This Interpretation applies to non-reciprocal distributions of assets by an entity to its owners acting in their capacity as owners, including distributions of non-cash assets (eg items of property, plant and equipment, businesses as defined in AASB 3, ownership interests in another entity or disposal groups as defined in AASB 5) and distributions that give owners a choice of receiving either non-cash assets or a cash alternative.

Preamble

Pronouncement

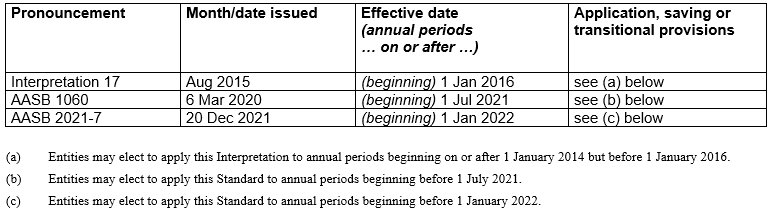

This compiled Interpretation applies to annual periods beginning on or after 1 January 2022. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 January 2022. It incorporates relevant amendments made up to and including 20 December 2021.

Prepared on 7 April 2022 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Interpretations

Compiled versions of Interpretations, original Interpretations and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2022

This compiled AASB Interpretation contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

AASB Interpretation 17 Distributions of Non-cash Assets to Owners (as amended) is set out in paragraphs 1 – Aus18.1 and Appendix A. Interpretations are listed in Australian Accounting Standard AASB 1048 Interpretation of Standards and AASB 1057 Application of Australian Accounting Standards sets out their application. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IFRIC 17

AASB Interpretation 17 Distributions of Non-cash Assets to Owners as amended incorporates Interpretation IFRIC 17 Distributions of Non-cash Assets to Owners as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IFRIC 17) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB Interpretation 17 also comply with IFRIC 17.

Not-for-profit entities’ compliance with IFRIC 17 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IFRIC 17.

Tier 2

Entities preparing general purpose financial statements under Australian Accounting Standards – Simplified Disclosures (Tier 2) will not be in compliance with IFRS Standards.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

AASB Interpretation 17

Interpretation 17 was issued in August 2015.

This compiled version of Interpretation 17 applies to annual periods beginning on or after 1 January 2022. It incorporates relevant amendments contained in other AASB pronouncements up to and including 20 December 2021 (see Compilation Details).

References

• AASB 3 Business Combinations

• AASB 5 Non-current Assets Held for Sale and Discontinued Operations

• AASB 7 Financial Instruments: Disclosures

• AASB 10 Consolidated Financial Statements

• AASB 13 Fair Value Measurement

• AASB 101 Presentation of Financial Statements

• AASB 110 Events after the Reporting Period

Background

1

Sometimes an entity distributes assets other than cash (non-cash assets) as dividends to its owners[1] acting in their capacity as owners. In those situations, an entity may also give its owners a choice of receiving either non-cash assets or a cash alternative. Constituents have requested guidance on how an entity should account for such distributions.

2

Australian Accounting Standards do not provide guidance on how an entity should measure distributions to its owners (commonly referred to as dividends). AASB 101 requires an entity to present details of dividends recognised as distributions to owners either in the statement of changes in equity or in the notes to the financial statements.

Paragraph 7 of AASB 101 defines owners as holders of instruments classified as equity.

Scope

3

This Interpretation applies to the following types of non-reciprocal distributions of assets by an entity to its owners acting in their capacity as owners:

(a) distributions of non-cash assets (eg items of property, plant and equipment, businesses as defined in AASB 3, ownership interests in another entity or disposal groups as defined in AASB 5); and

(b) distributions that give owners a choice of receiving either non-cash assets or a cash alternative.

4

This Interpretation applies only to distributions in which all owners of the same class of equity instruments are treated equally.

5

This Interpretation does not apply to a distribution of a non-cash asset that is ultimately controlled by the same party or parties before and after the distribution. This exclusion applies to the separate, individual and consolidated financial statements of an entity that makes the distribution.

6

In accordance with paragraph 5, this Interpretation does not apply when the non-cash asset is ultimately controlled by the same parties both before and after the distribution. Paragraph B2 of AASB 3 states that ‘A group of individuals shall be regarded as controlling an entity when, as a result of contractual arrangements, they collectively have the power to govern its financial and operating policies so as to obtain benefits from its activities.’ Therefore, for a distribution to be outside the scope of this Interpretation on the basis that the same parties control the asset both before and after the distribution, a group of individual shareholders receiving the distribution must have, as a result of contractual arrangements, such ultimate collective power over the entity making the distribution.

7

In accordance with paragraph 5, this Interpretation does not apply when an entity distributes some of its ownership interests in a subsidiary but retains control of the subsidiary. The entity making a distribution that results in the entity recognising a non-controlling interest in its subsidiary accounts for the distribution in accordance with AASB 10.

8

This Interpretation addresses only the accounting by an entity that makes a non-cash asset distribution. It does not address the accounting by shareholders who receive such a distribution.

Issues

9

When an entity declares a distribution and has an obligation to distribute the assets concerned to its owners, it must recognise a liability for the dividend payable. Consequently, this Interpretation addresses the following issues:

(a) When should the entity recognise the dividend payable?

(b) How should an entity measure the dividend payable?

(c) When an entity settles the dividend payable, how should it account for any difference between the carrying amount of the assets distributed and the carrying amount of the dividend payable?

Consensus

When to recognise a dividend payable

10

The liability to pay a dividend shall be recognised when the dividend is appropriately authorised and is no longer at the discretion of the entity, which is the date:

(a) when declaration of the dividend, eg by management or the board of directors, is approved by the relevant authority, eg the shareholders, if the jurisdiction requires such approval, or

(b) when the dividend is declared, eg by management or the board of directors, if the jurisdiction does not require further approval.

Measurement of a dividend payable

11

An entity shall measure a liability to distribute non-cash assets as a dividend to its owners at the fair value of the assets to be distributed.

12

If an entity gives its owners a choice of receiving either a non-cash asset or a cash alternative, the entity shall estimate the dividend payable by considering both the fair value of each alternative and the associated probability of owners selecting each alternative.

13

At the end of each reporting period and at the date of settlement, the entity shall review and adjust the carrying amount of the dividend payable, with any changes in the carrying amount of the dividend payable recognised in equity as adjustments to the amount of the distribution.

Accounting for any difference between the carrying amount of the assets distributed and the carrying amount of the dividend payable when an entity settles the dividend payable

14

When an entity settles the dividend payable, it shall recognise the difference, if any, between the carrying amount of the assets distributed and the carrying amount of the dividend payable in profit or loss.

Presentation and disclosures

15

An entity shall present the difference described in paragraph 14 as a separate line item in profit or loss.

16

An entity shall disclose the following information, if applicable:

(a) the carrying amount of the dividend payable at the beginning and end of the period; and

(b) the increase or decrease in the carrying amount recognised in the period in accordance with paragraph 13 as result of a change in the fair value of the assets to be distributed.

17

If, after the end of a reporting period but before the financial statements are authorised for issue, an entity declares a dividend to distribute a non-cash asset, it shall disclose:

(a) the nature of the asset to be distributed;

(b) the carrying amount of the asset to be distributed as of the end of the reporting period; and

(c) the fair value of the asset to be distributed as of the end of the reporting period, if it is different from its carrying amount, and the information about the method(s) used to measure that fair value required by paragraphs 93(b), (d), (g) and (i) and 99 of AASB 13.

Effective date

18

[Deleted by the AASB]

Aus18.1

An entity shall apply this Interpretation for annual periods beginning on or after 1 January 2016. Earlier application is permitted for periods beginning on or after 1 January 2014 but before 1 January 2016. If an entity applies this Interpretation for a period beginning before 1 January 2016, it shall disclose that fact.

19–20

[Deleted by the AASB]

Appendix A -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Interpretation.

AusA1

Paragraphs 16 and 17 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Illustrative examples

These examples accompany, but are not part of, AASB Interpretation 17.

Scope of the Interpretation (paragraphs 3–8)

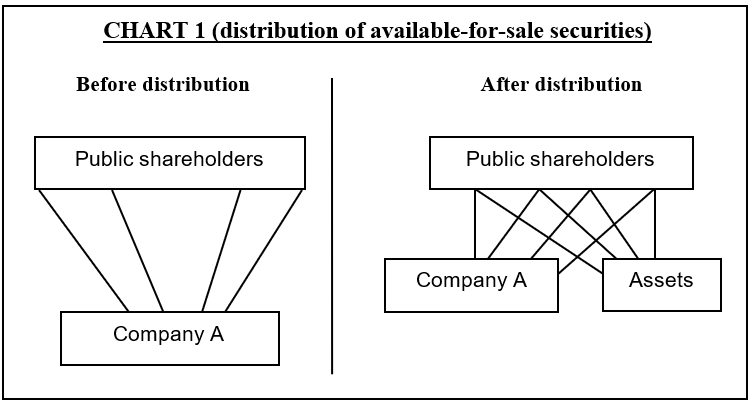

IE1

Assume Company A is owned by public shareholders. No single shareholder controls Company A and no group of shareholders is bound by a contractual agreement to act together to control Company A jointly. Company A distributes certain assets (eg available-for-sale securities) pro rata to the shareholders. This transaction is within the scope of the Interpretation.

IE2

However, if one of the shareholders (or a group bound by a contractual agreement to act together) controls Company A both before and after the transaction, the entire transaction (including the distributions to the non-controlling shareholders) is not within the scope of the Interpretation. This is because in a pro rata distribution to all owners of the same class of equity instruments, the controlling shareholder (or group of shareholders) will continue to control the non-cash assets after the distribution.

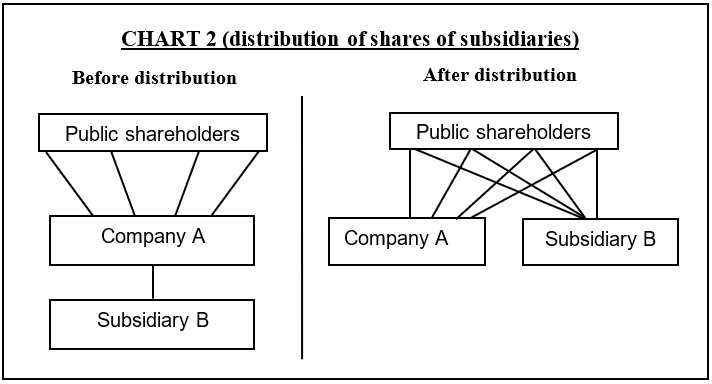

IE3

Assume Company A is owned by public shareholders. No single shareholder controls Company A and no group of shareholders is bound by a contractual agreement to act together to control Company A jointly. Company A owns all of the shares of Subsidiary B. Company A distributes all of the shares of Subsidiary B pro rata to its shareholders, thereby losing control of Subsidiary B. This transaction is within the scope of the Interpretation.

IE4

However, if Company A distributes to its shareholders shares of Subsidiary B representing only a non-controlling interest in Subsidiary B and retains control of Subsidiary B, the transaction is not within the scope of the Interpretation. Company A accounts for the distribution in accordance with AASB 10 Consolidated Financial Statements. Company A controls Company B both before and after the transaction.

Compilation details

AASB Interpretation 17 Distributions of Non-cash Assets to Owners (as amended)

Compilation details are not part of Interpretation 17.

This compiled Interpretation applies to annual periods beginning on or after 1 January 2022. It takes into account amendments up to and including 20 December 2021 and was prepared on 7 April 2022 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Interpretation issued by the AASB. Instead, it is a representation of Interpretation 17 (August 2015) as amended by other pronouncements, which are listed in the table below.

Table of pronouncements

Table of amendments

Basis for Conclusions on IFRIC 17

IFRIC 17 Distributions of Non-cash Assets to Owners

This Basis for Conclusions accompanies, but is not part of, AASB Interpretation 17. An IFRIC Basis for Conclusions may be amended to reflect any additional requirements in the AASB Interpretation or AASB Accounting Standards.

Introduction

BC1

This Basis for Conclusions summarises the IFRIC’s considerations in reaching its consensus. Individual IFRIC members gave greater weight to some factors than to others.

BC2

At present, International Financial Reporting Standards (IFRSs) do not address how an entity should measure distributions to owners acting in their capacity as owners (commonly referred to as dividends). The IFRIC was told that there was significant diversity in practice in how entities measured distributions of non-cash assets.

BC3

The IFRIC published draft Interpretation D23 Distributions of Non-cash Assets to Owners for public comment in January 2008 and received 56 comment letters in response to its proposals.

Scope (paragraphs 3–8)

Should the Interpretation address all transactions between an entity and its owners?

BC4

The IFRIC noted that an asset distribution by an entity to its owners is an example of a transaction between an entity and its owners. Transactions between an entity and its owners can generally be categorised into the following three types:

(a) exchange transactions between an entity and its owners.

(b) non-reciprocal transfers of assets by owners of an entity to the entity. Such transfers are commonly referred to as contributions from owners.

(c) non-reciprocal transfers of assets by an entity to its owners. Such transfers are commonly referred to as distributions to owners.

BC5

The IFRIC concluded that the Interpretation should not address exchange transactions between an entity and its owners because that would probably result in addressing all related party transactions. In the IFRIC’s view, such a scope was too broad for an Interpretation. Instead, the IFRIC concluded that the Interpretation should focus on distributions of assets by an entity to its owners acting in their capacity as owners.

BC6

In addition, the IFRIC decided that the Interpretation should not address distributions in which owners of the same class of equity instrument are not all treated equally. This is because, in the IFRIC’s view, such distributions might imply that at least some of the owners receiving the distributions indeed gave up something to the entity and/or other owners. In other words, such distributions might be more in the nature of exchange transactions.

Should the Interpretation address all types of asset distributions?

BC7

The IFRIC was told that there was significant diversity in the measurement of the following types of non-reciprocal distributions of assets by an entity to its owners acting in their capacity as owners:

(a) distributions of non-cash assets (eg items of property, plant and equipment, businesses as defined in IFRS 3, ownership interests in another entity or disposal groups as defined in IFRS 5 Non-current Assets Held for Sale and Discontinued Operations) to its owners; and

(b) distributions that give owners a choice of receiving either non-cash assets or a cash alternative.

BC8

The IFRIC noted that all distributions have the same purpose, ie to distribute assets to an entity’s owners. It therefore concluded that the Interpretation should address the measurement of all types of asset distributions with one exception set out in paragraph 5 of the Interpretation.

A scope exclusion: a distribution of an asset that is ultimately controlled by the same party or parties before and after the distribution

BC9

In the Interpretation, the IFRIC considered whether it should address how an entity should measure a distribution of an asset (eg an ownership interest in a subsidiary) that is ultimately controlled by the same party or parties before and after the distribution. In many instances, such a distribution is for the purpose of group restructuring (eg separating two different businesses into two different subgroups). After the distribution, the asset is still controlled by the same party or parties.

BC9

In the Interpretation, the IFRIC considered whether it should address how an entity should measure a distribution of an asset (eg an ownership interest in a subsidiary) that is ultimately controlled by the same party or parties before and after the distribution. In many instances, such a distribution is for the purpose of group restructuring (eg separating two different businesses into two different subgroups). After the distribution, the asset is still controlled by the same party or parties.

BC10

In addition, the IFRIC noted that dealing with the accounting for a distribution of an asset within a group would require consideration of how a transfer of any asset within a group should be accounted for in the separate or individual financial statements of group entities.

BC11

For the reasons described in paragraphs BC9 and BC10, the IFRIC concluded that the Interpretation should not deal with a distribution of an asset that is ultimately controlled by the same party or parties before and after the distribution.

BC12

In response to comments received on the draft Interpretation, the IFRIC redeliberated whether the scope of the Interpretation should be expanded to include a distribution of an asset that is ultimately controlled by the same party or parties before and after the distribution. The IFRIC decided not to expand the scope of the Interpretation in the light of the Board’s decision to add a project to its agenda to address common control transactions.

BC13

The IFRIC noted that many commentators believed that most distributions of assets to an entity’s owners would be excluded from the scope of the Interpretation by paragraph 5. The IFRIC did not agree with this conclusion. It noted that in paragraph B2 of IFRS 3 Business Combinations (as revised in 2008), the Board concluded that a group of individuals would be regarded as controlling an entity only when, as a result of contractual arrangements, they collectively have the power to govern its financial and operating policies so as to obtain benefits from its activities. In addition, in Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate in May 2008, the Board clarified in the amendments to IAS 27 Consolidated and Separate Financial Statements that the distribution of equity interests in a new parent to shareholders in exchange for their interests in the existing parent was not a common control transaction.[2]

The consolidation guidance was removed from IAS 27 and the Standard was renamed Separate Financial Statements by IFRS 10 Consolidated Financial Statements issued in May 2011. The accounting requirements for transactions between owners did not change.

BC14

Consequently, the IFRIC decided that the Interpretation should clarify that unless there is a contractual arrangement among shareholders to control the entity making the distribution, transactions in which the shares or the businesses of group entities are distributed to shareholders outside the group (commonly referred to as a spin-off, split-off or demerger) are not transactions between entities or businesses under common control. Therefore they are within the scope of the Interpretation.

BC15

Some commentators on D23 were concerned about situations in which an entity distributes some but not all of its ownership interests in a subsidiary and retains control. They believed that the proposed accounting for the distribution of ownership interests representing a non-controlling interest in accordance with D23 was inconsistent with the requirements of IAS 27 (as amended in 2008). That IFRS requires changes in a parent’s ownership interest in a subsidiary that do not result in a loss of control to be accounted for as equity transactions. The IFRIC had not intended the Interpretation to apply to such transactions so did not believe it conflicted with the requirements of IAS 27. As a result of the concerns expressed, the IFRIC amended the Interpretation to make this clear.

BC16

Some commentators on D23 were also concerned about situations in which a subsidiary with a non-controlling interest distributes assets to both the parent and the non-controlling interests. They questioned why only the distribution to the controlling entity is excluded from the scope of the Interpretation. The IFRIC noted that when the parent controls the subsidiary before and after the transaction, the entire transaction (including the distribution to the non-controlling interest) is not within the scope of the Interpretation and is accounted for in accordance with IAS 27.

BC17

Distributions to owners may involve significant portions of an entity’s operations. In such circumstances, sometimes referred to as split-off, some commentators on D23 were concerned that it would be difficult to determine which of the surviving entities had made the distribution. They thought that it might be possible for each surviving entity to recognise the distribution of the other. The IFRIC agreed with commentators that identifying the distributing entity might require judgement in some circumstances. However, the IFRIC concluded that the distribution could be recognised in only one entity’s financial statements.

When to recognise a dividend payable (paragraph 10) and amendment to IAS 10

BC18

D23 did not address when an entity should recognise a liability for a dividend payable and some respondents asked the IFRIC to clarify this issue. The IFRIC noted that in IAS 10 Events after the Reporting Period paragraph 13 states that ‘If dividends are declared (ie the dividends are appropriately authorised and no longer at the discretion of the entity) after the reporting period but before the financial statements are authorised for issue, the dividends are not recognised as a liability at the end of the reporting period because no obligation exists at that time.’

BC19

Some commentators stated that in many jurisdictions a commonly held view is that the entity has discretion until the shareholders approve the dividend. Therefore, constituents holding this view believe a conflict exists between ‘declared’ and the explanatory phrase in the brackets in IAS 10 paragraph 13. This is especially true when the sentence is interpreted as ‘declared by management but before the shareholders’ approval’. The IFRIC concluded that the point at which a dividend is appropriately authorised and no longer at the discretion of the entity will vary by jurisdiction.

BC20

Therefore, as a consequence of this Interpretation the IFRIC decided to recommend that the Board amend IAS 10 to remove the perceived conflict in paragraph 13. The IFRIC also noted that the principle on when to recognise a dividend was in the wrong place within the IASB’s authoritative documents. The Board agreed with the IFRIC’s conclusions and amended IAS 10 as part of its approval of the Interpretation. The Board confirmed that this Interpretation had not changed the principle on when to recognise a dividend payable; however, the principle was moved from IAS 10 into the Interpretation and clarified but without changing the principle.

How should an entity measure a dividend payable? (paragraphs 11–13)

BC21

IFRSs do not provide guidance on how an entity should measure distributions to owners. However, the IFRIC noted that a number of IFRSs address how a liability should be measured. Although IFRSs do not specifically address how an entity should measure a dividend payable, the IFRIC decided that it could identify potentially relevant IFRSs and apply their principles to determine the appropriate measurement basis.

Which IFRSs are relevant to the measurement of a dividend payable?

BC22

The IFRIC considered all IFRSs that prescribe the accounting for a liability. Of those, the IFRIC concluded that IAS 37 Provisions, Contingent Assets and Contingent Liabilities and IAS 39 Financial Instruments: Recognition and Measurement[3] were the most likely to be relevant. The IFRIC concluded that other IFRSs were not applicable because most of them addressed only liabilities arising from exchange transactions and some of them were clearly not relevant (eg IAS 12 Income Taxes). As mentioned above, the Interpretation addresses only non-reciprocal distributions of assets by an entity to its owners.

IFRS 9 Financial Instruments replaced IAS 39. IFRS 9 applies to all items that were previously within the scope of IAS 39.

BC23

Given that all types of distributions have the purpose of distributing assets to owners, the IFRIC decided that all dividends payable should be measured the same way, regardless of the types of assets to be distributed. This also ensures that all dividends payable are measured consistently.

BC24

Some believed that IAS 39 was the appropriate IFRS to be used to measure dividends payable. They believed that, once an entity declared a distribution to its owners, it had a contractual obligation to distribute the assets to its owners. However, IAS 39 would not cover dividends payable if they were considered to be non-contractual obligations. In addition, IAS 39 covers some but not all obligations that require an entity to deliver non-cash assets to another entity. It does not cover a liability to distribute non-financial assets to owners. The IFRIC therefore concluded that it was not appropriate to conclude that all dividends payable should be within the scope of IAS 39.

BC25

The IFRIC then considered IAS 37, which is generally applied in practice to determine the accounting for liabilities other than those arising from executory contracts and those addressed by other IFRSs. IAS 37 requires an entity to measure a liability on the basis of the best estimate of the expenditure required to settle the present obligation at the end of the reporting period. Consequently, in D23 the IFRIC decided that it was appropriate to apply the principles in IAS 37 to all dividends payable (regardless of the types of assets to be distributed). The IFRIC decided that to apply IAS 37 to measure a liability for an obligation to distribute non-cash assets to owners, an entity should consider the fair value of the assets to be distributed. The fair value of the assets to be distributed is clearly relevant no matter which approach in IAS 37 is taken to determine the best estimate of the expenditure required to settle the liability.

BC26

However, in response to comments received on D23, the IFRIC reconsidered whether the Interpretation should specify that all dividends payable should be measured in accordance with IAS 37. The IFRIC noted that many respondents were concerned that D23 might imply that the measurement attribute in IAS 37 should always be interpreted to be fair value. This was not the intention of D23 as that question is part of the Board’s project to amend IAS 37. In addition, many respondents were not certain whether measuring the dividend payable ‘by reference to’ the fair value of the assets to be distributed required measurement at their fair value or at some other amount.

BC27

Therefore, the IFRIC decided to modify the proposal in D23 to require the dividend payable to be measured at the fair value of the assets to be distributed, without linking to any individual standard its conclusion that fair value is the most relevant measurement attribute. The IFRIC also noted that if the assets being distributed constituted a business, its fair value could be different from the simple sum of the fair value of the component assets and liabilities (ie it includes the value of goodwill or the identified intangible assets).

Should any exception be made to the principle of measuring a dividend payable at the fair value of the assets to be distributed?

BC28

Some are concerned that the fair value of the assets to be distributed might not be reliably measurable in all cases. They believe that exceptions should be made in the following circumstances:

(a) An entity distributes an ownership interest of another entity that is not traded in an active market and the fair value of the ownership interest cannot be measured reliably. The IFRIC noted that IAS 39[4] does not permit investments in equity instruments that do not have a quoted market price in an active market[5] and whose fair value cannot be measured reliably to be measured at fair value.

(b) An entity distributes an intangible asset that is not traded in an active market and therefore would not be permitted to be carried at a revalued amount in accordance with IAS 38 Intangible Assets.

IFRS 9 Financial Instruments requires all investments in equity instruments to be measured at fair value.

IFRS 13 Fair Value Measurement, issued in May 2011, defines fair value and contains the requirements for measuring fair value. IFRS 13 defines a Level 1 input as a quoted price in an active market for an identical asset or liability. Level 2 inputs include quoted prices for identical assets or liabilities in markets that are not active. As a result IFRS 9 refers to such equity instruments as ‘an equity instrument that does not have a quoted price in an active market for an identical instrument (ie a Level 1 input)’.

BC29

The IFRIC noted that in accordance with IAS 39 paragraphs AG80 and AG81,[6] the fair value of equity instruments that do not have a quoted price in an active market[7] is reliably measurable if:

(a) the variability in the range of reasonable fair value estimates is not significant for that instrument, or

(b) the probabilities of the various estimates within the range can be reasonably assessed and used in estimating fair value.

IFRS 9 Financial Instruments deleted paragraphs AG80 and AG81 of IAS 39. IFRS 13 Fair Value Measurement, issued in May 2011, defines fair value and contains requirements for measuring fair value. IFRS 13 defines a Level 1 input as a quoted price in an active market for an identical asset or liability. Level 2 inputs include quoted prices for identical assets or liabilities in markets that are not active. As a result IFRS 9 refers to such equity instruments as ‘an equity instrument that does not have a quoted price in an active market for an identical instrument (ie a Level 1 input)’.

IFRS 13 Fair Value Measurement, issued in May 2011, defines fair value and contains requirements for measuring fair value. IFRS 13 defines a Level 1 input as a quoted price in an active market for an identical asset or liability. Level 2 inputs include quoted prices for identical assets or liabilities in markets that are not active. As a result IFRS 9 refers to such equity instruments as ‘an equity instrument that does not have a quoted price in an active market for an identical instrument (ie a Level 1 input)’.

BC30

The IFRIC noted that, when the management of an entity recommends a distribution of a non-cash asset to its owners, one or both of the conditions for determining a reliable measure of the fair value of equity instruments that do not have a quoted price in an active market is likely to be satisfied. Management would be expected to know the fair value of the asset because management has to ensure that all owners of the entity are informed of the value of the distribution. For this reason, it would be difficult to argue that the fair value of the assets to be distributed cannot be determined reliably.

BC31

In addition, the IFRIC recognised that in some cases the fair value of an asset must be estimated. As mentioned in paragraph 86 of the Framework for the Preparation and Presentation of Financial Statements,[8] the use of reasonable estimates is an essential part of the preparation of financial statements and does not undermine their reliability.

now paragraph 4.41 of the Conceptual Framework. References to the Framework are to IASC’s Framework for the Preparation and Presentation of Financial Statements, adopted by the IASB in 2001. In September 2010 the IASB replaced the Framework with the Conceptual Framework for Financial Reporting.

BC32

The IFRIC noted that a reason why IAS 38 and IAS 39[9] require some assets to be measured using a historical cost basis is cost-benefit considerations. The cost of determining the fair value of an asset not traded in an active market at the end of each reporting period could outweigh the benefits. However, because an entity would be required to determine the fair value of the assets to be distributed only once at the time of distribution, the IFRIC concluded that the benefit (ie informing users of the financial statements of the value of the assets distributed) outweighs the cost of determining the fair value of the assets.

IFRS 9 Financial Instruments eliminated the requirement in IAS 39 for some assets to be measured using a historical cost basis.

BC33

Furthermore, the IFRIC noted that dividend income, regardless of whether it is in the form of cash or non-cash assets, is within the scope of IAS 18 Revenue[10] and is required to be measured at the fair value of the consideration received. Although the Interpretation does not address the accounting by the recipient of the non-cash distribution, the IFRIC concluded that the Interpretation did not impose a more onerous requirement on the entity that makes the distribution than IFRSs have already imposed on the recipient of the distribution.

IFRS 15 Revenue from Contracts with Customers, issued in May 2014, replaced IAS 18 Revenue. IFRS 15 does not address dividends. Dividends should be accounted for in accordance with IFRS 9, or IAS 39 if applicable.

BC34

For the reasons described in paragraphs BC28–BC33, the IFRIC concluded that no exceptions should be made to the requirement that the fair value of the asset to be distributed should be used in measuring a dividend payable.

Whether an entity should remeasure the dividend payable (paragraph 13)

BC35

The IFRIC noted that paragraph 59 of IAS 37 requires an entity to review the carrying amount of a liability at the end of each reporting period and to adjust the carrying amount to reflect the current best estimate of the liability. Other IFRSs such as IAS 19 Employee Benefits similarly require liabilities that are based on estimates to be adjusted each reporting period. The IFRIC therefore decided that the entity should review and adjust the carrying amount of the dividend payable to reflect its current best estimate of the fair value of the assets to be distributed at the end of each reporting period and at the date of settlement.

BC36

The IFRIC concluded that, because any adjustments to the best estimate of the dividend payable reflect changes in the estimated value of the distribution, they should be recognised as adjustments to the amount of the distribution. In accordance with IAS 1 Presentation of Financial Statements (as revised in 2007), distributions to owners are required to be recognised directly in the statement of changes in equity. Similarly, adjustments to the amount of the distribution are also recognised directly in the statement of changes in equity.

BC37

Some commentators argued that the changes in the estimated value of the distribution should be recognised in profit or loss because changes in liabilities meet the definition of income or expenses in the Framework. However, the IFRIC decided that the gain or loss on the assets to be distributed should be recognised in profit or loss when the dividend payable is settled. This is consistent with other IFRSs (IAS 16, IAS 38, IAS 39[11] ) that require an entity to recognise in profit or loss any gain or loss arising from derecognition of an asset. The IFRIC concluded that the changes in the dividend payable before settlement related to changes in the estimate of the distribution and should be accounted for in equity (ie adjustments to the amount of the distribution) until settlement of the dividend payable.

IFRS 9 Financial Instruments replaced IAS 39. IFRS 9 applies to all items that were previously within the scope of IAS 39.

When the entity settles the dividend payable, how should it account for any difference between the carrying amount of the assets distributed and the carrying amount of the dividend payable? (paragraph 14)

BC38

When an entity distributes the assets to its owners, it derecognises both the assets distributed and the dividend payable.

BC39

The IFRIC noted that, at the time of settlement, the carrying amount of the assets distributed would not normally be greater than the carrying amount of the dividend payable because of the recognition of impairment losses required by other applicable standards. For example, paragraph 59 of IAS 36 Impairment of Assets requires an entity to recognise an impairment loss in profit or loss when the recoverable amount of an asset is less than its carrying amount. The recoverable amount of an asset is the higher of its fair value less costs to sell and its value in use in accordance with paragraph 6 of IAS 36. When an entity has an obligation to distribute the asset to its owners in the near future, it would not seem appropriate to measure an impairment loss using the asset’s value in use. Furthermore, IFRS 5 requires an entity to measure an asset held for sale at the lower of its carrying amount and its fair value less costs to sell. Consequently, the IFRIC concluded that when an entity derecognises the dividend payable and the asset distributed, any difference will always be a credit balance (referred to below as the credit balance).

BC40

In determining how the credit balance should be accounted for, the IFRIC first considered whether it should be recognised as an owner change in equity.

BC41

The IFRIC acknowledged that an asset distribution was a transaction between an entity and its owners. The IFRIC also observed that distributions to owners are recognised as owner changes in equity in accordance with IAS 1 (as revised in 2007). However, the IFRIC noted that the credit balance did not arise from the distribution transaction. Rather, it represented the cumulative unrecognised gain associated with the asset. It reflects the performance of the entity during the period the asset was held until it was distributed.

BC42

Some might argue that, since an asset distribution does not result in the owners of an entity losing the future economic benefits of the asset, the credit balance should be recognised directly in equity. This view would be based upon the proprietary perspective in which the reporting entity does not have substance of its own separate from that of its owners. However, the IFRIC noted that the Framework requires an entity to consider the effect of a transaction from the perspective of the entity for which the financial statements are prepared. Under the entity perspective, the reporting entity has substance of its own, separate from that of its owners. In addition, when there is more than one class of equity instruments, the argument that all owners of an entity have effectively the same interest in the asset would not be valid.

BC43

For the reasons described in paragraphs BC41 and BC42, the IFRIC concluded that the credit balance should not be recognised as an owner change in equity.

BC44

The IFRIC noted that, as explained in the Basis for Conclusions on IAS 1, the Board explicitly prohibited any income or expenses (ie non-owner changes in equity) from being recognised directly in the statement of changes in equity. Any such income or expenses must be recognised as items of comprehensive income first.

BC45

The statement of comprehensive income in accordance with IAS 1 includes two components: items of profit or loss, and items of other comprehensive income. The IFRIC therefore discussed whether the credit balance should be recognised in profit or loss or in other comprehensive income.

BC46

IAS 1 does not provide criteria for when an item should be recognised in profit or loss. However, paragraph 88 of IAS 1 states: ‘An entity shall recognise all items of income and expense in a period in profit or loss unless an IFRS requires or permits otherwise.’

BC47

The IFRIC considered the circumstances in which IFRSs require items of income and expense to be recognised as items of other comprehensive income, mainly as follows:

(a) some actuarial gains or losses arising from remeasuring defined benefit liabilities provided that specific criteria set out in IAS 19 are met.

(b) a revaluation surplus arising from revaluation of an item of property, plant and equipment in accordance with IAS 16 or revaluation of an intangible asset in accordance with IAS 38.

(c) an exchange difference arising from the translation of the results and financial positions of an entity from its functional currency into a presentation currency in accordance with IAS 21 The Effects of Changes in Foreign Exchange Rates.

(d) an exchange difference arising from the translation of the results and financial position of a foreign operation into a presentation currency of a reporting entity for consolidation purposes in accordance with IAS 21.

(e) a change in the fair value of an available-for-sale[12] investment in accordance with IAS 39.

(f) a change in the fair value of a hedging instrument qualifying for cash flow hedge accounting in accordance with IAS 39.[13]

BC48

The IFRIC concluded that the requirement in IAS 1 prevents any of these items from being applied by analogy to the credit balance. In addition, the IFRIC noted that, with the exception of the items described in paragraph BC47(a)–(c), the applicable IFRSs require the items of income and expenses listed in paragraph BC47 to be reclassified to profit or loss when the related assets or liabilities are derecognised. Those items of income and expenses are recognised as items of other comprehensive income when incurred, deferred in equity until the related assets are disposed of (or the related liabilities are settled), and reclassified to profit or loss at that time.

BC49

The IFRIC noted that, when the dividend payable is settled, the asset distributed is also derecognised. Therefore, given the existing requirements in IFRSs, even if the credit balance were recognised as an item of other comprehensive income, it would have to be reclassified to profit or loss immediately. As a result, the credit balance would appear three times in the statement of comprehensive income—once recognised as an item of other comprehensive income, once reclassified out of other comprehensive income to profit or loss and once recognised as an item of profit or loss as a result of the reclassification. The IFRIC concluded that such a presentation does not faithfully reflect what has occurred. In addition, users of financial statements were likely to be confused by such a presentation.

BC50

Moreover, when an entity distributes its assets to its owners, it loses the future economic benefit associated with the assets distributed and derecognises those assets. Such a consequence is, in general, similar to that of a disposal of an asset. IFRSs (eg IAS 16, IAS 38, IAS 39[14] and IFRS 5) require an entity to recognise in profit or loss any gain or loss arising from the derecognition of an asset. IFRSs also require such a gain or loss to be recognised when the asset is derecognised. As mentioned in paragraph BC42, the Framework requires an entity to consider the effect of a transaction from the perspective of an entity for which the financial statements are prepared. For these reasons, the IFRIC concluded that the credit balance and gains or losses on derecognition of an asset should be accounted for in the same way.

IFRS 9 Financial Instruments replaced IAS 39. IFRS 9 applies to all items that were previously within the scope of IAS 39.

BC51

Furthermore, paragraph 92 of the Framework[15] states: ‘Income is recognised in the income statement when an increase in future economic benefits related to an increase in an asset or a decrease of a liability has arisen that can be measured reliably’ (emphasis added). At the time of the settlement of a dividend payable, there is clearly a decrease in a liability. Therefore, the credit balance should be recognised in profit or loss in accordance with paragraph 92 of the Framework. Some might argue that the entity does not receive any additional economic benefits when it distributes the assets to its owners. As mentioned in paragraph BC41, the credit balance does not represent any additional economic benefits to the entity. Instead, it represents the unrecognised economic benefits that the entity obtained while it held the assets.

now paragraph 4.47 of the Conceptual Framework

BC52

The IFRIC also noted that paragraph 55 of the Framework[16] states: ‘The future economic benefits embodied in an asset may flow to the entity in a number of ways. For example, an asset may be: (a) used singly or in combination with other assets in the production of goods or services to be sold by the entity; (b) exchanged for other assets; (c) used to settle a liability; or (d) distributed to the owners of the entity [emphasis added].’

now paragraph 4.10 of the Conceptual Framework

BC53

In the light of these requirements, in D23 the IFRIC concluded that the credit balance should be recognised in profit or loss. This treatment would give rise to the same accounting results regardless of whether an entity distributes non-cash assets to its owners, or sells the non-cash assets first and distributes the cash received to its owners. Most commentators on D23 supported the IFRIC’s conclusion and its basis.

BC54

Some IFRIC members believed that it would be more appropriate to treat the distribution as a single transaction with owners and therefore recognise the credit balance directly in equity. This alternative view was included in D23 and comments were specifically invited. However, this view was not supported by commentators. To be recognised directly in equity, the credit balance must be considered an owner change in equity in accordance with IAS 1. The IFRIC decided that the credit balance does not arise from the distribution transaction. Rather, it represents the increase in value of the assets. The increase in the value of the asset does not meet the definition of an owner change in equity in accordance with IAS 1. Rather, it meets the definition of income and should be recognised in profit and loss.

BC55

The IFRIC recognised respondents’ concerns about the potential ‘accounting mismatch’ in equity resulting from measuring the assets to be distributed at carrying amount and measuring the dividend payable at fair value. Consequently, the IFRIC considered whether it should recommend that the Board amend IFRS 5 to require the assets to be distributed to be measured at fair value.

BC56

In general, IFRSs permit remeasurement of assets only as the result of a transaction or an impairment. The exceptions are situations in which the IFRSs prescribe current measures on an ongoing basis as in IASs 39 and 41 Agriculture, or permit them as accounting policy choices as in IASs 16, 38 and 40 Investment Property. As a result of its redeliberations, the IFRIC concluded that there was no support in IFRSs for requiring a remeasurement of the assets because of a decision to distribute them. The IFRIC noted that the mismatch concerned arises only with respect to assets that are not carried at fair value already. The IFRIC also noted that the accounting mismatch is the inevitable consequence of IFRSs using different measurement attributes at different times with different triggers for the remeasurement of different assets and liabilities.

BC57

If a business is to be distributed, the fair value means the fair value of the business to be distributed. Therefore, it includes goodwill and intangible assets. However, internally generated goodwill is not permitted to be recognised as an asset (paragraph 48 of IAS 38). Internally generated brands, mastheads, publishing titles, customer lists and items similar in substance are not permitted to be recognised as intangible assets (paragraph 63 of IAS 38). In accordance with IAS 38, the carrying amounts of internally generated intangible assets are generally restricted to the sum of expenditure incurred by an entity. Consequently, a requirement to remeasure an asset that is a business would contradict the relevant requirements in IAS 38.

BC58

Furthermore, in addition to the lack of consistency with other IFRSs, changing IFRS 5 this way (ie to require an asset held for distribution to owners to be remeasured at fair value) would create internal inconsistency within IFRS 5. There would be no reasonable rationale to explain why IFRS 5 could require assets that are to be sold to be carried at the lower of fair value less costs to sell and carrying value but assets to be distributed to owners to be carried at fair value. The IFRIC also noted that this ‘mismatch’ would arise only in the normally short period between when the dividend payable is recognised and when it is settled. The length of this period would often be within the control of management. Therefore, the IFRIC decided not to recommend that the Board amend IFRS 5 to require assets that are to be distributed to be measured at fair value.

Amendment to IFRS 5

BC59

IFRS 5 requires an entity to classify a non-current asset (or disposal group) as held for sale if its carrying amount will be recovered principally through a sale transaction rather than through continuing use. IFRS 5 also sets out presentation and disclosure requirements for a discontinued operation.

BC60

When an entity has an obligation to distribute assets to its owners, the carrying amount of the assets will no longer be recovered principally through continuing use. The IFRIC decided that the information required by IFRS 5 is important to users of financial statements regardless of the form of a transaction. Therefore, the IFRIC concluded that the requirements in IFRS 5 applicable to non-current assets (or disposal groups) classified as held for sale and to discontinued operations should also be applied to assets (or disposal groups) held for distribution to owners.

BC61

However, the IFRIC concluded that requiring an entity to apply IFRS 5 to non-current assets (disposal groups) held for distribution to owners would require amendments to IFRS 5. This is because, in the IFRIC’s view, IFRS 5 at present applies only to non-current assets (disposal groups) held for sale.

BC62

The Board discussed the IFRIC’s proposal at its meeting in December 2007. The Board agreed with the IFRIC’s conclusion that IFRS 5 should be amended to apply to non-current assets held for distribution to owners as well as to assets held for sale. However, the Board noted that IFRS 5 requires an entity to classify a non-current asset as held for sale when the sale is highly probable and the entity is committed to a plan to sell (emphasis added). Consequently, the Board directed the IFRIC to invite comments on the following questions:

(a) Should an entity apply IFRS 5 when it is committed to make a distribution or when it has an obligation to distribute the assets concerned?

(b) Is there a difference between those dates?

(c) If respondents believe that there is a difference between the dates and that an entity should apply IFRS 5 at the commitment date, what is the difference? What indicators should be included in IFRS 5 to help an entity to determine that date?

BC63

On the basis of the comments received, the IFRIC noted that, in many jurisdictions, shareholders’ approval is required to make a distribution. Therefore, in such jurisdictions there could be a difference between the commitment date (ie the date when management is committed to the dividend) and the obligation date (ie the date when the dividend is approved by the shareholders). On the other hand, some commentators think that, when a distribution requires shareholders’ approval, the entity cannot be committed until that approval is obtained: in that case, there would be no difference between two dates.

BC64

The IFRIC concluded that IFRS 5 should be applied at the commitment date at which time the assets must be available for immediate distribution in their present condition and the distribution must be highly probable. For the distribution to be highly probable, it should meet essentially the same conditions required for assets held for sale. Further, the IFRIC concluded that the probability of shareholders’ approval (if required in the jurisdiction) should be considered as part of the assessment of whether the distribution is highly probable. The IFRIC noted that shareholder approval is also required for the sale of assets in some jurisdictions and concluded that similar consideration of the probability of such approval should be required for assets held for sale.

BC65

The Board agreed with the IFRIC’s conclusions and amended IFRS 5 as part of its approval of the Interpretation.

Summary of main changes from the draft Interpretation

BC66

The main changes from the IFRIC’s proposals in D23 are as follows:

(a) Paragraphs 3–8 were modified to clarify the scope of the Interpretation.

(b) Paragraph 10 clarifies when to recognise a dividend payable.

(c) Paragraphs 11–13 were modified to require the dividend payable to be measured at the fair value of the assets to be distributed without linking the IFRIC’s conclusion that fair value is the most relevant measurement attribute to any individual standard.

(d) Illustrative examples were expanded to set out clearly the scope of the Interpretation.

(e) The Interpretation includes the amendments to IFRS 5 and IAS 10.

(f) The Basis for Conclusions was changed to set out more clearly the reasons for the IFRIC’s conclusions.

IFRS 9 Financial Instruments eliminated the category of available-for-sale financial assets.

IFRS 9 Financial Instruments replaced the hedge accounting requirements in IAS 39.

Deleted IFRIC 17 text

Deleted IFRIC 17 text is not part of AASB Interpretation 17.

18

An entity shall apply this Interpretation prospectively for annual periods beginning on or after 1 July 2009. Retrospective application is not permitted. Earlier application is permitted. If an entity applies this Interpretation for a period beginning before 1 July 2009, it shall disclose that fact and also apply IFRS 3 (as revised in 2008), IAS 27 (as amended in May 2008) and IFRS 5 (as amended by this Interpretation).

19

IFRS 10, issued in May 2011, amended paragraph 7. An entity shall apply that amendment when it applies IFRS 10.

20

IFRS 13, issued in May 2011, amended paragraph 17. An entity shall apply that amendment when it applies IFRS 13.