Illustrative example

This example accompanies, but is not part of, AASB 139.

Facts

IE1

On 1 January 20X1, Entity A identifies a portfolio comprising assets and liabilities whose interest rate risk it wishes to hedge. The liabilities include demandable deposit liabilities that the depositor may withdraw at any time without notice. For risk management purposes, the entity views all of the items in the portfolio as fixed rate items.

IE2

For risk management purposes, Entity A analyses the assets and liabilities in the portfolio into repricing time periods based on expected repricing dates. The entity uses monthly time periods and schedules items for the next five years (ie it has 60 separate monthly time periods).[8] The assets in the portfolio are prepayable assets that Entity A allocates into time periods based on the expected prepayment dates, by allocating a percentage of all of the assets, rather than individual items, into each time period. The portfolio also includes demandable liabilities that the entity expects, on a portfolio basis, to repay between one month and five years and, for risk management purposes, are scheduled into time periods on this basis. On the basis of this analysis, Entity A decides what amount it wishes to hedge in each time period.

In this example principal cash flows have been scheduled into time periods but the related interest cash flows have been included when calculating the change in the fair value of the hedged item. Other methods of scheduling assets and liabilities are also possible. Also, in this example, monthly repricing time periods have been used. An entity may choose narrower or wider time periods.

IE3

This example deals only with the repricing time period expiring in three months’ time, ie the time period maturing on 31 March 20X1 (a similar procedure would be applied for each of the other 59 time periods). Entity A has scheduled assets of CU100 million[9] and liabilities of CU80 million into this time period. All of the liabilities are repayable on demand.

In this example monetary amounts are denominated in ‘currency units (CU)’.

IE4

Entity A decides, for risk management purposes, to hedge the net position of CU20 million and accordingly enters into an interest rate swap[10] on 1 January 20X1 to pay a fixed rate and receive LIBOR, with a notional principal amount of CU20 million and a fixed life of three months.

The example uses a swap as the hedging instrument. An entity may use forward rate agreements or other derivatives as hedging instruments.

IE5

This example makes the following simplifying assumptions:

(a) the coupon on the fixed leg of the swap is equal to the fixed coupon on the asset;

(b) the coupon on the fixed leg of the swap becomes payable on the same dates as the interest payments on the asset; and

(c) the interest on the variable leg of the swap is the overnight LIBOR rate. As a result, the entire fair value change of the swap arises from the fixed leg only, because the variable leg is not exposed to changes in fair value due to changes in interest rates.

In cases when these simplifying assumptions do not hold, greater ineffectiveness will arise. (The ineffectiveness arising from (a) could be eliminated by designating as the hedged item a portion of the cash flows on the asset that are equivalent to the fixed leg of the swap.)

IE6

It is also assumed that Entity A tests effectiveness on a monthly basis.

IE7

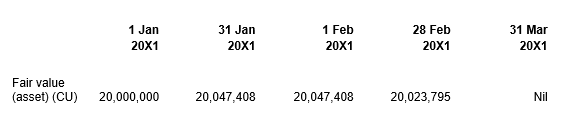

The fair value of an equivalent non-prepayable asset of CU20 million, ignoring changes in value that are not attributable to interest rate movements, at various times during the period of the hedge is as follows:

IE8

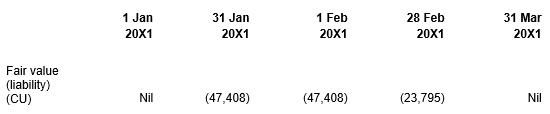

The fair value of the swap at various times during the period of the hedge is as follows:

Accounting treatment

IE9

On 1 January 20X1, Entity A designates as the hedged item an amount of CU20 million of assets in the three-month time period. It designates as the hedged risk the change in the value of the hedged item (ie the CU20 million of assets) that is attributable to changes in LIBOR. It also complies with the other designation requirements set out in paragraphs 88(d) and AG119 of the Standard.

IE10

Entity A designates as the hedging instrument the interest rate swap described in paragraph IE4.

End of month 1 (31 January 20X1)

IE11

On 31 January 20X1 (at the end of month 1) when Entity A tests effectiveness, LIBOR has decreased. Based on historical prepayment experience, Entity A estimates that, as a consequence, prepayments will occur faster than previously estimated. As a result it re-estimates the amount of assets scheduled into this time period (excluding new assets originated during the month) as CU96 million.

IE12

The fair value of the designated interest rate swap with a notional principal of CU20 million is (CU47,408)[11] (the swap is a liability).

see paragraph IE8

IE13

Entity A computes the change in the fair value of the hedged item, taking into account the change in estimated prepayments, as follows.

(a) First, it calculates the percentage of the initial estimate of the assets in the time period that was hedged. This is 20 per cent (CU20 million ÷ CU100 million).

(b) Second, it applies this percentage (20 per cent) to its revised estimate of the amount in that time period (CU96 million) to calculate the amount that is the hedged item based on its revised estimate. This is CU19.2 million.

(c) Third, it calculates the change in the fair value of this revised estimate of the hedged item (CU19.2 million) that is attributable to changes in LIBOR. This is CU45,511 (CU47,408[12] × (CU19.2 million ÷ CU20 million)).

ie CU20,047,408 – CU20,000,000. See paragraph IE7.

IE14

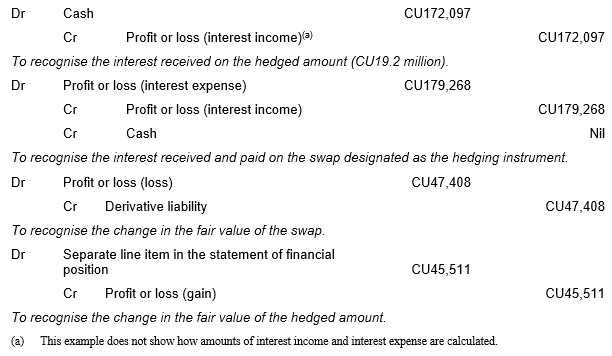

Entity A makes the following accounting entries relating to this time period:

IE15

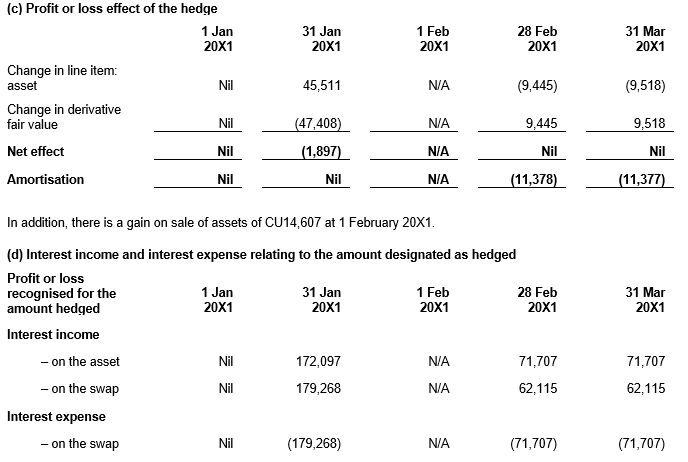

The net result on profit or loss (excluding interest income and interest expense) is to recognise a loss of (CU1,897). This represents ineffectiveness in the hedging relationship that arises from the change in estimated prepayment dates.

Beginning of month 2

IE16

On 1 February 20X1 Entity A sells a proportion of the assets in the various time periods. Entity A calculates that it has sold 81/3 per cent of the entire portfolio of assets. Because the assets were allocated into time periods by allocating a percentage of the assets (rather than individual assets) into each time period, Entity A determines that it cannot ascertain into which specific time periods the sold assets were scheduled. Hence it uses a systematic and rational basis of allocation. Based on the fact that it sold a representative selection of the assets in the portfolio, Entity A allocates the sale proportionately over all time periods.

IE17

On this basis, Entity A computes that it has sold 81/3 per cent of the assets allocated to the three-month time period, ie CU8 million (81/3 per cent of CU96 million). The proceeds received are CU8,018,400, equal to the fair value of the assets.[13] On derecognition of the assets, Entity A also removes from the separate line item in the statement of financial position an amount that represents the change in the fair value of the hedged assets that it has now sold. This is 81/3 per cent of the total line item balance of CU45,511, ie CU3,793.

The amount realised on sale of the asset is the fair value of a prepayable asset, which is less than the fair value of the equivalent non-prepayable asset shown in paragraph IE7.

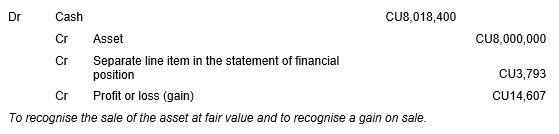

IE18

Entity A makes the following accounting entries to recognise the sale of the asset and the removal of part of the balance in the separate line item in the statement of financial position:

Because the change in the amount of the assets is not attributable to a change in the hedged interest rate no ineffectiveness arises.

IE19

Entity A now has CU88 million of assets and CU80 million of liabilities in this time period. Hence the net amount Entity A wants to hedge is now CU8 million and, accordingly, it designates CU8 million as the hedged amount.

IE20

Entity A decides to adjust the hedging instrument by designating only a proportion of the original swap as the hedging instrument. Accordingly, it designates as the hedging instrument CU8 million or 40 per cent of the notional amount of the original swap with a remaining life of two months and a fair value of CU18,963.[14] It also complies with the other designation requirements in paragraphs 88(a) and AG119 of the Standard. The CU12 million of the notional amount of the swap that is no longer designated as the hedging instrument is either classified as held for trading with changes in fair value recognised in profit or loss, or is designated as the hedging instrument in a different hedge.[15]

CU47,408 × 40 per cent

The entity could instead enter into an offsetting swap with a notional principal of CU12 million to adjust its position and designate as the hedging instrument all CU20 million of the existing swap and all CU12 million of the new offsetting swap.

IE21

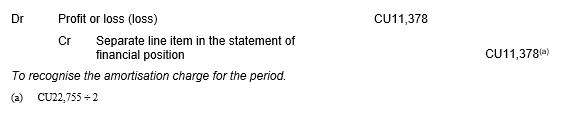

As at 1 February 20X1 and after accounting for the sale of assets, the separate line item in the statement of financial position is CU41,718 (CU45,511 – CU3,793), which represents the cumulative change in fair value of CU17.6 million[16] of assets. However, as at 1 February 20X1, Entity A is hedging only CU8 million of assets that have a cumulative change in fair value of CU18,963.[17] The remaining separate line item in the statement of financial position of CU22,755[18] relates to an amount of assets that Entity A still holds but is no longer hedging. Accordingly Entity A amortises this amount over the remaining life of the time period, ie it amortises CU22,755 over two months.

CU19.2 million – (81/3% × CU19.2 million)

CU41,718 × (CU8 million ÷ CU17.6 million)

CU41,718 – CU18,963

IE22

Entity A determines that it is not practicable to use a method of amortisation based on a recalculated effective yield and hence uses a straight-line method.

End of month 2 (28 February 20X1)

IE23

On 28 February 20X1 when Entity A next tests effectiveness, LIBOR is unchanged. Entity A does not revise its prepayment expectations. The fair value of the designated interest rate swap with a notional principal of CU8 million is (CU9,518)[19] (the swap is a liability). Also, Entity A calculates the fair value of the CU8 million of the hedged assets as at 28 February 20X1 as CU8,009,518.[20]

CU23,795 [see paragraph IE8] × (CU8 million ÷ CU20 million)

CU20,023,795 [see paragraph IE7] × (CU8 million ÷ CU20 million)

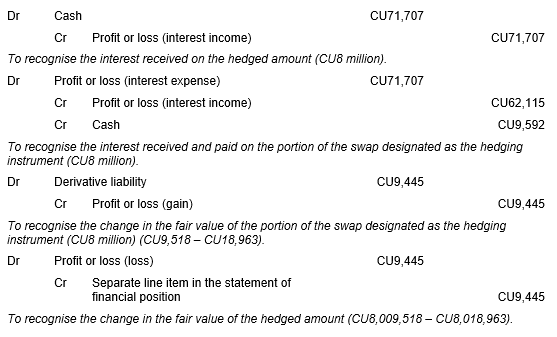

IE24

Entity A makes the following accounting entries relating to the hedge in this time period:

IE25

The net effect on profit or loss (excluding interest income and interest expense) is nil reflecting that the hedge is fully effective.

IE26

Entity A makes the following accounting entry to amortise the line item balance for this time period:

End of month 3

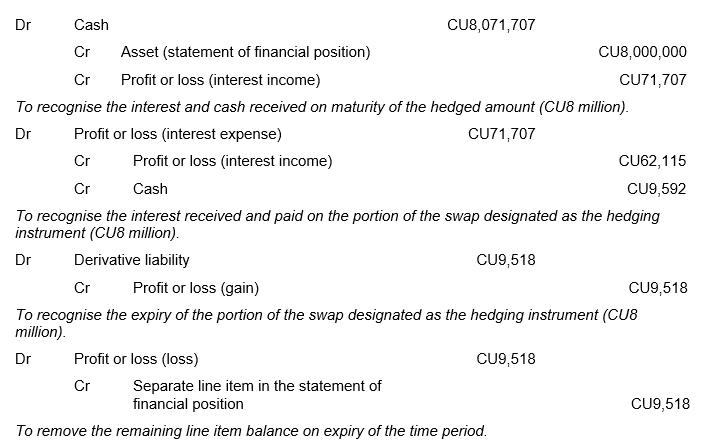

IE27

During the third month there is no further change in the amount of assets or liabilities in the three-month time period. On 31 March 20X1 the assets and the swap mature and all balances are recognised in profit or loss.

IE28

Entity A makes the following accounting entries relating to this time period:

IE29

The net effect on profit or loss (excluding interest income and interest expense) is nil reflecting that the hedge is fully effective.

IE30

Entity A makes the following accounting entry to amortise the line item balance for this time period:

Summary

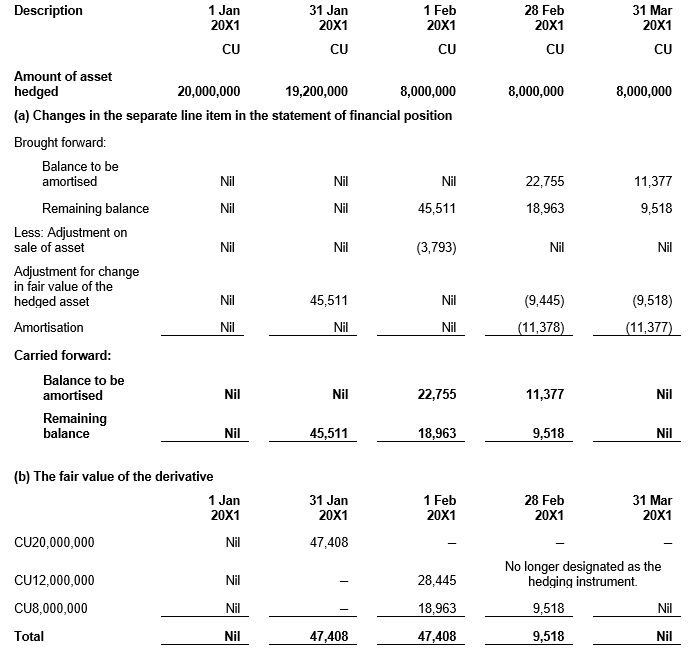

IE31

The tables below summarise:

(a) changes in the separate line item in the statement of financial position;

(b) the fair value of the derivative;

(c) the profit or loss effect of the hedge for the entire three-month period of the hedge; and

(d) interest income and interest expense relating to the amount designated as hedged.