Measurement

46

Current tax liabilities (assets) for the current and prior periods shall be measured at the amount expected to be paid to (recovered from) the taxation authorities, using the tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

47

Deferred tax assets and liabilities shall be measured at the tax rates that are expected to apply to the period when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

48

Current and deferred tax assets and liabilities are usually measured using the tax rates (and tax laws) that have been enacted. However, in some jurisdictions, announcements of tax rates (and tax laws) by the government have the substantive effect of actual enactment, which may follow the announcement by a period of several months. In these circumstances, tax assets and liabilities are measured using the announced tax rate (and tax laws).

49

When different tax rates apply to different levels of taxable income, deferred tax assets and liabilities are measured using the average rates that are expected to apply to the taxable profit (tax loss) of the periods in which the temporary differences are expected to reverse.

50

[Deleted]

51

The measurement of deferred tax liabilities and deferred tax assets shall reflect the tax consequences that would follow from the manner in which the entity expects, at the end of the reporting period, to recover or settle the carrying amount of its assets and liabilities.

51A

In some jurisdictions, the manner in which an entity recovers (settles) the carrying amount of an asset (liability) may affect either or both of:

(a) the tax rate applicable when the entity recovers (settles) the carrying amount of the asset (liability); and

(b) the tax base of the asset (liability).

In such cases, an entity measures deferred tax liabilities and deferred tax assets using the tax rate and the tax base that are consistent with the expected manner of recovery or settlement.

51B

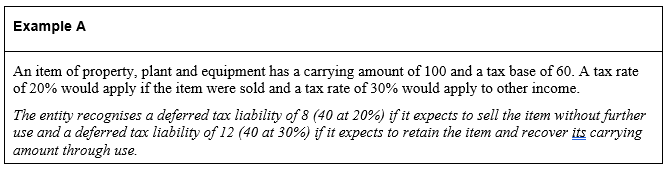

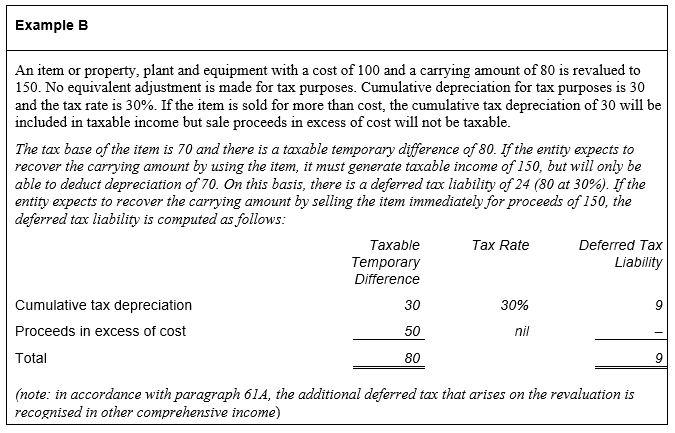

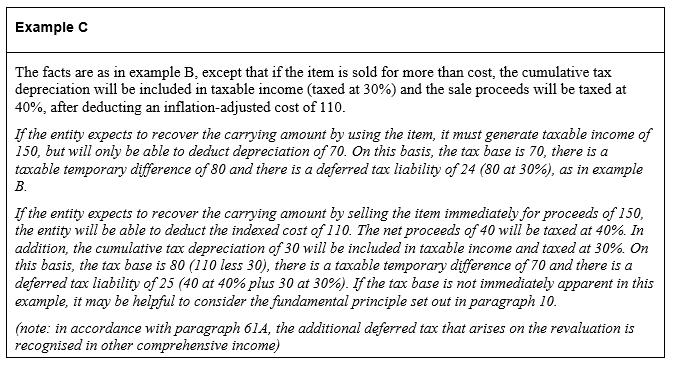

If a deferred tax liability or deferred tax asset arises from a non-depreciable asset measured using the revaluation model in AASB 116, the measurement of the deferred tax liability or deferred tax asset shall reflect the tax consequences of recovering the carrying amount of the non-depreciable asset through sale, regardless of the basis of measuring the carrying amount of that asset. Accordingly, if the tax law specifies a tax rate applicable to the taxable amount derived from the sale of an asset that differs from the tax rate applicable to the taxable amount derived from using an asset, the former rate is applied in measuring the deferred tax liability or asset related to a non-depreciable asset.

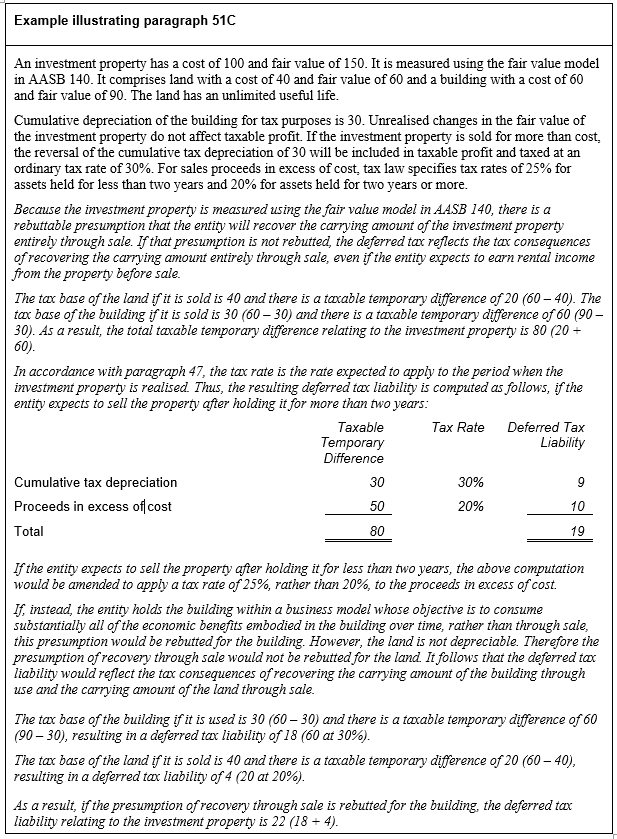

51C

If a deferred tax liability or asset arises from investment property that is measured using the fair value model in AASB 140, there is a rebuttable presumption that the carrying amount of the investment property will be recovered through sale. Accordingly, unless the presumption is rebutted, the measurement of the deferred tax liability or deferred tax asset shall reflect the tax consequences of recovering the carrying amount of the investment property entirely through sale. This presumption is rebutted if the investment property is depreciable and is held within a business model whose objective is to consume substantially all of the economic benefits embodied in the investment property over time, rather than through sale. If the presumption is rebutted, the requirements of paragraphs 51 and 51A shall be followed.

51D

The rebuttable presumption in paragraph 51C also applies when a deferred tax liability or a deferred tax asset arises from measuring investment property in a business combination if the entity will use the fair value model when subsequently measuring that investment property.

51E

Paragraphs 51B–51D do not change the requirements to apply the principles in paragraphs 24–33 (deductible temporary differences) and paragraphs 34–36 (unused tax losses and unused tax credits) of this Standard when recognising and measuring deferred tax assets.

52

[moved and renumbered 51A]

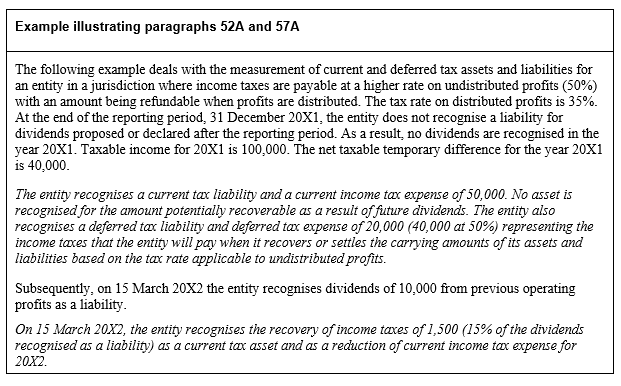

52A

In some jurisdictions, income taxes are payable at a higher or lower rate if part or all of the net profit or retained earnings is paid out as a dividend to shareholders of the entity. In some other jurisdictions, income taxes may be refundable or payable if part or all of the net profit or retained earnings is paid out as a dividend to shareholders of the entity. In these circumstances, current and deferred tax assets and liabilities are measured at the tax rate applicable to undistributed profits.

52B

[Deleted]

53

Deferred tax assets and liabilities shall not be discounted.

54

The reliable determination of deferred tax assets and liabilities on a discounted basis requires detailed scheduling of the timing of the reversal of each temporary difference. In many cases such scheduling is impracticable or highly complex. Therefore, it is inappropriate to require discounting of deferred tax assets and liabilities. To permit, but not to require, discounting would result in deferred tax assets and liabilities which would not be comparable between entities. Therefore, this Standard does not require or permit the discounting of deferred tax assets and liabilities.

55

Temporary differences are determined by reference to the carrying amount of an asset or liability. This applies even where that carrying amount is itself determined on a discounted basis, for example in the case of retirement benefit obligations (see AASB 119 Employee Benefits).

56

The carrying amount of a deferred tax asset shall be reviewed at the end of each reporting period. An entity shall reduce the carrying amount of a deferred tax asset to the extent that it is no longer probable that sufficient taxable profit will be available to allow the benefit of part or all of that deferred tax asset to be utilised. Any such reduction shall be reversed to the extent that it becomes probable that sufficient taxable profit will be available.