Illustrative examples

These examples accompany, but are not part of, AASB Interpretation 17.

Scope of the Interpretation (paragraphs 3–8)

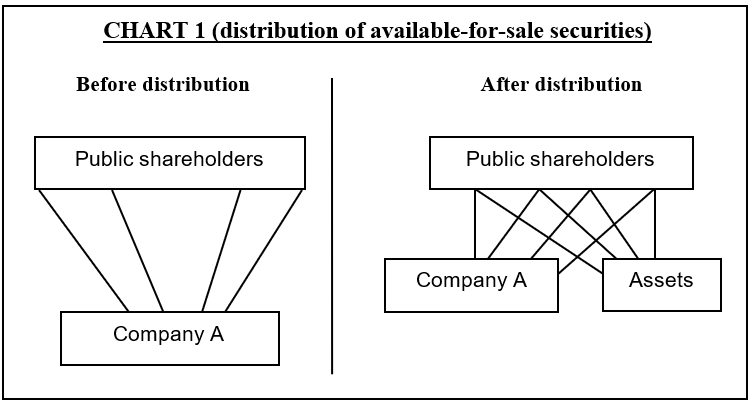

IE1

Assume Company A is owned by public shareholders. No single shareholder controls Company A and no group of shareholders is bound by a contractual agreement to act together to control Company A jointly. Company A distributes certain assets (eg available-for-sale securities) pro rata to the shareholders. This transaction is within the scope of the Interpretation.

IE2

However, if one of the shareholders (or a group bound by a contractual agreement to act together) controls Company A both before and after the transaction, the entire transaction (including the distributions to the non-controlling shareholders) is not within the scope of the Interpretation. This is because in a pro rata distribution to all owners of the same class of equity instruments, the controlling shareholder (or group of shareholders) will continue to control the non-cash assets after the distribution.

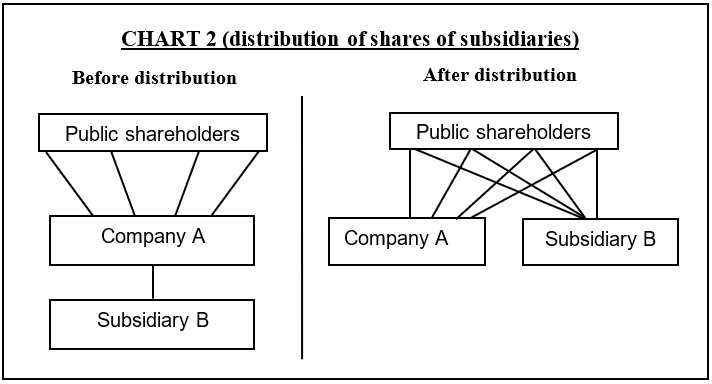

IE3

Assume Company A is owned by public shareholders. No single shareholder controls Company A and no group of shareholders is bound by a contractual agreement to act together to control Company A jointly. Company A owns all of the shares of Subsidiary B. Company A distributes all of the shares of Subsidiary B pro rata to its shareholders, thereby losing control of Subsidiary B. This transaction is within the scope of the Interpretation.

IE4

However, if Company A distributes to its shareholders shares of Subsidiary B representing only a non-controlling interest in Subsidiary B and retains control of Subsidiary B, the transaction is not within the scope of the Interpretation. Company A accounts for the distribution in accordance with AASB 10 Consolidated Financial Statements. Company A controls Company B both before and after the transaction.