The purpose of this Standard is to specify the minimum content of a concise financial report prepared under the Corporations Act 2001.

Preamble

Pronouncement

FOR-PROFIT (FP) ENTITIES

This compiled Standard applies to annual reporting periods beginning on or after 1 January 2018. Earlier application is permitted for annual reporting periods beginning on or after 1 January 2014 but before 1 January 2018.

NOT-FOR-PROFIT (NFP) ENTITIES

This compiled Standard applies to annual reporting periods beginning on or after 1 January 2019. Earlier application is permitted for annual reporting periods beginning on or after 1 January 2014 but before 1 January 2019.

This version of the Standard incorporates relevant amendments made up to and including 9 December 2016.

Prepared on 20 August 2019 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2019

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Requests and enquiries concerning reproduction and rights for commercial purposes should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1039 Concise Financial Reports (as amended) is set out in paragraphs 1 – 37. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 1039 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Accounting Standard AASB 1039

The Australian Accounting Standards Board made Accounting Standard AASB 1039 Concise Financial Reports under section 334 of the Corporations Act 2001 on 27 August 2008.

This compiled version of AASB 1039 applies to annual reporting periods beginning on or after 1 January 2018 for for-profit entities, and to annual reporting periods beginning on or after 1 January 2019 for not-for-profit entities. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 9 December 2016 (see Compilation Details).

Application

1

This Standard applies to a concise financial report prepared by an entity in accordance with paragraph 314(2)(a) in Part 2M.3 of the Corporations Act.

2

Under the Corporations Act a company, registered scheme or disclosing entity can elect to send to its members for a financial year a concise report, which includes a concise financial report, instead of the financial report.

3

Where an entity is the parent of a group, this Standard applies to the consolidated financial statements of the entity and the notes to those statements, and does not require that parent financial information be provided.

4

If the entity provides parent financial information in addition to consolidated financial information, the parent financial information is also subject to the requirements of this Standard.

5

[Deleted by the AASB]

Operative Date

6

This Standard applies to annual reporting periods beginning on or after 1 January 2009.

[Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

7

This Standard may be applied to annual reporting periods beginning on or after 1 January 2005 but before 1 January 2009 provided that AASB 101 Presentation of Financial Statements (September 2007) and AASB 8 Operating Segments are also applied to the period. If an entity adopts this Standard for an earlier period, it shall disclose that fact.

8

When applied or operative, this Standard supersedes AASB 1039 Concise Financial Reports made on 14 April 2005.

Purpose of Standard

9

The purpose of this Standard is to specify the minimum content of a concise financial report.

10

The requirements of the Corporations Act relating to concise financial reports are based on the view that a concise financial report can provide members with information relevant to evaluating the business, without giving them fully detailed accounting disclosures. For some members, the provision of less detailed information is expected to be sufficient to meet their needs for an understanding of the financial performance, financial position and financing and investing activities of the company, registered scheme or disclosing entity.

11

The minimum content required by this Standard is intended also to provide sufficient information to permit members to identify if and when they consider it would be useful to obtain more comprehensive and detailed information by requesting a copy of the financial report.

Preparation and Presentation

12

The financial statements and specific disclosures (identified in paragraphs 28 to 32 of this Standard) required in a concise financial report shall be derived from the financial report of the entity. Any other information included in a concise financial report shall be consistent with the financial report of the entity.

13

In order to achieve consistency and comparability with information included in the financial report, this Standard requires the accounting policies relating to recognition and measurement applied in the preparation of a concise financial report to be the same as those adopted in the preparation of the financial report.

14

This Standard prescribes the minimum information to be disclosed in a concise financial report but does not prescribe the format in which that information is presented. The format for the presentation of information in a concise financial report is developed having regard to the particular circumstances of the entity and the presentation of relevant, reliable, understandable and comparable information about the entity’s financial performance, financial position and financing and investing activities. Entities are encouraged to develop a format that best meets the information needs of their members.

15

The consistency required by paragraph 12 means that information voluntarily included in the concise financial report is determined in accordance with the treatment adopted in the financial report. When the information in the financial report was determined in accordance with an Accounting Standard, the same treatment is adopted in the concise financial report.

16

The nature and estimated magnitude of particular items are disclosed if it is likely that the concise financial report would be misleading without such disclosures.

17

The content of a concise financial report specified in this Standard constitutes the minimum level of disclosure. Where there are particular features of the operations and activities of the entity that are significant, the entity may need to provide additional information in the concise financial report in order to comply with paragraph 16. Similarly, members benefit from industry-specific disclosures, for example, disclosure of additional information by mining companies in relation to exploration and evaluation expenditure and decommissioning costs, and by banks and other financial institutions in relation to doubtful debts.

Financial Statements

18

A concise financial report shall include the following financial statements:

(a) a statement of profit or loss and other comprehensive income for the annual reporting period;

(b) a statement of financial position as at the end of the annual reporting period;

(c) a statement of cash flows for the annual reporting period; and

(d) a statement of changes in equity for the annual reporting period.

19

In accordance with paragraph 10A of AASB 101 Presentation of Financial Statements, an entity may present all items of income and expense recognised in a period in a single statement of profit or loss and other comprehensive income or present the profit or loss section in a separate statement of profit or loss.

20

Each financial statement shall be presented as it is in the financial report, in accordance with other Accounting Standards, except for the omission of cross-references to notes to the financial statements in the financial report.

21

All the notes to the financial statements required by other Accounting Standards are not required in the concise financial report. For example, this Standard does not require an entity that uses the direct method in the statement of cash flows to provide a reconciliation of cash flows arising from operating activities to profit or loss. However, information required in some notes by other Accounting Standards is required when specified in this Standard.

22

It is recommended that the financial statements in the concise financial report be cross-referenced, where appropriate, to disclosures included in the concise financial report.

23

When the entity is a parent and only the consolidated financial statements are presented, the lack of financial statements for the parent would not be regarded as contravening paragraph 21.

24

The financial statements of entities other than listed companies shall be accompanied by discussion and analysis to assist the understanding of members.

25

Listed companies are not required by this Standard to provide discussion and analysis in the concise financial report because, unlike other entities, they are required by section 299A of the Corporations Act to provide an operational and financial report in the Directors’ Report that is part of the concise report. Paragraph 24 only exempts listed companies from the statutory obligation to provide discussion and analysis of the financial statements. It does not prohibit a listed company from providing any discussion and analysis that it considers would assist a reader to understand the financial statements in the concise financial report.

26

The information reported in the financial statements will be enhanced by a discussion and analysis of the principal factors affecting the financial performance, financial position and financing and investing activities of the entity. The extent of the discussion and analysis provided will vary from entity to entity, and from year to year, as is necessary in the circumstances to help compensate for the brevity of the concise financial report compared with the financial report.

27

In most situations, the content of the discussion and analysis would cover at least the following areas:

(a) in relation to the statement of profit or loss and other comprehensive income:

(i) trends in revenues;

(ii) the effects of significant economic or other events on the operations of the entity;

(iii) the main influences on costs of operations; and

(iv) measures of financial performance such as return on sales, return on assets and return on equity;

(b) in relation to the statement of financial position:

(i) changes in the composition of assets;

(ii) the relationship between debt and equity; and

(iii) significant movements in assets, liabilities and equity items;

(c) in relation to the statement of cash flows:

(i) changes in cash flows from operations;

(ii) financing of capital expenditure programs; and

(iii) servicing and repayment of borrowings; and

(d) in relation to the statement of changes in equity:

(i) changes in the composition of the components of equity; and

(ii) causes of significant changes in subscribed capital, such as rights issues, share buy-backs or capital reductions.

Specific Disclosures

28

When the entity has prepared its financial report on the basis that the entity is not a going concern, or where the going concern basis has become inappropriate after the reporting date, this fact shall be disclosed.

29

The following information shall be disclosed for each reportable segment identified in the financial report in accordance with AASB 8 Operating Segments:

(a) revenues from sales to external customers and revenues from transactions with other operating segments of the same entity if the specified amounts are included in the measure of segment profit or loss reviewed by the chief operating decision maker or are otherwise regularly provided to the chief operating decision maker, even if not included in that measure of segment profit or loss;

(b) a measure of profit or loss;

(c) a measure of total assets; and

(d) a measure of liabilities if such amount is regularly provided to the chief operating decision maker.

30

The following items for the period shall be disclosed even if the amounts are zero:

(a) the amount of revenue recognised in accordance with AASB 15 Revenue from Contracts with Customers;

(b) the amount of dividends, in aggregate and per share, in respect of each class of shares included in equity, identifying:

(i) dividends paid during the period and date of payment; and

(ii) dividends proposed or declared before the financial report was authorised for issue, and the expected date of payment, separately identifying, where relevant, those recognised from those not recognised as a distribution to equity holders during the period; and

(c) where the entity is required to comply with AASB 133 Earnings per Share, the amount of basic earnings per share and diluted earnings per share.

31

The following items shall be disclosed:

(a) the presentation currency used;

(b) in respect of each event occurring after the reporting date that does not relate to conditions existing at the reporting date, the information required by paragraph 21 of AASB 110 Events after the Reporting Period; and

(c) where there is a change in accounting policy or estimates from those used in the preceding reporting period, or a correction of a prior period error, which has a material effect in the current reporting period or is expected to have a material effect in a subsequent reporting period, the information required about such a change or correction by the relevant Accounting Standards that are applicable to the current reporting period.

32

The concise financial report for the period when an entity first adopts Australian equivalents to IFRSs shall provide directions as to the location in the financial report of the reconciliations and other disclosures required by paragraphs 39 and 40 of AASB 1 First-time Adoption of Australian Accounting Standards. A summary of this information shall be included in the concise financial report.

Relationship to Financial Report

33

The first page of the concise financial report shall prominently display advice to the effect that:

(a) the concise financial report is an extract from the financial report;

(b) the financial statements and specific disclosures included in the concise financial report have been derived from the financial report;

(c) the concise financial report cannot be expected to provide as full an understanding of the financial performance, financial position and financing and investing activities of the entity as the financial report; and

(d) further financial information can be obtained from the financial report and that the financial report is available, free of charge, on request to the entity.

Comparative Information

34

Any requirements relating to comparative information in other Accounting Standards that have been adopted in the preparation of the financial report are applicable in this Standard.

35

When disclosure is not required with respect to the current reporting period for an item in paragraphs 28 to 32 of this Standard but was required in the preceding reporting period, it is still necessary to disclose the comparative information.

Definitions

36

In this Standard, technical terms have the same meaning as in the relevant Accounting Standards applied in the preparation of the financial report for the current reporting period.

37

The terms ‘concise report’, ‘concise financial report’, ‘financial report’, ‘listed company’ and ‘members’ have the meanings as given or used in Chapter 2M of the Corporations Act.

Compilation details

Accounting Standard AASB 1039 Concise Financial Reports (as amended)

Compilation details are not part of AASB 1039.

This compiled Standard applies to annual reporting periods beginning on or after 1 January 2018 for for-profit entities, and to annual reporting periods beginning on or after 1 January 2019 for not-for-profit entities. It takes into account amendments up to and including 9 December 2016 and was prepared on 20 August 2019 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1039 (August 2008) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

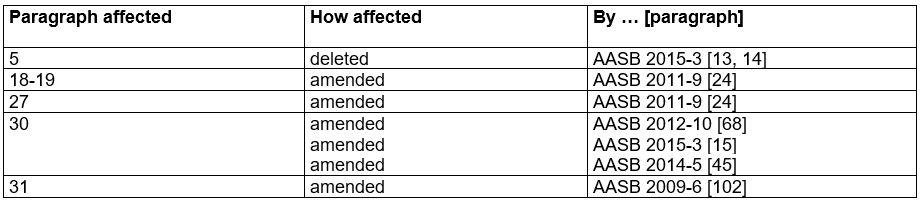

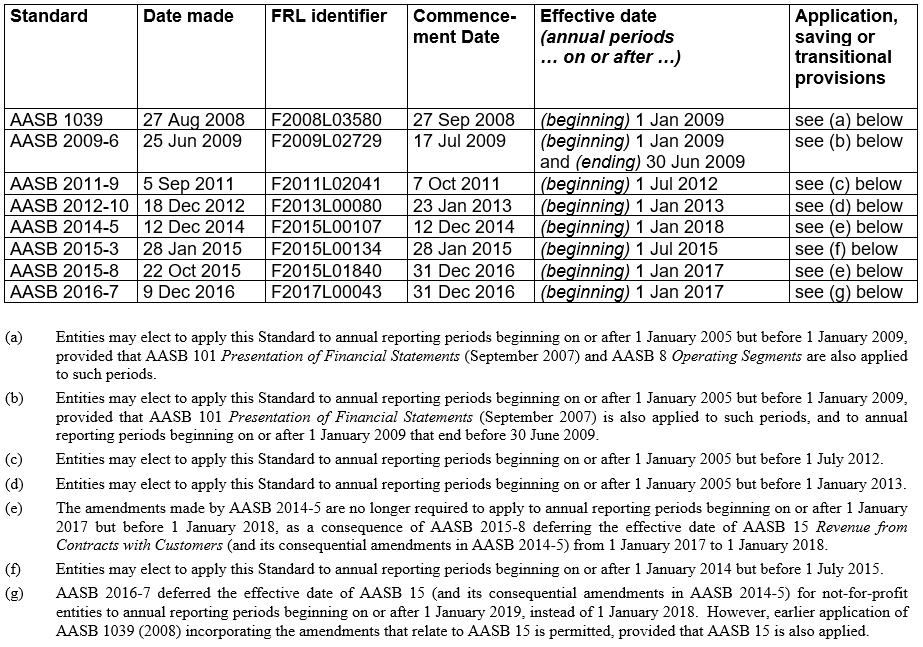

Table of amendments