Implementation guidance

This implementation guidance accompanies, but is not part of, AASB 1059.

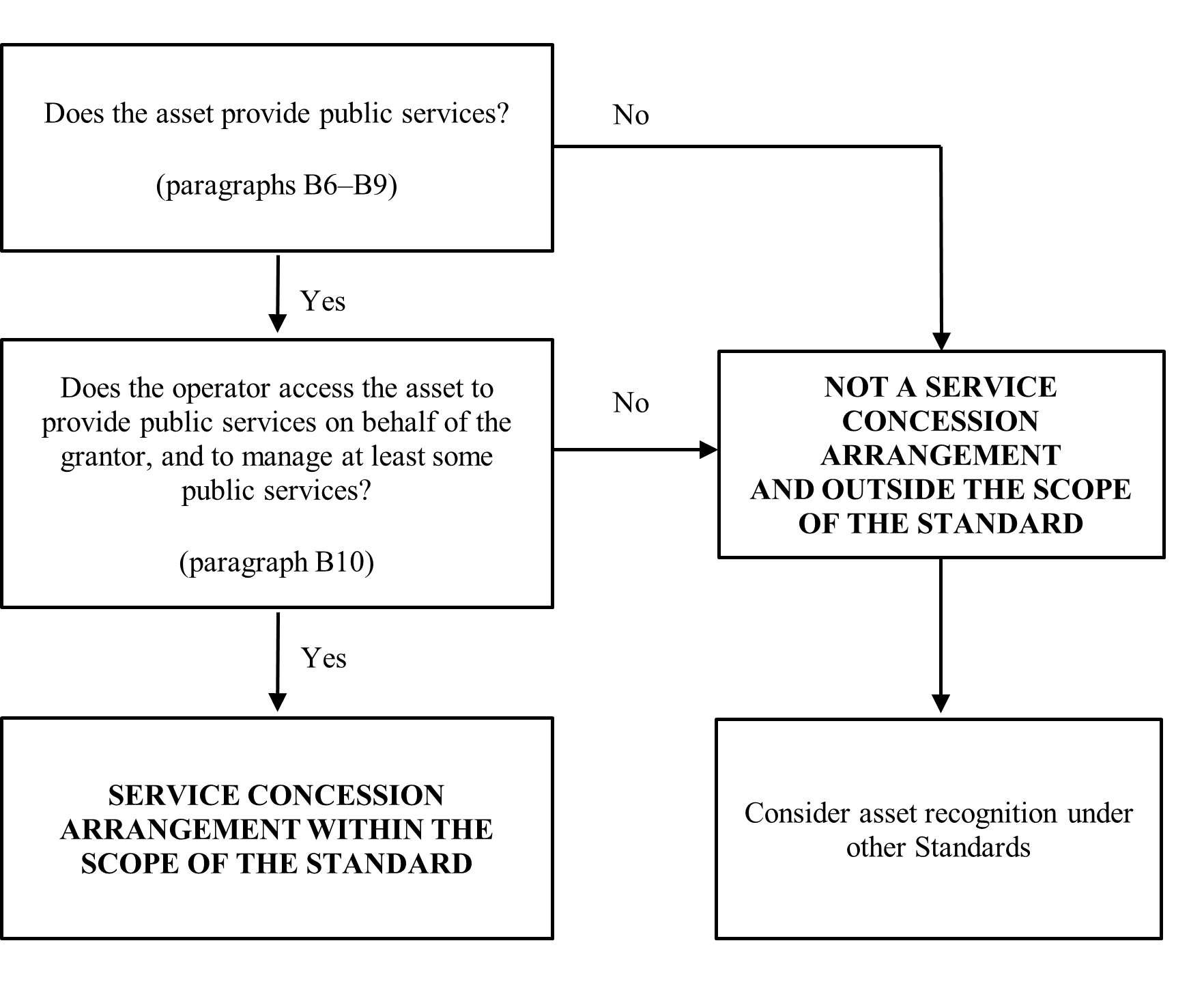

IG1

The purpose of this Implementation Guidance is to illustrate certain aspects of the requirements of AASB 1059. Except in respect of arrangements that are concluded to be service concession arrangements, the implementation guidance identifies the parties to an arrangement as the grantor and the operator for convenience, without reference to the definitions in Appendix A.

Accounting framework for service concession arrangements

IG2

The diagram below summarises some of the key decisions in determining whether an arrangement is a service concession arrangement within the scope of AASB 1059. It does not address the period of time or operator compensation requirements of the definition of a service concession arrangement.

Guidance examples

IG3

The guidance examples below illustrate the key decisions outlined in the diagram in paragraph IG2 for assessing whether an arrangement is a service concession arrangement – and therefore within the scope of AASB 1059, assuming that the period of time and operator compensation requirements are met – in the following circumstances:

(a) the operator provides limited services for the asset; and

(b) the operator has management responsibilities for some services.

Example 1: Limited operator services

IG4

In this example, the relevant terms of the arrangement for assessing whether it is within the scope of AASB 1059 are:

(a) a grantor enters into an arrangement that involves the operator constructing a school;

(b) the school provides public services as the basic purpose of the school is to provide education services that are necessary or essential to the general public. The education services provided by the school are accessible to the public, even if it is a subset of the community that uses the services. The assessment of the public service nature of the school is consistent with paragraph B6;

(c) the grantor is responsible for the services relating to the delivery of education and operational services such as the recruitment of teachers and administration staff, and the maintenance of the school facilities; and

(d) the operator is responsible for cleaning and security services for the school.

IG4

In this example, the relevant terms of the arrangement for assessing whether it is within the scope of AASB 1059 are:

(a) a grantor enters into an arrangement that involves the operator constructing a school;

(b) the school provides public services as the basic purpose of the school is to provide education services that are necessary or essential to the general public. The education services provided by the school are accessible to the public, even if it is a subset of the community that uses the services. The assessment of the public service nature of the school is consistent with paragraph B6;

(c) the grantor is responsible for the services relating to the delivery of education and operational services such as the recruitment of teachers and administration staff, and the maintenance of the school facilities; and

(d) the operator is responsible for cleaning and security services for the school.

IG5

Based on these facts and circumstances, the grantor concludes the operator does not access the school to provide public services as its provision of cleaning and security services does not constitute management of at least some of the public services provided by the school (refer paragraph B10). Accordingly, the arrangement is not a service concession arrangement and is outside the scope of AASB 1059 (paragraph 2). The cleaning and security services represent an outsourced service to the grantor to enable it to provide the public services through the school.

Example 2(a): Facility maintenance at discretion of operator

IG6

In this example, the facts in Example 1 apply, except that the operator is also responsible for maintenance of the school facilities by maintaining the school to a specified condition. The operator has discretion as to when and how it conducts maintenance of the school facilities.

IG6

In this example, the facts in Example 1 apply, except that the operator is also responsible for maintenance of the school facilities by maintaining the school to a specified condition. The operator has discretion as to when and how it conducts maintenance of the school facilities.

IG7

Based on the facts and circumstances, whilst the operator provides maintenance of the school facilities, facility maintenance does not represent a significant component of the public services provided by the school. Therefore, the operator’s responsibility for maintenance does not involve the operator in managing the school services (refer paragraph B10). Accordingly, the arrangement is not a service concession arrangement and is outside the scope of AASB 1059 (paragraph 2). The maintenance services represent an outsourced service to the grantor to enable it to provide the public services through the school.

Example 2(b): Operator has management responsibilities

IG8

In this example, the facts in Example 1 apply, except that the operator is also responsible for certain operational services, in determining how many staff are required and organising classes, teachers and administrative staff, and for maintenance of the school facilities by providing upgrades and maintaining the school to a specified condition. The operator has discretion as to when and how it carries out these responsibilities.

IG8

In this example, the facts in Example 1 apply, except that the operator is also responsible for certain operational services, in determining how many staff are required and organising classes, teachers and administrative staff, and for maintenance of the school facilities by providing upgrades and maintaining the school to a specified condition. The operator has discretion as to when and how it carries out these responsibilities.

IG9

Based on these facts and circumstances, the grantor concludes the operator accesses the school to provide public services and is responsible for at least some of the management of the school services. The operator fulfils this management responsibility through its significant operational and maintenance responsibilities, even though the staff are provided by the grantor (refer paragraph B10). Accordingly, the arrangement is a service concession arrangement within the scope of AASB 1059.

IG10

The diagram below summarises the recognition and measurement requirements for assets (other than goodwill) and service concession arrangements subject to AASB 1059.

References to Australian Accounting Standards that apply to typical types of arrangements involving an asset combined with provision of a service

IG11

The table below sets out the typical types of arrangements for private sector participation in the provision of public sector services and provides references to Accounting Standards that may apply to those arrangements. The list of arrangement types is not exhaustive. The purpose of the table is to highlight the continuum of arrangements. It is not the AASB’s intention to convey the impression that bright lines exist between the accounting requirements for various types of arrangements.

IG12

The shaded text shows arrangements within the scope of AASB 1059.

|

Category |

Lease |

Service provision |

Sale |

|||

|

Typical arrangement types |

Lease (e.g. operator leases asset from grantor) |

Service outsourcing contract (specific tasks eg debt collection) |

Rehabilitate-operate-transfer |

Build-operate-transfer |

Build-own-operate |

100% Divestment/ Privatisation/ Corporation |

|

Asset ownership |

Grantor |

|

Operator |

|||

|

Capital investment |

Grantor |

Operator |

|

|||

|

Demand risk |

Shared |

Grantor |

Grantor and/or Operator |

Operator |

||

|

Typical duration |

8–20 years |

1–5 years |

25-30 years |

|

Indefinite (or may be limited by contract or licence) |

|

|

Significant residual interest |

Grantor |

|

Operator |

|||

|

Relevant |

||||||

IG13

The table below compares the key features of various common types of arrangements for private sector participation in the provision of public services. This table presents simple arrangements, however the classification of an arrangement as a construction contract with a service outsourcing contract, lease, service concession arrangement, or sale or privatisation will depend on the specific terms and conditions of the arrangement.

|

Features |

Construction contract with service outsourcing contract1 |

Lease2 (grantor is lessor) |

Service concession arrangement3 |

Sale/Privatisation4 |

|

Determining whether arrangement is within the scope of AASB 1059 (paragraphs 2, IG2) |

Conclusion (based on analysis below) – Outside the scope of AASB 1059 and grantor controls the asset. |

Conclusion (based on analysis below) – Depending on terms of arrangement, can be outside or within the scope of AASB 1059. |

Conclusion (based on analysis below) – Within the scope of AASB 1059 and grantor controls the asset. |

Conclusion (based on analysis below) – Outside the scope of AASB 1059 and grantor does not control the asset. |

|

Operator provides public services related to the asset on behalf of the grantor and is responsible for the management of at least some of the public services (paragraph B10)? |

Operator provides construction services. Operator acts as an agent in providing public services and related services as predetermined by the grantor |

Operator involvement in the management of the public services and related services varies, depending on the lease terms (ie operator may have full involvement or be limited to facility management that is not a significant component of the public services provided by the asset). |

Operator involved in management of public services provided by the asset that is not predetermined by grantor (ie operator has discretion as to how the public services are provided and managed). |

Operator does not provide public services on behalf of the grantor, despite any protective rights of the grantor. |

|

Determining whether grantor controls the asset for recognition as service concession asset (paragraph 5(a)) |

Grantor controls or regulates all three aspects. |

Operator typically controls all three aspects in a lease, but grantor might control or regulate some. |

Grantor controls or regulates all three aspects. |

Grantor might control or regulate any of these aspects (especially pricing) but not all three aspects. |

|

Grantor controls or regulates services provided by operator with the asset? |

Grantor controls or regulates services. |

Operator typically controls services. |

Grantor controls or regulates services. |

Operator typically controls services. |

|

Grantor controls or regulates recipients of services? |

Grantor controls recipients of services. |

Operator typically controls recipients of services. |

Grantor controls recipients of services. |

Operator typically controls recipients of services. |

|

Grantor controls or regulates pricing of services? |

Grantor controls pricing of services. |

Operator typically controls pricing of services. |

Grantor controls pricing of services. |

Operator might not control pricing of services. |

|

Grantor controls underlying use of the asset? |

Grantor controls the asset and the right to use the asset. |

Operating lease: Grantor (lessor) retains control of the asset and operator (lessee) has right-of-use asset. Finance lease: Grantor (lessor) relinquishes control of asset to operator (lessee): · lessor derecognises asset and recognises receivable · lessee recognises right-of-use asset. |

Grantor retains control of asset and the right to use the asset. Operator only has a right to access the asset. |

Operator controls the asset and the right to use the asset. |

|

Determining whether grantor controls any significant residual interest in the asset at the end of the arrangement (paragraph 5(b)) |

Grantor controls any significant residual interest at end of arrangement. |

Depending on terms of arrangement, grantor or operator might control residual interest in the asset. |

Grantor controls any significant residual interest at end of arrangement. |

Depending on terms of arrangement, grantor or operator might control residual interest in the asset. |

|

Grantor controls any significant residual interest at end of arrangement? |

Grantor controls any significant residual interest at end of arrangement. |

Operating lease: Grantor (lessor) controls significant residual interest. Finance lease: No significant residual interest expected. |

Grantor controls any significant residual interest at end of arrangement. |

Sale: No significant residual interest expected. Privatisation: Grantor may control any significant residual interest. |

|

Grantor’s interest restricts operator’s practical ability to sell or pledge asset (paragraph B33)? |

Operator has no ability to sell or pledge the asset. |

Operating lease: Grantor’s (lessor’s) interest restricts operator’s (lessee’s) practical ability to sell or pledge asset. Finance lease: Protective rights of the grantor (lessor) typically define the scope of the operator’s (lessee’s) right of use. |

Grantor’s interest restricts operator’s practical ability to sell or pledge asset. |

Sale: Not applicable. Privatisation: Grantor’s interest restricts operator’s practical ability to sell or pledge asset. |

|

Relevant Accounting Standards |

AASB 1059 |

|||

|

NOTES: 1 A construction contract with a service outsourcing contract is a contract for the construction of an asset or a combination of assets with provision of services over a specified period. 2 A lease is a contract that conveys the right to use a specified asset for a period of time in exchange for consideration (as defined in AASB 16). 3 A service concession arrangement is a contract between a grantor and an operator in which the operator has the right to access the service concession asset to provide public services on behalf of the grantor, the operator is responsible for at least some of the management of the public services, and the operator is compensated for the services over the period of the service concession arrangement (as defined in AASB 1059). 4 A sale or privatisation is an arrangement that transfers the asset and its related services from public to private ownership/ control. |

||||

Guidance examples

IG14

The guidance examples below illustrate the features of the types of arrangements for private sector participation in the provision of public services that are outlined in the table in paragraph IG13:

(a) an arrangement that is a construction contract with a service contract;

(b) an arrangement that contains a lease;

(c) an arrangement that contains a service concession arrangement that is partly regulated and partly unregulated; and

(d) an arrangement that is a sale or privatisation.

Example 3: Construction contract with limited operator services

IG15

This example illustrates an arrangement that involves the operator agreeing to construct an asset or group of assets (a school) for the grantor with a contract for the provision of cleaning and security services over a specified period of time. The example is based on the facts and circumstances in Example 1 (paragraphs IG4–IG5). The grantor:

(a) in accordance with paragraph 2 – determines the arrangement for the construction of the school and the provision of the services is outside the scope of AASB 1059, consistent with paragraphs IG4–IG5; and

(b) assesses whether it controls the school or has a right to use the school for recognition under another Accounting Standard. In making this assessment, the grantor considers that:

• the services the operator provides with the school would be based on the service contract agreed by the grantor and the operator; and

• the control of or right to use the asset would depend on the service contract, including who has title to the land on which the school is built, the terms of the arrangement and the disposition of any residual interest.

IG15

This example illustrates an arrangement that involves the operator agreeing to construct an asset or group of assets (a school) for the grantor with a contract for the provision of cleaning and security services over a specified period of time. The example is based on the facts and circumstances in Example 1 (paragraphs IG4–IG5). The grantor:

(a) in accordance with paragraph 2 – determines the arrangement for the construction of the school and the provision of the services is outside the scope of AASB 1059, consistent with paragraphs IG4–IG5; and

(b) assesses whether it controls the school or has a right to use the school for recognition under another Accounting Standard. In making this assessment, the grantor considers that:

• the services the operator provides with the school would be based on the service contract agreed by the grantor and the operator; and

• the control of or right to use the asset would depend on the service contract, including who has title to the land on which the school is built, the terms of the arrangement and the disposition of any residual interest.

Example 4: Lease and service concession arrangement – regulated and unregulated

IG16

Example 4 illustrates an arrangement that involves the operator agreeing to construct an asset or group of assets for the grantor with a contract for the provision of services or maintenance (including facilities maintenance) of the asset(s) over a specified period of time. The arrangement is partly regulated and unregulated by the grantor. The relevant terms of the arrangement are:

(a) a grantor enters into an arrangement that involves the operator constructing a hospital and then maintaining the hospital buildings. The grantor determines the hospital is capable of being operated with separately identifiable public and private wings;

(b) the public wing of the hospital is expected to provide health services to the general public for no cost to the patients. The grantor is responsible for the services relating to the delivery of medical services and operational services, including setting key performance requirements, but the operator is responsible for the employment of the doctors, nurses and administration staff and scheduling the various services;

(c) the private wing of the hospital is expected to provide health services to private patients of the hospital. The operator is responsible for the services relating to the delivery of medical services and operational services, including the employment of doctors, nurses and administration staff. The operator also determines the pricing of the services charged to patients;

(d) the hospital is considered to provide public services, as the basic purpose of the hospital is to provide health services that are necessary or essential to the general public. The health services provided by the hospital are accessible to the public, even if it is a subset of the community that uses the services and notwithstanding that the private wing of the hospital is to be used by private patients. The assessment of the public service nature of the hospital is consistent with paragraph B6;

(e) the operator is responsible for the cleaning and security services and facility maintenance of both the public wing and the private wing of the hospital. The operator has discretion as to when and how it conducts the facility maintenance of providing upgrades and maintenance of the hospital to a specified condition;

(f) the grantor is entitled to the residual interest in both the public wing and the private wing of the hospital at the end of the term of the arrangement, as both wings will transfer to the grantor. During the term of the arrangement, the grantor’s residual interest and the requirement for the grantor to specifically approve any transferee restricts the operator from selling or pledging the hospital; and

(g) both the public and private wings are built on government land, leased to the operator for a nominal fee.

IG16

Example 4 illustrates an arrangement that involves the operator agreeing to construct an asset or group of assets for the grantor with a contract for the provision of services or maintenance (including facilities maintenance) of the asset(s) over a specified period of time. The arrangement is partly regulated and unregulated by the grantor. The relevant terms of the arrangement are:

(a) a grantor enters into an arrangement that involves the operator constructing a hospital and then maintaining the hospital buildings. The grantor determines the hospital is capable of being operated with separately identifiable public and private wings;

(b) the public wing of the hospital is expected to provide health services to the general public for no cost to the patients. The grantor is responsible for the services relating to the delivery of medical services and operational services, including setting key performance requirements, but the operator is responsible for the employment of the doctors, nurses and administration staff and scheduling the various services;

(c) the private wing of the hospital is expected to provide health services to private patients of the hospital. The operator is responsible for the services relating to the delivery of medical services and operational services, including the employment of doctors, nurses and administration staff. The operator also determines the pricing of the services charged to patients;

(d) the hospital is considered to provide public services, as the basic purpose of the hospital is to provide health services that are necessary or essential to the general public. The health services provided by the hospital are accessible to the public, even if it is a subset of the community that uses the services and notwithstanding that the private wing of the hospital is to be used by private patients. The assessment of the public service nature of the hospital is consistent with paragraph B6;

(e) the operator is responsible for the cleaning and security services and facility maintenance of both the public wing and the private wing of the hospital. The operator has discretion as to when and how it conducts the facility maintenance of providing upgrades and maintenance of the hospital to a specified condition;

(f) the grantor is entitled to the residual interest in both the public wing and the private wing of the hospital at the end of the term of the arrangement, as both wings will transfer to the grantor. During the term of the arrangement, the grantor’s residual interest and the requirement for the grantor to specifically approve any transferee restricts the operator from selling or pledging the hospital; and

(g) both the public and private wings are built on government land, leased to the operator for a nominal fee.

IG17

The grantor assesses separately (consistent with paragraphs B6–B7) whether the public wing and the private wing are within the scope of AASB 1059.

Hospital – Public wing (regulated)

Scope

IG18

Based on the facts and circumstances, the grantor determines:

(a) the operator accesses the public wing of the hospital to provide public services and is responsible for at least some of the management of the hospital services. The operator fulfils this management responsibility by employing the staff and scheduling services; and

(b) the public wing of the hospital is a service concession arrangement that is within the scope of AASB 1059, in accordance with paragraph 2.

Grantor’s control of asset for recognition under paragraph 5

IG19

Based on the facts and circumstances, the grantor determines it controls the underlying asset (the public wing of the hospital) in the service concession arrangement, as the arrangement entered into by the grantor and the operator specifies:

(a) the grantor controls or regulates (as required by paragraph 5(a)):

- the services provided by the public wing of the hospital – the grantor is responsible for the delivery and standard of performance of the medical and operational services;

- the recipients of the services – the public wing of the hospital is expected to provide health services to the general public; and

- the pricing of the services – the public wing of the hospital is to provide health services at no cost to the patients; and

(b) the grantor controls the significant residual interest in the asset (the public wing of the hospital) at the end of the arrangement in accordance with paragraph 5(b), as the grantor is entitled to this residual interest. Additionally, during the term of the arrangement, the operator is restricted from selling or pledging the public wing of the hospital (refer paragraphs B32–B33).

Recognition of arrangement

IG20

Given the public wing of the hospital is within the scope of AASB 1059 (paragraph 2) and the grantor controls the asset in accordance with paragraphs 5(a) and (b), the grantor recognises the public wing of the hospital provided by the operator as a service concession asset.

Hospital – Private wing (unregulated)

Scope

IG21

Based on the facts and circumstances, the grantor determines:

(a) the operator uses the private wing of the hospital to provide services to private patients of the hospital. The operator is also responsible for the management of the private wing by providing the medical and operational services and staff; and

(b) the private wing of the hospital is not a service concession arrangement, in accordance with paragraph 2, because the services in the private wing are not being provided to the public on behalf of a public sector entity.

Recognition of arrangement

IG22

Notwithstanding the grantor cannot recognise the private wing of the hospital as a service concession asset, the grantor assesses whether it controls the asset (the private wing of the hospital) under another Accounting Standard, such as AASB 16. In this example, as the grantor controls the land on which the private wing is located, which provides legal control of the private wing, and the operator is prevented from selling or pledging its interest in the private wing, the grantor controls the private wing. However, the arrangement provides the operator with the right to use the private wing, because the private wing is a separately identifiable asset and the operator controls the services provided, which patients will be admitted, and the prices to be charged during the specified arrangement term. Accordingly:

(a) where the grantor retains substantially all the risks and rewards incidental to ownership, the grantor is the lessor in an operating lease; or

(b) where the operator has substantially all the risks and rewards incidental to ownership, the grantor derecognises the asset and recognises a receivable in accordance with the accounting for a finance lease.

IG23

In this example, the wings of the hospital are capable of being separated into a public wing (regulated portion) and a private wing (unregulated portion). However, some service concession arrangements may involve a hospital that is partly regulated and partly unregulated based on the number of patients that are admitted as a public patient or a private patient, instead of being physically separate as per paragraph IG16(a). In such circumstances, judgement will be required as to the relative significance of the regulated versus unregulated activities in order to determine whether the grantor has control of the asset and/or has granted a right of use to the operator. For example, if the hospital admissions are expected to comprise substantially public patients, then the admission of private patients would be considered as ancillary (unregulated) activities of the hospital and the hospital considered to be used wholly for regulated purposes in addressing the accounting for the service concession asset. In addition, a lease from the grantor to the operator requires a specifically identifiable asset with a right of use granted for a specified time, so in these circumstances it is unlikely a lease could be identified.

Example 5(a): Sale

IG24

This example illustrates an arrangement that involves a public sector entity (a State Government – the grantor) selling an asset (electricity distribution business) to a private sector entity (the operator). The relevant terms of the arrangement are:

(a) in exchange for the sale of the electricity distribution business, the grantor receives cash relating to the sale of its interest in the net assets of the business, and settlement by the operator of the liabilities of the business;

(b) the operator is able to operate the electricity distribution business subject to regulation by a third-party regulator of electricity distributors. Additionally, although the operator has discretion to set the prices of the electricity services, the operator must seek the third-party regulator’s approval for changes in pricing; and

(c) the operator controls:

- the operating activities of the electricity distribution business, including decisions to expand or modify the distribution network or to continue providing electricity services, subject to protective rights of the grantor to ensure electricity supply in certain circumstances. If the operator decides to discontinue providing electricity services, the grantor has an option to buy back the business from the operator at fair value; and

- the recipients of the services – the operator can expand the distribution network beyond the network existing at the time of entering the contract without requiring the grantor’s approval.

IG24

This example illustrates an arrangement that involves a public sector entity (a State Government – the grantor) selling an asset (electricity distribution business) to a private sector entity (the operator). The relevant terms of the arrangement are:

(a) in exchange for the sale of the electricity distribution business, the grantor receives cash relating to the sale of its interest in the net assets of the business, and settlement by the operator of the liabilities of the business;

(b) the operator is able to operate the electricity distribution business subject to regulation by a third-party regulator of electricity distributors. Additionally, although the operator has discretion to set the prices of the electricity services, the operator must seek the third-party regulator’s approval for changes in pricing; and

(c) the operator controls:

- the operating activities of the electricity distribution business, including decisions to expand or modify the distribution network or to continue providing electricity services, subject to protective rights of the grantor to ensure electricity supply in certain circumstances. If the operator decides to discontinue providing electricity services, the grantor has an option to buy back the business from the operator at fair value; and

- the recipients of the services – the operator can expand the distribution network beyond the network existing at the time of entering the contract without requiring the grantor’s approval.

Scope

IG25

Based on the facts and circumstances, the grantor concludes the arrangement for the electricity distribution business is outside the scope of AASB 1059 (paragraph 2) – although electricity distribution would be regarded as public services, the operator does not provide the services on behalf of the grantor and the arrangement is not for a specific period of time. The grantor’s protective rights do not mean that the operator provides the services on behalf of the grantor. The protective rights would have the same impact as for an operator that had developed its own electricity network rather than purchasing it from a grantor – the rights do not give the grantor control of the distribution network.

Grantor’s control of asset for recognition

IG26

The grantor would also be unable to recognise a service concession asset in these circumstances, because the grantor is able to control or regulate only some of the aspects addressed in paragraph 5(a), as follows:

(a) the grantor controls the pricing of the services provided by the operator, as the requirement for the operator to seek approval from the third-party regulator removes the operator’s ability to regulate the pricing and, for the purpose of paragraph 5(a), the pricing of the services is therefore considered to be set implicitly by the grantor (refer paragraph B20);

(b) the operator controls the services to be provided by the business. The grantor’s protective rights and option to buy back the business from the operator, in the event the operator decides to discontinue the provision of electricity services, do not prevent the operator determining the services to be provided; and

(c) the operator controls the recipients of the services as outlined in paragraph IG24(c).

IG27

There is no residual interest in the arrangement, as the sale is not limited to a specified period, and so the grantor would also not satisfy the requirements of paragraph 5(b). Furthermore, the grantor’s buy-back option is exercisable only at fair value and so does not give the grantor any significant residual interest. As the asset need not be used for the provision of public services for its entire remaining economic life (the operator has discretion as to how to use the asset) and the criteria in paragraph 5(a) are not met, the conditions in paragraph 6 for a whole-of-life asset are not met.

IG28

Although the grantor cannot recognise a service concession asset, the grantor assesses whether it controls the electricity distribution network, has the right to use the network, or controls any other rights requiring recognition under another Accounting Standard. In making this assessment, the grantor takes into account the factors noted in the previous paragraphs.

Recognition of arrangement

IG29

Based on the assessment in paragraphs IG26–IG27, the grantor determines that it does not control the asset or have a right to use the asset subsequent to the sale of the electricity distribution business. The grantor therefore derecognises the asset under another Accounting Standard, such as AASB 116.

Example 5(b): Privatisation

IG30

In this example, the facts in Example 5(a) apply, except that:

(a) the State Government (the grantor) enters into an arrangement with a private sector entity (the operator) to operate the electricity distribution business for 100 years, instead of the operator purchasing the business from the grantor; and

(b) at the end of the arrangement (ie in 100 years’ time), the distribution network reverts to the grantor. The operator must maintain the electricity distribution network to the specified age and condition at the end of the arrangement.

IG30

In this example, the facts in Example 5(a) apply, except that:

(a) the State Government (the grantor) enters into an arrangement with a private sector entity (the operator) to operate the electricity distribution business for 100 years, instead of the operator purchasing the business from the grantor; and

(b) at the end of the arrangement (ie in 100 years’ time), the distribution network reverts to the grantor. The operator must maintain the electricity distribution network to the specified age and condition at the end of the arrangement.

IG31

Based on the facts and circumstances, the grantor determines:

(a) the arrangement for the operator to operate the electricity distribution network is outside the scope of AASB 1059, as the grantor’s protective rights to ensure electricity supply in certain circumstances do not mean that the operator provides the services on behalf of the grantor;

(b) even if the arrangement was a service concession arrangement, it does not control the asset for recognition under paragraph 5(a), for the reasons outlined in paragraphs IG26(a)–(c); and

(c) it controls the significant residual interest at the end of the arrangement, as the electricity distribution network reverts to the grantor at the end of the arrangement. Accordingly, the arrangement is a privatisation and not a sale.

IG32

Based on the assessment in the previous paragraph, the grantor determines that it does not control the asset (the electricity distribution network) or have a right to use the asset under the arrangement. The grantor’s protective rights do not give the grantor any more significant interest in the distribution network than it would have with those same rights in relation to an operator that had developed its own network. The grantor therefore derecognises the asset under another Accounting Standard, such as AASB 116, and determines whether it controls any other rights requiring recognition under another Accounting Standard.