The objective of this Standard is to prescribe the accounting and disclosure requirements for investments in subsidiaries, joint ventures and associates when an entity prepares separate financial statements.

Preamble

Pronouncement

This compiled Standard applies to annual periods beginning on or after 1 January 2022. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 January 2022. It incorporates relevant amendments made up to and including 20 December 2021.

Prepared on 7 April 2022 by the staff of the Australian Accounting Standards Board.

Compilation no. 2

Compilation date: 31 December 2021

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2022

This compiled AASB Standard contains IFRS Foundation copyright material. Digital devices and links are copyright of the Commonwealth. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

All existing rights in this material are reserved outside Australia. Reproduction outside Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce IFRS Foundation copyright material for commercial purposes outside Australia should be addressed to the IFRS Foundation at www.ifrs.org.

Rubric

Australian Accounting Standard AASB 127 Separate Financial Statements (as amended) is set out in paragraphs 1 – Aus20.2 and Appendix A. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 127 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with IAS 27

AASB 127 Separate Financial Statements as amended incorporates IAS 27 Separate Financial Statements as issued and amended by the International Accounting Standards Board (IASB). Australian specific paragraphs (which are not included in IAS 27) are identified with the prefix “Aus”. Paragraphs that apply only to not-for-profit entities begin by identifying their limited applicability.

Tier 1

For-profit entities complying with AASB 127 also comply with IAS 27.

Not-for-profit entities’ compliance with IAS 27 will depend on whether any “Aus” paragraphs that specifically apply to not-for-profit entities provide additional guidance or contain applicable requirements that are inconsistent with IAS 27.

Tier 2

Entities preparing general purpose financial statements under Australian Accounting Standards – Simplified Disclosures (Tier 2) will not be in compliance with IFRS Standards.

AASB 1053 Application of Tiers of Australian Accounting Standards explains the two tiers of reporting requirements.

Accounting Standard AASB 127

The Australian Accounting Standards Board made Accounting Standard AASB 127 Separate Financial Statements under section 334 of the Corporations Act 2001 on 7 August 2015.

This compiled version of AASB 127 applies to annual periods beginning on or after 1 January 2022. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 20 December 2021 (see Compilation Details).

Scope

2

This Standard shall be applied in accounting for investments in subsidiaries, joint ventures and associates when an entity elects, or is required by local regulations, to present separate financial statements.

3

This Standard does not mandate which entities produce separate financial statements. It applies when an entity prepares separate financial statements that comply with Australian Accounting Standards.

Definitions

4

The following terms are used in this Standard with the meanings specified:

4[1]

Consolidated financial statements are the financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity.

4[2]

Separate financial statements are those presented by an entity in which the entity could elect, subject to the requirements in this Standard, to account for its investments in subsidiaries, joint ventures and associates either at cost, in accordance with AASB 9 Financial Instruments, or using the equity method as described in AASB 128 Investments in Associates and Joint Ventures.

Definitions [further paragraphs]

5

The following terms are defined in Appendix A of AASB 10 Consolidated Financial Statements, Appendix A of AASB 11 Joint Arrangements and paragraph 3 of AASB 128:

• associate

• control of an investee

• equity method

• group

• investment entity

• joint control

• joint venture

• joint venturer

• parent

• significant influence

• subsidiary

6

Separate financial statements are those presented in addition to consolidated financial statements or in addition to the financial statements of an investor that does not have investments in subsidiaries but has investments in associates or joint ventures in which the investments in associates or joint ventures are required by AASB 128 to be accounted for using the equity method, other than in the circumstances set out in paragraphs 8–8A.

7

The financial statements of an entity that does not have a subsidiary, associate or joint venturer’s interest in a joint venture are not separate financial statements.

8

An entity that is exempted in accordance with paragraphs 4(a), Aus4.1 and Aus4.2 of AASB 10 from consolidation or paragraphs 17, Aus17.1 and Aus17.2 of AASB 128 from applying the equity method may present separate financial statements as its only financial statements.

8A

An investment entity that is required, throughout the current period and all comparative periods presented, to apply the exception to consolidation for all of its subsidiaries in accordance with paragraph 31 of AASB 10 presents separate financial statements as its only financial statements.

Preparation of separate financial statements

9

Separate financial statements shall be prepared in accordance with all applicable Standards, except as provided in paragraph 10.

10

When an entity prepares separate financial statements, it shall account for investments in subsidiaries, joint ventures and associates either:

(a) at cost;

(b) in accordance with AASB 9; or

(c) using the equity method as described in AASB 128.

The entity shall apply the same accounting for each category of investments. Investments accounted for at cost or using the equity method shall be accounted for in accordance with AASB 5 Non-current Assets Held for Sale and Discontinued Operations when they are classified as held for sale or for distribution (or included in a disposal group that is classified as held for sale or for distribution). The measurement of investments accounted for in accordance with AASB 9 is not changed in such circumstances.

11

If an entity elects, in accordance with paragraph 18 of AASB 128, to measure its investments in associates or joint ventures at fair value through profit or loss in accordance with AASB 9, it shall also account for those investments in the same way in its separate financial statements.

11A

If a parent is required, in accordance with paragraph 31 of AASB 10, to measure its investment in a subsidiary at fair value through profit or loss in accordance with AASB 9, it shall also account for its investment in a subsidiary in the same way in its separate financial statements.

11B

When a parent ceases to be an investment entity, or becomes an investment entity, it shall account for the change from the date when the change in status occurred, as follows:

(a) when an entity ceases to be an investment entity, the entity shall account for an investment in a subsidiary in accordance with paragraph 10. The date of the change of status shall be the deemed acquisition date. The fair value of the subsidiary at the deemed acquisition date shall represent the transferred deemed consideration when accounting for the investment in accordance with paragraph 10.

(i) [deleted]

(ii) [deleted]

(b) when an entity becomes an investment entity, it shall account for an investment in a subsidiary at fair value through profit or loss in accordance with AASB 9. The difference between the previous carrying amount of the subsidiary and its fair value at the date of the change of status of the investor shall be recognised as a gain or loss in profit or loss. The cumulative amount of any gain or loss previously recognised in other comprehensive income in respect of those subsidiaries shall be treated as if the investment entity had disposed of those subsidiaries at the date of change in status.

12

Dividends from a subsidiary, a joint venture or an associate are recognised in the separate financial statements of an entity when the entity’s right to receive the dividend is established. The dividend is recognised in profit or loss unless the entity elects to use the equity method, in which case the dividend is recognised as a reduction from the carrying amount of the investment.

13

When a parent reorganises the structure of its group by establishing a new entity as its parent in a manner that satisfies the following criteria:

(a) the new parent obtains control of the original parent by issuing equity instruments in exchange for existing equity instruments of the original parent;

(b) the assets and liabilities of the new group and the original group are the same immediately before and after the reorganisation; and

(c) the owners of the original parent before the reorganisation have the same absolute and relative interests in the net assets of the original group and the new group immediately before and after the reorganisation,

and the new parent accounts for its investment in the original parent in accordance with paragraph 10(a) in its separate financial statements, the new parent shall measure cost at the carrying amount of its share of the equity items shown in the separate financial statements of the original parent at the date of the reorganisation.

14

Similarly, an entity that is not a parent might establish a new entity as its parent in a manner that satisfies the criteria in paragraph 13. The requirements in paragraph 13 apply equally to such reorganisations. In such cases, references to ‘original parent’ and ‘original group’ are to the ‘original entity’.

Disclosure

15

An entity shall apply all applicable Standards when providing disclosures in its separate financial statements, including the requirements in paragraphs 16–17.

16

When a parent, in accordance with paragraphs 4(a), Aus4.1 and Aus4.2 of AASB 10, elects not to prepare consolidated financial statements and instead prepares separate financial statements, it shall disclose in those separate financial statements:

(a) the fact that the financial statements are separate financial statements; that the exemption from consolidation has been used; the name and principal place of business (and country of incorporation, if different) of the entity whose consolidated financial statements that comply with International Financial Reporting Standards have been produced for public use; and the address where those consolidated financial statements are obtainable.

(b) a list of significant investments in subsidiaries, joint ventures and associates, including:

(i) the name of those investees.

(ii) the principal place of business (and country of incorporation, if different) of those investees.

(iii) its proportion of the ownership interest (and its proportion of the voting rights, if different) held in those investees.

(c) a description of the method used to account for the investments listed under (b).

Aus16.1

When a not-for-profit parent, in accordance with paragraphs 4(a), Aus4.1 and Aus4.2 of AASB 10, elects not to prepare consolidated financial statements and instead prepares separate financial statements, it shall disclose in those separate financial statements the disclosures specified in paragraph 16, with the exception that the reference in paragraph 16(a) to ‘International Financial Reporting Standards’ is replaced by a reference to ‘Australian Accounting Standards’.

16A

When an investment entity that is a parent (other than a parent covered by paragraphs 16–Aus16.1) prepares, in accordance with paragraph 8A, separate financial statements as its only financial statements, it shall disclose that fact. The investment entity shall also present the disclosures relating to investment entities required by AASB 12 Disclosure of Interests in Other Entities.

17

When a parent (other than a parent covered by paragraphs 16–Aus16.1 or paragraph 16A) or an investor with joint control of, or significant influence over, an investee prepares separate financial statements, the parent or investor shall identify the financial statements prepared in accordance with AASB 10, AASB 11 or AASB 128 to which they relate. The parent or investor shall also disclose in its separate financial statements:

(a) the fact that the statements are separate financial statements and the reasons why those statements are prepared if not required by law.

(b) a list of significant investments in subsidiaries, joint ventures and associates, including:

(i) the name of those investees.

(ii) the principal place of business (and country of incorporation, if different) of those investees.

(iii) its proportion of the ownership interest (and its proportion of the voting rights, if different) held in those investees.

(c) a description of the method used to account for the investments listed under (b).

Effective date and transition

18

An entity shall apply this Standard for annual periods beginning on or after 1 January 2016. Earlier application is permitted for periods beginning on or after 1 January 2014 but before 1 January 2016. If an entity applies this Standard earlier, it shall disclose that fact and apply AASB 10, AASB 11, AASB 12 and AASB 128 at the same time.

18A

AASB 2013-5 Amendments to Australian Accounting Standards – Investment Entities, issued in August 2013, amended the previous version of this Standard as follows: amended paragraphs 5, 6, 17 and 18, and added paragraphs 8A, 11A–11B, 16A and 18B–18I. An entity shall apply those amendments for annual periods beginning on or after 1 January 2014. Early adoption is permitted. If an entity applies those amendments earlier, it shall disclose that fact and apply all amendments included in Investment Entities at the same time.

18B

If, at the date of initial application of AASB 2013-5 (which, for the purposes of this Standard, is the beginning of the annual reporting period for which those amendments are applied for the first time), a parent concludes that it is an investment entity, it shall apply paragraphs 18C–18I to its investment in a subsidiary.

18C

At the date of initial application, an investment entity that previously measured its investment in a subsidiary at cost shall instead measure that investment at fair value through profit or loss as if the requirements of this Standard had always been effective. The investment entity shall adjust retrospectively the annual period immediately preceding the date of initial application and shall adjust retained earnings at the beginning of the immediately preceding period for any difference between:

(a) the previous carrying amount of the investment; and

(b) the fair value of the investor’s investment in the subsidiary.

18D

At the date of initial application, an investment entity that previously measured its investment in a subsidiary at fair value through other comprehensive income shall continue to measure that investment at fair value. The cumulative amount of any fair value adjustment previously recognised in other comprehensive income shall be transferred to retained earnings at the beginning of the annual period immediately preceding the date of initial application.

18E

At the date of initial application, an investment entity shall not make adjustments to the previous accounting for an interest in a subsidiary that it had previously elected to measure at fair value through profit or loss in accordance with AASB 9, as permitted in paragraph 10.

18F

Before the date that AASB 13 Fair Value Measurement is adopted, an investment entity shall use the fair value amounts previously reported to investors or to management, if those amounts represent the amount for which the investment could have been exchanged between knowledgeable, willing parties in an arm’s length transaction at the date of the valuation.

18G

If measuring the investment in the subsidiary in accordance with paragraphs 18C–18F is impracticable (as defined in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors), an investment entity shall apply the requirements of this Standard at the beginning of the earliest period for which application of paragraphs 18C–18F is practicable, which may be the current period. The investor shall adjust retrospectively the annual period immediately preceding the date of initial application, unless the beginning of the earliest period for which application of this paragraph is practicable is the current period. When the date that it is practicable for the investment entity to measure the fair value of the subsidiary is earlier than the beginning of the immediately preceding period, the investor shall adjust equity at the beginning of the immediately preceding period for any difference between:

(a) the previous carrying amount of the investment; and

(b) the fair value of the investor’s investment in the subsidiary.

If the earliest period for which application of this paragraph is practicable is the current period, the adjustment to equity shall be recognised at the beginning of the current period.

18H

If an investment entity has disposed of, or lost control of, an investment in a subsidiary before the date of initial application of AASB 2013-5, the investment entity is not required to make adjustments to the previous accounting for that investment.

18I

Notwithstanding the references to the annual period immediately preceding the date of initial application (the ‘immediately preceding period’) in paragraphs 18C–18G, an entity may also present adjusted comparative information for any earlier periods presented, but is not required to do so. If an entity does present adjusted comparative information for any earlier periods, all references to the ‘immediately preceding period’ in paragraphs 18C–18G shall be read as the ‘earliest adjusted comparative period presented’. If an entity presents unadjusted comparative information for any earlier periods, it shall clearly identify the information that has not been adjusted, state that it has been prepared on a different basis, and explain that basis.

18J

AASB 2014-9 Amendments to Australian Accounting Standards – Equity Method in Separate Financial Statements, issued in December 2014, amended the previous version of this Standard as follows: amended paragraphs 4–7, 10, 11B and 12. An entity shall apply those amendments for annual periods beginning on or after 1 January 2016 retrospectively in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. Earlier application is permitted. If an entity applies those amendments for an earlier period, it shall disclose that fact.

Withdrawal of AASB pronouncements

Aus20.2

This Standard repeals AASB 127 Separate Financial Statements issued in August 2011. Despite the repeal, after the time this Standard starts to apply under section 334 of the Corporations Act (either generally or in relation to an individual entity), the repealed Standard continues to apply in relation to any period ending before that time as if the repeal had not occurred.

[Note: When this Standard applies under section 334 of the Corporations Act (either generally or in relation to an individual entity), it supersedes the application of the repealed Standard.]

Appendix A -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusA1

Paragraphs 15–17 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

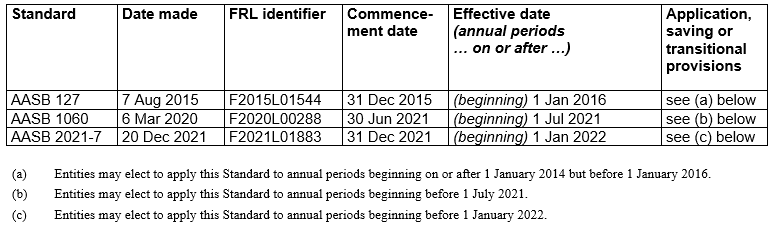

Compilation details

Accounting Standard AASB 127 Separate Financial Statements (as amended)

Compilation details are not part of AASB 127.

This compiled Standard applies to annual periods beginning on or after 1 January 2022. It takes into account amendments up to and including 20 December 2021 and was prepared on 7 April 2022 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 127 (August 2015) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments