This Interpretation clarifies how to apply the recognition and measurement requirements in AASB 112 when there is uncertainty over income tax treatments.

Preamble

Pronouncement

This compiled Interpretation applies to annual periods beginning on or after 1 July 2021. Earlier application is permitted for annual periods beginning before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Interpretations

Compiled versions of Interpretations, original Interpretations and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This compiled AASB Interpretation contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

AASB Interpretation 23 Uncertainty over Income Tax Treatments (as amended) is set out in paragraphs 1 – 14 and Appendices A – C. Interpretations are listed in Australian Accounting Standard AASB 1048 Interpretation of Standards and AASB 1057 Application of Australian Accounting Standards sets out their application. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IFRIC 23

AASB Interpretation 23 Uncertainty over Income Tax Treatments as amended incorporates Interpretation IFRIC 23 Uncertainty over Income Tax Treatments as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IFRIC 23) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB Interpretation 23 also comply with IFRIC 23.

Not-for-profit entities’ compliance with IFRIC 23 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IFRIC 23.

Tier 2

Entities preparing general purpose financial statements under Australian Accounting Standards – Simplified Disclosures (Tier 2) will not be in compliance with IFRS Standards.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

AASB Interpretation 23

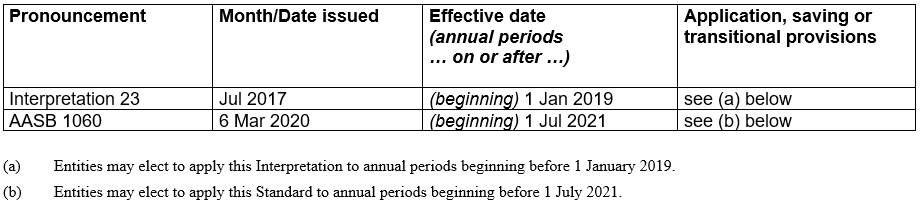

Interpretation 23 was issued in July 2017.

This compiled version of Interpretation 23 applies to annual periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB pronouncements up to and including 6 March 2020 (see Compilation Details).

Background

2

It may be unclear how tax law applies to a particular transaction or circumstance. The acceptability of a particular tax treatment under tax law may not be known until the relevant taxation authority or a court takes a decision in the future. Consequently, a dispute or examination of a particular tax treatment by the taxation authority may affect an entity’s accounting for a current or deferred tax asset or liability.

3

In this Interpretation:

(a) ‘tax treatments’ refers to the treatments used by an entity or that it plans to use in its income tax filings.

(b) ‘taxation authority’ refers to the body or bodies that decide whether tax treatments are acceptable under tax law. This might include a court.

(c) an ‘uncertain tax treatment’ is a tax treatment for which there is uncertainty over whether the relevant taxation authority will accept the tax treatment under tax law. For example, an entity’s decision not to submit any income tax filing in a tax jurisdiction, or not to include particular income in taxable profit, is an uncertain tax treatment if its acceptability is uncertain under tax law.

Scope

4

This Interpretation clarifies how to apply the recognition and measurement requirements in AASB 112 when there is uncertainty over income tax treatments. In such a circumstance, an entity shall recognise and measure its current or deferred tax asset or liability applying the requirements in AASB 112 based on taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates determined applying this Interpretation.

Issues

5

When there is uncertainty over income tax treatments, this Interpretation addresses:

(a) whether an entity considers uncertain tax treatments separately;

(b) the assumptions an entity makes about the examination of tax treatments by taxation authorities;

(c) how an entity determines taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates; and

(d) how an entity considers changes in facts and circumstances.

Consensus

Whether an entity considers uncertain tax treatments separately

6

An entity shall determine whether to consider each uncertain tax treatment separately or together with one or more other uncertain tax treatments based on which approach better predicts the resolution of the uncertainty. In determining the approach that better predicts the resolution of the uncertainty, an entity might consider, for example, (a) how it prepares its income tax filings and supports tax treatments; or (b) how the entity expects the taxation authority to make its examination and resolve issues that might arise from that examination.

7

If, applying paragraph 6, an entity considers more than one uncertain tax treatment together, the entity shall read references to an ‘uncertain tax treatment’ in this Interpretation as referring to the group of uncertain tax treatments considered together.

Examination by taxation authorities

8

In assessing whether and how an uncertain tax treatment affects the determination of taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates, an entity shall assume that a taxation authority will examine amounts it has a right to examine and have full knowledge of all related information when making those examinations.

Determination of taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates

9

An entity shall consider whether it is probable that a taxation authority will accept an uncertain tax treatment.

10

If an entity concludes it is probable that the taxation authority will accept an uncertain tax treatment, the entity shall determine the taxable profit (tax loss), tax bases, unused tax losses, unused tax credits or tax rates consistently with the tax treatment used or planned to be used in its income tax filings.

11

If an entity concludes it is not probable that the taxation authority will accept an uncertain tax treatment, the entity shall reflect the effect of uncertainty in determining the related taxable profit (tax loss), tax bases, unused tax losses, unused tax credits or tax rates. An entity shall reflect the effect of uncertainty for each uncertain tax treatment by using either of the following methods, depending on which method the entity expects to better predict the resolution of the uncertainty:

(a) the most likely amount—the single most likely amount in a range of possible outcomes. The most likely amount may better predict the resolution of the uncertainty if the possible outcomes are binary or are concentrated on one value.

(b) the expected value—the sum of the probability-weighted amounts in a range of possible outcomes. The expected value may better predict the resolution of the uncertainty if there is a range of possible outcomes that are neither binary nor concentrated on one value.

12

If an uncertain tax treatment affects current tax and deferred tax (for example, if it affects both taxable profit used to determine current tax and tax bases used to determine deferred tax), an entity shall make consistent judgements and estimates for both current tax and deferred tax.

Changes in facts and circumstances

13

An entity shall reassess a judgement or estimate required by this Interpretation if the facts and circumstances on which the judgement or estimate was based change or as a result of new information that affects the judgement or estimate. For example, a change in facts and circumstances might change an entity’s conclusions about the acceptability of a tax treatment or the entity’s estimate of the effect of uncertainty, or both. Paragraphs A1–A3 set out guidance on changes in facts and circumstances.

14

An entity shall reflect the effect of a change in facts and circumstances or of new information as a change in accounting estimate applying AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. An entity shall apply AASB 110 Events after the Reporting Period to determine whether a change that occurs after the reporting period is an adjusting or non-adjusting event.

Appendix A -- Application Guidance

This appendix is an integral part of AASB Interpretation 23 and has the same authority as the other parts of Interpretation 23.

Changes in facts and circumstances (paragraph 13)

A1

In applying paragraph 13 of this Interpretation, an entity shall assess the relevance and effect of a change in facts and circumstances or of new information in the context of applicable tax laws. For example, a particular event might result in the reassessment of a judgement or estimate made for one tax treatment but not another, if those tax treatments are subject to different tax laws.

A2

Examples of changes in facts and circumstances or new information that, depending on the circumstances, can result in the reassessment of a judgement or estimate required by this Interpretation include, but are not limited to, the following:

(a) examinations or actions by a taxation authority. For example:

(i) agreement or disagreement by the taxation authority with the tax treatment or a similar tax treatment used by the entity;

(ii) information that the taxation authority has agreed or disagreed with a similar tax treatment used by another entity; and

(iii) information about the amount received or paid to settle a similar tax treatment.

(b) changes in rules established by a taxation authority.

(c) the expiry of a taxation authority’s right to examine or re-examine a tax treatment.

A3

The absence of agreement or disagreement by a taxation authority with a tax treatment, in isolation, is unlikely to constitute a change in facts and circumstances or new information that affects the judgements and estimates required by this Interpretation.

Disclosure

A4

When there is uncertainty over income tax treatments, an entity shall determine whether to disclose:

(a) judgements made in determining taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates applying paragraph 122 of AASB 101 Presentation of Financial Statements; and

(b) information about the assumptions and estimates made in determining taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates applying paragraphs 125–129 of AASB 101.

A5

If an entity concludes it is probable that a taxation authority will accept an uncertain tax treatment, the entity shall determine whether to disclose the potential effect of the uncertainty as a tax-related contingency applying paragraph 88 of AASB 112.

Appendix B -- Effective date and transition

This appendix is an integral part of Interpretation 23 and has the same authority as the other parts of Interpretation 23.

Effective date

B1

An entity shall apply this Interpretation for annual reporting periods beginning on or after 1 January 2019. Earlier application is permitted. If an entity applies this Interpretation for an earlier period, it shall disclose that fact.

Transition

B2

On initial application, an entity shall apply this Interpretation either:

(a) retrospectively applying AASB 108, if that is possible without the use of hindsight; or

(b) retrospectively with the cumulative effect of initially applying the Interpretation recognised at the date of initial application. If an entity selects this transition approach, it shall not restate comparative information. Instead, the entity shall recognise the cumulative effect of initially applying the Interpretation as an adjustment to the opening balance of retained earnings (or other component of equity, as appropriate). The date of initial application is the beginning of the annual reporting period in which an entity first applies this Interpretation.

Appendix C -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusC1

Paragraphs A4 and A5 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Illustrative examples

These examples accompany, but are not part of, Interpretation 23.

IE1

These examples portray hypothetical situations illustrating how an entity might apply some of the requirements in Interpretation 23 based on the limited facts presented. In all the examples, as required by paragraph 8 of Interpretation 23, the entity has assumed that the taxation authority will examine amounts it has a right to examine and have full knowledge of all related information when making those examinations.

Example 1—The expected value method is used to reflect the effect of uncertainty for tax treatments considered together

IE2

Entity A’s income tax filing in a jurisdiction includes deductions related to transfer pricing. The taxation authority may challenge those tax treatments. In the context of applying AASB 112, the uncertain tax treatments affect only the determination of taxable profit for the current period.

IE3

Entity A notes that the taxation authority’s decision on one transfer pricing matter would affect, or be affected by, the other transfer pricing matters. Applying paragraph 6 of Interpretation 23, Entity A concludes that considering the tax treatments of all transfer pricing matters in the jurisdiction together better predicts the resolution of the uncertainty. Entity A also concludes it is not probable that the taxation authority will accept the tax treatments. Consequently, Entity A reflects the effect of the uncertainty in determining its taxable profit applying paragraph 11 of Interpretation 23.

IE4

Entity A estimates the probabilities of the possible additional amounts that might be added to its taxable profit, as follows:

|

|

|

Estimated additional amount, CU(a) |

|

Probability, % |

|

Estimate of expected value, CU |

|

|

|

Outcome 1 |

|

– |

|

5% |

|

– |

|

|

|

Outcome 2 |

|

200 |

|

5% |

|

10 |

|

|

|

Outcome 3 |

|

400 |

|

20% |

|

80 |

|

|

|

Outcome 4 |

|

600 |

|

20% |

|

120 |

|

|

|

Outcome 5 |

|

800 |

|

30% |

|

240 |

|

|

|

Outcome 6 |

|

1,000 |

|

20% |

|

200 |

|

|

|

|

|

|

|

100% |

|

650 |

|

|

|

(a) In these Illustrative Examples, currency amounts are denominated in ‘currency units’ (CU) |

|

|||||||

IE5

Outcome 5 is the most likely outcome. However, Entity A observes that there is a range of possible outcomes that are neither binary nor concentrated on one value. Consequently, Entity A concludes that the expected value of CU650 better predicts the resolution of the uncertainty.

IE6

Accordingly, Entity A recognises and measures its current tax liability applying AASB 112 based on taxable profit that includes CU650 to reflect the effect of the uncertainty. The amount of CU650 is in addition to the amount of taxable profit reported in its income tax filing.

Example 2—The most likely amount method is used to reflect the effect of uncertainty when recognising and measuring deferred tax and current tax

IE7

Entity B acquires for CU100 a separately identifiable intangible asset that has an indefinite life and, therefore, is not amortised applying AASB 138 Intangible Assets. The tax law specifies that the full cost of the intangible asset is deductible for tax purposes, but the timing of deductibility is uncertain. Applying paragraph 6 of Interpretation 23, Entity B concludes that considering this tax treatment separately better predicts the resolution of the uncertainty.

IE8

Entity B deducts CU100 (the cost of the intangible asset) in calculating taxable profit for Year 1 in its income tax filing. At the end of Year 1, Entity B concludes it is not probable that the taxation authority will accept the tax treatment. Consequently, Entity B reflects the effect of the uncertainty in determining its taxable profit and the tax base of the intangible asset applying paragraph 11 of Interpretation 23. Entity B concludes the most likely amount that the taxation authority will accept as a deductible amount for Year 1 is CU10 and that the most likely amount better predicts the resolution of the uncertainty.

IE9

Accordingly, in recognising and measuring its deferred tax liability applying AASB 112 at the end of Year 1, Entity B calculates a taxable temporary difference based on the most likely amount of the tax base of CU90 (CU100 – CU10) to reflect the effect of the uncertainty, instead of the tax base calculated based on Entity B’s income tax filing (CU0).

IE10

Similarly, as required by paragraph 12 of Interpretation 23, Entity B reflects the effect of the uncertainty in determining taxable profit for Year 1 using judgements and estimates that are consistent with those used to calculate the deferred tax liability. Entity B recognises and measures its current tax liability applying AASB 112 based on taxable profit that includes CU90 (CU100 – CU10). The amount of CU90 is in addition to the amount of taxable profit included in its income tax filing. This is because Entity B deducted CU100 in calculating taxable profit for Year 1, whereas the most likely amount of the deduction is CU10.

Compilation details

AASB Interpretation 23 Uncertainty over Income Tax Treatments (as amended)

Compilation details are not part of Interpretation 23.

This compiled Interpretation applies to annual periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Interpretation issued by the AASB. Instead, it is a representation of Interpretation 23 (July 2017) as amended by other Accounting Standards, which are listed in the table below.

Table of pronouncements

Table of amendments

Basis for Conclusions on IFRIC 23

Uncertainty over Income Tax Treatments

This Basis for Conclusions accompanies, but is not part of, AASB Interpretation 23. An IFRIC Basis for Conclusions may be amended to reflect any additional requirements in the AASB Interpretation or AASB Accounting Standards.

Background

BC1

The Committee received a question asking when it is appropriate for entities to recognise a current tax asset if tax laws require entities to make payments in respect of a disputed tax treatment. In the circumstance the question described, the entity intended to appeal a tax ruling.

BC2

IAS 12 Income Taxes includes requirements on recognition and measurement of tax assets and liabilities, but does not specify how to reflect uncertainty. The Committee observed that entities apply diverse reporting methods when the application of tax law is uncertain.

BC3

Accordingly, in October 2015 the Committee published a draft Interpretation Uncertainty over Income Tax Treatments for public comment. It received 61 comment letters. The Committee considered the comments received in developing this Interpretation.

Scope

BC4

The question that the Committee received related to a particular circumstance in which an entity is required to make a payment to a taxation authority in respect of a disputed income tax treatment. However, in discussing the issue, the Committee noted that a similar question could arise in other circumstances in which there is uncertainty over income tax treatments. Consequently, the Committee decided that the Interpretation should address the accounting for income taxes whenever tax treatments involve uncertainty that affects the application of IAS 12. Respondents to the draft Interpretation generally supported the scope that the Committee proposed.

BC5

Uncertainty over income tax treatments may affect both current and deferred tax. For example, the timing of deductibility of the cost of an intangible asset under tax law may be uncertain and this may affect both taxable profit and the tax base of the asset, which in turn affects the determination of current and deferred tax respectively. The Committee decided to require a consistent approach to reflecting the effect of uncertainty for both current and deferred tax; therefore, the Interpretation applies in determining both current and deferred tax.

BC6

The Committee developed the Interpretation as an interpretation of IAS 12, ie the requirements in the Interpretation add to, and complement, the requirements in IAS 12. The Committee decided not to expand the scope of the Interpretation to taxes or levies outside the scope of IAS 12 because it was concerned that a wider scope might create conflicts within IFRS Standards.

Interest and penalties

BC7

IAS 12 does not explicitly refer to interest and penalties payable to, or receivable from, a taxation authority, nor are they explicitly referred to in other IFRS Standards.

BC8

A number of respondents to the draft Interpretation suggested that the Interpretation explicitly include interest and penalties associated with uncertain tax treatments within its scope. Some said that entities account for interest and penalties differently depending on whether they apply IAS 12 or IAS 37 Provisions, Contingent Liabilities and Contingent Assets to those amounts.

BC9

The Committee decided not to add to the Interpretation requirements relating to interest and penalties associated with uncertain tax treatments. Rather, the Committee noted that if an entity considers a particular amount payable or receivable for interest and penalties to be an income tax, then that amount is within the scope of IAS 12 and, when there is uncertainty, also within the scope of this Interpretation. Conversely, if an entity does not apply IAS 12 to a particular amount payable or receivable, then this Interpretation does not apply to that amount, regardless of whether there is uncertainty.

Consensus

Whether an entity considers uncertain tax treatments separately

BC10

The amount of a tax asset or liability could be affected by whether an entity considers each uncertain tax treatment separately or together with one or more other uncertain tax treatments. Consequently, the Committee decided to include the requirement in paragraph 6 of the Interpretation in this respect. The Committee noted that an entity may need to use judgement in applying that requirement.

Examination by taxation authorities

BC11

The Committee decided that an entity should assume a taxation authority will examine amounts it has a right to examine and have full knowledge of all related information. In making this decision, the Committee noted that paragraphs 46–47 of IAS 12 require an entity to measure tax assets and liabilities based on tax laws that have been enacted or substantively enacted.

BC12

A few respondents to the draft Interpretation suggested that an entity consider the probability of examination, instead of assuming that an examination will occur. These respondents said such a probability assessment would be particularly important if there is no time limit on the taxation authority’s right to examine income tax filings.

BC13

The Committee decided not to change the examination assumption, nor create an exception to it for circumstances in which there is no time limit on the taxation authority’s right to examine income tax filings. Almost all respondents to the draft Interpretation supported the examination assumption. The Committee also noted that the assumption of examination by the taxation authority, in isolation, would not require an entity to reflect the effects of uncertainty. The threshold for reflecting the effects of uncertainty is whether it is probable that the taxation authority will accept an uncertain tax treatment. In other words, the recognition of uncertainty is not determined based on whether a taxation authority examines a tax treatment.

Determination of taxable profit (tax loss), tax bases, unused tax losses, unused tax credits and tax rates

When to reflect the effect of uncertainty

BC14

Paragraph 24 of IAS 12 requires the recognition of deferred tax assets to the extent that it is probable that an entity will be able to use deductible temporary differences against taxable profit. The objective of IAS 12 also refers to a probable threshold in the context of deferred tax. In addition, although IAS 12 does not include an explicit recognition threshold for current tax, paragraph 14 of IAS 12 implies that a probable threshold applies to current tax assets arising from a tax loss.

BC15

Consequently, the Committee decided that an entity should reflect the effect of uncertainty in accounting for current and deferred tax when the entity concludes it is not probable that the taxation authority will accept an uncertain tax treatment (and thus, it is probable that the entity will receive or pay amounts relating to the uncertain tax treatment).

BC16

The Committee concluded that setting this explicit threshold for the recognition of the effect of uncertainty will increase comparability among entities and reduce some of the costs of measurement.

How to reflect the effect of uncertainty

BC17

To reflect the effect of uncertainty, the Committee decided that an entity should use the expected value or the most likely amount, whichever method better predicts the resolution of the uncertainty. This approach is similar to the approach used in IFRS 15 Revenue from Contracts with Customers to estimate the amount of variable consideration in a revenue contract.

BC18

The Committee considered whether to permit or require the use of a third measurement method, such as a ‘cumulative-probability approach’ (ie the measurement method used to reflect uncertainty over income tax treatments in US Generally Accepted Accounting Principles). The Committee observed that the inclusion of a third method would have complicated the judgements that need to be made in applying the Interpretation. This is because an entity would have had to assess which of three measurement methods best predicts the resolution of the uncertainty. The Committee also noted that IFRS Standards do not use the cumulative-probability approach, whereas the expected value and the most likely amount are used elsewhere in the Standards. Including a measurement method not used elsewhere in the Standards might have reduced comparability.

BC19

Consequently, the Committee decided not to permit or require a third measurement method to reflect the effects of uncertainty.

Changes in facts and circumstances

BC20

Considering uncertainty over income tax treatments means it is necessary to make estimates, and such estimation involves judgements based on available information. The information available to an entity about uncertain tax treatments can change over time. Consequently, the Committee decided that an entity should reassess a judgement or estimate required by the Interpretation when related facts and circumstances change.

BC21

The Committee also decided that an entity should reflect the effect of any changes in its judgements or estimates consistently with the requirements in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors for changes in accounting estimates.

Disclosure

BC22

IAS 1 Presentation of Financial Statements and IAS 12 provide disclosure requirements that may be relevant when there is uncertainty over income tax treatments. Consequently, instead of introducing new disclosure requirements, the Committee decided to highlight those existing requirements in the Interpretation.

Business combinations

BC23

The Committee considered whether the Interpretation should address the accounting for tax assets and liabilities acquired or assumed in a business combination when there is uncertainty over income tax treatments. The Committee noted that IFRS 3 Business Combinations applies to all assets acquired and liabilities assumed in a business combination. Consequently, the Committee concluded that the Interpretation should not explicitly address tax assets and liabilities acquired or assumed in a business combination.

BC24

Nonetheless, paragraph 24 of IFRS 3 requires an entity to account for deferred tax assets and liabilities that arise as part of a business combination applying IAS 12. Accordingly, the Interpretation applies to such assets and liabilities when there is uncertainty over income tax treatments that affect deferred tax.

Transition

BC25

The Committee observed that retrospective application of the Interpretation without the use of hindsight would often be impossible for entities. Consequently, the Committee decided not to require the restatement of comparative information when an entity first applies the Interpretation. However, the Committee concluded that an entity should not be prevented from applying the Interpretation retrospectively if it is able to do so without the use of hindsight. Consequently, the Committee decided to permit retrospective application if that is possible without the use of hindsight.

First-time adopters

BC26

The Committee observed that if a first-time adopter’s date of transition IFRS Standards is before the date the Interpretation is issued, the first-time adopter may face the same hindsight difficulties as entities that already apply IFRS Standards. Consequently, the Committee decided not to require first-time adopters whose date of transition to IFRS Standards is before 1 July 2017 to present in their first IFRS financial statements comparative information that reflects this Interpretation.