The objective of this Standard is to specify requirements for government departments relating to administered items.

Preamble

Pronouncement

This compiled Standard applies to annual periods beginning on or after 1 July 2021. Earlier application is permitted for annual periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board.

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1050 Administered Items (as amended) is set out in paragraphs 1 – 25 and Appendix B. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 1050 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with international pronouncements

This Standard contains relevant requirements for the disclosure of administered items by government departments that have been relocated from AAS 29 Financial Reporting by Government Departments in substantially unamended form (with some exceptions, as noted in Appendix A). Accordingly, the development of this Standard did not involve consideration of International Public Sector Accounting Standards (IPSAS) issued by the International Public Sector Accounting Standards Board (IPSASB) or International Financial Reporting Standards (IFRS Standards) issued by the International Accounting Standards Board (IASB).

The longer-term review of accounting for administered items will involve consideration of international pronouncements.

AASB 1050 and IPSAS

At the date of issue, this Standard has no corresponding IPSAS dealing specifically with administered items. Consistent with this Standard, paragraph 12 of IPSAS 9 Revenue from Exchange Transactions notes that amounts collected on behalf of third parties in a custodial or agency relationship are excluded from revenue.

The IPSASB is undertaking a project to develop a public sector conceptual framework. Administered items is a topic that will be addressed as part of that project.

AASB 1050 and IFRS Standards

At the date of issue, this Standard has no corresponding IFRS Standard dealing specifically with administered items. Consistent with this Standard, paragraph 8 of IAS 18 Revenue notes that amounts collected on behalf of third parties in an agency relationship are not revenue. In addition, where a bank is engaged in significant trust activities (which excludes safe custody functions), paragraph 55 of IAS 30 Disclosures in the Financial Statements of Banks and Similar Financial Institutions (superseded by IFRS 7 Financial Instruments: Disclosures from 1 January 2007) requires the disclosure of that fact and an indication of the extent of those activities.

Accounting Standard AASB 1050

The Australian Accounting Standards Board made Accounting Standard AASB 1050 Administered Items on 13 December 2007.

This compiled version of AASB 1050 applies to annual reporting periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Objective

1

The objective of this Standard is to specify requirements for government departments relating to administered items. Disclosures made in accordance with this Standard provide users with information relevant to assessing the performance of a government department, including accountability for resources entrusted to it.

Application

2

This Standard applies to general purpose financial statements of government departments.

3

This Standard applies to annual reporting periods beginning on or after 1 July 2008.

[Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

4

This Standard may be applied to annual reporting periods beginning on or after 1 January 2005 but before 1 July 2008, provided there is early adoption for the same annual reporting period of the following pronouncements being issued at about the same time, as applicable:

(a) AASB 1004 Contributions;

(b) AASB 1049 Whole of Government and General Government Sector Financial Reporting;

(c) AASB 1051 Land Under Roads;

(d) AASB 1052 Disaggregated Disclosures;

(e) AASB 2007-9 Amendments to Australian Accounting Standards arising from the Review of AASs 27, 29 and 31; and

(f) AASB Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities.

5

[Deleted by the AASB]

6

When applicable, this Standard, together with the Standards referred to in paragraph 4, supersede AAS 29 Financial Reporting by Government Departments as issued in June 1998, as amended.

Disclosure of Administered Income, Expenses, Assets and Liabilities

7

A government department shall disclose the following in its complete set of financial statements in relation to activities administered by the government department:

(a) administered income, showing separately:

(i) each major class of income; and

(ii) in respect of each major class of income, the amounts reliably attributable to each of the government department’s activities and the amounts not attributable to activities;

(b) administered expenses, showing separately:

(i) each major class of expense; and

(ii) in respect of each major class of expense, the amounts reliably attributable to each of the government department’s activities and the amounts not attributable to activities;

(c) administered assets, showing separately each major class of asset; and

(d) administered liabilities, showing separately each major class of liability.

8

AASB 1052 specifies requirements for the disclosure of income and expenses attributable to a government department’s activities. The principles in that Standard are applied in disclosing administered income and expenses reliably attributable to activities in accordance with paragraphs 7(a)(ii) and 7(b)(ii) of this Standard.

9

A government department’s operating statement only recognises income and expenses of the government department. Similarly, a government department’s statement of financial position only recognises assets that the government department controls and liabilities that involve a future sacrifice of the government department’s assets.

10

Items recognised in the statement of financial position include the assets and liabilities of the trusts that the government department controls and from whose activities the government department obtains benefits.

11

The responsibilities of a government department may encompass the levying or collection of taxes, fines and fees, the provision of goods and services at a charge to recipients, and the transfer of funds to eligible beneficiaries. These activities may give rise to income and expenses that are not attributable to the government department. This occurs, for example, where the government department is unable to use for its own purposes the proceeds of user charges, taxes, fines and fees it collects without further authorisation, or where the transfer of funds to eligible beneficiaries does not involve a reduction in the assets recognised in the government department’s statement of financial position. In addition, the government department may manage government assets in the capacity of an agent and may incur liabilities that, for example, while involving a future disbursement from the Consolidated Revenue Fund or other Fund will not involve a sacrifice of the assets that the government department controls as at the end of the reporting period. This administered income and these administered expenses, assets and liabilities are not recognised in the government department’s operating statement or statement of financial position.

12

A government department’s ability to control all, or a portion of, the proceeds of the user charges, fines and fees it levies may be subject to complex arrangements. Consistent with those arrangements, where a government department does not control any of the proceeds of the user charges, fines and fees that it levies, it does not recognise any of the proceeds of those user charges, fines and fees as income. Similarly, where, as a result of automatic appropriations or other authority, a government department controls some but not all of the proceeds of user charges, fines and fees, the department recognises as income only those amounts that it controls.

13

If taxes, fines, fees and other amounts that are not controlled by a government department were to be recognised as assets or income by the collecting government department, users could incorrectly assume that these amounts were available for the government department’s use.

14

The tax revenues, user charges, fines and fees administered by a government department and the amount of funds transferred to eligible beneficiaries are an important indicator of the government department’s performance in achieving its objectives. Therefore, paragraph 7 requires disclosure of income and expenses administered by a government department that are not recognised in the government department’s operating statement. Disclosure of this information by major class and by activity facilitates an assessment of activity costs and cost recoveries, and is therefore relevant to parliamentary decision making and enhances the discharge of accountability obligations. Even though a government department does not control such items, the effective and efficient administration of these items is an important role of the government department.

Taxes

15

It is unlikely that taxes, for example, income tax, will qualify as income of the agency responsible for their collection, for example, the Australian Taxation Office, or the central agency responsible for management of the Consolidated Revenue Fund, Trust Fund or other Fund, for example, Treasury. This is because the agency responsible for collecting taxes does not normally control the future economic benefits embodied in tax collections. Similarly, Treasury may be responsible for bank accounts into which tax collections are deposited, but until parliament has ‘appropriated funds’ for Treasury use or authorised the Treasury to make payments, the Treasury will not control those tax revenues.

16

Parliamentary appropriations made to enable the tax collection agency to perform its services are income of that agency. This is because the agency has the authority to deploy the appropriated funds for the achievement of its objectives and, consequently, controls the assets arising from the appropriation.

Transfer Payments

17

A government department does not recognise as income and expenses those amounts that the government department is responsible for transferring to eligible beneficiaries, consistent with legislation or other authority, but that the government department does not control. If these amounts were recognised as income on receipt by the government department and as expenses on payment by the government department, users could incorrectly assume that the government department controlled these amounts. Nevertheless, this Standard requires such amounts to be disclosed in the complete set of financial statements because that information may be relevant for understanding the government department’s financial performance, including assessments of accountability. Even though a government department does not control such items, their effective and efficient administration is an important role of the government department.

18

Consistent with a government department’s objectives and with legislation or other authority, amounts appropriated to government departments may include amounts to be transferred to third parties or recoupment of such amounts previously transferred by the government department. Such transfers may encompass payments for unemployment benefits, family allowances, age and invalid pensions, disaster relief, and grants and subsidies made to other governments or to other government or private sector entities.

19

Whether a government department recognises the amounts appropriated for transfer during the reporting period as income, and the amounts transferred during that reporting period as expenses, depends on whether the government department controls the assets to be transferred, and whether the amounts subsequently transferred constitute a reduction in the net assets of the government department.

20

Where amounts are transferred to eligible beneficiaries and the identity of the beneficiaries and the amounts to be transferred to them are determined by reference to legislation or other authority, it is unlikely that the government department controls the funds to be transferred. The government department is merely the agent responsible for the administration of the transfer process. As such, the government department does not benefit from the assets held for transfer, nor does it have the capacity to deny or regulate the access of eligible beneficiaries to the assets. Accordingly, the government department does not recognise assets and income in respect of amounts appropriated for transfer, nor expenses in respect of the amounts subsequently transferred.

21

Although transfers not controlled by a government department do not qualify for recognition in the financial statements, information about their nature and amount is relevant for understanding the government department’s financial performance.

22

Details of the broad categories of recipients and the amounts transferred to those recipients shall be disclosed in the government department’s complete set of financial statements.

23

In some cases it may not be clear whether the government department controls amounts to be transferred to eligible beneficiaries. For example, amounts may be appropriated to a government department for subsequent transfer, but the government department can exercise significant discretion in determining the amount or timing of payment, the identity of beneficiaries and the conditions under which the payments are to be made. In such cases, preparers and auditors use their judgement in deciding whether the government department controls the amounts to be transferred.

Accounting Basis

24

To facilitate the assessment of the costs incurred and the cost recoveries generated as a result of the government department’s activities, administered income, expenses, assets and liabilities are reported on the same basis adopted for the recognition of the elements of the financial statements.

Display of Information about Administered Items

25

The manner in which administered transactions are displayed in the financial statements of a government department will depend on the administrative arrangements adopted by the controlling government, and may therefore vary from jurisdiction to jurisdiction. For example, in some jurisdictions it may be appropriate for administered transactions to be displayed as a separate schedule to the operating statement and/or the statement of financial position. In other jurisdictions, a government department’s accountability for administered transactions may mean that it is appropriate for administered transactions to be displayed with, but clearly distinguishable from, the government department’s operating statement and/or statement of financial position.

Appendix A -- Comparison of AASB 1050 with AAS 29

This Appendix accompanies, but is not part of, AASB 1050.

This Standard reproduces the requirements relating to administered items contained in AAS 29, except that:

(a) paragraph 5.2.5 of AAS 29 encouraged disclosure of items collected or distributed on behalf of another entity or held in legal custody that are neither administered nor controlled. This Standard does not contain such an encouragement;

(b) in relation to transfer payments, paragraph 10.5.15 of AAS 29 noted that transfer payments not controlled by a government department do not qualify for recognition. However, the paragraph contemplated disclosure of the broad categories of recipients and the amounts transferred to those recipients. Paragraph 22 of this Standard requires such disclosures;

(c) paragraph 12.9.4 of AAS 29 encouraged the disclosure of information about administered assets and administered liabilities on an activity basis. This Standard does not contain such an encouragement; and

(d) paragraph 8 of this Standard requires the principles in AASB 1052 Disaggregated Disclosures to be applied in disclosing administered income and expenses reliably attributable to activities. AAS 29 did not include such a specific requirement.

The following table provides source references to paragraphs 7–25 of this Standard, most of which were derived from AAS 29. It is provided to facilitate an understanding of, and assist in the application of, the requirements in this Standard.

Paragraph in AASB 1050 | Relevant source paragraph/s in AAS 29 |

|---|---|

12.9 | |

New paragraph | |

12.9.1 | |

5.2.5 | |

12.9.2 | |

10.4.2 | |

6.3.11 | |

12.9.3 and last sentence of 6.3.11 | |

10.5.9 | |

First two sentences of paragraph 10.5.10 | |

6.3.12 | |

10.5.11 | |

10.5.12 | |

10.5.13 | |

10.5.15 | |

10.5.16 | |

12.9.6 | |

12.9.5 |

Appendix B -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusB1

Paragraphs 7, 8 and 22 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Compilation details

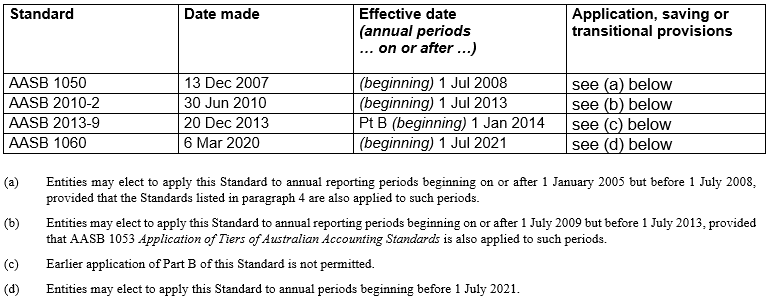

Accounting Standard AASB 1050 Administered Items (as amended)

Compilation details are not part of AASB 1050.

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 29 October 2021 by the staff of the Australian Accounting Standards Board (AASB).

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1050 (December 2007) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments