This Standard addresses the accounting by government departments and other government-related entities for contributions by owners, distributions to owners and the restructure of administrative arrangements. It also addresses the accounting for parliamentary appropriations received by government departments and the liabilities of government departments assumed by other entities.

Preamble

Pronouncement

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. Earlier application is permitted for annual reporting periods beginning on or after 1 January 2014 but before 1 July 2021. It incorporates relevant amendments made up to and including 6 March 2020.

Prepared on 21 July 2021 by the staff of the Australian Accounting Standards Board.

Compilation no. 4

Compilation date: 30 June 2021

Obtaining copies of Accounting Standards

Compiled versions of Standards, original Standards and amending Standards (see Compilation Details) are available on the AASB website: www.aasb.gov.au.

Australian Accounting Standards Board

PO Box 204

Collins Street West

Victoria 8007

AUSTRALIA

Phone: (03) 9617 7600

E-mail: [email protected]

Website: www.aasb.gov.au

Other enquiries

Phone: (03) 9617 7600

E-mail: [email protected]

Copyright

© Commonwealth of Australia 2021

This work is copyright, including the digital devices and links. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission. Requests and enquiries concerning reproduction and rights should be addressed to The National Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Victoria 8007.

Rubric

Australian Accounting Standard AASB 1004 Contributions (as amended) is set out in paragraphs 6 – 59 and Appendices A – B. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. AASB 1004 is to be read in the context of other Australian Accounting Standards, including AASB 1048 Interpretation of Standards, which identifies the Australian Accounting Interpretations, and AASB 1057 Application of Australian Accounting Standards. In the absence of explicit guidance, AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies.

Comparison with international pronouncements

AASB 1004 Contributions does not correspond directly with any specific IPSASB Standard or IFRS Standard.

AASB 1004 and IPSAS

Not-for-profit entities that comply with the requirements of AASB 1004 may not simultaneously be in compliance with the requirements of IPSAS 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) or IPSAS 40 Public Sector Combinations.

Both AASB 1004 and IPSAS 23 require subject transactions that meet the definition of contributions by owners to be recognised as equity transactions. The definitions of contributions by owners in the Standards are broadly consistent, however IPSAS 23 takes a more substance-over-form approach and does not address symmetry between a transferor and the transferee in relation to contributions by and distributions to owners.

Restructures of administrative arrangements (which require the transfer of a business) would typically meet the definition of an amalgamation under IPSAS 40. However, IPSAS 40 specifies measurement requirements, whereas AASB 1004 does not. AASB 1004 also treats the net transfer between the parties as a contribution by owners or distribution to owners, as applicable.

AASB 1004 and IFRS Standards

Not-for-profit entities that comply with the requirements of AASB 1004 may not simultaneously be in compliance with the requirements of IFRS Standards, which do not explicitly define contributions by owners. However, restructures of administrative arrangements are business combinations under common control, which are excluded from the scope of IFRS 3 Business Combinations.

Accounting Standard AASB 1004

The Australian Accounting Standards Board made Accounting Standard AASB 1004 Contributions under section 334 of the Corporations Act 2001 on 13 December 2007.

This compiled version of AASB 1004 applies to annual periods beginning on or after 1 July 2021. It incorporates relevant amendments contained in other AASB Standards made by the AASB up to and including 6 March 2020 (see Compilation Details).

Application

1‒5

[Deleted]

6

The following table identifies which paragraphs are applicable to each type of entity to which this Standard applies:

|

Type of entity to which the paragraph is applicable |

Content of paragraphs |

Para No. |

|

Government departments |

Parliamentary appropriations |

|

|

Liabilities of government departments assumed by other entities |

|

|

|

Contributions by owners and distributions to owners |

|

|

|

Restructure of administrative arrangements |

|

|

|

Other government controlled not-for-profit entities |

Restructure of administrative arrangements |

|

|

Local governments and whole of governments |

Contributions by owners and distributions to owners |

|

7

This Standard applies to annual reporting periods beginning on or after 1 July 2008.

[Note: For application dates of paragraphs changed or added by an amending Standard, see Compilation Details.]

8

This Standard may be applied to annual reporting periods beginning on or after 1 January 2005 but before 1 July 2008, provided there is early adoption for the same annual reporting period of the following pronouncements being issued at about the same time, as applicable:

(a) AASB 1049 Whole of Government and General Government Sector Financial Reporting;

(b) AASB 1050 Administered Items;

(c) AASB 1051 Land Under Roads;

(d) AASB 1052 Disaggregated Disclosures;

(e) AASB 2007-9 Amendments to Australian Accounting Standards arising from the Review of AASs 27, 29 and 31; and

(f) AASB Interpretation 1038 Contributions by Owners Made to Wholly-Owned Public Sector Entities.

9

[Deleted]

10

When applicable, this Standard, together with the Standards referred to in paragraph 8, supersede:

(a) AASB 1004 Contributions as notified in the Commonwealth of Australia Gazette No S 294, 22 July 2004;

(b) AAS 27 Financial Reporting by Local Governments, as amended;

(c) AAS 29 Financial Reporting by Government Departments, as amended; and

(d) AAS 31 Financial Reporting by Governments, as amended.

11‒31

[Deleted]

Parliamentary appropriations to government departments

Paragraph 32 of this Standard applies only to government departments.

32

Parliamentary appropriations over which a government department gains control during the reporting period shall be recognised as a direct adjustment to equity where the appropriation satisfies the definition of a contribution by owners.

33‒38

[Deleted]

Liabilities of government departments assumed by other entities

Paragraphs 39 to 43A of this Standard apply only to government departments.

39

A liability of a government department that is assumed by the government or other entity shall be accounted for as follows:

(a) on initial incurrence of the liability by the government department, the government department shall recognise a liability and an expense;

(b) on assumption of the liability by the government or other entity, the government department shall extinguish the liability and:

(i) when the assumption is not in the nature of a contribution by owners, the government department shall recognise income of an amount equivalent to the liability assumed; or

(ii) when the assumption of the liability is in the nature of a contribution by owners, the government department shall make a direct adjustment to equity of an amount equivalent to the liability assumed.

40

The obligation to make payments to employees in respect of long-service leave and other employee benefits may rest with the government, a central agency or other entity. However, the costs of long-service leave and other employee benefits are part of the cost of the goods and services provided by the government department for which those employees work. Employment contracts or employment arrangements may be such that a government or other entity, rather than the government department, directly incurs the obligation to settle liabilities that arise in respect of benefits of the government department’s employees. Alternatively, it may be that the government department initially incurs the obligation to settle such liabilities, and the government or other entity then assumes that obligation.

41

A government or other entity may initially incur, and then settle, obligations in respect of the wages, salaries and other costs of the employees of a government department during the reporting period. Similarly, other expenses of operating the government department during the reporting period, such as building occupancy expenses, may be incurred and settled by the government or other entity. In such cases, the government department does not recognise a liability when the expenses are initially incurred. Rather, the government department recognises income equivalent to the fair value of the employee services or other assets it receives, and recognises expenses of the same amount to reflect that the economic benefits represented by those employee services or other benefits have been consumed by the government department. For employee services, this normally occurs when the services are provided, but in some instances the costs of these services forms part of the cost of acquiring an asset.

42

When an employee transfers from one government department to another government department, the liability in respect of employee benefits accrued up to the transfer date is usually transferred to the transferee government department. In such cases, the transferor government department may make a payment to the transferee government department for the employee’s accrued benefits. When an employee transfers from one government department to another government department:

(a) the transferor government department extinguishes any liability for employee benefits recognised in respect of the employee, and recognises income equivalent to the liability extinguished. When a payment is made or is to be made by the transferor government department in consideration for the assumption of the liability by the transferee government department, the transferor government department extinguishes the liability and recognises a decrease in assets (cash) or an increase in liabilities (cash payable). When the payment is less than the total amount of the liability, the transferor government department recognises income equal to the amount of that shortfall; and

(b) the transferee government department recognises an expense and a liability in respect of any present obligations to pay accrued employee benefits in the future that are assumed as a consequence of the transfer. When a payment is made or is to be made to the transferee government department in consideration for the assumption of the liability, the transferee government department recognises the liability assumed and an increase in assets (cash or cash receivable). When the payment is less than the total amount of the liability for employee entitlements assumed, the transferee government department recognises an expense equal to the amount of that shortfall.

43

As noted in paragraphs 39 to 41, a government may initially incur or subsequently assume all obligations to make payments to employees of a government department in respect of long-service leave and other employee benefits. In such cases, the transfer of employees between government departments will not give rise to the need for the transferee government department to recognise expenses and liabilities or for the transferor government department to extinguish liabilities and recognise income as outlined in paragraph 42.

43A

A government department shall disclose liabilities that were assumed during the reporting period by the government or other entity.

44‒47

[Deleted]

Contributions by owners and distributions to owners of local governments, government departments and whole of governments

Paragraphs 48 to 53 of this Standard apply only to local governments, government departments and whole of governments.

48

Contributions by owners shall be recognised as a direct adjustment to equity when the contributed assets qualify for recognition.

49

Distributions to owners shall be recognised as a direct adjustment to equity when the associated reduction in assets, rendering of services or increase in liabilities qualifies for recognition.

50

It is important to distinguish contributions by owners from other contributions. It may be argued that contributions that are provided on the condition that they be expended on assets that increase the capacity of the entity to provide particular services should be classified as contributions of equity. However, such contributions would be contributions by owners, as defined in Appendix A to this Standard, only when the contributor establishes by way of the contribution a financial interest in the net assets of the entity that:

(a) conveys entitlement both to a financial return on the contribution and to distributions of any excess of assets over liabilities in the event of the entity being wound up; and/or

(b) can be sold, transferred or redeemed.

51

Contributions by owners are examples of non-reciprocal transfers. Examples of contributions by owners (and distributions to owners) are non-reciprocal transfers between a government department and the controlling government acting in its capacity as owner. Transactions with owners in their capacity as owners are not common in a local government context. A local government may on occasions receive contributions by owners, as defined in Appendix A to this Standard, such as investments in the capital of companies controlled by the governing body of the local government. Such contributions would need to be recognised as contributions of equity.

52

Contributions by owners can occur upon establishment of the entity or at a subsequent stage of the entity’s existence. Contributions by owners can be in the form of cash, nonmonetary assets such as property, plant and equipment, or the provision of services. In some instances, the contribution may result from the conversion of the entity’s liabilities into equity.

53

Reductions in equity as a result of distributions to owners (either dividends or returns of capital) can be in the form of a transfer of assets, a rendering of services or an increase in liabilities. Distributions from government departments to governments are made at the discretion of the government.

Restructure of administrative arrangements

Paragraphs 54 to 59 of this Standard apply only to government departments and other government controlled not-for-profit entities.

54

In relation to a restructure of administrative arrangements, a government controlled not-for-profit transferor entity shall recognise distributions to owners and a government controlled not-for-profit transferee entity shall recognise contributions by owners in respect of assets transferred.

55

In relation to a restructure of administrative arrangements, a government controlled not-for-profit transferor entity shall recognise contributions by owners and a government controlled not-for-profit transferee entity shall recognise distributions to owners in respect of liabilities transferred.

56

When both assets and liabilities are transferred as a consequence of a restructure of administrative arrangements, a government controlled not-for-profit transferor entity and a government controlled not-for-profit transferee entity shall recognise a net contribution by owners or distribution to owners, as applicable.

57

When activities are transferred as a consequence of a restructure of administrative arrangements, a government controlled not-for-profit transferee entity shall disclose the expenses and income attributable to the transferred activities for the reporting period, showing separately those expenses and items of income recognised by the transferor during the reporting period. If disclosure of this information would be impracticable, that fact shall be disclosed, together with an explanation of why this is the case.

58

For each material transfer, the assets and liabilities transferred as a consequence of a restructure of administrative arrangements during the reporting period shall be disclosed by class, and the counterparty transferor/transferee entity shall be identified. With respect to transfers that are individually immaterial, the assets and liabilities transferred shall be disclosed on an aggregate basis.

59

The disclosures required by paragraph 58 will assist users to identify the assets and liabilities recognised or derecognised as a result of a restructure of administrative arrangements separately from other assets and liabilities and to identify the transferor/transferee entity.

60‒68

[Deleted]

Appendix A -- Defined terms

This Appendix is an integral part of AASB 1004.

Contributions

A[1]

Non-reciprocal transfers to the entity.

Contributions by owners

A[2]

Future economic benefits that have been contributed to the entity by parties external to the entity, other than those which result in liabilities of the entity, that give rise to a financial interest in the net assets of the entity which:

(a) conveys entitlement both to distributions of future economic benefits by the entity during its life, such distributions being at the discretion of the ownership group or its representatives, and to distributions of any excess of assets over liabilities in the event of the entity being wound up; and/or

(b) can be sold, transferred or redeemed.

Non-reciprocal transfer

A[3]

A transfer in which the entity receives assets or services or has liabilities extinguished without directly giving approximately equal value in exchange to the other party or parties to the transfer.

Restructure of administrative arrangements

A[4]

The reallocation or reorganisation of assets, liabilities, activities and responsibilities amongst the entities that the government controls that occurs as a consequence of a rearrangement in the way in which activities and responsibilities as prescribed under legislation or other authority are allocated between the government’s controlled entities.

The scope of the requirements relating to restructures of administrative arrangements is limited to the transfer of a business (as defined in AASB 3 Business Combinations). The requirements do not apply to, for example, a transfer of an individual asset or a group of assets that is not a business.

Appendix B -- Australian simplified disclosures for Tier 2 entities

This appendix is an integral part of the Standard.

AusB1

Paragraphs 43A and 57–59 do not apply to entities preparing general purpose financial statements that apply AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities.

Compilation details

Accounting Standard AASB 1004 Contributions (as amended)

Compilation details are not part of AASB 1004.

This compiled Standard applies to annual reporting periods beginning on or after 1 July 2021. It takes into account amendments up to and including 6 March 2020 and was prepared on 21 July 2021 by the staff of the Australian Accounting Standards Board (AASB).

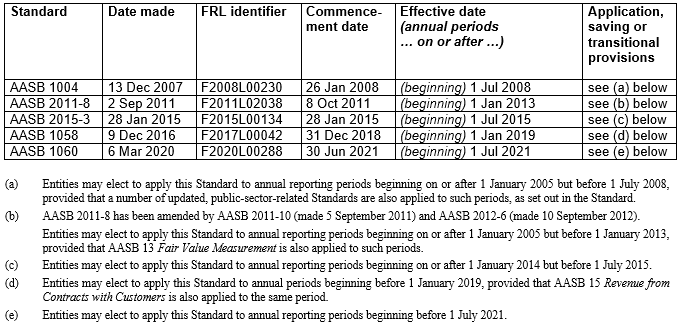

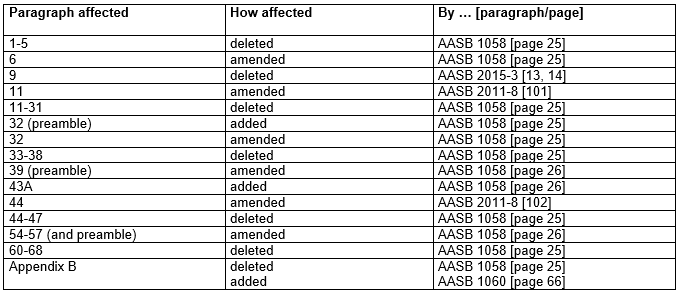

This compilation is not a separate Accounting Standard made by the AASB. Instead, it is a representation of AASB 1004 (December 2007) as amended by other Accounting Standards, which are listed in the table below.

Table of Standards

Table of amendments

Basis for Conclusions on AASB 1058

This Basis for Conclusions accompanies, but is not part of, AASB 1004. The Basis for Conclusions was originally published with AASB 1058 Income of Not-for-Profit Entities.

The Basis for Conclusions (relevant extracts only) is provided with this Standard as a linked PDF document. See AASB Extras at right.