Appendix E -- Australian implementation guidance for public sector entities

This appendix is an integral part of AASB 17 Insurance Contracts. It describes the application of paragraphs Aus6.1 and Aus6.2. The appendix applies only to public sector entities and does not affect the application of AASB 17 by private sector entities.

Introduction

E1

AASB 17 Insurance Contracts incorporates International Financial Reporting Standard IFRS 17 Insurance Contracts, issued by the International Accounting Standards Board. Consequently, the text of AASB 17 is generally expressed from the perspective of private sector entities. The AASB prepared this Appendix to explain and illustrate the application of the principles of paragraphs Aus6.1 and Aus6.2 of the Standard by public sector entities in relation to identifying public sector arrangements that give rise to insurance contracts that fall within the scope of AASB 17.

E2

Judgement needs to be exercised in applying the pre-requisites, indicators and other considerations based on each entity’s circumstances.

E3

For the purposes of this Appendix, in some cases relatively generic terms are used, rather than the more specific defined terms in AASB 17, because the guidance is focused on identifying the public sector activities to which AASB 17 applies. For example, this Appendix uses the term:

(a) ‘arrangement’ on the basis that some public sector arrangements will fall within the scope of AASB 17 and be insurance contracts, but some will not; and

(b) ‘participant’ on the basis that participants in arrangements that are insurance contracts will be policyholders, but participants in public sector arrangements that do not will fall within the scope of AASB 17 will not be policyholders.

E4

The guidance in paragraphs B7–B16 of Appendix B on distinguishing between insurance risks and other risks applies equally to public sector entities. However, because public sector entities often undertake a wider range of risk-bearing activities than private sector entities, additional guidance is needed to identify insurance contracts in a public sector context.

E5

Governments often arrange to provide support as a result of events that affect individuals and communities. Some of these arrangements involve transactions that are best accounted for as insurance contracts, while many of these arrangements relate to a government’s role in providing services such as social benefits, universal health care and disaster relief. In determining which of these types of arrangements give rise to insurance contracts that fall within the scope of AASB 17, an entity considers the pre-requisites, indicators and the other considerations outlined in paragraphs E6–E36.

Identifying insurance contracts in a public sector context (paragraphs Aus6.1 and Aus6.2)

Applying the pre-requisites, indicators and other considerations

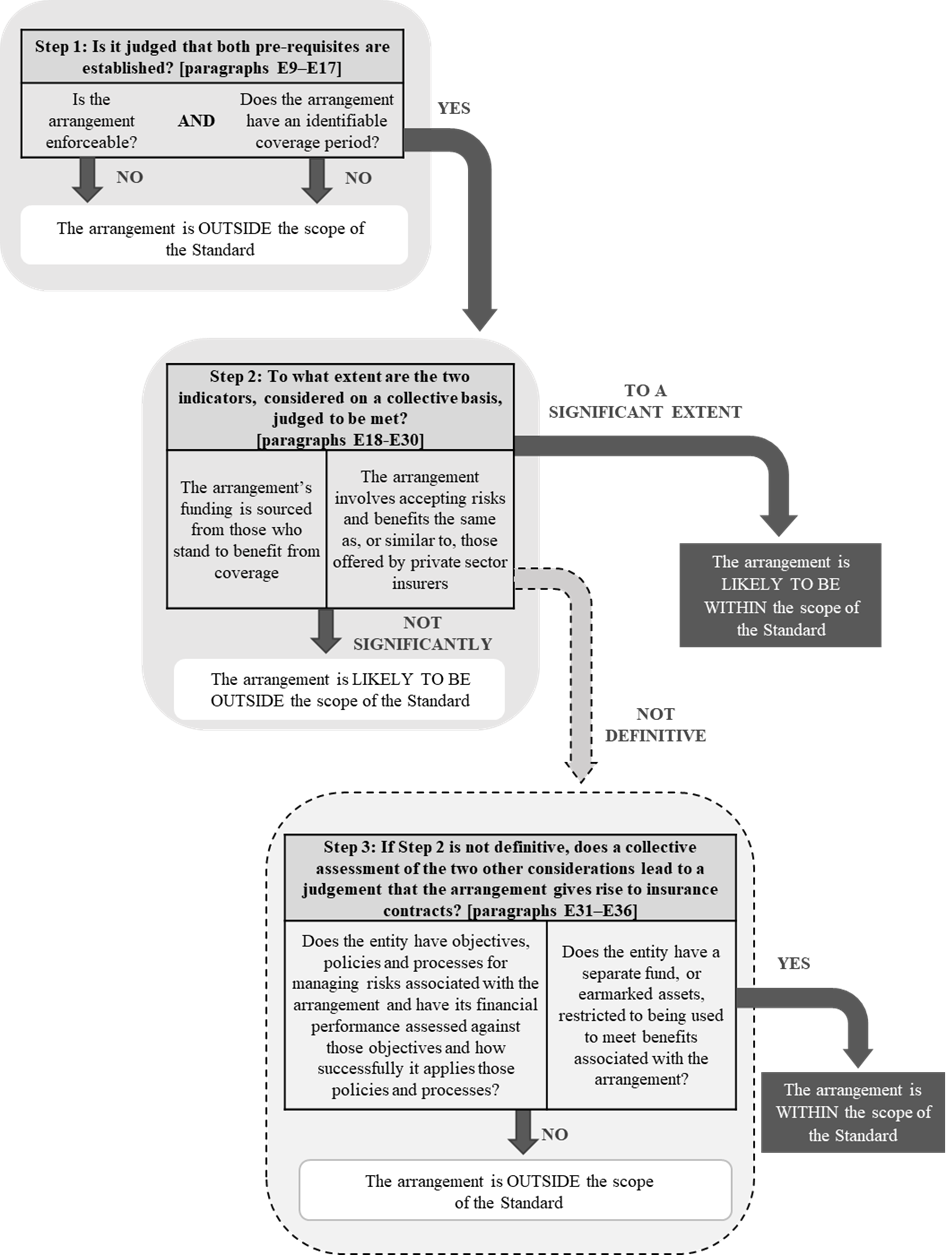

E6

In accordance with paragraph Aus6.1, a public sector entity would need to consider whether AASB 17 applies to an arrangement if, and only if, both of the following pre-requisites are established:

(a) the arrangement is enforceable – refer to guidance in paragraphs E9–E12; and

(b) the arrangement has an identifiable coverage period – refer to guidance in paragraphs E13–E17.

E7

When both of the pre-requisites in paragraph E6 are established in respect of an arrangement, subject to paragraphs 8 and 8A an entity applies the following indicators on a collective basis to determine whether the arrangement gives rise to insurance contracts that fall within the scope of AASB 17:

(a) the source and extent of funding – refer to guidance in paragraphs E18–E22; and

(b) the similarity of risks covered and benefits provided – refer to guidance in paragraphs E23–E30.

E8

When applying the indicators in paragraph E7 does not definitively determine whether an arrangement gives rise to insurance contracts that fall within the scope of AASB 17, a public sector entity applies the following other considerations on a collective basis to determine whether the arrangement gives rise to insurance contracts that fall within the scope of AASB 17:

(a) the management practices and assessment of financial performance applied – refer to guidance in paragraphs E31–E33; and

(b) the existence of a separate fund, or earmarked assets, that are restricted to being used to meet benefits – refer to guidance in paragraphs E34–E36.

E10

In determining whether there is an enforceable contract, the following matters are relevant:

(a) when a public sector entity or its controlling government does not have the practical ability under existing or substantively enacted legislation to deny or change promised benefits or amounts based on agreed parameters, it is indicative of an enforceable contract; and

(b) when an individual or entity can identify promised amounts or amounts based on agreed parameters that they will receive from the public sector entity on the occurrence of specified events, it is indicative of an enforceable contract.

E11

When a public sector entity or its controlling government has the practical ability under existing or substantively enacted legislation to retrospectively deny or substantively change promised benefits or compensation, the policyholder does not have enforceable rights under the arrangement and the public sector entity does not have enforceable obligations for promised amounts or for amounts based on agreed parameters. For example, if an entity can retrospectively make a substantive change to the amount of benefits, such as by curtailing compensation being paid to a beneficiary in relation to a past event under existing legislation, this indicates the arrangement is not enforceable.

E12

An arrangement that involves a public sector entity issuing documentation to another party, similar to an insurance contract issued by a private sector insurer, would be indicative of an agreement that creates enforceable rights and obligations. However, having some or all of the substantive rights and obligations for an insurance arrangement being set out in law or regulation would not necessarily mean that the arrangement is unsuitable to be accounted for as an insurance contract. In common with the private sector, arrangements need to be interpreted within a regulatory framework and, consistent with paragraphs 2 and Aus2.1, an entity is required to consider its substantive rights and obligations, whether they arise from a contract, law or regulation.

E14

In determining whether there is an identifiable coverage period for a public sector arrangement, the following factors may be relevant:

(a) there is documentation agreed between the public sector entity and a participant in an arrangement that identifies a period over which coverage is to be provided;

(b) funding, for example from participant premiums or levies, is associated with coverage for an identifiable period that may, for example, be set out in law or regulation; and

(c) a public sector arrangement is an adjunct, for example based on law or regulation, to an insurance contract issued by another entity (eg a private sector insurer) and a coverage period for the public sector arrangement can be determined by reference to the insurance contract of the other entity.

E15

In relation to paragraph E14(b), in some circumstances a public sector entity may be able to determine coverage periods for its arrangements based on the coverage periods identified when it sets premiums and benefits. For example, an arrangement may have a coverage period aligned with the entity’s annual reporting period on the basis that it sets premiums and benefits with the objective of raising funds from the arrangements in place in that year that are estimated to be sufficient to meet all the benefits, including future benefits, expected to arise from events that occur in that year.

E16

In relation to paragraph E14(c), in some cases the period over which claims for benefits might arise under a public sector arrangement would be determinable from the period over which coverage is provided under an insurance contract issued by a private sector insurer. This may be the case when, for example, the public sector entity’s arrangements are funded from a levy on the insurance contracts issued by private sector insurers and the levy is intended to meet claims for benefits arising from events that occur during the private sector insurance contract coverage periods. In other cases, the period over which claims for benefits might arise under a public sector arrangement may not be determinable from the period over which coverage is provided under an insurance contract issued by a private sector insurer. This may be the case when, for example, the public sector entity’s arrangements are funded from a levy on the insurance contracts issued by private sector insurers in a particular period and the levy is intended to meet claims for benefits arising from events in that period, rather than from events during the private sector insurance contract coverage periods.

E17

The following are examples of circumstances that would be indicative of an arrangement without an identifiable coverage period:

(a) a public sector entity has an open-ended arrangement to provide benefits based on eligibility criteria that relate to an individual’s inherent status, for example, age or disability;

(b) those who stand to benefit from an arrangement are eligible for compensation based only on suffering loss from a specified natural disaster; and

(c) a public sector entity’s policy is to raise funds from levies or by other means to meet claims from current and/or prior periods on a pay-as-you-go basis. Entities operating on a pay-as-you-go basis are focused on meeting net cash outflows expected to occur in the current period, rather than on meeting net cash outflows related to events that arise in a particular coverage period that may involve fund outflows expected to occur in both the current and future periods.

Indicator: Source and extent of funding

E18

Under an insurance contract, a policyholder usually pays premiums to an insurer. In most cases, the premiums are the primary source of funding the payment of any claims and the costs of operating the insurance business.

E19

When a public sector entity receives premiums or levies under an arrangement in exchange for accepting risks from those who stand to benefit, it is an indication that an arrangement gives rise to insurance contracts within the scope of AASB 17. The greater the extent to which the participant who stands to benefit from an arrangement is providing the funding, the more indicative this would be of a policyholder–insurer relationship and an arrangement that gives rise to insurance contracts that fall within the scope of AASB 17.

E20

The individual or entity from which the public sector entity receives premiums does not need to be a direct beneficiary of the arrangement. Instead, they may be an indirect beneficiary. For example, when a public sector entity receives levies from the participant for the purpose of compensating other parties that might be damaged by the participant’s actions, the benefit to the participant would often be that the damaged parties cannot seek additional compensation from them by other means.

E21

When all of a public sector entity’s funding to meet benefits is received in exchange for accepting risks from those who stand to benefit, this is highly indicative of an arrangement that gives rise to insurance contracts that fall within the scope of AASB 17. The lower the proportion of a public sector entity’s funding to meet benefits in exchange for accepting risks from those who stand to benefit, the less likely it is that those arrangements would be accounted for as insurance contracts. For example, a co-payment from a beneficiary that is intended to help ration services and is not intended to fully fund services is unlikely to indicate an arrangement that gives rise to insurance contracts that fall within the scope of AASB 17. When a public sector entity receives a significant portion of funding from sources such as general taxation, this would indicate that an arrangement does not give rise to insurance contracts that fall within the scope of AASB 17.

Indicator: Similarity of risks covered and benefits provided

E24

It is an indicator that a public sector entity arrangement gives rise to insurance contracts within the scope of AASB 17 when it involves accepting risks and providing benefits that are the same as, or similar to, those offered by private sector insurers. In some cases, public sector entities operate alongside private sector insurers to accept risks and provide benefits that are the same, for example in respect of employer liability for workers’ compensation risks.

E25

In some cases, public sector entities are monopolies in their jurisdictions and there are no relevant counterpart arrangements of private sector entities to consider. In these cases, consideration is given to whether a public sector entity’s arrangements involve accepting risks and providing benefits that are the same as, or are similar to, those offered by private sector insurers in other, similar jurisdictions. In relation to other jurisdictions, only information that is readily available need be considered. That is, public sector entities need not conduct an exhaustive search for counterpart arrangements.

E26

The greater the level of similarity between the risks accepted and benefits provided by a public sector entity and those offered by any relevant counterpart private sector insurer, the more likely it would be that an arrangement gives rise to insurance contracts that fall within the scope of AASB 17.

E27

In some cases, there will be a clear similarity between the risks being accepted and the benefits being provided by a public sector entity and private sector insurers, and this is highly indicative of an arrangement that gives rise to insurance contracts that fall within the scope of AASB 17.

E28

Public sector entities often fill gaps in a market left by the private sector because they pose the greatest risks and might generally be unprofitable or unsustainable for the private sector to cover. Of itself, the level of riskiness generally is not relevant to determining whether there is similarity between the risks covered and the benefits provided by public sector entities and private sector insurers. The similarity of the nature of the risks covered and benefits provided is the key focus. Accordingly, the nature of a risk covered by a public sector entity and private sector insurers could be the same, even though the level of risk borne by the public sector entity is more extreme.

Other consideration: Management practices and assessment of financial performance

E31

Consideration is given to the extent to which a public sector entity has objectives, policies and processes for managing risks associated with its arrangements and has its financial performance assessed against those objectives and how successfully it applies those policies and processes in determining whether an arrangement gives rise to insurance contracts that fall within the scope of AASB 17. In that context, an entity that has insurance contracts would be expected to conduct the following activities (either itself or via outsourcing):

(a) underwriting and risk assessment;

(b) managing the entity’s capital based on the measurement of risks and uncertainties relating to coverage and incurred claims and their potential future impacts; and

(c) fair and prudent claims management.

E32

In general, any public sector entity that is responsible for dispensing compensation (as an insurer or non-insurer) would be expected to have sound practices in respect of risk assessment, managing capital and managing claims. However, these features of some public sector arrangements are still regarded as a relevant consideration, in conjunction with the indicators identified in paragraph E7 and the other consideration identified in paragraph E8(b), to determine whether an arrangement gives rise to insurance contracts that fall within the scope of AASB 17, when the indicators are not definitive.

E33

In particular, it may imply that an arrangement gives rise to insurance contracts that fall within the scope of AASB 17 when an entity assesses the relative riskiness of participants and prices coverage based on those assessments. This does not mean an arrangement that involves an entity charging a standard amount to all participants, regardless of risk, is necessarily outside the scope of AASB 17, because some entities (even in the private sector) are subject to regulatory constraints on pricing (as acknowledged in paragraph 20), such as community-rated pricing.

E35

The existence of a separate fund, or earmarked assets, that are restricted to being used to meet benefits is a feature of many types of public sector arrangements. However, the feature is still regarded as a relevant consideration, in conjunction with the indicators identified in paragraph E7 and the other consideration identified in paragraph E8(a), to determine whether an arrangement gives rise to insurance contracts that fall within the scope of AASB 17, when the indicators are not definitive.

Diagram – Applying the pre-requisites, indicators and other considerations

E37

The diagram below illustrates the application of paragraphs Aus6.1, Aus6.2 and E6–E8 relevant to public sector entities for identifying arrangements that give rise to insurance contracts that fall within the scope of AASB 17. The diagram should be read in conjunction with the guidance set out in paragraphs E9–E36, as referenced in the diagram.