outstanding bank loan.

In this scenario, Community Centre H has a common understanding with the grantor that the monies are to be used towards easing the financial burden of the costs of the building extension. In accordance with paragraphs 20.3 and 20.5, the entity has a deferred revenue obligation and should reduce that obligation in a manner that faithfully represents the amount and pattern of the entity’s satisfaction of its commitments. However, the building works are already completed and the entity’s decision to apply the funds to loan repayments is an internal management decision. Even though the parties share a common understanding about the purpose of the grant, the grant was given to, in effect, support the entity’s operations over an unspecified period of time. For example, Community Centre H might prefer to use these monies to fund a new program that it would not otherwise have been able to run due to the need to fund the loan repayments. Therefore, per paragraph 20.12, Community Centre H records grant revenue simultaneously with receiving the grant monies.

Example I – Donations to an emergency appeal

Charity I announced an appeal for donations to provide emergency relief to victims of a cyclone on 20 February 20X2 and raised $200,000 in response. On its website, Charity I indicated that if greater funds are raised than needed for its cyclone emergency relief efforts, the excess funds will be redirected to another current, specific program of the charity – to assist victims of a recent earthquake in the same region.

On 15 June 20X2, Charity I announced that its emergency relief program for the cyclone is complete. Charity I spent $150,000 of the donated funds on that program. At 30 June 20X2, none of the remaining $50,000 donated funds had been spent by Charity I.

In its financial statements for the reporting period ending 30 June 20X2, Charity I records donation revenue of $150,000 in accordance with paragraph 20.5 for the expenditure of that amount in providing emergency relief to victims of the cyclone, resulting from the reduction in the deferred revenue obligation initially recorded in accordance with paragraph 20.3 when the donated funds were received. The charity continues to record the remaining deferred revenue obligation (liability) of $50,000 relating to the unspent donations that are to be redirected towards the earthquake assistance program. Charity I expects it will use the unspent donations within twelve months after the reporting date. Accordingly, Charity I classifies the deferred revenue obligation of $50,000 as a current liability.

The fact that Charity I will no longer spend funds donated primarily to provide emergency relief for victims of the cyclone on these efforts does not mean that there is no longer an unsatisfied common understanding between the donors and Charity I on 30 June 20X2 regarding the use of the funds. This is because, as evidenced by the communicated appeal terms, Charity I and the donors have a common understanding that Charity I will use the donations received to provide charitable assistance to victims of either the cyclone or the earthquake (ie perform in a particular manner). That common understanding exists regardless of whether there is an enforceable obligation against Charity I to expend the donated funds on either of the stated programs.

In accordance with paragraphs 20.5 and 20.8, the deferred revenue obligation of $50,000 is reduced and revenue recorded as the remaining donated funds are expended under the specific earthquake assistance program.

If Charity I did not indicate how it would spend any excess funds raised, then there would not be a common understanding between the parties as to how any monies not directed towards the cyclone efforts must be spent. In this scenario, in accordance with paragraphs 20.3–20.5, Charity I would record the entire $200,000 received as revenue of the reporting period ending 30 June 20X2. There would be no deferred revenue obligation at that date in this case.

Contingent assets

IE5

Example J illustrates the application of Section 19 to contingent assets in the form of pledges.

Example J – Pledges

Before the end of the reporting period, Charity J received written pledges from corporate donors of $200,000 to fund the building of water wells to provide clean drinking water in developing countries in response to an appeal for donations for that explicit purpose. Based on its previous experience with pledged donations, Charity J estimates it will receive only $120,000 of the pledged $200,000.

As at the end of the reporting period, no cash had been received. Charity J does not have an enforceable right to the pledged amounts.

In accordance with paragraph 20.18, Charity J does not record the pledged donations as an asset because it has not yet received the promised cash. However, Charity J determines the pledges meet the definition of a contingent asset, because those amounts are possible assets arising from past events (receipt of the written pledges), the existence of which will only be confirmed by the occurrence of one or more uncertain future events (cash transfers to Charity J) not wholly within Charity J’s control.

Based on its experience with previous appeals, Charity J concludes that the receipt of an inflow from the pledged donations is probable even if some pledges are not honoured. Accordingly, in accordance with paragraph 19.17, Charity J discloses that it has received pledges totalling $200,000 and that at least 60 per cent of these pledges are expected to be honoured.

(When received, the donations that were pledged are recorded as revenue only as the wells are built. This treatment recognises that because the donations were made in response to the specific appeal, Charity J and its donors have a common understanding that Charity J will only use these amounts for the building of the water wells, consistent with paragraphs 20.3(a) and 20.6–20.10 of this Standard.)